21

Selecting an alliance partner must be done judiciously to avoid competing with a firm’s own customers or

partners, cannibalizing its own product offering, or unintentionally transferring proprietary information

and technology.

____________________________________________________________________________________

Smartphones outsold personal computers for the first time in the fourth quarter of 2010. The Apple

the smartphone market.

On February 11, 2011, Nokia’s CEO, Stephen Elop, announced an alliance with Microsoft to establish

a third major player in the intensely competitive smartphone market, currently dominated by Google and

Apple. Under the deal, Nokia will adopt Windows Phone 7 (WP7) as its principal smartphone operating

system, replacing its own software, which has been losing market share. Nokia and Microsoft are betting

Under the agreement with Microsoft, WP7 becomes Nokia’s primary smartphone platform; Nokia also

agreed to help introduce WP7-powered smartphones in new consumer and business markets throughout

the world. The two firms will jointly market their products and integrate their mobile application online

stores such that Microsoft’s Marketplace (applications and media store) will absorb Nokia’s current

online applications and content store (Ovi). Nokia phones will use Microsoft’s Bing search engine, Zune

developers but that has sold relatively poorly since its introduction in late 2010. With the phase-out of its

discontinued Symbian operating system over a period of years, Nokia will be able to reduce substantially

its own research and development and marketing budgets. Microsoft will also benefit from Nokia’s

extensive intellectual property portfolio in the mobile market to strengthen the WP7 system. For

Microsoft, the deal represents a major opportunity to boost lagging sales in the mobile phone market and

technologies, such as Google’s Android operating system. For example, after failing to deliver mobile

phone technology that would compete with Apple’s and Google’s innovative systems, Taiwanese handset

manufacturer HTC lost interest in manufacturing smartphones based on what was then known as the

Windows Mobile operating system and now makes many different Android phone models in addition to

devices powered by WP7. Even though Microsoft’s Mobility software was substantially revamped and

22

the likes of those producing handsets powered by the Google operating system, Blackberry, and Apple

with only the Windows Phone 7–powered phone. The Mobile Phones operation would continue to

develop phones for Nokia’s mass market. The mass market feature–phone business represented Nokia’s

core business, in which the firm would produce large volumes of phones for the mass market

increase market penetration sharply. Android may be vulnerable due to a number of problems: platform

fragmentation, inconsistent updates and versions across devices, and the operating system’s becoming

slower as it is called on to support more applications. WP7, at this time, has none of these problems. If

customers become frustrated with Android, WP7 could gain significant share. As always, time will tell.

Discussion Questions

1. Conduct an external analysis of the smartphone market place (see Chapter 4).

Answer: Smartphones are showing signs of replacing PCs in some applications, as they

2. Conduct an internal analysis of Nokia and Microsoft (see Chapter 4).

Answer: Both companies have demonstrated substantial core capabilities: Microsoft in

operating system software and Nokia in making exceptionally high quality hardware.

3. What alternatives to a partnership did Nokia and Microsoft have? Why was a partnership

selected as the means of implementing the firm strategy to enter the smartphone market?

Answer: Microsoft could have acquired Nokia. With its lack of success in a prior partnership

in its effort to penetrate the smartphone marketplace, gaining control may have been an

appropriate strategy. In partnerships in which neither partner products or services are to be

4. Who do you believe benefitted most from the partnership (Microsoft or Nokia) and why?

Answer: While both partners need the other, Microsoft would seem to be the primary

beneficiary if the partnership is successful. On the surface, success in the smartphone market

General Electric and Comcast Join Forces

____________________________________________________________________________________

Key Points

Joint ventures are sometimes created if a business cannot be sold outright.

Such JVs are viewed as a way of improving a firm’s operations enabling the parent to exit the business

eventually at a higher value.

In an effort to shore up its big finance business, severely weakened during the 2008 financial crisis, and

to focus more on its manufacturing and infrastructure operations, General Electric (GE) sought to sell its

media and entertainment business, NBCUniversal. GE’s decision to sell also reflected the deteriorating

state of the broadcast television industry and a desire to exit a business that never quite fit with its

NBCUniversal was profitable in 2009, it was expected to go into the red in subsequent years.

Unable to find a buyer for the entire business at what GE believed was a reasonable price, GE sought

other options, including combining the operation with another media business. After extended

discussions, GE and Comcast announced a deal on December 2, 2009, to form a joint venture consisting

of NBCUniversal and selected Comcast assets. Comcast is primarily a cable company and provider of

programming content, with 24.3 million cable customers, 16.1 million high-speed Internet customers, and

7.8 million voice customers. Comcast hopes to diversify its holdings as it faces encroaching threats from

online video and more aggressive competition from satellite and phone companies that offer subscription

Comcast’s strategy is to integrate vertically by owning the content it distributes through its cable

operations. Previous attempts to do this, such as AOL’s acquisition of Time Warner in 2001, have ended

in failure, largely because the cultures of the two firms did not mesh. Some media companies have

merged successfully —for example, Time Warner’s merger with Turner Broadcasting. Having learned

from AOL’s rush to achieve synergy, Comcast is allowing the NBCUniversal JV to operate independent

The announcement raised significant concerns within the media and entertainment industry about the

potential for limiting access to both content and distribution by increasing industry concentration. After

receiving significant concessions, regulators approved the creation of the joint venture media giant on

January 17, 2011. The U.S. Federal Communications Commission and the Department of Justice required

Comcast and NBCUniversal to relinquish voting rights and board representation to Hulu, although they

contributed assets to determine ownership distribution, and finally determining how GE would be

compensated. The joint venture transaction based on the value of the assets contributed by both parties

was valued at $37.25 billion, consisting of GE’s contribution of NBCUniversal, valued at $30 billion, and

Comcast’s contribution of cable network assets valued at $7.25 billion. The ownership interests were

determined based on the value of the contributed assets and cash payments made to GE as described in

cash, Comcast received a 51% interest in the NBCUniversal JV.

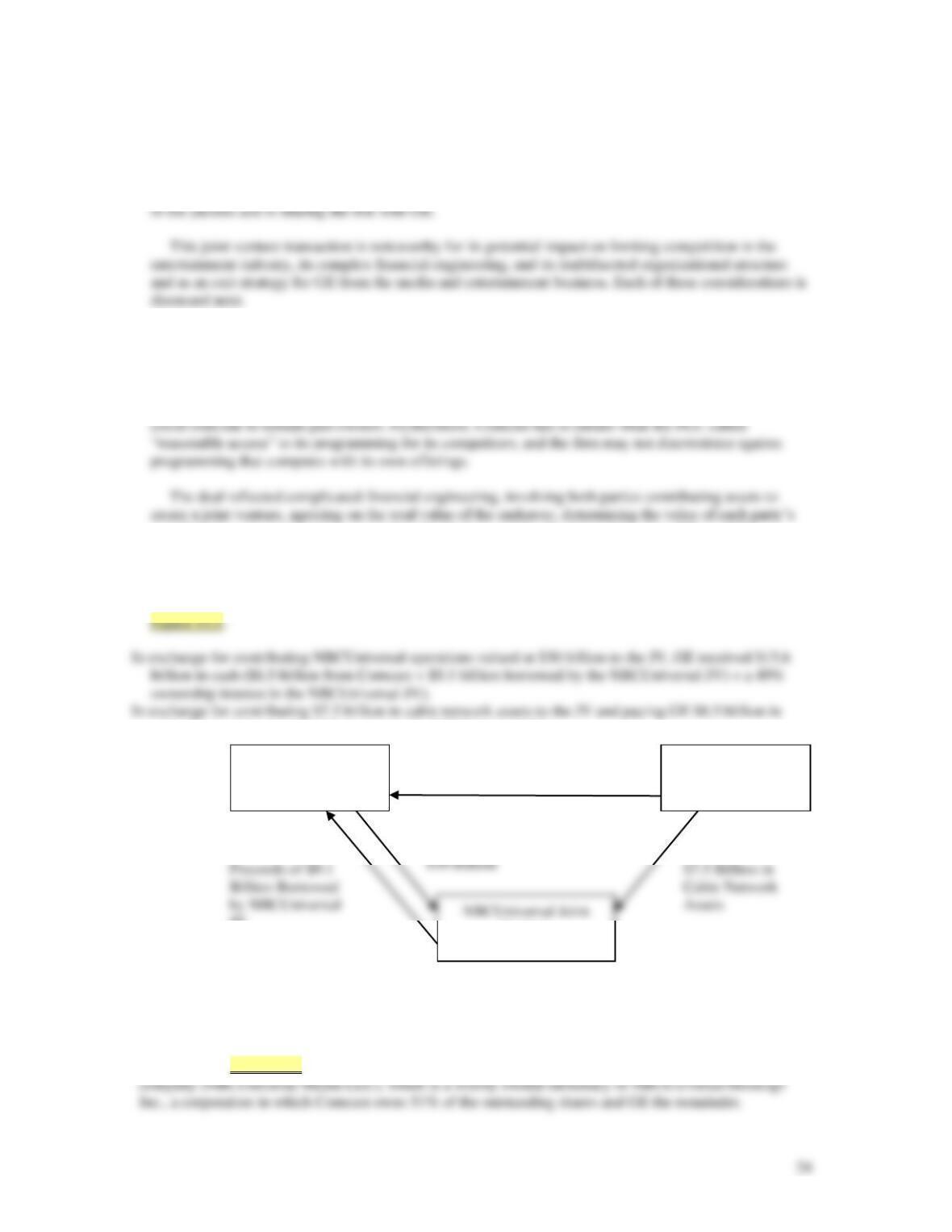

Figure 15.1

NBCUniversal Joint Venture at Closing.

Organizationally, the two parties own NBCUniversal indirectly through their ownership in a holding

company (see Figure 15.2). As part of the deal, NBCUniversal Inc. was converted to a limited liability

General Electric

Comcast

Venture

$6.5 Billion in Cash

NBCUniversal

Operations Valued at

$30 Billion

JV

25

NBCUniversal Holdings is the sole member (owner) in NBCUniversal Media LLC. By having the right to

designate the majority of the board members of NBCUniversal Holdings, Comcast effectively controls the

holding company and, in turn, NBCUniversal Media LLC. To maintain its status as a pass–through

organization for tax purposes, NBCUniversal Media makes quarterly distributions to the holding company,

120% of the “public market trading value” of NBCUniversal Holding, to be determined by an appraisal if

the business is not yet publicly traded, less 50% of the “public market trading value” greater than $28.4

In 2011, NBCUniversal Media had revenue of $19.3 billion, earnings before interest and taxes of $2.3

billion, and net income of $1.7 billion. While the financial outlook for the business has stabilized, the deal

continues to be subject to the criticism that there is little overlap between Comcast and NBCUniversal

Media’s businesses to provide significant cost savings. Moreover, big media deals have a poor track record,

as illustrated by the AOL Time Warner debacle. Comcast is placing a big bet that it will be able to combine

content and distribution successfully and to grow the value of the consolidated businesses. In contrast,

General Electric may be more intent on exercising its option to sell its interests unless the fortunes of

NBCUniversal Media improve dramatically in the coming years.

Discussion Questions

NBCUniversal

Holdings, Inc.

NBCUniversal

49% Ownership

Interest

51% Ownership

Interest

26

1. Speculate as to why GE may have found it difficult to manage NBC Universal. Be

specific.

Answer: GE is a highly diversified organization in infrastructure, manufacturing, financial

services, and media businesses. The lack of relatedness makes it exceedingly difficult for the

2. Why was the NBC Universal joint venture used to borrow the $9.1 billion paid to GE?

How might this impact the ongoing operation of NBCUniversal? What are the trade-offs the

partners are making in agreeing to fund a portion of the purchase price through

NBCUniversal?

Answer: By having NBCUniversal borrow the $9.1 billion, Comcast and GE may be able to

protect themselves from its creditors if the firm goes into bankruptcy because such loans are

backed by the NBCUniversal’s assets and cash flow. Furthermore, Comcast and GE are

3. Speculate as to the potential circumstances in which either Comcast or GE would be

likely to exercise their call or put options? Which party do you believe is likely to exercise

their options first and why?

4. What are the likely challenges Comcast and GE will have in integrating the various

businesses that comprise the joint venture? Be specific.

Answer: The challenges in integrating the two businesses are likely to be similar to those faced

5. Why did Comcast and GE choose to operate NBCUniversal as a limited liability

company rather than a corporation?

6. Speculate as to why the partners chose to operate NBCUniversal Media through a

holding company.

27

Answer: The holding company arrangement allows the two partners to indirectly own

Exxon-Mobil and Russia’s Rosneft Create Artic Oil and Gas Exploration Joint Venture

________________________________________________________________

Key Points

Contractual commitments in cross-border alliances are effective only to the extent they are enforced by

each country’s legal system.

The success of most alliances ultimately depends on the extent to which each partner needs the capabilities

and resources of the other.

______________________________________________________________________________

Exxon-Mobil (Exxon) finalized an agreement with the government-owned Russian oil and gas giant

Rosneft on April 16, 2012, to create a joint venture to explore for oil and gas in three designated areas in

the Russian portion of the Artic Ocean known as the Kara Sea. The agreement superseded a similar but

failed agreement with British Petroleum (BP) earlier in the year. Rosneft’s attempt to strike a similar pact

with BP in 2011 fell apart because the British company had a joint venture with a separate group of private

Russian investors, which blocked the Rosneft deal in an international court. While BP had planned to swap

stock, Exxon agreed to give Rosneft assets elsewhere in the world, including some that Exxon owns in the

deep waters of the Gulf of Mexico and in Texas. Future investments could total tens of billions of dollars.

The final agreement was contingent on Russia’s reducing taxes imposed on oil and gas companies.

The U.S. Geological Survey estimates that the Artic holds one–fifth of the world’s undiscovered,

recoverable oil and natural gas. The Kara Sea has an estimated 36 billion barrels of recoverable oil

reserves. Total oil and gas reserves are estimated to be 110 billion barrels of oil equivalent, four times

Exxon’s proven worldwide reserves. Drilling is expected to start in 2015, with Exxon shouldering most of

the costs. In exchange for access to these Rosneft properties, the agreement gives Rosneft an option to

invest in certain U.S. properties. Rosneft will own two-thirds and Exxon the remainder of the joint venture.

The initial commitment by the two companies is to invest $3.2 billion in exploration in the Kara Sea.

As a world leader in Artic exploration, Exxon is willing to share its expertise with Rosneft, as well as to

transfer technology, in exchange for access to Russia’s Artic region. The Russians are particularly

interested in learning the latest techniques employed in hydraulic fracturing (so–called “fracking”) of

The Russian government had long demanded reciprocity as part of any deal. This required that in

exchange for any ownership in Russian assets, the Russian partner should have the opportunity to invest in

assets owned by the other partner. The value of the assets Rosneft would own in the United States would be

in proportion to those Exxon would own in Russia. The agreement is risky, in view of Russia’s history of

reneging on deals with Western oil companies. For example, in 2006, it compelled Royal Dutch Shell to

sell 50% of a Sakhalin offshore property to state-owned Gazprom after Shell had spent more than $20

billion of its own money and that of other investors to build the project’s infrastructure.

British Petroleum and Russia’s Rosneft Swap Shares

Extending its already close ties with Russia, British Petroleum PLC announced an agreement to exchange

shares with Russia’s largest oil company, OAO Rosneft, on January 14, 2011. Rosneft is 75% owned by the

Russian government. BP and Rosneft also announced the formation of a JV to develop three massive

offshore exploration blocks that Rosneft owns in northern Russia. The two firms said they will jointly

Cameron, and Russia’s prime minister, Vladimir Putin. Russia holds one-fifth of the world’s proven

reserves of natural gas, and, by some estimates, the South Kara Sea contains some of the largest reserves of

oil and gas in the world.

The deal comes in the wake of BP’s sale of assets to raise funds to cover the costs of the Gulf of Mexico

oil spill in mid-2010. Such costs are expected to eventually total $40 billion. Rosneft, which had announced

The share exchange gives Rosneft a 5% interest in BP’s voting shares, making it BP’s single largest

shareholder. In return, BP receives a 9.5% ownership stake in Rosneft. Each stake is valued at about $7.8

billion. Both firms agreed to hold each other’s equity for at least two years before selling any stock. BP’s

shares currently pay a dividend about twice that of Rosneft’s. BP and Rosneft have stated publicly that they

believe investors have significantly undervalued their firms. The Russian government has a particularly

However, the terms of the share exchange imply a market capitalization for Rosneft of about $81 billion.

The transaction represents the first time there has been a cross-shareholding between major international

oil firms and a major government-owned national oil company. Unlike more conventional oil and gas JVs,

the Rosneft JV will not own the oil leases but merely the right to develop them. This structure is similar to

Russian oil company Gazrpom’s agreement with France’s Total SA and Norway’s Statoil for the

System and the London Stock Exchange. With the shares priced at $7.55 each, the offering raised about

$10.7 billion. Most of the proceeds went to the Russian government. BP began its relationship with Rosneft

by buying $1 billion in shares in the firm’s initial public offering, equivalent to 1.3%. Thus, the recent

agreement brings BP’s ownership interest in Rosneft to 10.8%.

Previous attempts to invest in Russia and to create partnerships between Russian state oil companies and

29

development to state-owned Gazprom. BP and Gazprom signed a global joint venture in 2007 in which

each was to contribute assets valued at $1.5 billion, but it was later dissolved due to disagreements between

BP and large Russian investors. TNK–BP, BP’s 50 percent–owned JV with a group of Russian billionaire

business people, has also had a troubled history. The JV that contributes a quarter of BP’s global

production and nearly a fifth of its reserves was rocked by a shareholder dispute in 2008 that cost BP some

Discussion Questions:

1. Speculate as to the purpose of the share swap between BP and Resnoft.

Answer: The overarching purpose of the exchange of shares between the two firms is to align

their interests and objectives, communicate to public investors the mutual confidence of both

firms, and to create synergies that will enhance the value of both firms’ shares. It is hoped that

2. What is the purpose of the 2-year lockup period during which neither partner can sell its

stock? How might the lock–up period impact the value of each firm’s holdings?

Answer: Since it is likely that it will take at least several years to tap the reserves believed to

be in the South Kara Sea, the lock-up period forces both parties to remain focused long

3. Would you expect the share exchange to be dilutive to BP shareholders in the short-run? In

the long-run. Explain your answer.

Answer: The dividend paid on BP shares is twice that paid on Rosneft common shares and the

4. Why would you expect the publicly traded Rosneft shares not to reflect the true value of the

firm?

30

5. How would you estimate the market capitalization for Rosneft based on the terms of the share

exchange? Show your work.

Answer: A share exchange ratio is defined as the offer price expressed as a market value

(MV) or price per share for a target firm divided by the acquiring firm’s current market value

6. How can BP best protect their interests in the JV with Rosneft in the highly uncertain political

and economic environment of Russia?

Answer: While the JV agreement can specify the rights of each party including if the JV is

SABMiller in Joint Venture with Molson Coors

On October 10, 2007, SABMiller (SAB) and Molson Coors (Coors) agreed to combine their U.S. brewing

operations into a joint venture corporation. The stated objective was to create a rival capable of competing

with Anheuser-Busch, the maker of Budweiser beer. SAB and Coors, the second and third largest

breweries, respectively, in the United States in terms of market share, have equal voting rights in the newly

formed entity. Each firm has five representatives on the board. In terms of ownership, SAB, the larger of

the two in terms of sales and profits, has a 58-percent stake and Coors a 42-percent position. The combined

operation, named MillerCoors, has about a 30 percent market share versus Anheuser’s 48 percent. Leo

Kiely, chief executive at Coors, became the chief executive officer of MillerCoors and Tom Long, head of

the SAB business in the United States, became the president and chief commercial officer. Peter Coors,

vice chairman of Coors, was tapped as the chairman and Graham Mackey, SAB’s chief executive officer,

the vice chairman of MillerCoors. Both Coors and SAB continue to operate separate global businesses.

From its roots in South Africa, the former SAB PLC grew rapidly over the previous decade by

expanding into fast growing economies such as China, Eastern Europe, and Latin America. SAB acquired

Miller Brewing Company in 2002, but the U.S. business failed to gain significant market share in

competing with Anheuser-Busch’s pervasive brand awareness and distribution strength. Molson Coors was

formed by the 2005 merger of Colorado’s Adolph Coors Co. and Canada’s Molson Inc., both family–

controlled companies. The families were unwilling to sell their entire companies to another firm. The JV

allows them to keep some control. Molson Coors, with dual headquarters in Montreal and Denver, has

major operations in Canada and Britain that would remain independent of SABMiller. Reflecting its larger

market share, brand recognition, and negotiating clout with distributors, Anheuser-Busch has operating

profit margins of 23 percent, double SAB’s or Coors’s margins. SAB is larger in terms of both revenue and

profit than Coors.

31

The major U.S. breweries have been experiencing growing competition from wine, specialty beers,

spirits, and imported beers. Spirits companies have raised the pressure on beer giants to merge by rolling

out sweet cocktails and other drinks to lure younger consumers. Premixed bottled drinks such as Smirnoff

Ice have seen sales triple in the last decade. The U.S. beer market is largely mature, with consumption

easier to negotiate for better placement for its ads and compete more effectively for ad rights to major

sporting events. The two firms are also geographically complementary. Miller is strong in the Midwest,

while Coors has large market share in the West.

Immediately following the joint venture announcement, Anheuser-Busch’s CEO August A. Busch IV

said in a message to employees that the brewer must capitalize on the significant transition confusion he

predicted would occur when Miller and Molson Coors blend their U.S. operations. Such confusion, he

predicted, would create great concern within the SABMiller/Coors field sales and wholesale organizations,

as people attempt to determine if they will have a role in this new structure.

Discussion Questions:

1. What tactics do you think Anheuser might employ to exploit the predicted confusion during

the integration of the SABMiller and Coors operations?

Answer: Following the announcement of a merger or joint venture, employees of the

organizations involved are likely to be uncertain about their roles in the future of the

2. How did the combination of the U.S. operations of SABMiller and MolsonCoors meet the

needs of the two parties? Why was a JV viewed as preferable to a merger of the two firm’s

global operations?

Neither SAB nor Coors were particularly profitable in the U.S. and were threatened with

declining market share in an increasingly mature market for their products. However, with