21

Answer: The form of payment was cash, due to its attractiveness to Heinz’s public shareholders. The use of

cash is common in these types of deals. The form of acquisition was the purchase of common stock from

2. How was ownership transferred in this deal? Speculate as to why this structure may have been used?

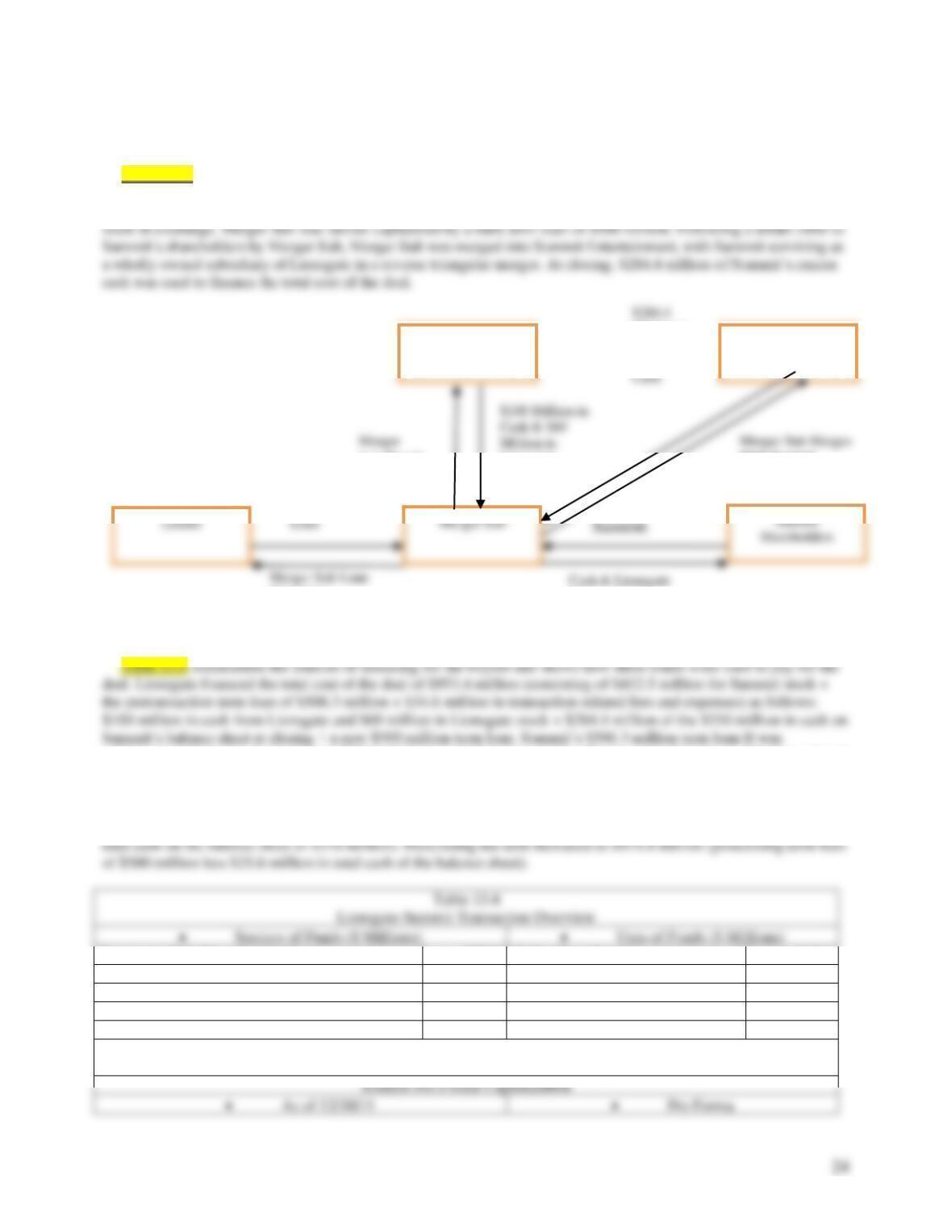

Answer: The deal structure involved a reverse triangular merger in which Heinz was merged into a wholly

owned subsidiary of Parent, with Heinz surviving. This preserves the Heinz brand name and results in a

holding company structure insulating 3G and Berkshire from Heinz liabilities in the event of bankruptcy. The

use of a subsidiary merger to transfer ownership from the Heinz’s public shareholders to the Parent may also

3. Describe the motivation for Berkshire and 3G to buy Heinz.

4. How will the investors be able to recover the 20% purchase price premium?

5. Do you believe that Heinz is a good candidate for a leveraged buyout? Explain your answer.

Answer: Yes. In the food manufacturing business for 120 years with a widely recognizable brand, the firm has

6. What do you believe was the purpose of the $1.5 billion senior secured revolving loan facility, and the $2.1

billion second lien bridge loan facility as part of the deal financing package?

7. Why do you believe Berkshire Hathaway wanted to receive preferred rather than common stock in exchange

22

for its investing $8 billion? Be specific.

Answer: The preferred stock has a $8 billion liquidation preference (i.e., assurance that holders are paid before

common shareholders in the event of liquidation), pays and accrues a 9% dividend (a rate well above

dividends decides to pay out its shareholders, the money will have been taxed three times.

INSIDE M&A: VERIZON FINANCES ITS $130 BILLION BUYOUT OF

VODAFONE’S STAKE IN VERIZON WIRELESS

Key Points

• The timing of buyouts is influenced heavily by equity and credit market conditions.

• To close deals, interim or “bridge financing” often is required and replaced with longer–term or “permanent

financing.”

• How deals are financed can impact a firm’s investment strategy long after the deal is completed.

_____________________________________________________________________________________

In a deal that has been in the making for almost a decade, Verizon Communications agreed to buy British–based

wireless carrier Vodafone’s 45% ownership stake in the Verizon Wireless joint venture corporation for $130 billion.

Formed in 2000, the joint venture serves more than 100 million customers in the United States.

Announced on September 2, 2013, the deal marked the crowning event in the careers of Vittorio Colao and Lowell

McAdam, the chief executives of Vodafone and Verizon, respectively. The agreement succeeded in rebuilding relations

between the two firms that had long been strained by clashes about the size of the dividend paid by the JV, matters of

strategy, and who would eventually achieve full ownership.

While Verizon sees growth in the U.S. wireless market it is due more to the potential growth in the car or home

security markets. While smartphone and cellphone growth may have plateaued, the growth in tablet computers is not

likely to drive demand for wireless communication since 90% of tablets sold connect only to Wi-Fi rather than cellular

wireless networks. For Vodafone, the deal leaves the British firm flush with cash to repay debt, reinvest in its

operations, and to buy competitors in Europe and in emerging markets.

The total consideration (purchase price) of $130 billion, consisted of $58.9 billion of cash, $60.2 billion of common

stock issued directly to Vodafone shareholders, $5 billion of notes to Vodafone, the sale of a minority stake in Omnitel

to Vodafone for $3.5 billion, and other net consideration of $2.4 billion (consisting of specific assets transferred

between Verizon and Vodafone). The price paid is equal to Verizon’s market value, enormous by most metrics. The

Verizon buyout of Vodafone was the third–largest corporate acquisition after Vodafone’s $203 billion (enterprise value)

takeover of German cell phone operator Mannesmann in 2000 and the $182 billion (enterprise value) merger of AOL

and Time Warner in 2001.

The timing of the deal reflects the near record low interest rate environment and the strength of Verizon’s own

stock. A higher Verizon share price meant that it would have to issue fewer new shares limiting the potentially dilutive

impact on the firm’s current shareholders. Another major issue was making sure the debt markets could absorb the

sheer amount of new Verizon debt without sending interest rates spiraling upward. The huge increase in Verizon’s

leverage was sure to catch the eye of credit rating agencies charged with evaluating the likelihood that borrowers could

repay their debt on a timely basis. While Verizon’s rating was reduced, it was only one notch from what it had been to

“investment grade,” rating agency jargon for ok for investors to buy.

Verizon hired two banks, JPMorgan Chase and Morgan Stanley, to raise $61 billion in debt to finance the cash

portion of the deal. The $61 billion raised exceeded the cash portion of the total consideration by $2.1 billion to leave

Verizon with a positive yearend cash balance. As lead banks, the two banks joined in a “syndicate” with Bank of

6.55%. These yields compared to the average BBB-rated industrial bond of 4.16% at the time and BBB bonds for

telecommunications companies averaging 4.34%.

The addition of a massive new debt load on Verizon’s books may tie the company’s hands in making major

investments for some time as its priority during the next several years will be reducing its leverage as quickly as

possible. It is likely to limit the firm’s ability to finance additional deals at least in the short-run and maybe longer if

the U.S. wireless market slows and smaller rivals compete more aggressively on price, as these factors erode the firm’s

cash flow.

Hollywood’s Biggest Independent Studios Combine in a Leveraged Buyout

Key Points

LBOs allow buyouts using relatively little cash and often rely heavily on the target firm’s assets to finance the

transaction.

Private equity investors often “cash out” of their investments by selling to a strategic buyer.

______________________________________________________________________________

The Lionsgate-Summit tie-up represented the culmination of more than four years of intermittent discussions between

the two firms. The number of studios making and releasing movies has been shrinking amid falling DVD sales and

was not until early 2012 that the two sides could reach agreement. The time was ripe because Summit’s investors were

looking for a way to cash in on the success of the firm’s Twilight movies series. Consisting of four films, this series had

grossed $2.5 billion worldwide. On February 2, 2012, Lionsgate announced that it had reached an agreement to acquire

Summit Entertainment by paying Summit shareholders $412.5 million in cash and stock for all of their outstanding

shares and assumed debt of $506.3 million. According to the merger agreement, Lionsgate would provide

Lionsgate is a diversified film and television production and distribution company, with a film library of 13,000

titles. The firm’s major distribution channels include home entertainment and prepackaged media (DVDs); digital

distribution (on-demand TV) and pay TV (premium network programming). Summit, also a producer and distributor of

film and TV content, has a less consistent track record in realizing successful releases, with the Twilight “franchise” its

primary success. However, Summit does have strong international licensing operations, with arrangements in the

Lionsgate as a market leader for young adult audiences. The combination also results in cost and revenue synergies,

more diversified cash flow streams, and greater access to international distribution channels.

Figure 13.3 illustrates the subsidiary structure for completing the buyout of Summit Entertainment LLC. As is

typical of such transactions, Lionsgate created a merger subsidiary (Merger Sub) and funded the subsidiary with its

equity contribution of $100 million in cash and $69 million in Lionsgate stock, receiving 100% of the subsidiary’s

Figure 13.3

Lionsgate-Summit Legal and Financing Structure.

refinanced with the new term loan for $500 million as part of the transaction. The new term loan is an obligation of and

is secured by the assets of Summit and its subsidiaries. It also is secured by a loan guarantee provided by Merger Sub,

created by Lionsgate to consummate the transaction. The guarantee is secured by the equity in Summit held by Merger

Sub. Lionsgate anticipates paying off the term loan well in advance of its 2016 maturity date out of future cash flows

from new movie releases. Summit’s pretransaction net debt was $196.3 million (pretransaction term loan of $506.3 less

Lionsgate Cash Consideration1

100.0

Seller Consideration

412.5

Lionsgate Stock Consideration2

69.0

Repay Term Loan

506.3

Summit Cash on Balance Sheet

284.4

Fees and expenses

34.6

New Term Loan

500.0

Total

953.4

953.4

1 Includes $55 million of Lionsgate cash and $45 million of convertible bond proceeds.

2 Includes $20 million of stock consideration to be issued to Summit sellers 60 days after closing.

Summit Pro Forma Capitalization

Lionsgate

Entertainment

Merger Sub

Summit

Entertainment

Summit

Shares

$500 Million

Sub Stock

Lionsgate

With Summit

Guarantee

Million in

Excess

Summit

Cash

25

$ Millions

Adjustment ($ Millions)

$ Millions

Cash3

310

(284.4)

25.6

Revolver ($200 million)

Prior Term Loan B Due 9/2016

(506.3)

New Term Loan B Due 9/2016

0.0

Total Debt

3 Total cash balance prior to the transaction announcement. $284 million is excess Summit cash used by Lionsgate to

finance a portion of the deal. The remaining $25.6 million is cash needed to meet working capital requirements.

4 Revolver commitments terminated for the acquisition.

5 Consists of $100 million in cash from Lionsgate and $69 million in Lionsgate stock.

Source: Lionsgate 8K filing with the Securities and Exchange Commission on 2/1/2012.

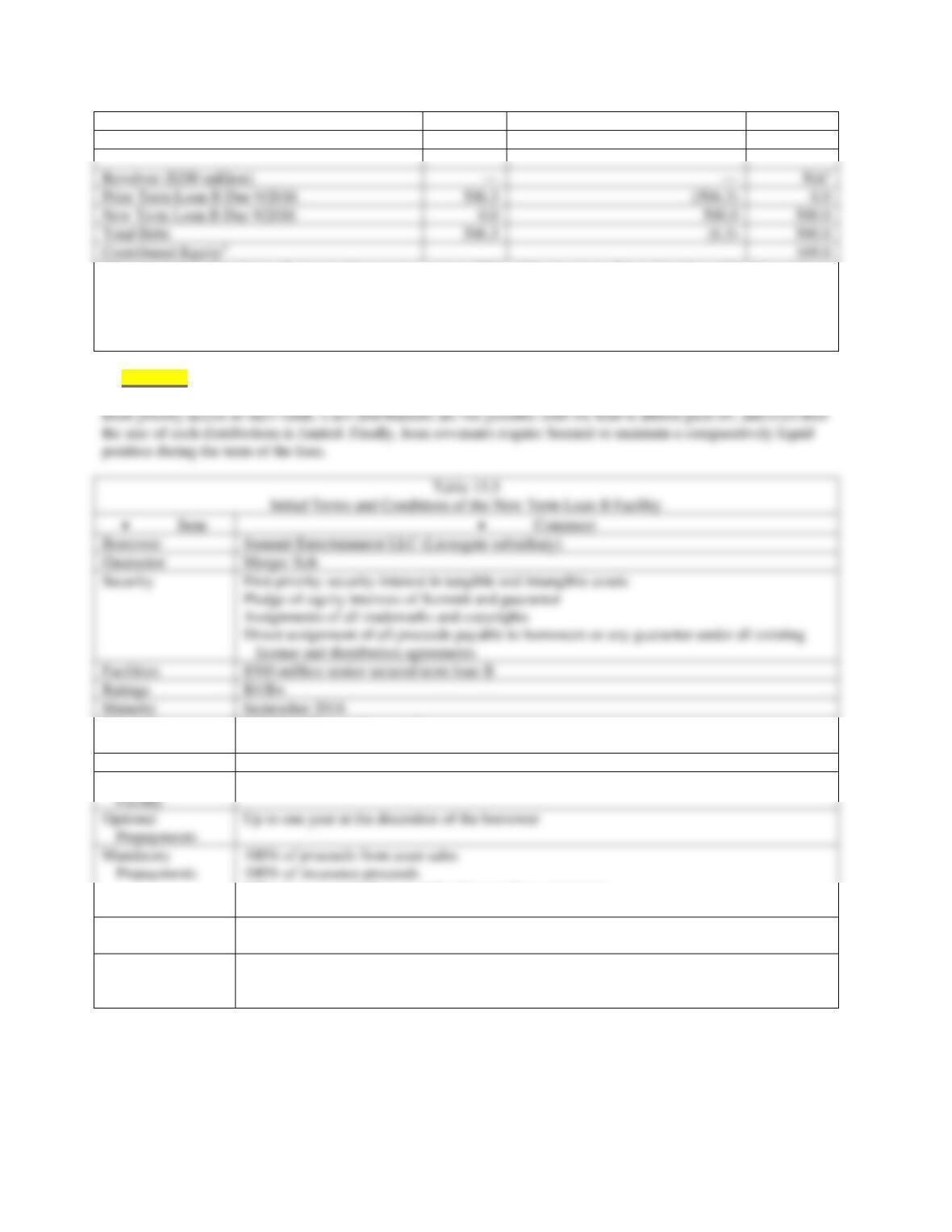

Table 13.5 presents the key features of the new term loan B facility. Note how Summit’s assets are used as collateral

to secure the loan. In addition, the lender has first priority on the proceeds from certain types of transactions, giving

Borrower

Summit Entertainment LLC (Lionsgate subsidiary)

Guarantor

Merger Sub

Facilities

$500 million senior secured term loan B

Ratings

B1/B+

Maturity

September 2016

Mandatory

Amortization

$13.75 million, paid quarterly

Pricing

To be determined

Incremental

Facility

None

Optional

Prepayments

Up to one year at the discretion of the borrower

50% of excess cash flow as defined in purchase agreement

Excess over mandatory maximum cash balance allowance

Permitted

Distributions

No distributions before loan facility is 75% amortized

Only distributions of up to $25 million allowed once loan is 75% amortized

Financial

Maintenance

Covenants

Fixed charge coverage ratio of 1.25 to 1

Minimum liquidity ratio of at least 1.1 to 1

Discussion Questions

1. What about Lionsgate’s acquisition of Summit indicates that this transaction should be characterized as a

leveraged buyout? How does Lionsgate use Summit’s assets to help finance the deal? Be specific.

26

Answer: LBOs are characterized by a substantial increase in a firm’s post-LBO debt-to–equity ratio (a

common measure of leverage), usually as a result of the substantial increase in borrowing to purchase stock

held by its pre-buyout private or public shareholders. However, in some instances, a firm’s leverage increases

even though there is no significant increase in borrowing. This may result from the way in which the target

firm’s assets are used to finance the buyout. For example, the investor group or firm initiating the takeover

.

2. How are $34.6 million in fees and expenses associated with the transaction paid for? Be specific.

3. Speculate as to why Lionsgate refinanced as part of the transaction the existing Summit Term Loan B due in

2016 that had been borrowed in the early 2000s.

4. Do you believe that Summit is a good candidate for a leveraged buyout? Explain your answer.

5. Why is Summit Entertainment organized as a limited liability company?

6. Why did Lionsgate make an equity contribution in the form of cash and stock to the Merger Sub rather than

making the cash portion of the contributed capital in the form of a loan?

TXU Goes Private in the Largest Private Equity Transaction in History—The Dark Side of Leverage

Key Points

The 2007/2008 financial crisis left many LBOs excessively leveraged.

As structured, the TXU buyout (now Energy Future Holdings) left no margin for error.

Excessive leverage severely limits the firm’s future financial options.

as 70% to 80% of their value. The other $8 billion used to finance the deal came from the private equity investors,

banks, and large institutional investors. They, too, have suffered huge losses. Having met its obligations to date, the

firm faces a $20 billion debt repayment coming due in 2014.

Wall Street banks were competing in 2007 to make loans to buyout firms on easier terms, with the banks also

investing their own funds in the deal. The allure to the banks was the prospect of dividing up as much as $1.1 billion in

The financial sponsor group, consisting of Kohlberg Kravis Roberts & Co, Texas Pacific Group, and Goldman

Sachs, created a shell corporation, referred to as Merger Sub Parent, and its wholly owned subsidiary Merger Sub. TXU

was merged into Merger Sub, with Merger Sub surviving. Each outstanding share of TXU common stock was

converted into the right to receive $69.25 in cash. Total cash required for the purchase was provided by the financial

sponsor group and lenders (Creditor Group) to Merger Sub. Regulatory authorities required that the debt associated

TXU). EFH’s primary direct subsidiary is Texas Competitive Electric Holdings, which holds TXU’s public utility

operating assets and liabilities. All TXU non-Sponsor Group–related debt incurred to finance the transaction is held by

EFH, while any debt incurred by the Sponsor Group is shown on the TH balance sheet. This legal structure allows for

the concentration of debt in TH and EFH, separate from the cash-generating assets held by Oncor and Texas

Competitive Electric Holdings.

when you compare actual December 31, 2009 (the last year for which public information is available), ratios with

required threshold levels.

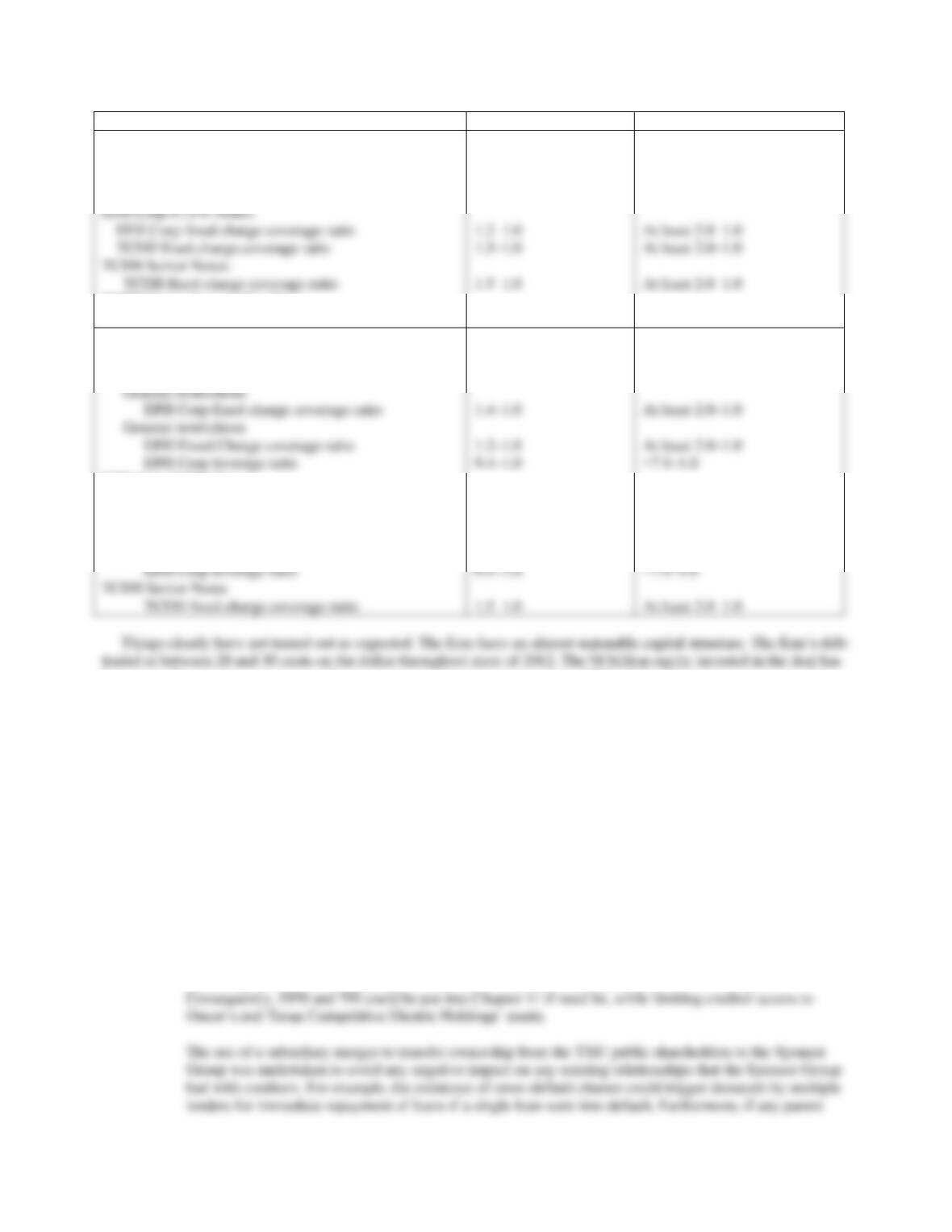

Table 13.6

EFH Holdings Debt Covenants

• December 31,

2009

• Threshold Level as of

December 31, 2009

Maintenance Covenant

28

adjusted EBITDA

Debt Incurrence Covenants

EFH Corp Senior Notes:

EFH Corp fixed charge coverage ratio

TCEH fixed charge coverage ratio

EFH Corp 9.75% Notes:

TCEH Senior Secured Facilities:

TCEH fixed charge coverage ratio

1.2–1.0

1.5–1.0

1.5–1.0

At least 2.0–1.0

At least 2.0–1.0

At least 2.0–1.0

Restricted Payments/Limitations on Investments

Covenants

EFH Corp Senior Notes

General restrictions

EFH Corp 9.75% Notes

General restrictions

EFH Corp fixed charge coverage ratio

General restrictions

EFH Corp fixed charge coverage ratio

EFH Corp leverage ratio

1.4–1.0

1.2–1.0

9.4–1.0

At least 2.0–1.0

At least 2.0–1.0

≤7.0–1.0

been virtually wiped out on paper. Absent a turnaround in natural gas prices, EFH is left with seeking a way to reduce

substantially the burden of the pending 2014 $20 billion loan payment with its lenders through a debt-for-equity swap

or more favorable terms on existing debt or by pursuing Chapter 11 bankruptcy. EFH has posted eight consecutive

quarterly losses. In December 2012, in an effort to extend debt maturities to buy time for a turnaround and to reduce

interest expense, EFH exchanged $1.15 billion of new payment–in-kind notes (interest is paid with more debt) for

existing notes with a face value of $1.6 billion. By any measure, this transaction illustrates the dark side of leverage.

Discussion Questions

1. How does the postclosing holding company structure protect the interests of the financial sponsor group

and the utility’s customers but potentially jeopardize creditor interests in the event of bankruptcy?

Answer: A holding company structure was used for two reasons: (1) to limit the risks to the financial and

creditor groups to potential liabilities and (2) to satisfy the requirement by Texas public utility regulators

to insulate the public utility from the additional debt service requirements created by the debt incurred to

finance the LBO. The structure effectively concentrates debt in EFH and TH, while separating the cash

producing assets in other legal entities (i.e., Oncor and Texas Competitive Electric Holdings).

29

2. What was the purpose of the pre-closing covenants and closing conditions as described in the merger

agreement?

3. Loan covenants exist to protect the lender. How might such covenants inhibit the EFH from meeting its

2014 $20 billion obligations?

4. As CEO of EFH, would you recommend to the board of directors as an appropriate strategy for paying the

$20 billion in debt that is maturing in 2014?

5. The substantial writedown of the net acquired assets in 2008 suggests that the purchase price paid for

TXU was too high. How might this impact KKR, TPG, and Goldman’s ability to earn financial returns

expected by their investors on the TXU acquisition? How might this writedown impact EFH’s ability

meet the $20 billion debt maturing in 2014?

Answer: The purchase price paid for TXU was clearly too high. Private equity investors were caught up in

the euphoria of 2007 when interest rates were exceptionally low and banks were aggressively competing

30

Lessons from Pep Boys’ Aborted Attempt to Go Private

Key Points

LBOs in recent years have involved financial sponsors’ providing a larger portion of the purchase price in cash than in

the past.

Financial sponsors focus increasingly on targets in which they have previous or related experience.

Deals that would have been completed in the early 2000s are more likely to be terminated or subject to renegotiation

than in the past.

_____________________________________________________________________________________

It ain’t over till it’s over” quipped former New York Yankees’ catcher Yogi Berra, famous for his malapropisms. The

oft-quoted comment was once again proven true in Pep Boys’ unsuccessful attempt to go private in 2012. On May 30,

2012, after nearly two years of discussions between Pep Boys and several interested parties, the firm announced that a

buyout agreement with the Gores Group (Gores), valued at approximately $1 billion (including assumed debt), had

collapsed, a victim of Pep Boys’ declining operating performance. The firm’s shares fell 20% on the news to $8.89 per

share, well below its level following the all-cash $15-a-share deal with Gores announced in January 2012. The terms of

the transaction also included a termination fee if either party failed to complete the deal by July 27, 2012. The failed

holdings (many of the firm’s store sites are owned by the firm). Such assets could be used as collateral underlying loans

to finance a portion of the purchase price. Furthermore, Gores has experience in retailing, having several retailers

among their portfolio of companies, including J. Mendel and Mexx.

The transaction reflected a structure common for deals of this type. Pep Boys had entered into a merger agreement

with Auto Acquisitions Group (the Parent), a shell corporation funded by cash provided by Gores as the financial

some degree of protection from Pep Boys’ liabilities. The purchase price was to have been financed by an equity

contribution of $489 million from limited partnerships managed by Gores and the balance by loans provided by

Barclays Bank PLC, Credit Suisse AG, and Wells Fargo Bank.

Upon learning that the Pep Boys’ reported earnings for the first quarter of 2012 would be well below expectations,

Gores attempted to renegotiate the terms of the deal, arguing that Pep Boys had breached the deal’s agreements. With

Pep Boys unwilling to accept a lower valuation, Gores exercised its right to terminate the deal by paying the $50

million breakup fee and agreed to reimburse Pep Boys for other costs it had incurred related to the deal. Pep Boys said

the firm will use the proceeds of the breakup fee to refinance a portion of its outstanding debt.

“Grave Dancer” Takes Tribune Corporation Private in an Ill-Fated Transaction

At the closing in late December 2007, well-known real estate investor Sam Zell described the takeover of the Tribune

Company as “the transaction from hell.” His comments were prescient in that what had appeared to be a cleverly

crafted, albeit highly leveraged, deal from a tax standpoint was unable to withstand the credit malaise of 2008. The end

came swiftly when the 161-year-old Tribune filed for bankruptcy on December 8, 2008.

On April 2, 2007, the Tribune Corporation announced that the firm’s publicly traded shares would be acquired in a

multistage transaction valued at $8.2 billion. Tribune owned at that time 9 newspapers, 23 television stations, a 25%

stake in Comcast’s SportsNet Chicago, and the Chicago Cubs baseball team. Publishing accounts for 75% of the firm’s

total $5.5 billion annual revenue, with the remainder coming from broadcasting and entertainment. Advertising and

from a C corporation to a Subchapter S corporation, allowing the firm to avoid corporate income taxes. However, it

would have to pay taxes on gains resulting from the sale of assets held less than ten years after the conversion from a C

to an S corporation (Figure 1).

Lenders

Lenders

Zell

$4 Billion

121 Million Shares

$4.05

$800 million (almost three times their preacquisition level), about 62% of the firm’s previous EBITDA cash flow of

$1.3 billion. While the ESOP owned the company, it was not be liable for the debt guaranteed by Tribune.

The conversion of Tribune into a Subchapter S corporation eliminated the firm’s current annual tax liability of $348

million. Such entities pay no corporate income tax but must pay all profit directly to shareholders, who then pay taxes

Zell

Tribune

Stage 1

$3.85 Billion

$.25 billion

126 Million Shares

$4.2 Billion

In an effort to reduce the firm’s debt burden, the Tribune Company announced in early 2008 the formation of a

partnership in which Cablevision Systems Corporation would own 97% of Newsday for $650 million, with Tribune

owning the remaining 3%. However, Tribune was unable to sell the Chicago Cubs (which had been expected to fetch as

much as $1 billion) and the minority interest in SportsNet Chicago to help reduce the debt amid the 2008 credit crisis.

12% of Tribune as a result of its prior sale of the Times Mirror to Tribune, and Dennis FitzSimons, the firm’s former

CEO, who received $17.7 million in severance and $23.8 million for his holdings of Tribune shares. Citigroup and

Merrill Lynch received $35.8 million and $37 million, respectively, in advisory fees. Morgan Stanley received $7.5

million for writing a fairness opinion letter. Finally, Valuation Research Corporation received $1 million for providing

a solvency opinion indicating that Tribune could satisfy its loan covenants.

What appeared to be one of the most complex deals of 2007, designed to reap huge tax advantages, soon became a

victim of the downward-spiraling economy, the credit crunch, and its own leverage. A lawsuit filed in late 2008 on

behalf of Tribune employees contended that the transaction was flawed from the outset and intended to benefit Sam

Zell and his advisors and Tribune’s board. Even if the employees win, they will simply have to stand in line with other

Tribune creditors awaiting the resolution of the bankruptcy court proceedings.

Discussion Questions:

1. What is the acquisition vehicle, post-closing organization, form of payment, form of acquisition, and tax

strategy described in this case study?

2. Describe the firm’s strategy to finance the transaction?

3. Is this transaction best characterized as a merger, acquisition, leveraged buyout, or spin–off? Explain your

answer.

4. Is this transaction taxable or non–taxable to Tribune’s public shareholders? To its post-transaction

shareholders? Explain your answer.

33

5. Comment on the fairness of this transaction to the various stakeholders involved. How would you apportion

the responsibility for the eventual bankruptcy of Tribune among Sam Zell and his advisors, the Tribune board,

and the largely unforeseen collapse of the credit markets in late 2008? Be specific.

Answer: The transaction was clearly highly leveraged by most measures. It was financed almost entirely with

debt, with Zell’s equity contribution amounting to less than 4 percent of the purchase price. The transaction

resulted in the Tribune being burdened with $13 billion in debt (including the approximate $5 billion currently

owed by Tribune). At this level, the firm’s debt was 10 times EBITDA, more than 2.5 times that of the

Financing LBOs—The SunGard Transaction

With their cash hoards accumulating at an unprecedented rate, there was little that buyout firms could do but to invest

in larger firms. Consequently, the average size of LBO transactions grew significantly during 2005. In a move

reminiscent of the blockbuster buyouts of the late 1980s, seven private investment firms acquired 100 percent of the

outstanding stock of SunGard Data Systems Inc. (SunGard) in late 2005. SunGard is a financial software firm known

for providing application and transaction software services and creating backup data systems in the event of disaster.

The company‘s software manages 70 percent of the transactions made on the Nasdaq stock exchange, but its biggest

business is creating backup data systems in case a client’s main systems are disabled by a natural disaster, blackout, or

terrorist attack. Its large client base for disaster recovery and back-up systems provides a substantial and predictable

cash flow.

SunGard’s new owners include Silver lake Partners, Bain Capital LLC, The Blackstone Group L.P., Goldman Sachs

Capital Partners, Kohlberg Kravis Roberts & Co., Providence Equity Partners Inc. and Texas Pacific Group. Buyout

firms in 2005 tended to band together to spread the risk of a deal this size and to reduce the likelihood of a bidding war.

Indeed, with SunGard, there was only one bidder, the investor group consisting of these seven firms.

The software side of SunGard is believed to have significant growth potential, while the disaster-recovery side

provides a large stable cash flow. Unlike many LBOs, the deal was announced as being all about growth of the

financial services software side of the business. The deal is structured as a merger, since SunGard would be merged

into a shell corporation created by the investor group for acquiring SunGard. Going private, allows SunGard to invest

heavily in software without being punished by investors, since such investments are expensed and reduce reported

earnings per share. Going private also allows the firm to eliminate the burdensome reporting requirements of being a

public company.

The buyout represented potentially a significant source of fee income for the investor group. In addition to the 2

percent management fees buyout firms collect from investors in the funds they manage, they receive substantial fee

income from each investment they make on behalf of their funds. For example, the buyout firms receive a 1 percent

deal completion fee, which is more than $100 million in the SunGard transaction. Buyout firms also receive fees paid

for by the target firm that is “going private” for arranging financing. Moreover, there are also fees for conducting due

diligence and for monitoring the ongoing performance of the firm taken private. Finally, when the buyout firms exit

their investments in the target firm via a sale to a strategic buyer or a secondary IPO, they receive 20 percent (i.e., so–

called carry fee) of any profits.

Under the terms of the agreement, SunGard shareholders received $36 per share, a 14 percent premium over the

SunGard closing price as of the announcement date of March 28, 2005, and 40 percent more than when the news first

leaked about the deal a week earlier. From the SunGard shareholders’ perspective, the deal is valued at $11.4 billion

dollars consisting of $10.9 billion for outstanding shares and “in-the-money” options (i.e., options whose exercise price

is less than the firm’s market price per share) plus $500 million in debt on the balance sheet.

The seven equity investors provided $3.5 billion in capital with the remainder of the purchase price financed by

commitments from a lending consortium consisting of Citigroup, J.P. Morgan Chase & Co., and Deutsche Bank. The

working capital needs and capital expenditures required obtaining commitments from lenders well in excess of $11.3

billion.

The merger financing consists of several tiers of debt and “credit facilities.” Credit facilities are arrangements for

extending credit. The senior secured debt and senior subordinated debt are intended to provide “permanent” or long–

term financing. Senior debt covenants included restrictions on new borrowing, investments, sales of assets, mergers

special purpose SunGard subsidiary will purchase receivables from SunGard, with the purchases financed through the

sale of the receivables to the lending consortium. The lenders subsequently finance the purchase of the receivables by

issuing commercial paper, which is repaid as the receivables are collected. The special purpose subsidiary is not shown

on the SunGard balance sheet. Based on the value of receivables at closing, the subsidiary could provide up to $500

million. The obligation of the lending consortium to buy the receivables will expire on the sixth anniversary of the

constitute 56 percent and subordinated or mezzanine debt comprises represents 44 percent.

SunGard Proforma Capital Structure

Pre-Merger Existing SunGard Debt Outstanding $Millions

Senior Notes (3.75% due in 2009) 250,000,000

Senior Notes (4.785 due in 2014) 250,000,000

6 year term

$4 billion term loan maturing in 7-1/2 years

Senior Subordinated Notes (≤$3 billion) 3,000,000,000

35

Blackstone Communications Partners I, L.P. 270,000,000

GS Capital Partners 2000, L.P. 250,000,000

1The roman numeral II refers to the fund providing the equity capital managed by the

partnership.

Case Study Discussion Questions:

1. SunGard is a software company with relatively few tangible assets. Yet, the ratio of debt to equity of almost 5

to 1. Why do you think lenders would be willing to engage in such a highly leveraged transaction for a firm of

this type?

2. Under what circumstances would SunGard refinance the existing $500 million in outstanding senior debt after

the merger? Be specific.

3. In what ways is this transaction similar to and different from those that were common in the 1980s? Be

specific.

4. Why are payment-in-kind securities (e.g., debt or preferred stock) particularly well suited for financing LBOs?

Under what circumstances might they be most attractive to lenders or investors?

5. Explain how the way in which the LBO is financed affects the way it is operated and the timing of when

equity investors choose to exit the business. Be specific.

HCA’S LBO REPRESENTS A HIGH-RISK BET ON GROWTH

While most LBOs are predicated on improving operating performance through a combination of aggressive cost cutting

and revenue growth, HCA laid out an unconventional approach in its effort to take the firm private. On July 24, 2006,

management again announced that it would “go private” in a deal valued at $33 billion including the assumption of

$11.7 billion in existing debt.

The approximate $21.3 billion purchase price for HCA’s stock was financed by a combination of $12.8 billion in

senior secured term loans of varying maturities and an estimated $8.5 billion in cash provided by Bain Capital, Merrill

Lynch Global Private Equity, and Kohlberg Kravis Roberts & Company. HCA also would take out a $4 billion

revolving credit line to satisfy immediate working capital requirements. The firm publicly announced a strategy of

improving performance through growth rather than through cost cutting. HCA’s network of 182 hospitals and 94

surgery centers is expected to benefit from an aging U.S. population and the resulting increase in health-care spending.

The deal also seems to be partly contingent on the government assuming a larger share of health-care costs in the

revenue growth assumptions fail to materialize. HCA’s management and equity investors have put themselves in a

position in which they seem to have relatively little influence over the factors that directly affect the firm’s future cash

flows.

Discussion Questions:

1. Does a hospital or hospital system represent a good or bad LBO candidate? Explain your answer.

Answer: Hospitals generally represent bad candidates. Hospital cash flow is heavily dependent on

government reimbursement rates which are likely to be declining in the future as the U.S. government

2. Having pledged not to engage in aggressive cost cutting, how do you think HCA and its financial sponsor

group planned on paying off the loans?

Answer: The financial sponsor group is assuming that increased government spending in view of the

Case Study. Sony Buys MGM

Sony’s long–term vision has been to create synergy between its consumer electronics products and music, movies, and

games. Sony, which bought Columbia Pictures in 1989 for $3.4 billion, had wanted to control Metro-Goldwyn-Mayer’s

film library for years, but it did not want to pay the estimated $5 billion it would take to acquire it. On September 14,

2004, a consortium, consisting of Sony Corp of America, Providence Equity Partners, Texas Pacific Group, and DLJ

Merchant Banking Partners, agreed to acquire MGM for $4.8 billion, consisting of $2.85 billion in cash and the

who holds a 74 percent stake in MGM, will make $2 billion because of the transaction. The private equity partners

could cash out within three-to-five years, with the consortium undertaking an initial public offering or sale to a strategic

investor. Major risks include the ability of the consortium partners to maintain harmonious relations and the

problematic growth potential of the DVD market.

Sony and MGM negotiations had proven to be highly contentious for almost five months when media giant Time

Warner Inc. emerged to attempt to satisfy Kerkorian’s $5 billion asking price. The offer was made in stock on the

assumption that Kerkorian would want a tax–free transaction. MGM’s negotiations with Time Warner stalled around

the actual value of Time Warner stock, with Kerkorian leery about Time Warner’s future growth potential. Time

Warner changed its bid in late August to an all cash offer, albeit somewhat lower than the Sony consortium bid, but it

refundable cash payment to MGM. As a testament to the adage that timing is everything, the revised Sony bid was

faxed to MGM just before the beginning of a board meeting to approve the Time Warner offer.

Discussion Questions:

1. Do you believe that MGM is an attractive LBO candidate? Why? Why not?

2. In what way do you believe that Sony’s objectives might differ from those of the private equity investors

making up the remainder of the consortium? How might such differences affect the management of MGM?

Identify possible short-term and long-term effects.

Answer: Sony wanted to gain access to the film library to help provide content for the growth in its play

station and games product lines. However, the private equity investors were more likely to want to cash out in

3. How did Time Warner’s entry into the bidding affect pace of the negotiations and the relative bargaining

power of MGM, Time Warner, and the Sony consortium?

Answer: The bargaining was contentious and stalled for 5 months until Time Warner converted the bilateral

4. What do you believe were the major factors persuading the MGM board to accept the Revised Sony bid? In

your judgment, do these factors make sense? Explain your answer.

RJR NABISCO GOES PRIVATE—

KEY SHAREHOLDER AND PUBLIC POLICY ISSUES

Background

and Roberts (KKR), to buy the firm for $90 per share (Wasserstein, 1998). The firm’s board immediately was faced

with the dilemma of whether to accept the KKR offer or to consider some other form of restructuring of the company.

The board appointed a committee of outside directors to assess the bid to minimize the appearance of a potential

conflict of interest in having current board members, who were also part of the buyout proposal from management, vote

on which bid to select.

borrowed to complete the transaction. The remaining debt was supplied by junk bond financing. The RJR shareholders

were the real winners, because the final purchase price constituted a more than 100% return from the $56 per share

price that existed just before the initial bid by RJR management.

Aggressive pricing actions by such competitors as Phillip Morris threatened to erode RJR Nabisco’s ability to

service its debt. Complex securities such as “increasing rate notes,” whose coupon rates had to be periodically reset to

about one-fourth of the firm’s common stock in public hands.

When KKR eventually fully liquidated its position in RJR Nabisco in 1995, it did so for a far smaller profit than

expected. KKR earned a profit of about $60 million on an equity investment of $3.1 billion. KKR had not done well for

the outside investors who had financed more than 90% of the total equity investment in KKR. However, KKR fared

much better than investors had in its LBO funds by earning more than $500 million in transaction fees, advisor fees,

shareholders is to take actions to maximize shareholder value; yet in the RJR Nabisco case, the management bid

appeared to be well below what was in the best interests of shareholders. Several proposals have been made to

minimize the potential for conflict of interest in the case of an MBO, including that directors, who are part of an MBO

effort, not be allowed to participate in voting on bids, that fairness opinions be solicited from independent financial

advisors, and that a firm receiving an MBO proposal be required to hold an auction for the firm.