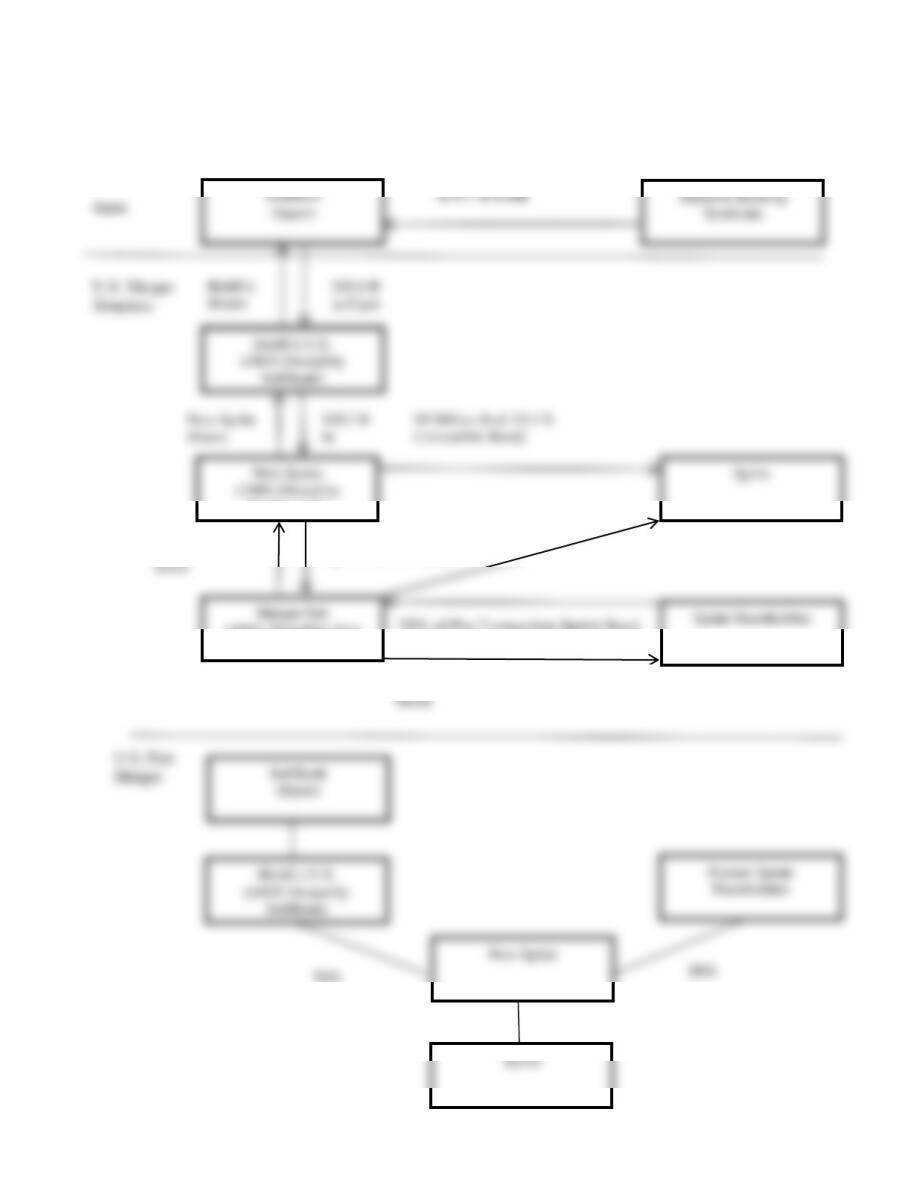

of the subsidiary’s stock. At closing, Merger Sub is merged into Sprint, with Sprint surviving. New Sprint provides

and 30% owned by former Sprint shareholders.

3.0 billion

3.6 billion

share4

4.6 billion

4.6 billion

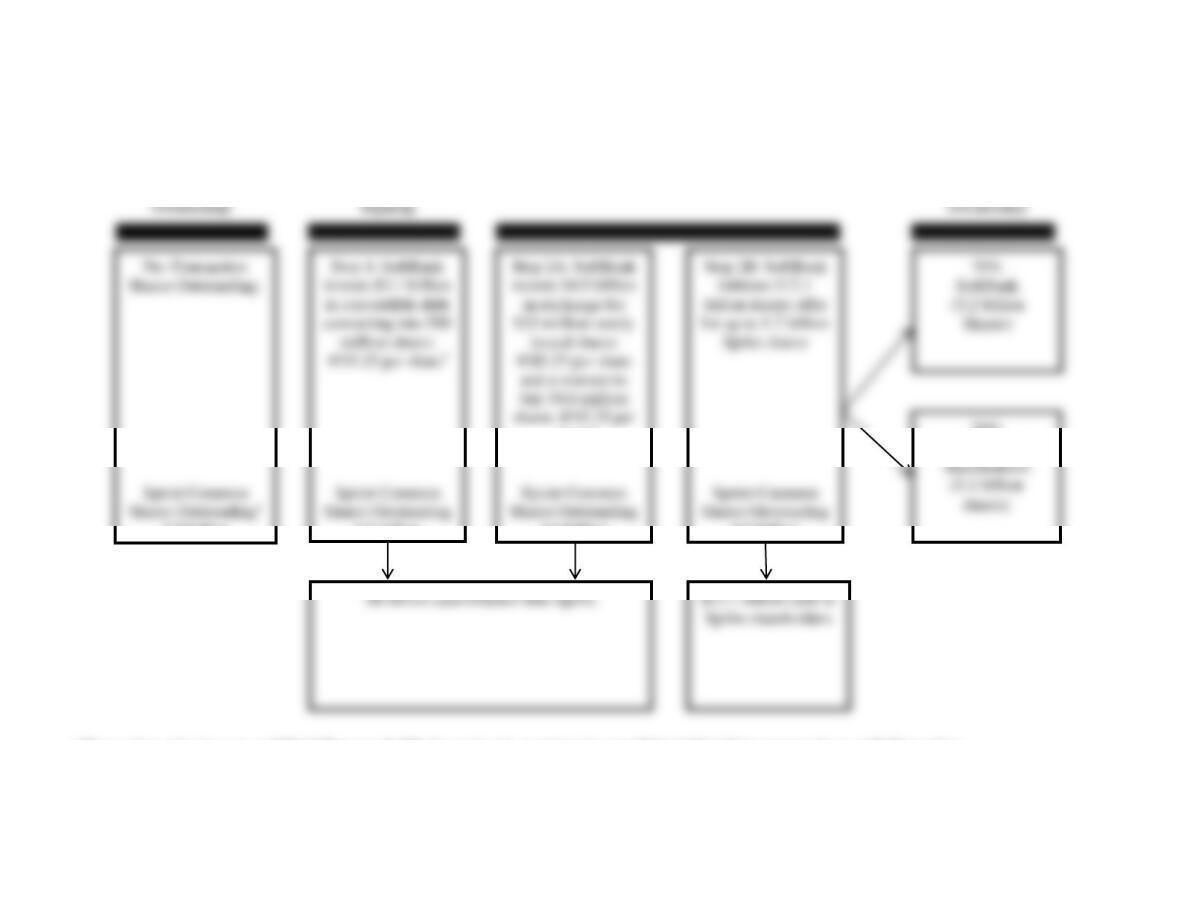

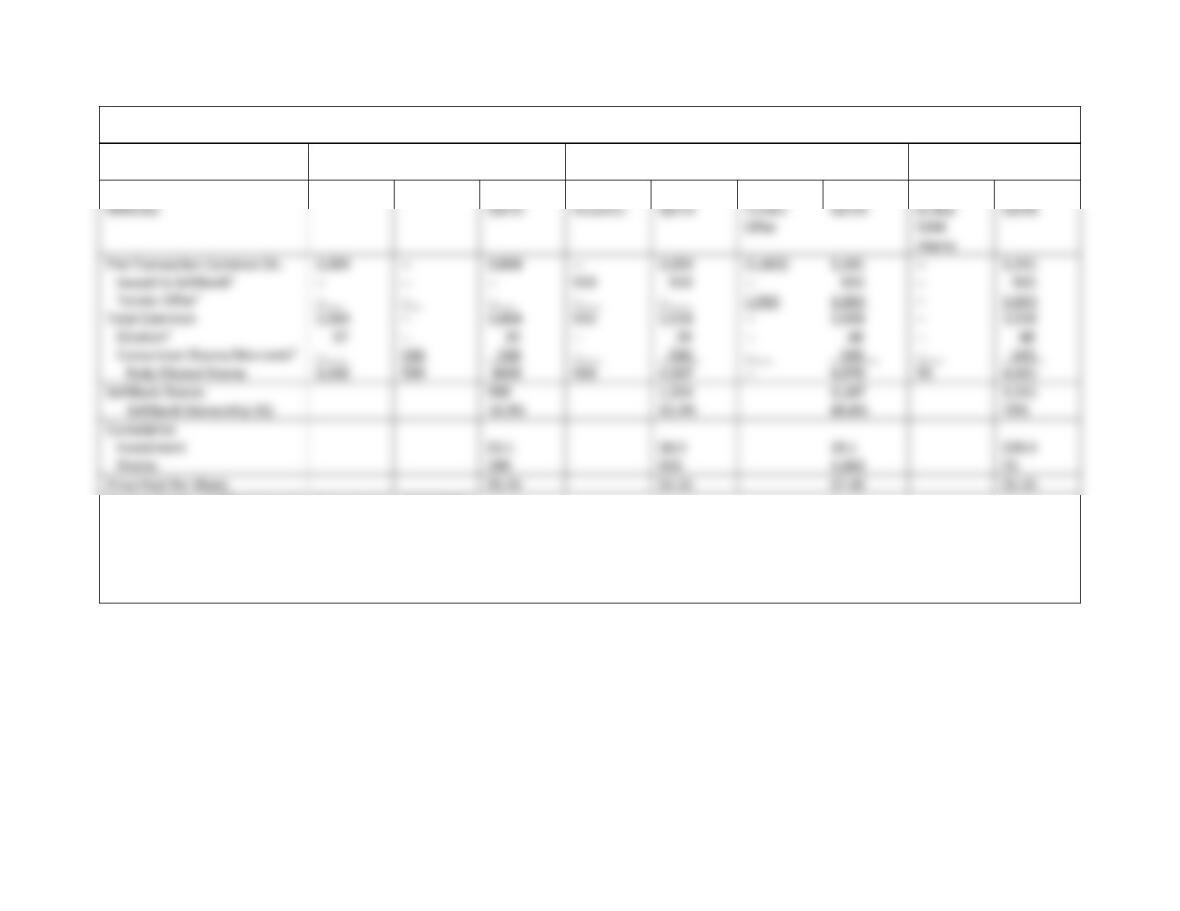

Pre-Transaction Immediately After At Close Post-Transaction

Ownership Signing Ownership

30%

Pre-Transaction

Shareholders

$8 billion cash infusion Into Sprint

$12.1 billion cash to

Figure 12.7 Transaction Timeline

(Total Purchase Price at Closing = $21.1 Billion)1

1The purchase price increases to $20.4 billion once SoftBank exercises its warrant to buy an additional 55 million common shares at $5.25 per share.

2Note that Sprint common shares outstanding are rounded to the nearest million.

3$3.1 billion / $5.25 = .6 billion shares

4$4.9 billion / $5.25 = .93 billion shares + .0546 billion shares = .9846 billion shares

Table 12.7 Calculating Shares Outstanding for Steps 1, 2A and 2B

Announcement Date

At Closing

5-Year Warrants

($ in Billions and Shares in

Millions)

Sprint

Conversion

Step 1

Sprint

Common

Issuance

Step 2A

Sprint

$12.1

Tender

Step 2B

Sprint

Warrants

to Buy

Step 2C

Sprint

Source: Sprint – SoftBank Investor Presentation, 10/15/2012

1New Sprint shares issued to SoftBank for that portion of the $17 billion contributed by SoftBank to Sprint and not used in the tender offer, that is, $17.0 –

$12.1 = $4.9 billion.

2Shares acquired in the public markets from Sprint shareholders who subscribe to the tender offer.

3Provides an estimate of the number of options whose exercise price is less than the offer price and therefore are likely to be converted to common shares.

4New Sprint shares issued to SoftBank when the convertible debt it purchased for $3.1 billion is converted

SoftBank

HoldCo U.S.)

(100% Owned by New

Srpint)

Sprint

Figure 12.8 SoftBank-Sprint Merger

Merger Sub

Stock

$12.1 Billion in New

Sprint Stock & Cash

55% of Pre-Transaction Sprint Stock

$12.1 Billion in Cash & New Sprint

Stock

70%

100%

Japanese Banking

$19.1 B Loan

Discussion Questions:

1. What is the form of payment and form of acquisition employed by SoftBank in its takeover of Sprint–

Nextel? Is all or some of the total consideration paid to Sprint shareholders tax free?

2. What is the purpose of the holding company structure adopted by SoftBank in this transaction?

3. Would you characterize this as a reverse or forward merger? Based on your answer why was this type of

reorganization selected by SoftBank? Will this takeover require a vote by Softbank shareholders?

4. The convertible debt is described as a “stock lockup.” How does the convertible debt discourage other

interested parties from bidding on Sprint?

5. What are the arguments for and against the proposed takeover being approved by U.S. regulators?

6. Why did SoftBank use New Sprint shares as part of the tender offer to Sprint shareholders rather than its

own shares?

7. What is the purpose of the reverse termination and termination fees employed in the transaction?

Energy Transfer Outbids Williams Companies for Southern Union—Alternative Bidding Strategies

_____________________________________________________________________________

Key Points

Higher bids involving stock and cash may be less attractive than a lower all-cash bid due to the uncertain nature of the value of the

acquirer’s stock.

Master limited partnerships represent an alternative means for financing a transaction in industries in which cash flows are relatively

predictable.

______________________________________________________________________________

Energy pipeline company Southern Union (Southern) offered significant synergistic opportunities for competitors Energy Transfer Equity

(ETE) and The Williams Companies (Williams). Increasing interest in natural gas as a less polluting but still affordable alternative to coal

and oil motivated both ETE and Williams to pursue Southern in mid-2011. Williams, already the nation’s largest pipeline company,

accounting for about 12% of the nation’s natural gas distribution by volume, viewed the acquisition as a means of solidifying its premier

lakes regions as well as Texas and New Mexico). It also owns local gas distribution companies that serve more than half a million end

users in Missouri and Massachusetts.

While both ETE and Williams were attracted to Southern because the firm’s shares were believed to be undervalued, the potential

synergies also are significant. ETE would transform the firm by expanding its business into the Midwest and Florida and offers a very

good complement to ETE’s existing Texas-focused operations. For Williams, it would create the dominant natural gas pipeline system for

the Midwest and Northeast and give it ownership interests in two pipelines running into Florida.

Despite the transition of exploration and production companies to liquids for distribution, Southern continued to trade, largely as an

annuity offering a steady, predictable financial return. During the six–month period prior to the start of the bidding war, Southern’s stock

was caught in a trading range between $27 and $30 per share. That changed in mid-June, when a $33-per-share bid from ETE, consisting

of both cash and stock valued by Southern at $4.2 billion, put Southern in “play.” The initial ETE offer was immediately followed by a

series of four offers and counteroffers, resulting in an all–cash counteroffer of $44 per share from The Williams Companies, valuing

Southern at $5.5 billion. This bid was later topped with an ETE offer of $44.25 per Southern share, boosting Southern’s valuation to

approximately $5.6 billion.

firm’s founder and chairman, George Lindemann, and its president, Eric D. Herschmann.

ETE removed any concerns about the firm’s ability to finance the cash portion of the transaction when it announced on August 5,

2011, that it had received financing commitments for $3.7 billion from a syndicate consisting of 11 U.S. and foreign banks. The firm also

announced that it had received regulatory approval from the Federal Trade Commission to complete the transaction.

As part of the agreement with ETE, Southern contributed its 50% interest in Citrus Corporation to Energy Transfer Partners for $2

billion. The cash proceeds from the transfer will be used to repay a portion of the acquisition financing and to repay existing Southern

27

pipeline assets into Energy Transfer Partners and Regency Energy Partners, eliminating their being subject to double taxation. These

actions helped to offset a portion of the purchase price paid to acquire Southern Union.

In retrospect, ETE may have invited the Williams bid because of the confusing nature of its initial bid. According to the firm’s first

full due diligence.

Discussion Questions

1. If you were a Southern shareholder, would you have found the Williams or the Energy Transfer Equity bid more attractive?

Explain your answer.

2. The all-cash Williams bid was contingent on the firm completing full due diligence on Southern Union. Why would this

represent a potential risk to Southern Union shareholders?

Answer: The Williams Companies had based their bid on less than complete information gleaned from public sources or from

their own knowledge of the business. They had not been given access to the audited financial statements of Southern Union; nor

3. Energy Transfer Equity transferred Southern Union’s pipeline assets into its primary master limited partnerships in order to

finance a portion of the purchase price. In what way could this action be viewed as a means of offsetting a portion of the

purchase price? In what way may this action have created a tax liability for Energy Transfer Equity?

Answer: Both Williams and ETE would have moved Southern’s pipeline assets into their master limited partnerships. Williams

would likely pass the pipelines into Williams Partners, while ETE would likely transfer the pipelines to Energy Transfer Partners

4. What do you believe are the key assumptions underlying either the Energy Transfer Equity or the Williams valuations of

Southern Union?

Teva Pharmaceuticals Buys Barr Pharmaceuticals to Create a Global Powerhouse

Key Points

Foreign acquirers often choose to own U.S. firms in limited liability corporations.

American Depository Shares (ADSs) often are used by foreign buyers, since their shares do not trade directly on U.S. stock exchanges.

28

Despite a significant regulatory review, the firms employed a fixed share-exchange ratio in calculating the purchase price, leaving each at

risk of Teva share price changes.

_____________________________________________________________________________________

On December 23, 2008, Teva Pharmaceuticals Ltd. completed its acquisition of U.S.-based Barr Pharmaceuticals Inc. The merged

businesses created a firm with a significant presence in 60 countries worldwide and about $14 billion in annual sales. Teva

annual sales of about $2.5 billion, Barr is engaged primarily in the development, manufacture, and marketing of generic and proprietary

pharmaceuticals and is one of the world’s leading generic–drug companies. Barr also is involved actively in the development of generic

biologic products, an area that Barr believes provides significant prospects for long-term earnings and profitability.

Based on the average closing price of Teva American Depository Shares (ADSs) on NASDAQ on July 16, 2008, the last trading day in

the United States before the merger’s announcement, the total purchase price was approximately $7.4 billion, consisting of a combination

could have changed between signing and closing, because the share–exchange ratio was fixed, per the merger agreement.

By most measures, the offer price for Barr shares constituted an attractive premium over the value of Barr shares prior to the merger

announcement. Based on the closing price of a Teva ADS on the NASDAQ Stock Exchange on July 16, 2008, the consideration for each

outstanding share of Barr common stock for Barr shareholders represented a premium of approximately 42% over the closing price of

Barr common stock on July 16, 2008, the last trading day in the United States before the merger announcement. Since the merger

highly complementary with Teva’s and extends Teva’s product offering and product development pipeline into new and attractive product

categories, such as a substantial women’s healthcare business. The merger also is a response to the ongoing global trend of consolidation

among the purchasers of pharmaceutical products as governments are increasingly becoming the primary purchaser of generic drugs.

Under the merger agreement, a wholly owned Teva corporate subsidiary, the Boron Acquisition Corp. (i.e., acquisition vehicle),

merged with Barr, with Barr surviving the merger as a wholly owned subsidiary of Teva. Immediately following the closing of the

employee agreements or declare any dividends or buy back any outstanding stock. Barr also agreed not to engage in one or more

transactions or investments or assume any debt exceeding $25 million. The firm also promised not to change any accounting practices in

any material way or in a manner inconsistent with generally accepted accounting principles. Barr also committed not to solicit alternative

bids from any other possible investors between the signing of the merger agreement and the closing.

Teva agreed that from the period immediately following closing and ending on the first anniversary of closing it would require Barr or

2 ADSs may be issued in uncertificated form or certified as an American Depositary Receipt, or ADR. ADRs provide evidence that a

specified number of ADSs have been deposited by Teva commensurate with the number of new ADSs issued to Barr shareholders.

29

Barr employee would be maintained at no less than the levels in effect before closing. Bonus plans also would be maintained at levels no

less favorable than those in existence before the closing of the merger.

The key closing conditions that applied to both Teva and Barr included satisfaction of required regulatory and shareholder approvals,

compliance with all prevailing laws, and that no representations and warranties were found to have been breached. Moreover, both parties

had to provide a certificate signed by the chief executive officer and the chief financial officer that their firms had performed in all

material respects all obligations required to be performed in accordance with the merger agreement prior to the closing date and that

neither business had suffered any material damage between the signing and the closing.

The merger agreement had to be approved by a majority of the outstanding voting shares of Barr common stock. Shareholders failing

information” from the FTC, whose effect was to extend the HSR waiting period another 30 days. Teva and Barr received FTC and Justice

Department approval once potential antitrust concerns had been dispelled. Given the global nature of the merger, the two firms also had to

file with the European Union Antitrust Commission as well as with other country regulatory authorities.

Discussion Questions

1. Why do you believe that Teva chose to acquire the outstanding stock of Barr rather than selected assets? Explain your answer.

Answer: Much of the value of Barr is intangible in the form of patents, brand names, and in-process research and development.

The latter generally represents unpatented ideas and processes which have not been commercialized but may have the potential

2. Mergers of businesses with operations in many countries must seek approval from a number of regulatory agencies. How might

this affect the time between the signing of the agreement and the actual closing? How might the ability to realize synergy

following the merger of the two businesses be affected by actions required by the regulatory authorities before granting their

approval? Be specific.

Answer: Regulatory approvals for cross-border (i.e., multinational) transaction can be both expensive, time consuming, and

nightmarish because of inconsistent regulations from one country to another. Some countries charge filing fees in the hundreds

of dollars and others charge thousands. Antitrust regulators have historically tended to follow different standards, impose

3. What it the importance of the pre-closing covenants signed by both Teva and Barr?

30

4. What is the importance of the closing conditions in the merger agreement? What could happen if any of the closing conditions

are breached (i.e., violated)?

Answer: Closing conditions are obligations that must be satisfied in order to require the other party to close the deal. Unless

these conditions are not satisfied, either party may refrain from closing. If any condition is unsatisfied or breached including that

5. Speculate as to why Teva offered Barr shareholders a combination of Teva stock and cash for each Barr share outstanding and

why Barr was willing to accept a fixed share exchange ratio rather than some type of collar arrangement.

Answer: Teva may have used a combination of stock and cash to appeal a wider range of Barr shareholders thereby increasing

Johnson & Johnson Uses Financial Engineering to Acquire Synthes Corporation

_____________________________________________________________________________

Key Points

While tax considerations rarely are the primary motivation for takeovers, they make transactions more attractive.

Tax considerations may impact where and when investments such as M&As are made.

Foreign cash balances give multinational corporations flexibility in financing M&As.

_____________________________________________________________________________________

United States–based Johnson & Johnson (J&J), the world’s largest healthcare products company, employed creative tax strategies in

undertaking the biggest takeover in its history. When J&J first announced that it would acquire Swiss medical device maker Synthes for

$19.7 million in stock and cash, the firm indicated that the deal would dilute its current shareholders due to the issuance of 204 million

new shares. Investors expressed their dismay by pushing the firm’s share price down immediately following the announcement. J&J

looked for a way to make the deal more attractive to investors while preserving the composition of the purchase price paid to Synthes’

shareholders (two-thirds stock and the remainder in cash). They could defer the payment of taxes on that portion of the purchase price

received in J&J shares until such shares were sold; however, they would incur an immediate tax liability on any cash received.

Having found a loophole in the IRS’s guidelines for utilizing funds held in foreign subsidiaries, J&J was able to make the deal’s

financing structure accretive to earnings following closing. In 2011, the IRS had ruled that cash held in foreign operations repatriated to

the United States would be considered a dividend paid by the subsidiary to the parent, subject to the appropriate tax rate. Because the

United States has the highest corporate tax rate among developed countries, U.S. multinational firms have an incentive to reinvest

earnings of their foreign subsidiaries abroad.

With this in mind, J&J used the foreign earnings held by its Irish subsidiary to buy 204 million of its own shares, valued at $12.9

billion, held by Goldman Sachs and JPMorgan, which had previously acquired J&J shares in the open market. The buyback of J&J shares

held by these investment banks increased the consolidated firm’s earnings per share. These shares, along with cash, were exchanged for

outstanding Synthes’ shares to fund the transaction. J&J also avoided a hefty tax payment by not repatriating these earnings to the United

States, where they would have been taxed at a 35% corporate rate rather than the 12% rate in Ireland. Investors reacted favorably,

boosting J&J’s share price by more than 2% in mid-2012, when the firm announced the deal would be accretive rather than dilutive.

Presumably, the IRS will move to prevent future deals from being financed in a similar manner.

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question Johnson & Johnson might ask about a 2009

transaction involving pharmaceutical companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and Company

(“Merck”) and Schering–Plough Corp. (Schering-Plough) voted overwhelmingly to approve a $41.1 billion merger of the two firms. With

annual revenues of $42.4 billion, the new Merck will be second in size only to global pharmaceutical powerhouse Pfizer Inc.

respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual cost savings, with Merck reducing its workforce

by about 15 percent through facility consolidations, a highly complementary product offering, and the substantial number of new drugs

under development at Schering-Plough. Furthermore, the deal increases Merck’s international presence, since 70 percent of Schering–

Plough’s revenues come from abroad. The combined firms both focus on biologics (i.e., drugs derived from living organisms). The new

combined Schering-Plough and Merck companies into the subsidiaries. Merger Sub 1 was merged into Schering-Plough, with Schering-

Plough the surviving firm. Merger Sub 2 was merged with Merck, with Merck surviving as a wholly-owned subsidiary of Schering-

Plough. The end result is the appearance that Schering-Plough (renamed Merck) acquired Merck through its wholly-owned subsidiary

(Merger Sub 2). In reality, Merck acquired Schering-Plough.

Former shareholders of Schering-Plough and Merck become shareholders in the new Merck. The “New Merck” is simply Schering–

2008 revenues and about 70 percent of the firm’s international revenues. Consequently, retaining these revenues following the merger was

important to both Merck and Schering-Plough.

The multi-step process for implementing this transaction is illustrated in the following diagrams. From a legal perspective, all these

actions occur concurrently.