Answer: Common restructuring strategies that could have been used as an alternative to a reverse merger include a

spin-off, split-off or equity carve-out. These options are discussed in Chapters 1 and in considerable detail in Chapter

16.

A spin-off involves the payment of the stock of T-Mobile held by Deutsche-Telekom to its shareholders as a

dividend. Procedurally, it is relatively straight forward as the board of directors has the sole right to declare the type

(cash or stock) and timing of dividends. Properly structured the dividend would be tax-free to Deutsche–Telekom’s

shareholders. The distribution would have the added advantage of giving the receiving shareholder the right to

2. What are the primary disadvantages and advantages of a reverse merger strategy?

Answer: As with any merger, the acquirer is taking responsibility for the known and unknown legal and financial

liabilities of the other party. Thus, extensive due diligence is required. As with an equity carve-out, the merged firms

will have minority shareholders. The existence of the public shareholders requires periodically filing reports with the

3. In what way might the use of the T-Mobile/MetroPCS impact value?

Answer: The use of a reverse merger has all of the advantages (and disadvantages) of a conventional statutory merger.

That is, all assets and liabilities known and unknown automatically transfer by rule of law to the merged firms. The

impact on value can be positive or negative depending on the types and magnitude of unknown liabilities and assets

4. What are the key assumptions implicit in the Deutsche-Telekom restructuring strategy for T-Mobile?

Answer: Deutsche-Telekom sees this deal as an exit strategy from T-Mobil. The objective is to undertake an IPO at

5. What is the form of payment used in this deal? Why might this form have been selected? What are the advantages and

disadvantages of the form of payment used in this deal?

Answer: The form of payment for MetroPCS is a combination of cash and stock. This combination may have been

used because an all-cash deal would have required a substantial increase in borrowing further burdening Newco; using

6. What is the form of acquisition used in this deal? Why might this form have been chosen? What are the advantages and

disadvantages of the form of acquisition used in this case study?

Answer: The form of acquisition reflects what is being acquired (stock or assets) and how ownership is conveyed. In

Sanofi Acquires Genzyme in a Test of Wills

Key Points

Contingent value rights help bridge price differences between buyers and sellers when the target’s future earnings

performance is dependent on the realization of a specific event.

They are most appropriate when the target firm is a large publicly traded firm with numerous shareholders.

______________________________________________________________________________

Facing a patent expiration precipice in 2015, big pharmaceutical companies have been scrambling to find new sources of

revenue to offset probable revenue losses as many of their most popular drugs lose patent protection. Generic drug

companies are expected to make replacement drugs and sell them at a much lower price.

Focusing on the biotechnology market, French-based drug company Sanofi-Aventis SA (Sanofi) announced on February

17, 2011, the takeover of U.S.-based Genzyme Corp. (Genzyme) for $74 per share, or $20.1 billion in cash, plus a

contingent value right (CVR). The CVR could add as much as $14 a share or another $3.8 billion, to the purchase price if

23

at a time when debt was cheap and when Genzyme’s share price was depressed, having fallen from a 2008 peak of $83.25

to $47.16 in June 2010. Genzyme’s depressed share price reflected manufacturing problems that had lowered sales of its

best-selling products. Genzyme continued to recover from the manufacturing challenges that had temporarily shut down

operations at its main site in 2009. The plant is the sole source of Genzyme’s top-selling products, Gaucher’s disease

treatment Cerezyme and Fabry disease drug Fabrazyme. Both were in short supply throughout 2010 due to the plant’s

that the Genzyme shareholders would accept the offer rather than risk seeing their shares fall to $50. The shares, however,

traded sharply higher at $70.49 per share, signaling that investors were expecting Sanofi to have to increase its bid.

Viehbacher said he might increase the bid if Genzyme would be willing to disclose more information about the firm’s

ongoing manufacturing problems and the promising new market potential for its multiple sclerosis drug.

In a letter made public on August 29, 2010, Sanofi indicated that it had been trying to engage Genzyme in acquisition

that the firm was worth at least $80 per share. He based this value on the improvement in the firm’s manufacturing

operations and the revenue potential of Lemtrada, Genzyme’s experimental treatment for multiple sclerosis, which once

approved for sale by the FDA was projected by Genzyme to generate billions of dollars annually. Despite Genzyme’s

refusal to participate in takeover discussions, Sanofi declined to raise its initial offer in view of the absence of other bidders.

Sanofi finally initiated an all-cash hostile tender offer for all of the outstanding Genzyme shares at $69 per share on

The CVR helped to allay fears that Sanofi would overpay and that the drug Lemtrada would not be approved by the

FDA. Under the terms of the CVR, Genzyme shareholders would receive $1 per share if Genzyme were able to meet

certain production targets in 2011 for Cerezyme and Fabrazyme, whose output had been sharply curtailed by viral

contamination at its plant in 2009. Each right would yield an additional $1 if Lemtrada wins FDA approval. Additional

payments will be made if Lemtrada hits certain other annual revenue targets. The CVR, which runs until the end of 2020,

included a “top–up” option granted by the Genzyme board to Sanofi. The “top–up” option would be triggered when Sanofi

acquired 75% of Genzyme’s outstanding shares through its tender offer. The 75% threshold could have been lower had

Genzyme had more authorized but unissued shares to make up the difference between the 90% requirement for the short-

form merger and the number of shares accumulated as a result of the tender offer. The deal also involved the so-called dual-

track model of simultaneously filing a proxy statement for a shareholders’ meeting and vote on the merger while the tender

offer is occurring to ensure that the deal closes as soon as possible.

Discussion Questions

1. The deal was structured as a tender offer coupled with a “top up” option to be followed by a backend short

form merger. Why might this structure be preferable to a more common statutory merger deal or a tender offer

followed by a backend merger requiring a shareholder vote?

24

Answer: Merger deals require target firm shareholder approvals which might delay the closing significantly,

giving rise to the potential for another bidder to appear, a dissident shareholder to gain support, or in an share

2. Speculate as to the purpose of the dual track model in which the bidder initiates a tender offer and

simultaneously files a prospectus to hold a shareholders meeting and vote on a merger

3. Describe the takeover tactics employed by Sanofi. Discuss why each one might have been used.

Answer: Sanofi was opportunistic in its approach to Genzyme. Timing was critical. Debt financing was

cheap, Genzyme’s share price was depressed, and its major competitors were too preoccupied to participate in

an auction for Genzyme. Sanofi wanted a friendly takeover to minimize disrupting efforts to improve the

firm’s manufacturing operations and to minimize the loss of key employees, customers, and suppliers that

often accompany vitriolic hostile takeover battles.

4. Describe the antitakeover strategy employed by Genzyme. Discuss why each may have been employed. In

your opinion, did the Genzyme strategy work?

Answer: Genzyme’s defensive strategy appeared to consist of stalling tactics including but not limited to

simply ignoring overtures from Genzyme. The motivation for this “just say know” strategy may have been to

buy time to improve operational performance and in turn earnings which would enable the firm to argue for a

higher value. In addition, once the tender offer was underway, Genzyme was compelled to publicly state a

25

5. What alternatives could Sanofi used instead of the CVR to bridge the difference in how the parties valued

Genzyme? Discuss the advantages and disadvantages of each.

Answer: A CVR is a specific type of an earnout. Under an earnout, a portion of the purchase price is deferred

and dependent on future events. It is used to bridge the gap between buyer and seller purchase price

expectations. A CVR is an increasingly popular version of an earnout in public company sales, especially the

pharmaceutical industry. CVRs are usually shorter in duration than earnouts and tied to the objectively

6. How might both the target and bidding firm benefit from the top-up option?

Answer: The bidder benefits by avoiding the delay associated with a more conventional backend merger

7. How might the existence of a CVR limit Sanofi’s ability to realize certain types of synergies? Be specific.

Answer: As is true with earnouts, the CVR may limit Sanofi’s ability to integrate the two firms in order to

realize certain cost reductions and operating efficiencies because the two firms must be operated separately. If

Swiss Pharmaceutical Giant Novartis Takes Control of Alcon

_________________________________________________________________________________________________

Key Points

Parent firms frequently find it appropriate to buy out minority shareholders to reduce costs and to simplify future decision

making.

Acquirers may negotiate call options with the target firm after securing a minority position to implement so-called

“creeping takeovers.”

_________________________________________________________________________________________________

In December 2010, Swiss pharmaceutical company Novartis AG completed its effort to acquire, for $12.9 billion, the

remaining 23% of U.S.-listed eye care group Alcon Incorporated (Alcon) that it did not already own. This brought the total

purchase price for 100% of Alcon to $52.2 billion. Novartis had been trying to purchase Alcon’s remaining publicly traded

shares since January 2010, but its original offer of 2.8 Novartis shares, valued at $153 per Alcon share, met stiff resistance

from Alcon’s independent board of directors, which had repeatedly dismissed the Novartis bid as “grossly inadequate.”

26

Novartis finally relented, agreeing to pay $168 per share, the average price it had paid for the Alcon shares it already

2.8 shares exceeded $168, the number of Novartis shares would be reduced. By acquiring all outstanding Alcon shares,

In 2008, with global financial markets in turmoil, Novartis acquired, for cash, a minority position in food giant Nestlé’s

wholly owned subsidiary Alcon. Nestlé had acquired 100% of Alcon in 1978 and retained that position until 2002, when it

2008 plus $28.1 billion in 2010). On the same day, Novartis also offered to acquire the remaining publicly held shares that

it did not already own in a share exchange valued at $153 per share in which 2.8 shares of its stock would be exchanged for

each Alcon share.

While the Nestlé deal seemed likely to receive regulatory approval, the offer to the minority shareholders was assailed

immediately as too low. At $153 per share, the offer was well below the Alcon closing price on January 4, 2010, of

shares also lost 3%, falling to $52.81. On August 9, 2010, Novartis received approval from European Union regulators to

buy the stake in Alcon, making it easier for it to take full control of Alcon.

With the buyout of Nestlé’s stake in Alcon completed, Novartis was now faced with acquiring the remaining 23% of the

outstanding shares of Alcon stock held by the public. Under Swiss takeover law, Novartis needed a majority of Alcon board

members and two-thirds of shareholders to approve the terms for the merger to take effect and for Alcon shares to convert

merger in which the minority shares convert to Novartis shares at the 2.8 share-exchange offer.

Provisions in the Swiss takeover code require a mandatory offer whenever a bidder purchases more than 33.3% of

another firm’s stock. In a mandatory offer, Novartis would also be subject to the Swiss code’s minimum-bid rule, which

would require Novartis to pay $181 per share in cash to Alcon’s minority shareholders, the same bid offered to Nestlé. By

replacing the Nestlé-appointed directors with their own slate of candidates and owning more than two-thirds of the Alcon

Discussion Questions

1. Speculate as to why Novartis acquired only a 25 percent stake in Alcon in 2008.

Answer: Nestle may have been unwilling to sell more Alcon shares because of the depressed state of the

27

2. Why was the price ($181 per share) at which Novartis exercised its call option in 2010 to increase its stake in

Alcon to 77 so much higher than what it paid ($143 per share) for an approximate 25 percent stake in Alcon in

early 2008?

Answer: Novartis went from buying a 25 percent minority stake, subject to a minority discount from the

3. Alcon and Novartis shares dropped by 5 percent and 3 percent, respectively, immediately following the

announcement that Novartis would exercise its option to buy Nestle’s majority holdings of Alcon shares.

Explain why this happened.

4. How do Swiss takeover laws compare to comparable U.S. laws. Which are more appropriate and why?

Answer: U.S. law enables an acquirer owning more than 50.1 percent of another firm to force the minority

shareholders to sell their shares, often in exchange for preferred shares or debt. This is done to prevent a

6. Discuss how Novartis may have arrived at the estimate of $137 per share as the intrinsic value of

Alcon.

What are the key underlying assumptions? Do you believe that the minority shareholders should receive the

same price as Nestle?

Answer: Novartis argued that the $164 price of publicly traded Alcon stock prior to Novartis exercising its

call option reflected speculation that the eventual buyout of the minority shareholders of Alcon would take

Illustrating How Deal Structure Affects Value—The FaceBook / Instagram Deal

_________________________________________________________________________________________________

Key Points:

Deal structures affect value by limiting risk to the parties involved or exposing them to risk.

The value of cash received at closing is certain, whereas the value of stock is not.

Mechanisms exist to limit such risk; however, they often come with a cost to the party seeking risk mitigation.

_________________________________________________________________________________________________

long-term profitability.

Facebook’s dual class shareholder structure gives Mr. Zuckerberg effective control of the firm, despite owning only

28.4% of outstanding class B shares. This control made it possible for the lofty valuation to be placed on Instagram and for

the deal to be negotiated so rapidly. Indeed, the Instagram offer price may have reflected the euphoria preceding the

Facebook IPO. The heady environment immediately prior to the Facebook IPO also may have convinced the Instagram

shareholders that they had little to lose and much to gain by accepting a mostly stock deal involving a fixed share–exchange

ratio. That is, the number of Facebook shares exchanged for each Instagram share would remain unchanged, despite any

appreciation (depreciation) in Facebook shares between the signing of the agreement and the closing of the deal.

Boston Scientific Overcomes Johnson & Johnson to Acquire Guidant—A Lesson in Bidding Strategy

Johnson & Johnson, the behemoth American pharmaceutical company, announced an agreement in December 2004 to

acquire Guidant for $76 per share for a combination of cash and stock. Guidant is a leading manufacturer of implantable

heart defibrillators and other products used in angioplasty procedures. The defibrillator market has been growing at 20

percent annually, and J&J desired to reenergize its slowing growth rate by diversifying into this rapidly growing market.

Soon after the agreement was signed, Guidant’s defibrillators became embroiled in a regulatory scandal over failure to

inform doctors about rare malfunctions. Guidant suffered a serious erosion of market share when it recalled five models of

its defibrillators.

The subsequent erosion in the market value of Guidant prompted J&J to renegotiate the deal under a material adverse

change clause common in most M&A agreements. J&J was able to get Guidant to accept a lower price of $63 a share in

mid-November. However, this new agreement was not without risk.

The renegotiated agreement gave Boston Scientific an opportunity to intervene with a more attractive informal offer on

December 5, 2005, of $72 per share. The offer price consisted of 50 percent stock and 50 percent cash. Boston Scientific, a

Despite the more favorable offer, Guidant’s board decided to reject Boston Scientific’s offer in favor of an upwardly

revised offer of $71 per share made by J&J on January 11, 2005. The board continued to support J&J’s lower bid, despite

the furor it caused among big Guidant shareholders. With a market capitalization nine times the size of Boston Scientific,

the Guidant board continued to be enamored with J&J’s size and industry position relative to Boston Scientific.

Boston Scientific realized that it would be able to acquire Guidant only if it made an offer that Guidant could not refuse

between the signing of the agreement and the actual closing. This was indeed a possibility, since the J&J offer did not

include a collar arrangement.

Boston Scientific decided to boost the new bid to $80 per share, which it believed would deter any further bidding from

J&J. J&J had been saying publicly that Guidant was already “fully valued.” Boston Scientific reasoned that J&J had created

a public relations nightmare for itself. If J&J raised its bid, it would upset J&J shareholders and make it look like an

undisciplined buyer. J&J refused to up its offer, saying that such an action would not be in the best interests of its

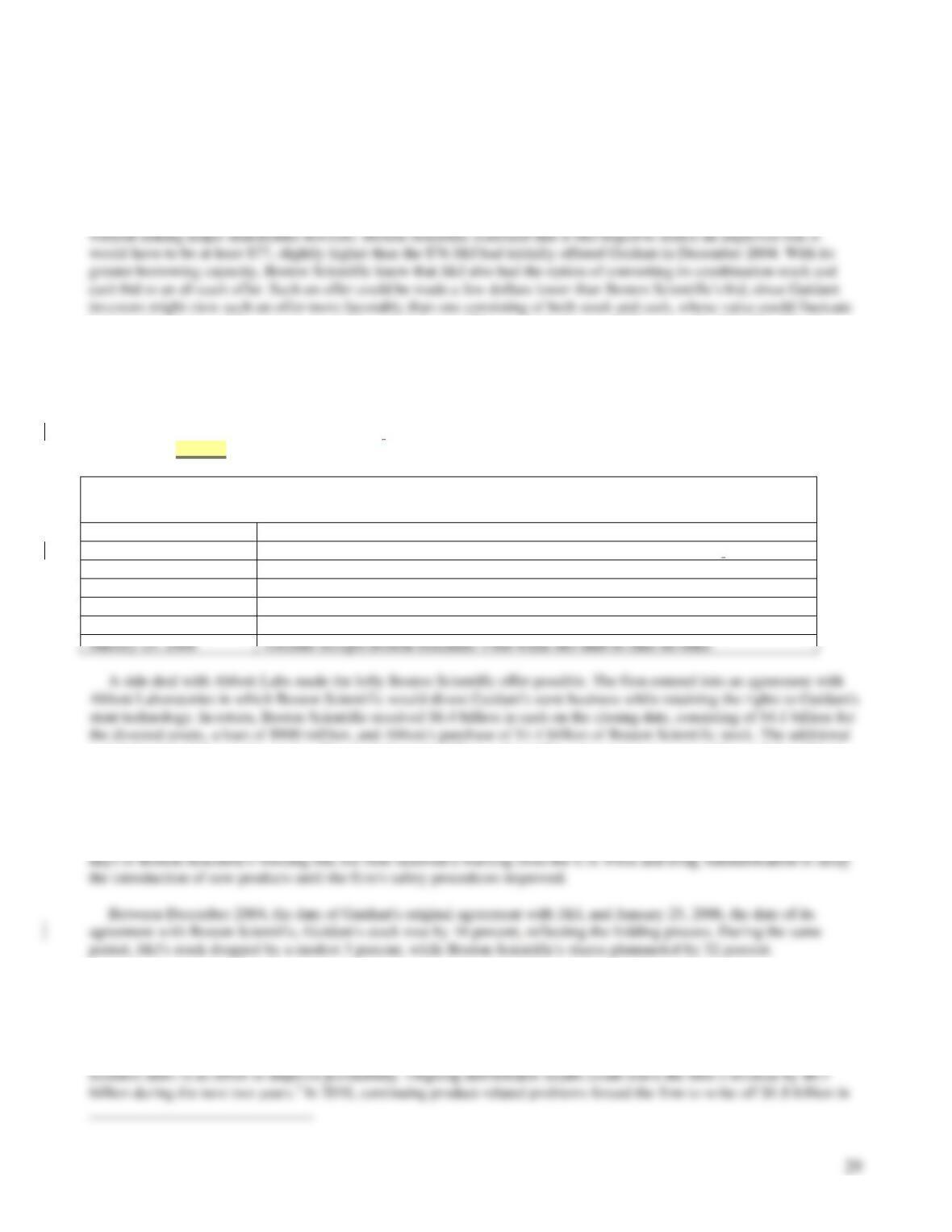

shareholders. Table 1 summarizes the key events timeline.

Table 1

Boston Scientific and Johnson & Johnson Bidding Chronology

Date

Comments

December 15, 2004

J&J reaches agreement to buy Guidant for $25.4 billion in stock and cash.

November 15, 2005

Value of J&J deal is revised downward to $21.5 billion.

December 5, 2005

Boston Scientific offers $25 billion.

January 11, 2006

Guidant accepts a J&J counteroffer valued at $23.2 billion.

January 17, 2006

Boston Scientific submits a new bid valued at $27 billion.

January 25, 2006

Guidant accepts Boston Scientific’s bid when J&J fails to raise its offer.

cash helped fund the purchase price. This deal also helped Boston Scientific gain regulatory approval by enabling Abbott

Labs to become a competitor in the stent business. Merrill Lynch and Bank of America each would lend $7 billion to fund a

portion of the purchase price and provide the combined firms with additional working capital.

To complete the transaction, Boston Scientific paid $27 billion, consisting of cash and stock, to Guidant shareholders

and another $800 million as a breakup fee to J&J. In addition, the firm is burdened with $14.9 billion in new debt. Within

As a result of product recalls and safety warnings on more than 50,000 Guidant cardiac devices, the firm‘s sales and

profits plummeted. Between the announcement date of its purchase of Guidant in December 2005 and year-end 2006,

Boston Scientific lost more than $18 billion in shareholder value. In acquiring Guidant, Boston Scientific increased its total

shares outstanding by more than 80 percent and assumed responsibility for $6.5 billion in debt, with no proportionate

increase in earnings. In early 2010, Boston Scientific underwent major senior management changes and spun off several

impaired goodwill associated with the Guidant acquisition. At less than $8 per share throughout most of 2010, Boston

Scientific’s share price is about one-fifth of its peak of $35.55 on December 5, 2005, the day the firm announced its bid for

Guidant.

Discussion Questions

1. What were the key differences between J&J’s and Boston Scientific’s bidding strategy? Be specific.

Answer: J&J’s style could be characterized as self–assured and reactive and Boston Scientific’s as

opportunistic and nimble. J&J was willing to reopen their bid for Guidant by executing the material adverse

change clause in the agreement of purchase and sale and to renegotiate aggressively a much lower offer price.

2. What might J&J have done differently to avoid igniting a bidding war?

Answer: Immediately following its announcement that it had reached an agreement to be acquired by Johnson

3. What evidence is given that J&J may not have taken Boston Scientific as a serious bidder?

Answer: J&J announced publicly that Guidant was fully valued at its cash and stock bid of $76 per Guidant

share. The firm refused to raise its bid to the higher Boston Scientific bid of $80, possibly believing that the

7. Explain how differing assumptions about market growth, potential synergies, and the size of the potential liability

related to product recalls affected the bidding?

Answer: The potential product related liability initiated the bidding war as it provided Boston Scientific with

an opportunity to intervene in what had been a signed agreement. J&J and Boston Scientific simply had

Buyer Consortium Wins Control of ABN Amro

The biggest banking deal on record was announced on October 9, 2007, resulting in the dismemberment of one of Europe’s

largest and oldest financial services firms, ABN Amro (ABN). A buyer consortium consisting of The Royal Bank of

Scotland (RBS), Spain‘s Banco Santander (Santander), and Belgium’s Fortis Bank (Fortis) won control of ABN, the largest

bank in the Netherlands, in a buyout valued at $101 billion.

European banks had been under pressure to grow through acquisitions and compete with larger American rivals to avoid

becoming takeover targets themselves. ABN had been viewed for years as a target because of its relatively low share price.

However, rival banks were deterred by its diverse mixture of businesses, which was unattractive to any single buyer. Under

would own the Asian and investment banking units. Merrill Lynch served as the sole investment advisor for the group’s

participants. Caught up in the global capital market meltdown, Fortis was forced to sell the ABN Amro assets it had

acquired to its Dutch competitor ING in October 2008.

Discussion Questions:

1. In your judgment, what are likely to be some of the major challenges in assembling a buyer consortium to acquire

and subsequently dismember a target firm such as ABN Amro? In what way do you thing the use of a single

investment advisor might have addressed some of these issues?

Answer: Finding willing and financially able partners with a synergistic fit to a specific target firm is difficult.

2. The ABN Amro transaction was completed at a time when the availability of credit was limited due to the sub-

prime mortgage loan problem originating in the United States. How might the use of a group rather than a single

buyer have facilitated the purchase of ABN Amro?

3. The same outcome could have been achieved if a single buyer had reached agreement with other banks to acquire

selected pieces of ABN before completing the transaction. The pieces could then have been sold at the closing.

Why might the use of the consortium been a superior alternative?

Answer: Pre-selling businesses before closing is a technique that makes sense mostly for target firms whose assets

are managed largely independently. Consequently, such assets can be easily divested upon closing to other parties

Pfizer Acquires Wyeth Labs Despite Tight Credit Markets

Pfizer and Wyeth began joint operations on October 22, 2009, when Wyeth shares stopped trading and each Wyeth share

was converted to $33 in cash and 0.985 of a Pfizer share. Valued at $68 billion, the cash and stock deal was first announced

cholesterol-lowering drug Lipitor, which accounted for 25 percent of the firm’s $52 billion in 2008 revenue. Pfizer also

faces 14 other patent expirations through 2014 on drugs that, in combination with Lipitor, contribute more than one-half of

the firm’s total revenue. Pfizer is not alone, Merck, Bristol-Myers Squibb, and Eli Lilly are all facing significant revenue

reduction due to patent expirations during the next five years as competition from generic drugs undercuts their pricing.

Wyeth will also be losing its patent protection on its top-selling drug, the antidepressant Effexor XR.

financing and $26 billion in cash and marketable securities. Pfizer also announced plans to cut its quarterly dividend in half

to $0.16 per share to help finance the transaction. However, there were still questions about the firm’s ability to complete

the transaction in view of the turmoil in the credit markets.

Many transactions that were announced during 2008 were never closed because buyers were unable to arrange financing

and would later claim that the purchase agreement had been breached due to material adverse changes in the business

differences over price or strategy but rather under what circumstances Pfizer could back out of the deal. Under the terms of

the final agreement, Pfizer would have been liable to pay Wyeth $4.5 billion if its credit rating dropped prior to closing and

it could not finance the transaction. At about 6.6 percent of the purchase price, the termination fee was about twice the

normal breakup fee for a transaction of this type.

What made this deal unique was that the failure to obtain financing as a pretext for exit could be claimed only under

Using Form of Payment as a Takeover Strategy:

Chevron’s Acquisition of Unocal

Unocal ceased to exist as an independent company on August 11, 2005 and its shares were de-listed from the New York

Stock Exchange. The new firm is known as Chevron. In a highly politicized transaction, Chevron battled Chinese oil–

producer, CNOOC, for almost four months for ownership of Unocal. A cash and stock bid by Chevron, the nation’s second

largest oil producer, made in April valued at $61 per share was accepted by the Unocal board when it appeared that

33

the merger agreement with a new cash and stock bid valued at $63 per share in late July. Despite the significant difference

in the value of the two bids, the Unocal board recommended to its shareholders that they accept the amended Chevron bid

in view of the growing doubt that U.S. regulatory authorities would approve a takeover by CNOOC.

In its strategy to win Unocal shareholder approval, Chevron offered Unocal shareholders three options for each of their

option (3) would attract those Unocal shareholders who were interested in cash but also wished to enjoy any appreciation in

the stock of the combined companies.

The agreement of purchase and sale between Chevron and Unocal contained a “proration clause.” This clause enabled

Chevron to limit the amount of total cash it would payout under those options involving cash that it had offered to Unocal

10.1 million elected the cash and stock combination. No election was made for approximately .3 million shares. Based on

these results, the amount of cash needed to satisfy the number shareholders electing the all–cash option far exceeded the

amount that Chevron was willing to pay. Consequently, as permitted in the merger agreement, the all-cash offer was

prorated resulting in the Unocal shareholders who had elected the all-cash option receiving a combination of cash and stock

rather than $69 per share. The mix of cash and stock was calculated as shown in Exhibit 1.

Exhibit 1. Prorating All-Cash Elections

1. Determine the available cash election amount (ACEA): Aggregate cash amount minus the amount of cash

to be paid to Unocal shareholders selecting the combination of cash and stock (i.e., Option 3).

ACEA = $27.60 x 272 million (Unocal shares outstanding) – 10.1

2. Determine the elected cash amount (ECA): Amount equal to $69 multiplied by the

number of shares of Unocal common stock electing the all-cash option.

3. Determine the cash proration factor (CPF): ACEA/ECA

CPF = $7.2 / $16.7 = .4311

4. Determine the prorated cash merger consideration (PCMC): An amount in cash equal

to $69 multiplied by the cash proration factor.

5. Determine the prorated stock merger consideration (PSMC): 1.03 multiplied by 1 – CPF.

34

PSMC = 1.03 x (1- .4311) = .5860

6. Determine the stock and cash mix (SCM): Sum of the prorated cash (PCMC) and stock

(PSMC) merger considerations exchanged for each share of Unocal common stock.

SCM = $29.74 + .5860 of a Chevron share

stock options are 22.1 and 242 million, respectively. This is the reverse of what actually happened. The mix of stock and

cash would have been prorated as shown in Exhibit 2.

Exhibit 12. Prorating All-Stock Elections

1. Determine the available cash election amount (ACEA): Same as step 1 above.

ACEA = $7.2 billion

2. Determine the elected cash amount (ECA): Amount equal to $69 multiplied by the number of shares of

Unocal common stock electing the all-cash option.

3. Determine the excess cash amount (EXCA): Difference between ACEA and ECA.

EXCA = $7.2 – $1.5 = $5.7

4. Determine the prorated cash merger consideration (PCMC): EXCA divided by number of Unocal shares

elected the all-stock option.

5. Determine the stock proration factor (SPF): $69 minus the prorated cash merger

consideration divided by $69.

6. Determine the prorated stock price consideration (PSPC): The number of shares of

Chevron stock equal to 1.03 multiplied by the stock proration factor.

7. Determine the stock and cash mix (SCM): Each Unocal share to be exchanged in an

all-stock election is converted into the right to receive the prorated cash merger

consideration and the prorated stock merger consideration.

SCM = $23.55 + .6785 of a Chevron share for each Unocal share

It is typical of large transactions in which the target has a large, diverse shareholder base that acquiring firms offer

target shareholders a “menu” of alternative forms of payment. The objective is to enhance the likelihood of success by

Discussion Questions

1. What was the form of payment employed by both bidders for Unocal? In your judgment, why were they

different? Be specific.

Answer: Chevron offered Unocal shareholders three options including all cash, all stock, and a combination of

both. CNOOC countered with an all-cash bid. CNOOC tried to appeal to those Unocal shareholders who wanted