CHAPTER 4.

4.1 Risk Aversion: (Answers to a), b), c), and d) are given together here)

0

Y

2

Y

R

2R Y

2

R

0

Y

2

)Y(‘‘U

0

Y

1

)Y(‘U

Y

1

)Y(U )1(

2

A

R

A

3

2

0

Y

1

Y

R

1R Y

1

R

0

Y

1

)Y(‘‘U

0

Y

1

)Y(‘U

Yln)Y(U )2(

2

A

R

A

2

1

2

A

R

A2

(3) U(Y) Y

U‘(Y) Y 0 0

U‘‘(Y) 1 Y 0

1

R Y

R 1

R1

0

YY

0

Y

R

YR

R

0Yexp)Y(‘‘U

00Yexp)Y(‘U

Yexp)Y(U )4(

R

R

A

2

0

Y

1

Y

R

1R Y

1

R

10Y1)Y(‘‘U

Y)Y(‘U

Y

)Y(U )5(

2

A

R

A

2

1

0RY

Y

R

YR

YY

R

0

Y2

4

Y

R

0Y

Y2

2

R

0

Y2

2

R

02)Y(‘‘U

2

Y0Y2)Y(‘U

0,0,YY)Y(U )6(

A

A

A

R

2

2

A

R

A

2

AR

AR

AR

RR

1

U Y Y 1

Y

RR

U Y exp Y 1 Y

RR

Y1

U Y 1

Y

In the last utility function above, we should better use 1-, so that

1

R

,

Y

1

R

and ,

1

YY

YU RA

1

(look at RR = 1- = ). After this change,

every derivative w.r.t. is positive. If we increase , we increase the level of risk

aversion (both absolute and relative).

4.2. Certainty equivalent .

The problem to be solved is: find x such that

xUYUYU 1

22

1

11

where

1

i

Y

denotes outcome of lottery L1 in state i and

i denotes the probability of state i.

4.3. Risk premium.

The problem to be solved (indifference between insurance and no insurance) is

i

i

EU Y lnY (i) ln 100,000 P

where P is the insurance premium, Yi is the worth in state i and

)i(

is the probability of

state i. The solution to the problem is

P 100,000 exp EU Y

A

111

Ex (2) (4) (9) 4.75

424

%

5)861(

3

1

x

~

EB

2 2 2 2

A

111

(2 4.75) (4 4.75) (9 4.75) 6.6875

424

2222

B)58(

3

1

)56(

3

1

)51(

3

1

= 26/3 =

3

2

8

.

So,

AB

Ex Ex

%%

,

2

B

2

A

Thus we cannot compare the two investment opportunities using the mean-variance

criterion.

(ii) Now let’s compare them under FSD.

Let F(

A

x

~

) be denoted

~

A

x

~

B

x

~

4‘‘24)‘‘1(6‘‘10.5

1.1‘‘2

,

55.

2

1.1

‘‘

Thus the probability premium is

05.50.55.

The probability premium has fallen became the agent is wealthier in the case and is

4.7 No. Reworking the data of Table 3.3 shows that it is not always the case that

0dt)t(F)t(F

x

034

.

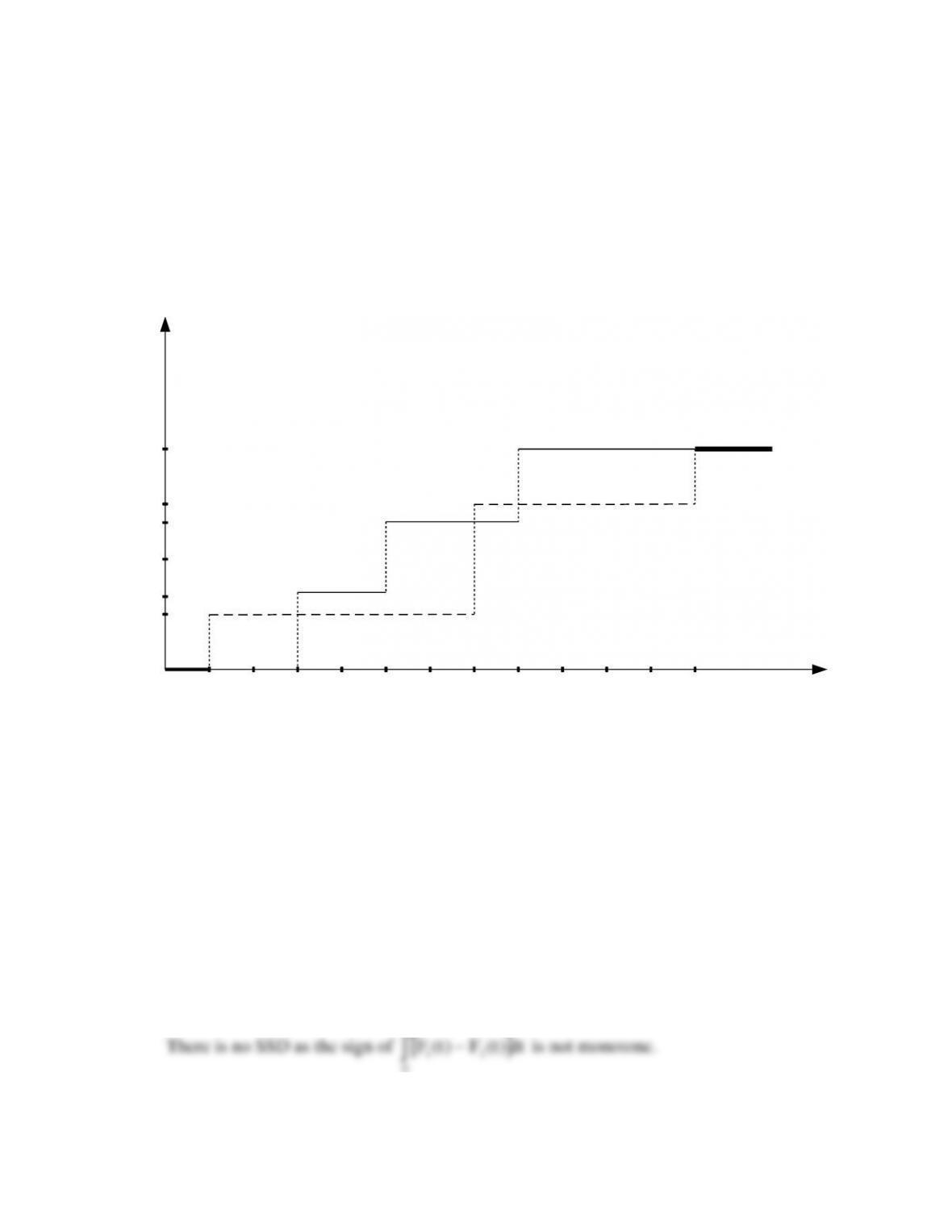

4.8 a) State by state dominance : no.

b) FSD : yes. See graph

Probability

1

1/3

2/3

10 20

z

~

z

~

y

~

y

~

and

These two notions are not equivalent.

4.9 Certainty equivalent.

The problem to be solved is: find Y such that

–

1

0

–

1

0

0

1

0

2000Y

Y500Y1000Y

500Y

2

1000Y

Y2

500Y

2

1000Y1000Y

1000Y1000Y

500Y

2

1000Y

1

1000Y

1

500YU1000YU

2

1

1000YU

2

1

222

22

4.10. Risk premium.

The problem to be solved is: find P such that

.expYP

1000Yln1000Yln

2

1

expPY

PYln1000Yln1000Yln

2

1

where P is the insurance premium.

50.0100000YP

13.5010000YP

The utility function is DARA, so the outcome (smaller premium associated with higher

wealth) was expected.

4.11. Case 1 Case 2 Case 3

ba

ba

EE

ba

ba

EE

ba

ba

EE

Case 1: cannot conclude with FSD, but B SSD A

Case 2: A FSD B, A SSD B

Case 3: cannot conclude (general case)

4.12 a.

))(LY(EU)CEY(U

)000,2000,10(

)000,1000,10(

)CE000,10( 2.2.2.

2.

)000,6000,10(

15.

2.

)000,5000,10(

20.

2.

)000,3000,10(

35. 2.2.2.

173846.)CE000,10(2.

752.5

173846.

1

)CE000,10(2.

CE = -3702.2

3450

)6000(15.)5000(2.)3000(35.)2000(2.)1000(1.L

~

E

)z

~

,y()z

~

(E)y,z

~

(CE

2.252)z

~

,y(

If the agent were risk neutral the CE = – 3450

b. If

0)y(‘‘U,0)y(‘U

, the agent loves risk. The premium would be negative here.

4.13 Current Wealth :

Y+

-L

0

1

Insurance Policy :

– ph

h

0

1

Certainly

1p

a. Agent solves

)phyln()1()hLphyln(max

h

The F.O.C. is

phy

)1(p

)p1(hLy

)p1(

, which solves for

)LY(

p1

1

p

Yh

Note : if p = 0, h =

; if

Yph,1

.

b. expected gain is

Lph

c.

L)LY(

p1

1

p

Ypph

p

d.

)LY(

p1

1

p

Yh

)LY(

1

1

Yh

= L.

The agent will perfectly insure. None ; this is true for all risk averse individuals.

4.14

)x

~

(,x

~

)z

~

(,z

~

a.

4.64.2321)2(.12)3(.10)4(.5)1(.10x

~

E

7.538.5.14.)1(.30)2(.4)5(.3)2(2.z

~

E

22222

x

~)4.612(2.)4.610(3.)4.65(4.)4.610(1.

= 26.9 + .78 + 3.9 + 6.27

= 37.85

15.6

x

~

22222

z

~)7.530(1.)7.54(2.)7.53(5.)7.52(2.

= 2.74 + 3.65 + .58 + 59.04

= 66.01

12.8

z

~

There is mean variance dominance in favor of

x

~

:

z

~

x

~

and z

~

Ex

~

E

. The latter is due to the large outlying payment of 30.

b. 2nd order stochastic dominance :

r

)r(Fx

~

r

0xdt)t(F

)r(Fz

~

r

0zdt)t(F

r

0zx dt)t(F)t(F

-10

.1

.1

0

0

.1

-9

.1

.2

0

0

.2

-8

.1

.3

0

0

.3

-7

.1

.4

0

0

.4

-6

.1

.5

0

0

.5

-5

.1

.6

0

0

.6

-4

.1

.7

0

0

.7

-3

.1

.8

0

0

.8

-2

.1

.9

0

0

.9

-1

.1

1.0

0

0

1.0

0

.1

1.1

0

0

1.1

1

.1

1.2

0

0

1.2

2

.1

1.3

.2

.2

1.1

3

.1

1.4

.7

.9

.5

4

.1

1.5

.9

1.8

-.3

4.15

Y

G

B

1

lottery

initial wealth

a. If he already owns the lottery,

s

P

must satisfy

)BY(U)1()GY(U)PY(U s

s

P

)BY(U)1()GY(U)PY(U s

b

P

:

)BPY(U)1()GPY(U)Y(U bb

)BPY)(1()GPY(Y bb

B)1(GPb

4.16 Mean-variance: Ex1 = 6.75,

22.15)( 2

1

; Ex2 = 5.37,

25.4)( 2

2

; no dominance.

FSD: No dominance:

1

4321

2/3

1/4

1/3

1/2

1

98765

1 and 2

2

121110

3/4

SSD:

x

dt)t(f

x

01

dt)t(F

x

01

dt)t(f

x

02

dt)t(F

x

02

dt)t(F)t(F

x

021

0

0

0

0

0

0

1

.25

.25

0

0

.25

2

.25

.50

0

0

.50

3

.25

.75

0

0

.75

4

.25

1

.33

.33

.67

5

.25

1.25

.33

.66

.67

6

.25

1.50

.66

1.32

.18

7

.50

2

.66

1.98

.02

8

.50

2.50

1

2.98

-.48

x

0

21 )()(

Using Expected utility. Generally speaking, one would expect the more risk averse individuals to prefer investment

2 while less risk averse agents would tend to favor investment 1