CHAPTER 14.

14.1 a.

.17

.07

.09

1.51.5

A

C

B

i

Er

i

b

b. Using A, B ; we want

BAAAP b)w1(bw0b

)1)(w1()5(.w0 AA

1w,2w;1w5. BAA

Using B, C :

CCBBP bwbw0b

)5.1(w)1(w0 CB

BB w5.15.1w0

2w,3w;5.1w5. CBB

c. We need to find the proportions of A and C that give the same b as asset B.

Thus,

CAAAB b)w1(bw1b

)5.1)(w1()5(.w1 AA

2

1

w;

2

1

wCA

With these proportions :

CAP Er

2

1

Er

2

1

Er

B

Er09.12.)17(.

2

1

)07(.

2

1

B1P eF109.R 1

B

w

,

0)e,ecov( BP

.

Now we assume these assets are each well diversified portfolios so that

0ee BP

.

2

d. As a result the prices of A, C will rise and their expected returns fall. The opposite will

happen to B.

e.

.14

.06

.10

1.51.5

i

Er

i

b

A

Er

B

Er

C

Er

A

b

B

b

C

b

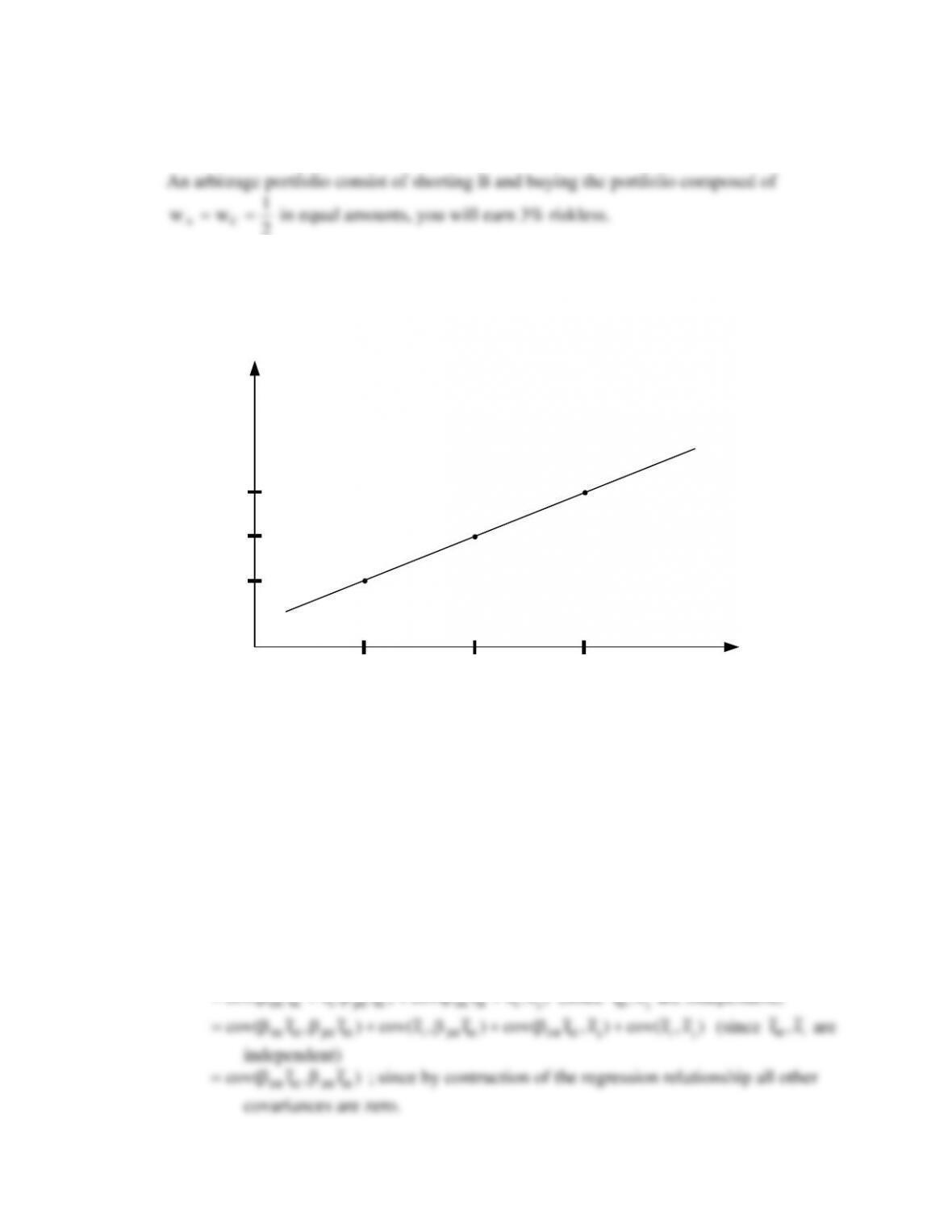

There is no longer an arbitrage opportunity : expected returns are consistent with relative

systematic risk.

14.2. a. Since

0),r

~

cov( jM

,

)var()r

~

var()var( jMjMj

2

j

2j

2

M

2

jM

2j

2

M

2

jM

0

b.

ij i iM M i j jM M j

cov( r , r )

% % % %

)

~

r

~

,

~

r

~

cov( jMjMiMiM

(constants do not affect covariances)

)

~

,

~

r

~

cov()r

~

,

~

r

~

cov( jiMiMMjMiMiM

(since

jM ~

,r

~

are independent)

covariances are zero.

2

MjiMMjMiM )r

~

,r

~

cov(

14.3. The CAPM model is an equilibrium model built on structural hypotheses about investors’

preferences and expectations and on the condition that asset markets are at equilibrium.

The APT observes market prices on a large asset base and derives, under the hypothesis

compatible if the market portfolio were simply another way to synthesize the several

factors identified by the APT: under the conditions spelled out in section 12.x, the two

14.4. The main distinction is that the A-D theory is a full structural general equilibrium theory

while the APT is a no-arbitrage approach to pricing. The former prices all assets from

securities and extract from them the prices of the fundamental securities. Use the latter

for pricing other assets or arbitrary cash flows.

14.5 True. The APT is agnostic about beliefs. It simply requires that the observed prices and

returns, presumably the product of a large number of agents trading on the basis of

14.6

a. From the main APT equation and the problem data, one obtains the following system :

This system can easily be solved for

b. (i) If there is a risk free asset one must have

)rr(rr fMPifPii

.

Thus

4

1

1P1P1 41

, and

2

1

2P2P2 42

.

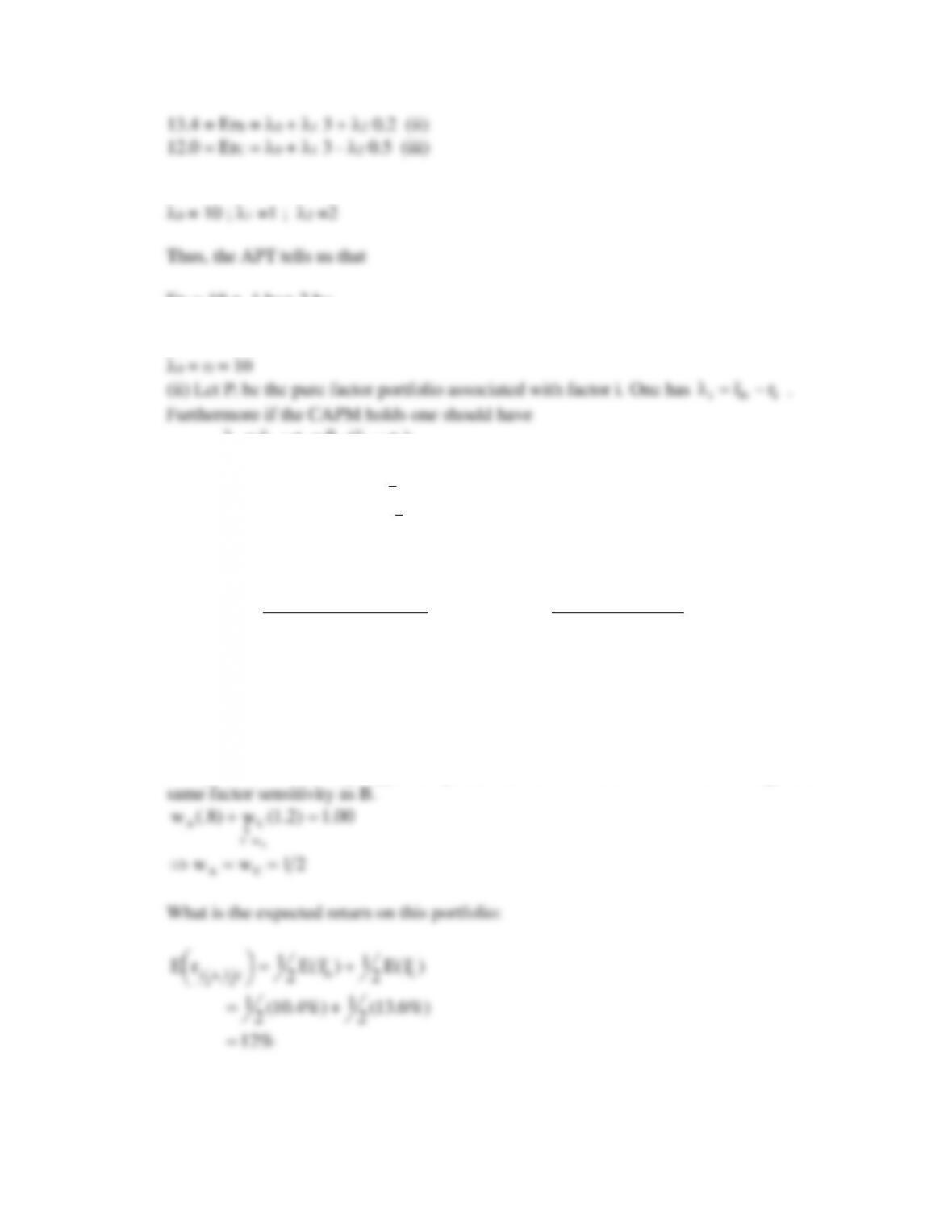

14.7.

Expected APT Return

Expected Returns

A

r

= 4%+.8(8%) = 10.4%

10.4%

B

r

= 4%+1(8%) = 12.0%

12.0%

C

r

= 4%+1.2(8%) = 13.6%

13.6%

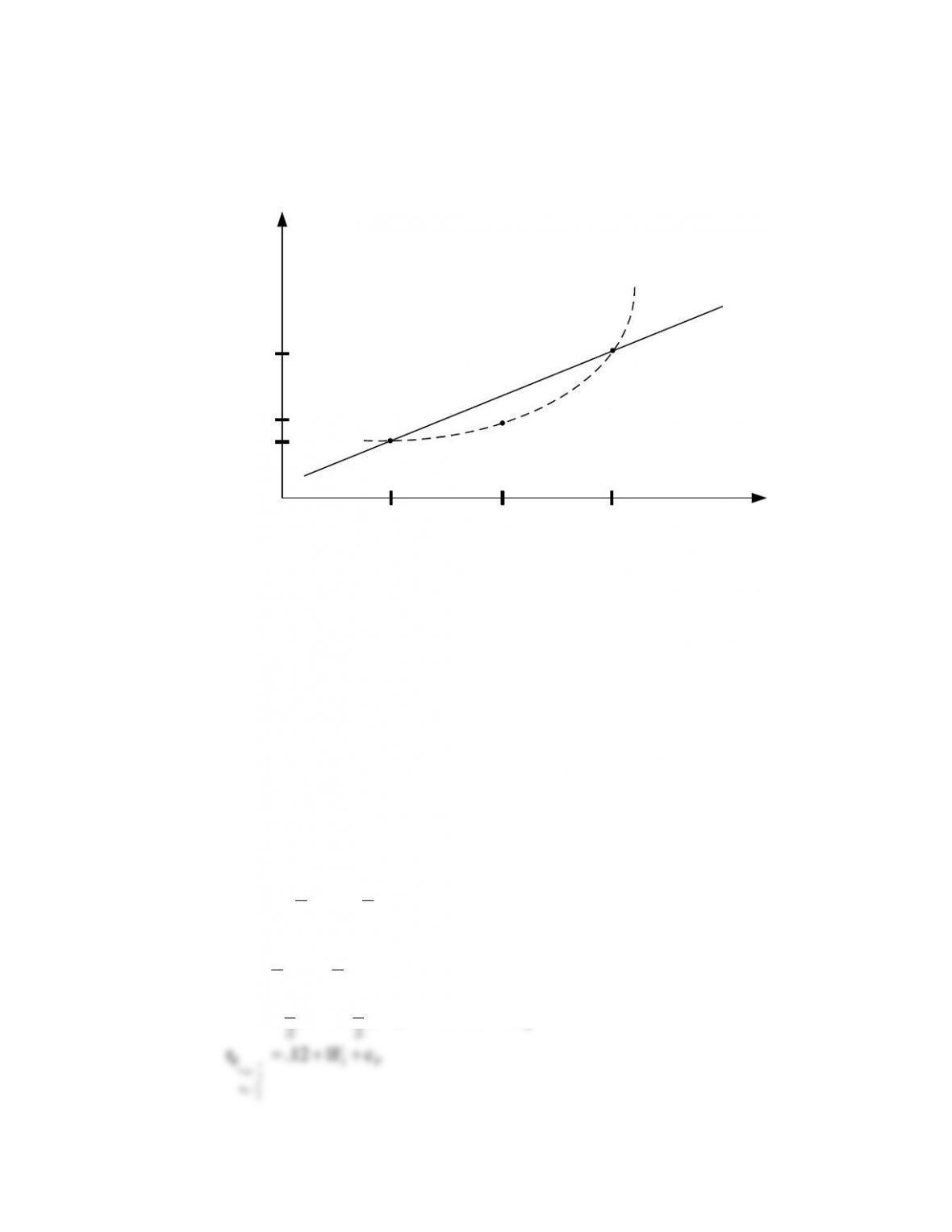

The Expected return of B is less than what is consistent with the APT.

This provides an arbitrage opportunity. Consider a combination of A and C that gives the

This clearly provides an arbitrage opportunity: short portfolio B, buy a portfolio of ½ A

and ½ C.

14.8

That diversifiable risk is not priced has long been considered as the main lesson of the CAPM. While defining

systematic risk differently (in terms of the consumption portfolio rather than the market portfolio), the CCAPM

leads to the same conclusion. So does the APT with possibly yet another definition for systematic risk, at least in the