Chapter 09 – Interest Rate Risk II

9-32

Education.

Price – market Price – duration Amount

determined estimation of error

c. Given that convexity is 212.4, what are the bond price predictions in each of the four

cases using the duration plus convexity relationship? What is the amount of error in

these predictions?

Price Price

Price duration & duration &

market convexity convexity Amount

determined estimation estimation of error

At +0.10%: $988.85 -$11.15 $988.85 $0.00

Chapter 09 – Interest Rate Risk II

9-33

d. Diagram and label clearly the results in parts (a), (b) and (c).

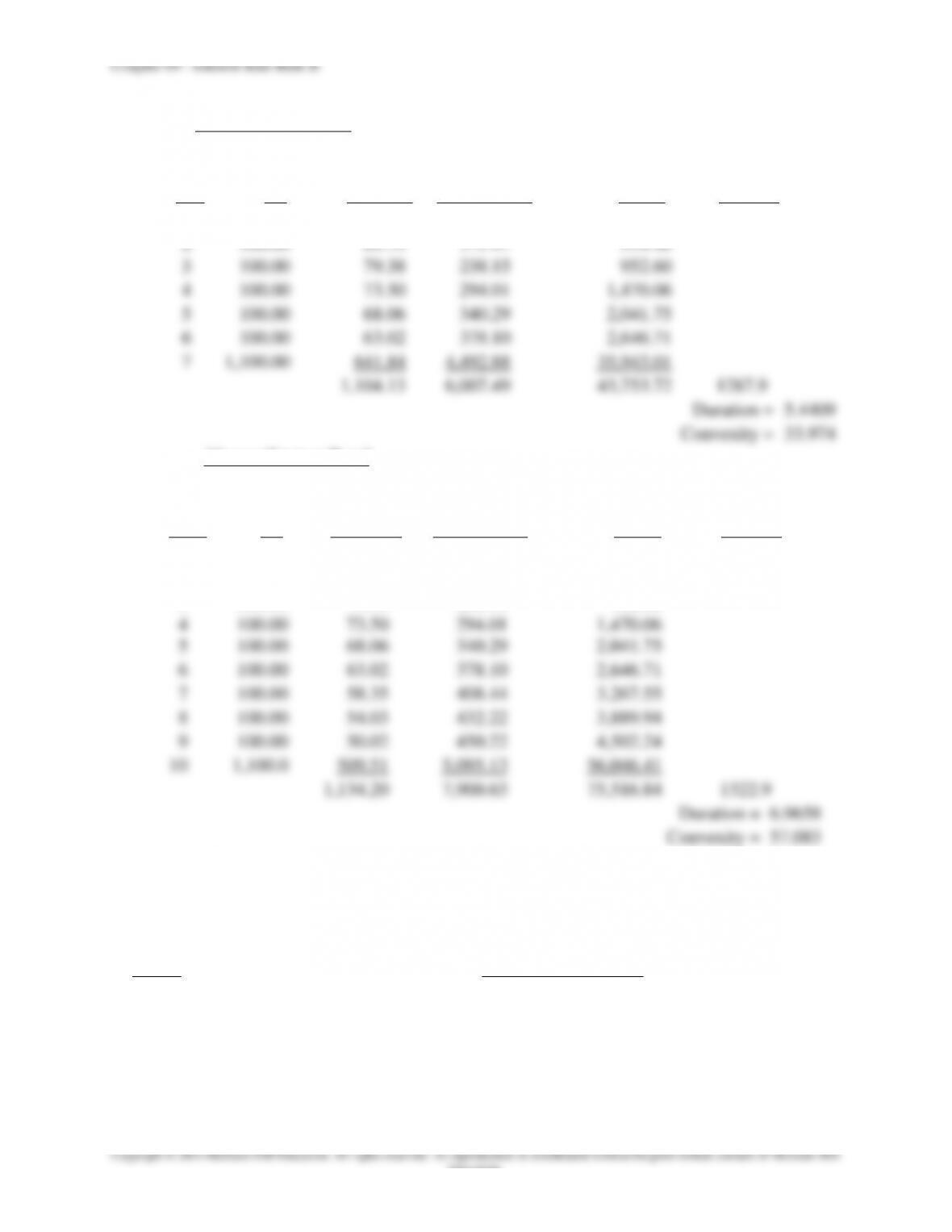

35. Estimate the convexity for each of the following three bonds, all of which trade at yield to

maturity of 8 percent and have face values of $1,000.

A 7-year, zero-coupon bond.

A 7-year, 10 percent annual coupon bond.

A 10-year, 10 percent annual coupon bond that has a duration value of 6.994 years (i.e.,

approximately 7 years).

$600

$1,000

$1,400

46810 12

Percent Yield-to-Maturity

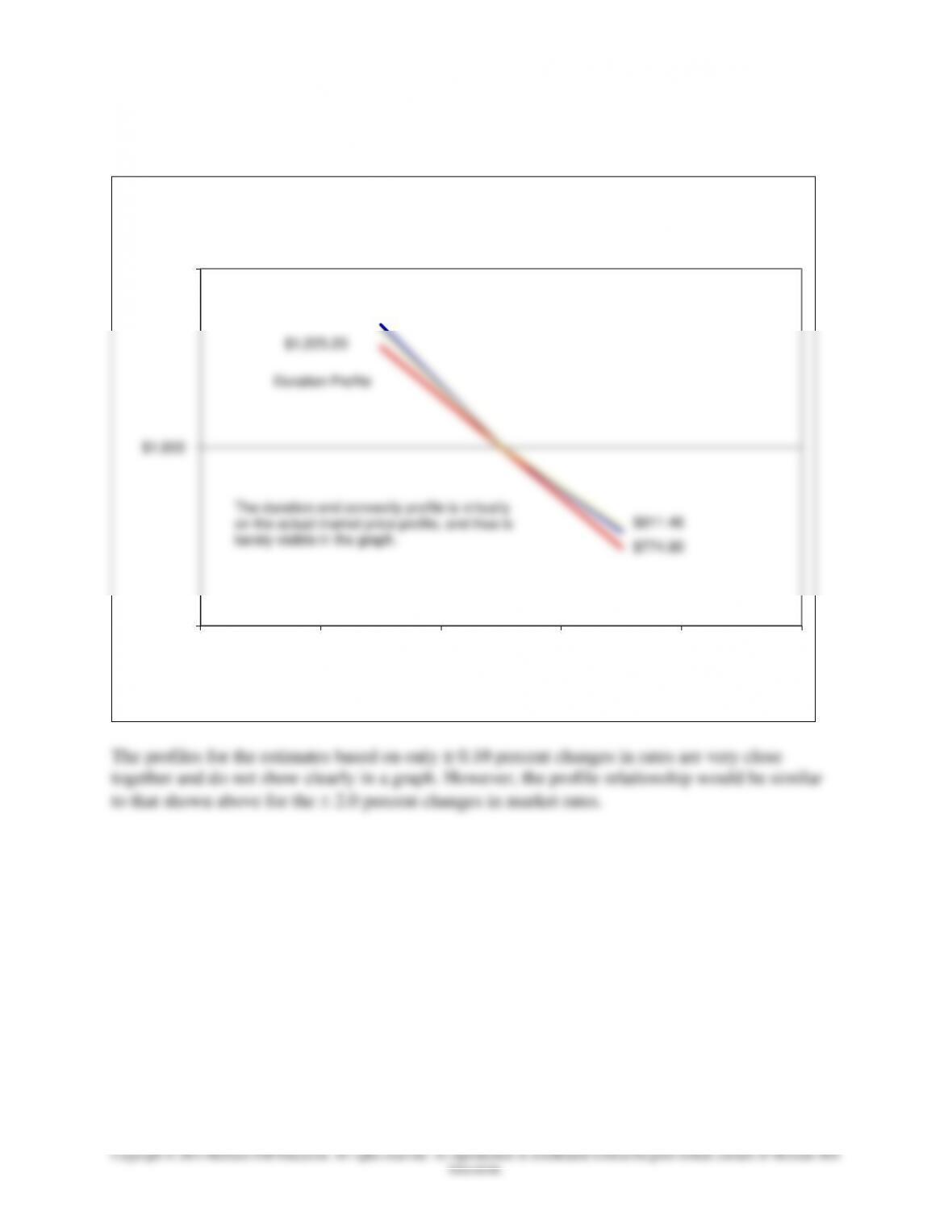

Rate-Price Relationships

Actual Market Price

Duration Profile

The duration and convexity profile is virtually

on the actual market price profile, and thus is

barely visible in the graph.

$811.46

$774.80

$1,275.30

$1,225.20

Chapter 09 – Interest Rate Risk II

Market Value Market Value Capital Loss + Capital Gain

at 8.01 percent at 7.99 percent Divided by Original Price

9-35

Education.

7-year Coupon Bond

Par value =

$1,000

Coupon =

10%

R =

8%

Maturity =

7 years

t .

CF

PVof CF

PV of CF x t

x(1+t)

x(1+R)2

1

100.00

92.59

92.59

185.19

2

100.00

85.73

171.47

514.40

3

100.00

79.38

238.15

952.60

4

100.00

73.50

294.01

1,470.06

5

100.00

68.06

340.29

2,041.75

6

100.00

63.02

378.10

2,646.71

7

1,100.00

641.84

4,492.88

35,943.01

1,104.13

6,007.49

43,753.72

1287.9

Duration

=

5.4409

Convexity

=

33.974

10-year Coupon Bond

Par value =

$1,000

Coupon =

10%

R =

8%

Maturity =

10 years

t .

CF

PV of CF

PV of CF x t

x(1+t)

x(1+R)2

1

100.00

92.59

92.59

185.19

2

100.00

85.73

171.47

514.40

3

100.00

79.38

238.15

952.60

4

100.00

73.50

294.01

1,470.06

5

100.00

68.06

340.29

2,041.75

6

100.00

63.02

378.10

2,646.71

7

100.00

58.35

408.44

3,267.55

8

100.00

54.03

432.22

3,889.94

9

100.00

50.02

450.22

4,502.24

10

1,100.0

509.51

5,095.13

56,046.41

1,134.20

7,900.63

75,516.84

1322.9

Duration

=

6.9658

Convexity

=

57.083

Integrated Mini Case: Calculating and Using Duration GAP

State Bank’s balance sheet is listed below. Market yields and durations (in years) are in

parenthesis, and amounts are in millions.

Assets Liabilities and Equity

Cash $20 Demand deposits $250

Fed funds (5.05%, 0.02) 150 MMDAs (4.5%, 0.50)

T-bills (5.25%, 0.22) 300 (no minimum balance requirement) 360

T-bonds (7.50%, 7.55) 200 CDs (4.3%, 0.48) 715

Consumer loans (6%, 2.50) 900 CDs (6%, 4.45) 1,105

C&I loans (5.8%, 6.58) 475 Fed funds (5%, 0.02) 515

Chapter 09 – Interest Rate Risk II

9-36

Education.

Fixed-rate mortgages (7.85%, 19.50) 1,200 Commercial paper (5.05%, 0.45) 400

Variable-rate mortgages, Subordinated debt:

repriced @ quarter (6.3%, 0.25) 580 Fixed-rate (7.25%, 6.65) 200

Premises and equipment 120 Total liabilities $3,545

Equity 400

Total assets $3,945 Total liabilities and equity $3,945

a. What is State Bank’s duration gap?

b. Use these duration values to calculate the expected change in the value of the assets and

liabilities of State Bank for a predicted increase of 1.5 percent in interest rates.

c. What is the change in equity value forecasted from the duration values for a predicted increase

in interest rates of 1.5 percent?

Integrated Mini Case Chapters 8 and 9: Calculating and Using Repricing and Duration GAP

Chapter 09 – Interest Rate Risk II

9-37

Education.

State Bank’s balance sheet is listed below. Market yields and durations (in years) are in

parenthesis, and amounts are in millions.

Assets Liabilities and Equity

Cash $31 Demand deposits $253

Fed funds (2.05%, 0.02) 150 Savings accounts (0.5%, 1.25) 50

3-month T-bills (3.25%, 0.22) 200 MMDAs (3.5%, 0.50)

8-year T-bonds (6.50%, 7.55) 250 (no minimum balance requirement) 460

5-year munis (7.20%, 4.25) 50 3-month CDs (3.2%, 0.20) 175

6-month consumer loans (5%, 0.42) 250 1-year CDs (3.5%, 0.95) 375

5-year car loans (6%, 3.78) 350 5-year CDs (5%, 4.85) 350

7-month C&I loans (4.8%, 0.55) 200 Fed funds (2%, 0.02) 225

2-year C&I loans (4.15%, 1.65) 275 Repos (2%, 0.05) 290

Fixed-rate mortgages (5.10%, 0.48) 6-month commercial paper

(maturing in 5 months) 450 (4.05%, 0.55) 300

Fixed-rate mortgages (6.85%, 0.85) Subordinate notes:

(maturing in 1 year) 300 1-year fixed rate (5.55%, 0.92) 200

Fixed-rate mortgages (5.30%, 4.45) Subordinated debt:

(maturing in 5 years) 275 7-year fixed rate (6.25%, 6.65) 100

Fixed-rate mortgages (5.40%, 18.25) Total liabilities $2,778

(maturing in 20 years) 355

Premises and equipment 20 Equity 3078

Total assets $3,156 Total liabilities and equity $3,156

a. What is the repricing gap if the planning period is six months? One year?

Assets Repricing period

Cash $31 Not rate sensitive

Fed funds (2.05%) 150 6-months

3-month T-bills (3.25%) 200 6-months

Chapter 09 – Interest Rate Risk II

9-38

Education.

Liabilities and Equity Repricing Period

Demand deposits $253 Not rate sensitive

Savings accounts (0.5%) 50 6-months

MMDAs (3.5%)

(no minimum balance requirement) 460 6-months

b. What is State Bank’s duration gap?

c. What is the impact over the next six months on net interest income if interest rates on RSAs

increase 50 basis points and on RSLs increase 35 basis points? Explain the results.

Chapter 09 – Interest Rate Risk II

9-39

Education.

d. What is the impact over the next year on net interest income if interest rates on RSAs decrease

(increase) 35 basis points and on RSLs decrease (increase) 50 basis points? Explain the results.

e. Use these duration values to calculate the expected change in the value of the assets and

liabilities of State Bank for a predicted decrease of 0.35 percent in interest rates on assets and

0.50 percent on liabilities.

Chapter 09 – Interest Rate Risk II

9-40

Education.

f. What is the change in equity value forecasted from the duration values for decrease of 0.35

percent in interest rates on assets and 0.50 percent on liabilities?

g. Use the duration gap model to calculate the change in equity value if the relative change in all

market interest rates is a decrease of 50 basis points.

Additional Example for Chapter 9

This example is to estimate both the duration and convexity of a 6-year bond paying 5 percent

coupon annually and the annual yield to maturity is 6 percent.

6-year Coupon Bond

Par value =

$1,000

Coupon =

5%

R =

6%

Maturity =

6 years

t .

CF

PV of CF

PV of CF x t

x(1+t)

x(1+R)2

1

$50.00

$47.17

$47.17

$94.34

2

$50.00

$44.50

$89.00

$267.00

3

$50.00

$41.98

$125.94

$503.77

4

$50.00

$39.60

$158.42

$792.09

5

$50.00

$37.36

$186.81

1,120.89

6

$1,050.00

$740.21

$4,441.25

31,088.76

$950.83

$5,048.60

33,866.85

1068.3

Duration

=

5.3097

Convexity

=

31.7

Using the textbook method:

Chapter 09 – Interest Rate Risk II

9-41

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

CX = 108 [(950.3506-950.8268)/950.8268 + (951.3032-950.8268)/950.8268]

= 108[-0.0005007559 + 0.0005501073] = 31.70

What is the effect of a 2 percent increase in interest rates, from 6 percent to 8 percent?

Using Present Values, the percentage change is:

= ($950.8268 – $861.3136)/ $950.8268 = -9.41%

Using the duration formula: ΔMVA = -D x ΔR/(1 + R) + 0.5CX(R)2

= -5.3097 x [(0.02)/1.06] + 0.5(31.7)(0.02)2

= -0.1002 + .0063 = -9.38%

Adding convexity adds more precision. Duration alone would have given the answer of -10.02%.