Chapter 09 – Interest Rate Risk II

9-21

Education.

24. The balance sheet for Gotbucks Bank, Inc. (GBI), is presented below ($ millions):

Assets Liabilities and Equity

Cash $30 Core deposits $20

Federal funds 20 Federal funds 50

Loans (floating) 105 Euro CDs 130

Loans (fixed) 65 Equity 20

Total assets $220 Total liabilities & equity $220

Notes to the balance sheet: The fed funds rate is 8.5 percent, the floating loan rate is LIBOR + 4

percent, and currently LIBOR is 11 percent. Fixed rate loans have five-year maturities, are priced

at par, and pay 12 percent annual interest. The principal is repaid at maturity. Core deposits are

fixed rate for two years at 8 percent paid annually. The principal is repaid at maturity. Euro CDs

currently yield 9 percent.

a. What is the duration of the fixed-rate loan portfolio of Gotbucks Bank?

Five-year Loan (values in millions of $s)

Par value = $65 Coupon rate = 12% Annual payments

R = 12% Maturity = 5 years

t CFt DFt CFt x DFt CFt x DFt x t

b. If the duration of the floating-rate loans and fed funds is 0.36 year, what is the duration

of GBI’s assets?

Chapter 09 – Interest Rate Risk II

9-22

c. What is the duration of the core deposits if they are priced at par?

Two-year Core Deposits (values in millions of $s)

Par value = $20 Coupon rate = 8% Annual payments

R = 8% Maturity = 2 years

t CFt DFt CFt x DFt CFt x DFt x t

d. If the duration of the Euro CDs and fed funds liabilities is 0.401 year, what is the

duration of GBI’s liabilities?

e. What is GBI’s duration gap? What is its interest rate risk exposure?

f. What is the impact on the market value of equity if the relative change in all interest

rates is an increase of 1 percent (100 basis points)? Note that the relative change in

interest rates is R/(1+R) = 0.01.

g. What is the impact on the market value of equity if the relative change in all interest

rates is a decrease of 0.5 percent (-50 basis points)?

h. What variables are available to GBI to immunize the bank? How much would each

variable need to change to get DGAP equal to zero?

9-23

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Immunization requires the bank to have a leverage adjusted duration gap of 0. Therefore, GBI

could reduce the duration of its assets to 0.5032 (0.5535 x 200/220) years by using more fed

funds and floating rate loans. Or GBI could use a combination of reducing asset duration and

increasing liability duration in such a manner that DGAP is 0.

25. Hands Insurance Company issued a $90 million, one-year note at 8 percent add-on annual

interest (paying one coupon at the end of the year) or with an 8 percent yield. The proceeds

were used to fund a $100 million, two-year commercial loan with a 10 percent coupon rate

and a 10 percent yield. Immediately after these transactions were simultaneously closed, all

market interest rates increased 1.5 percent (150 basis points).

a. What is the true market value of the loan investment and the liability after the change in

interest rates?

b. What impact did these changes in market value have on the market value of the FI’s

equity?

c. What was the duration of the loan investment and the liability at the time of issuance?

Two-year Loan (values in millions of $s)

Par value = $100 Coupon rate = 10% Annual payments

R = 10% Maturity = 2 years

t CFt DFt CFt x DFt CFt x DFt x t

d. Use these duration values to calculate the expected change in the value of the loan and

the liability for the predicted increase of 1.5 percent in interest rates.

Chapter 09 – Interest Rate Risk II

9-24

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

The approximate change in the market value of the loan for a 1.5 percent change is:

.300,603,2$000,000,100$*

10.1

015.

*9091.1A −=−=

The expected market value of the loan using

the above formula is $97,396,700.

The approximate change in the market value of the note for a 1.5 percet change is:

.000,250,1$000,000,90$ x

08.1

015.0

x 0.1L −=−=

The expected market value of the note

using the above formula is $88,750,000.

e. What is the duration gap of Hands Insurance Company after the issuance of the asset

and note?

f. What is the change in equity value forecasted by this duration gap for the predicted

increase in interest rates of 1.5 percent?

g. If the interest rate prediction had been available during the time period in which the

loan and the liability were being negotiated, what suggestions would you have offered

to reduce the possible effect on the equity of the company? What are the difficulties in

implementing your ideas?

9-25

Education.

26. The following balance sheet information is available (amounts in thousands of dollars and

duration in years) for a financial institution:

Amount Duration

T-bills $90 0.50

T-notes 55 0.90

T-bonds 176 x

Loans 2,724 7.00

Deposits 2,092 1.00

Federal funds 238 0.01

Equity 715

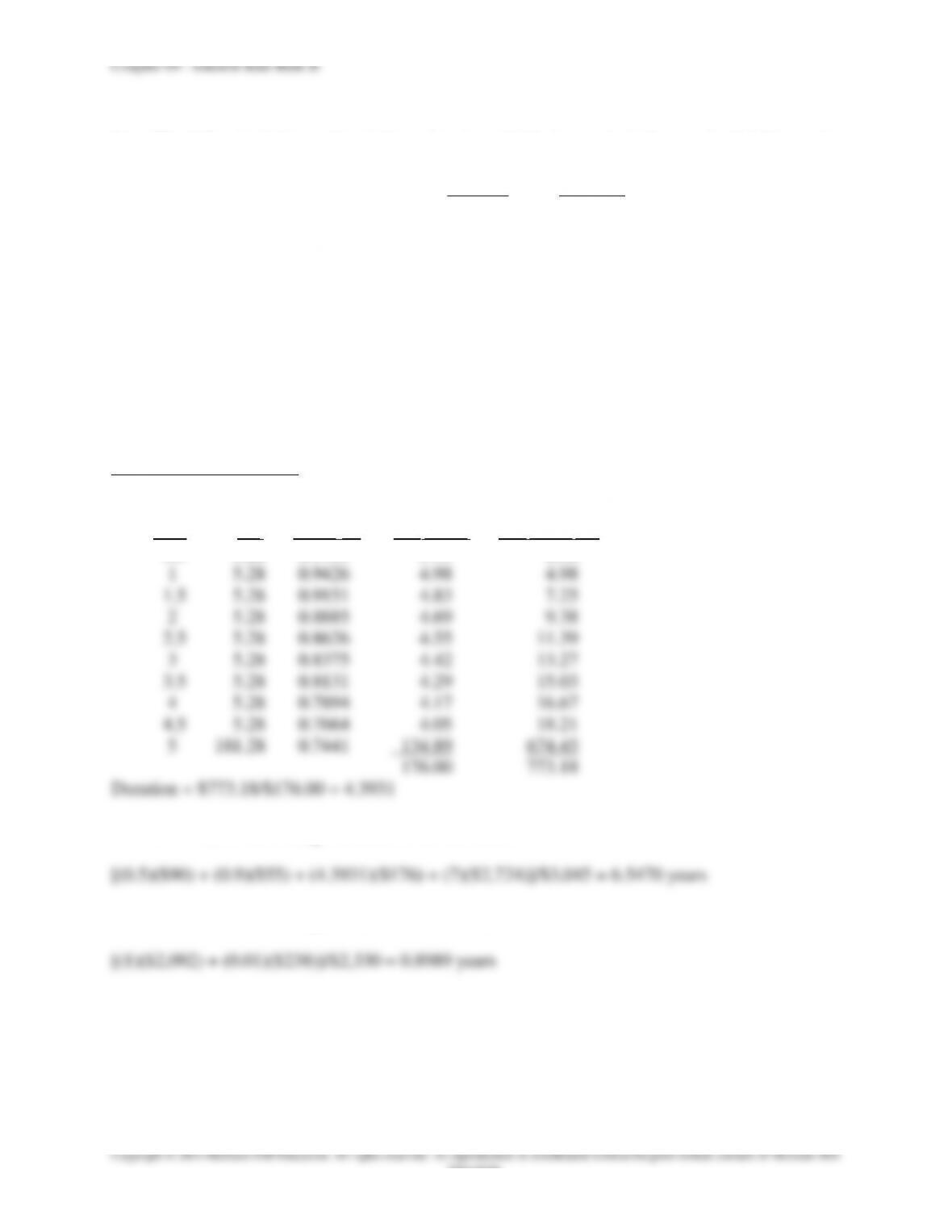

Treasury bonds are five-year maturities paying 6 percent semiannually and selling at par.

a. What is the duration of the T-bond portfolio?

Five-year Treasury Bond

Par value = $176 Coupon rate = 6% Semiannual payments

R = 6% Maturity = 5 years

t CFt DFt CFt x DFt CFt x DFt x t

0.5 5.28 0.9709 5.13 2.56

b. What is the average duration of all the assets?

c. What is the average duration of all the liabilities?

d. What is the leverage adjusted duration gap? What is the interest rate risk exposure?

Chapter 09 – Interest Rate Risk II

9-26

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

DGAP = DA – kDL = 6.5470 – ($2,330/$3,045)(0.8989) = 5.8592 years

The duration gap is positive, indicating that an increase in interest rates will lead to a decrease in

the market value of equity.

e. What is the forecasted impact on the market value of equity caused by a relative

upward shift in the entire yield curve of 0.5 percent [i.e., R/(1+R) = 0.0050]?

The market value of the equity will change by:

f. If the yield curve shifts downward by 0.25 percent [i.e., R/(1+R) = -0.0025], what is

the forecasted impact on the market value of equity?

g. What variables are available to the financial institution to immunize the balance sheet?

How much would each variable need to change to get DGAP equal to 0?

27. Assume that a goal of the regulatory agencies of financial institutions is to immunize the

ratio of equity to total assets, that is, (E/A) = 0. Explain how this goal changes the desired

duration gap for the institution. Why does this differ from the duration gap necessary to

immunize the total equity? How would your answers to part (h) in problem 23 and part (g)

in problem 25 change if immunizing equity to total assets was the goal?

Chapter 09 – Interest Rate Risk II

9-27

Education.

28. Identify and discuss three criticisms of using the duration gap model to immunize the

portfolio of a financial institution.

The three criticisms are:

a Immunization is a dynamic problem because duration changes over time. Thus, it is

29. In general, what changes have occurred in the financial markets that would allow financial

institutions to restructure their balance sheets more rapidly and efficiently to meet desired

goals? Why is it critical for an FI manager who has a portfolio immunized to match a

desired investment horizon to rebalance the portfolio periodically? What is convexity?

Why is convexity a desirable feature to capture in a portfolio of assets?

30. A financial institution has an investment horizon of two years 9.33 months (or 2.777 years).

The institution has converted all assets into a portfolio of 8 percent, $1,000, three-year

bonds that are trading at a yield to maturity of 10 percent. The bonds pay interest annually.

The portfolio manager believes that the assets are immunized against interest rate changes.

Chapter 09 – Interest Rate Risk II

9-28

a. Is the portfolio immunized at the time of bond purchase? What is the duration of the

bonds?

Three-year Bonds

Par value = $1,000 Coupon rate = 8% Annual payments

R = 10% Maturity = 3 years

t CFt DFt CFt x DFt CFt x DFt x t

b. Will the portfolio be immunized one year later?

Two-year Bonds

Par value = $1,000 Coupon rate = 8% Annual payments

R = 10% Maturity = 2 years

t CFt DFt CFt x DFt CFt x DFt x t

c. Assume that one-year, 8 percent zero-coupon bonds are available in one year. What

proportion of the original portfolio should be placed in these bonds to rebalance the

portfolio?

9-29

Education.

31. Consider a 12-year, 12 percent annual coupon bond with a required return of 10 percent.

The bond has a face value of $1,000.

a. What is the price of the bond?

b. If interest rates rise to 11 percent, what is the price of the bond?

c. What has been the percentage change in price?

d. Repeat parts (a), (b), and (c) for a 16-year bond.

e. What do the respective changes in bond prices indicate?

32. Consider a five-year, 15 percent annual coupon bond with a face value of $1,000. The bond

is trading at a yield to maturity of 12 percent.

a. What is the price of the bond?

b. If the yield to maturity increases 1 percent, what will be the bond’s new price?

c. Using your answers to parts (a) and (b), what is the percentage change in the bond’s

price as a result of the 1 percent increase in interest rates?

Chapter 09 – Interest Rate Risk II

9-30

Education.

d. Repeat parts (b) and (c) assuming a 1 percent decrease in interest rates.

e. What do the differences in your answers indicate about the rate-price relationships of

fixed-rate assets?

33. Consider a $1,000 bond with a fixed-rate 10 percent annual coupon rate and a maturity (N)

of 10 years. The bond currently is trading at a yield to maturity (YTM) of 10 percent.

a. Complete the following table:

Change

Coupon $ Change in Price % Change in Price

N Rate YTM Price from Par from Par

8 10% 9% $1,055.35 $55.35 5.535%

b. Use this information to verify the principles of interest rate-price relationships for

fixed-rate financial assets.

Chapter 09 – Interest Rate Risk II

9-31

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Rule 3. The change in value of longer-term fixed-rate financial assets increases at a

decreasing rate.

For the increase in rates from 10 percent to 11 percent, the difference in the change in price

between the 10-year and 11-year assets is $3.18 ($62.07 – $58.89), while the difference in the

change in price between the 11-year and 12-year assets is $2.86 ($64.93 – $62.07).

Rule 4. Although not mentioned in Appendix 9A, for a given percentage () change in

interest rates, the increase in price for a decrease in rates is greater than the decrease in

value for an increase in rates.

For rates decreasing from 10 percent to 9 percent, the 10-year bond increases $64.18. But for

rates increasing from 10 percent to 11 percent, the 10-year bond decreases $58.89.

The following questions and problems are based on material in Appendix 9B to the chapter.

34. MLK Bank has an asset portfolio that consists of $100 million of 30-year, 8 percent

coupon, $1,000 bonds that sell at par.

a. What will be the bonds’ new prices if market yields change immediately by 0.10

percent? What will be the new prices if market yields change immediately by 2.00

percent?

b. The duration of these bonds is 12.1608 years. What are the predicted bond prices in

each of the four cases using the duration rule? What is the amount of error between the

duration prediction and the actual market values?