Chapter 09 – Interest Rate Risk II

9-1

Education.

Solutions for End-of-Chapter Questions and Problems: Chapter Nine

1. What is the difference between book value accounting and market value accounting? How do

interest rate changes affect the value of bank assets and liabilities under the two methods?

What is marking to market?

Book value accounting reports assets and liabilities at the original issue values. Market value

2. What are the two different general interpretations of the concept of duration, and what is

the technical definition of this term? How does duration differ from maturity?

3. A one-year, $100,000 loan carries a coupon rate and a market interest rate of 12 percent.

The loan requires payment of accrued interest and one-half of the principal at the end of six

months. The remaining principal and accrued interest are due at the end of the year.

a. What will be the cash flows at the end of six months and at the end of the year?

b. What is the present value of each cash flow discounted at the market rate? What is the

total present value?

Chapter 09 – Interest Rate Risk II

9-2

Education.

c. What proportion of the total present value of cash flows occurs at the end of six

months? What proportion occurs at the end of the year?

d. What is the duration of this loan?

OR

t CF PVof CF PV of CF x t

½ $56,000 $52,830.19 $26,415.09

4. Two bonds are available for purchase in the financial markets. The first bond is a two-year,

$1,000 bond that pays an annual coupon of 10 percent. The second bond is a two-year,

$1,000, zero-coupon bond.

a. What is the duration of the coupon bond if the current yield-to-maturity (R) is 8

percent?10 percent? 12 percent? (Hint: You may wish to create a spreadsheet program

to assist in the calculations.)

Chapter 09 – Interest Rate Risk II

9-3

Education.

b. How does the change in the yield to maturity affect the duration of this coupon bond?

c. Calculate the duration of the zero-coupon bond with a yield to maturity of 8 percent, 10

percent, and 12 percent.

d. How does the change in the yield to maturity affect the duration of the zero-coupon bond?

Chapter 09 – Interest Rate Risk II

9-4

Education.

e. Why does the change in the yield to maturity affect the coupon bond differently than it

affects the zero-coupon bond?

5. What is the duration of a five-year, $1,000 Treasury bond with a 10 percent semiannual

coupon selling at par? Selling with a yield to maturity of 12 percent? 14 percent? What can

you conclude about the relationship between duration and yield to maturity? Plot the

relationship. Why does this relationship exist?

Five-year Treasury Bond: Par value = $1,000 Coupon rate = 10% Semiannual payments

R = 10% Maturity = 5 years

t CFt DFt CFt x DFt CFt x DFt x t

0.5 50 0.9524 47.620 23.810

1.0 50 0.9070 45.350 45.350

R = 12% Maturity = 5 years

t CFt CFt x DFt CFt x DFt x t

0.5 50 47.17 23.58

1.0 50 44.50 44.50

Chapter 09 – Interest Rate Risk II

9-5

Education.

R = 14% Maturity = 5 years

t CFt CFt x DFt CFt x DFt x t

0.5 50 46.73 23.36

1.0 50 43.67 43.67

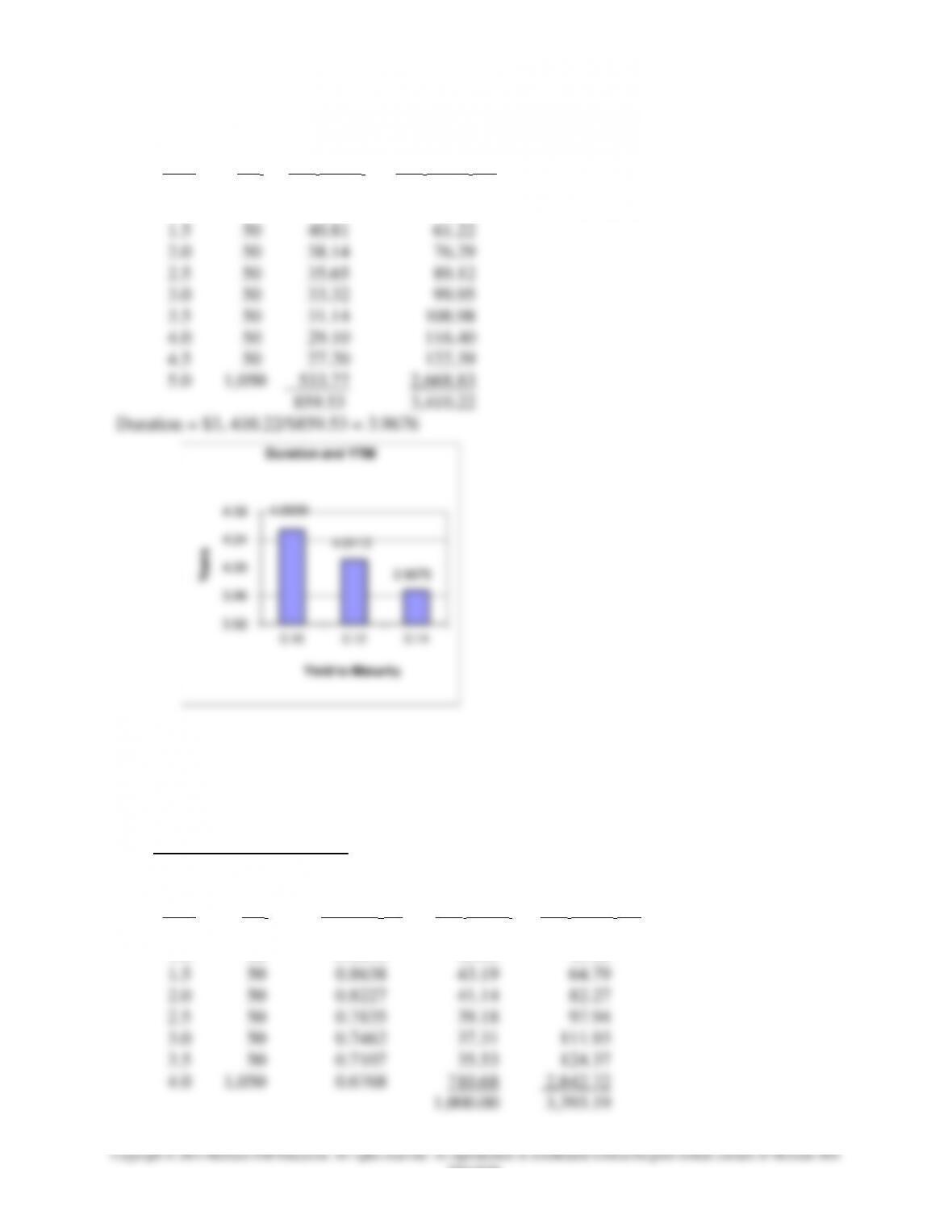

6. Consider three Treasury bonds each of which has a 10 percent semiannual coupon and

trades at par.

a. Calculate the duration for a bond that has a maturity of four years, three years, and two years?

Four-year Treasury Bond: Par value = $1,000 Coupon rate = 10% Semiannual payments

R = 10% Maturity = 4 years

t CFt DFt CFt x DFt CFt x DFt x t

0.5 50 0.9524 47.62 23.81

1.0 50 0.9070 45.35 45.35

2.0 50 0.8227 41.14 82.27

2.5 50 0.7835 39.18 97.94

3.0 50 0.7462 37.31 111.93

3.5 50 0.7107 35.53 124.37

4.0 1,050 0.6768 710.68 2,842.72

1,000.00 3,393.19

4.0539

4.0113

3.9676

3.92

3.96

4.00

4.04

4.08

0.10 0.12 0.14

Years

Yield to Maturity

Duration and YTM

Chapter 09 – Interest Rate Risk II

9-6

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

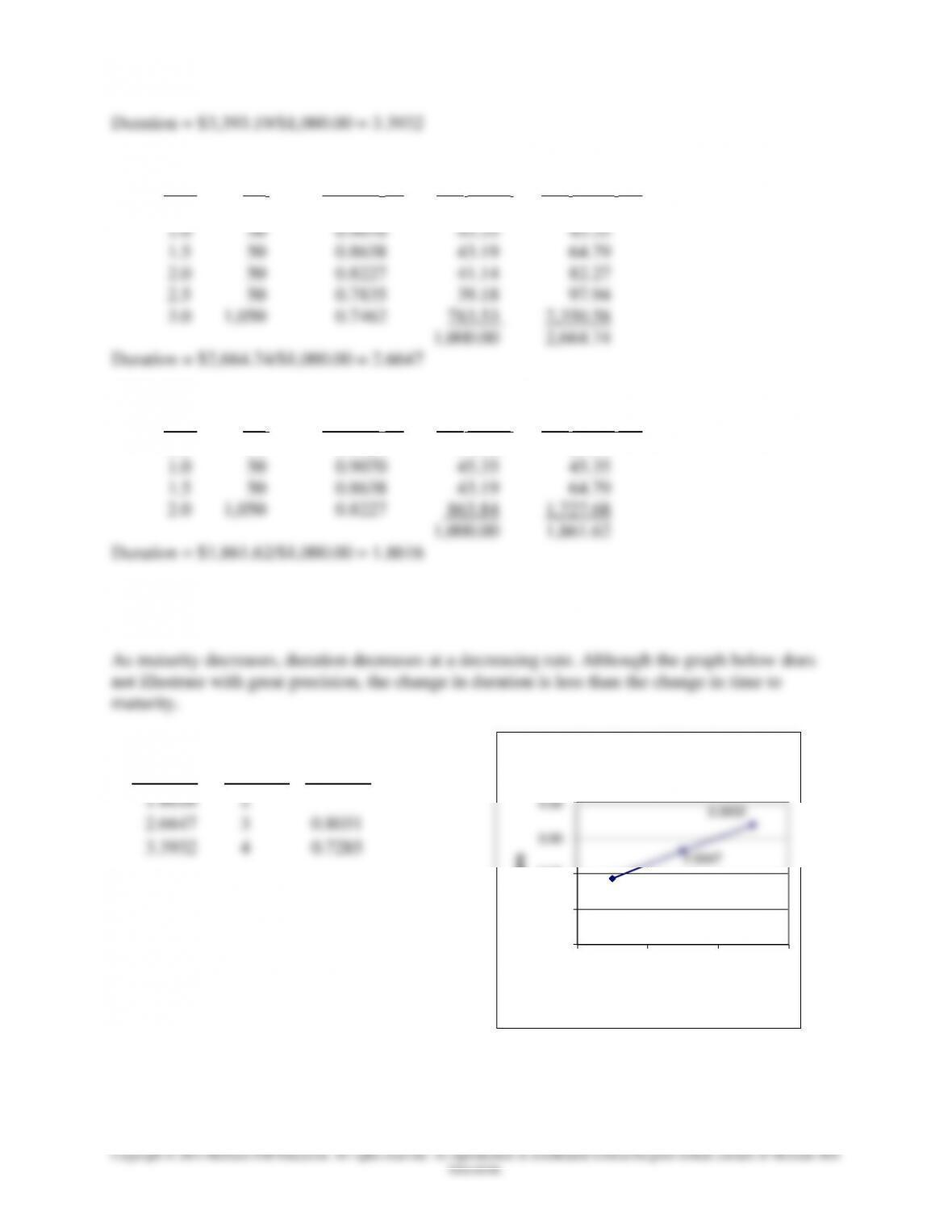

Duration = $3,393.19/$1,000.00 = 3.3932

R = 10% Maturity = 3 years

t CFt DFt CFt x DFt CFt x DFt x t

0.5 50 0.9524 47.62 23.81

R = 10% Maturity = 2 years

t CFt DFt CFt x DFt CFt x DFt x t

0.5 50 0.9524 47.62 23.81

b. What conclusions can you reach about the relationship of duration and the time to

maturity? Plot the relationship.

1.8616

2.6647

3.3932

0.00

1.00

2.00

3.00

4.00

2 3 4

Years

Time to Maturity

Duration and Maturity

Change in

Duration

Maturity

Duration

1.8616

2

2.6647

3

0.8031

3.3932

4

0.7285

Chapter 09 – Interest Rate Risk II

9-7

Education.

7. A six-year, $10,000 CD pays 6 percent interest annually and has a 6 percent yield to

maturity. What is the duration of the CD? What would be the duration if interest were paid

semiannually? What is the relationship of duration to the relative frequency of interest

payments?

Six-year CD: Par value = $10,000 Coupon rate = 6%

R = 6% Maturity = 6 years Annual payments

t CFt DFt CFt x DFt CFt x DFt x t

1 600 0.9434 566.04 566.04

R = 6% Maturity = 6 years Semiannual payments

t CFt DFt CFt x DFt CFt x DFt x t

0.5 300 0.9709 291.26 145.63

1 300 0.9425 282.78 282.78

1.5 300 0.9151 274.54 411.81

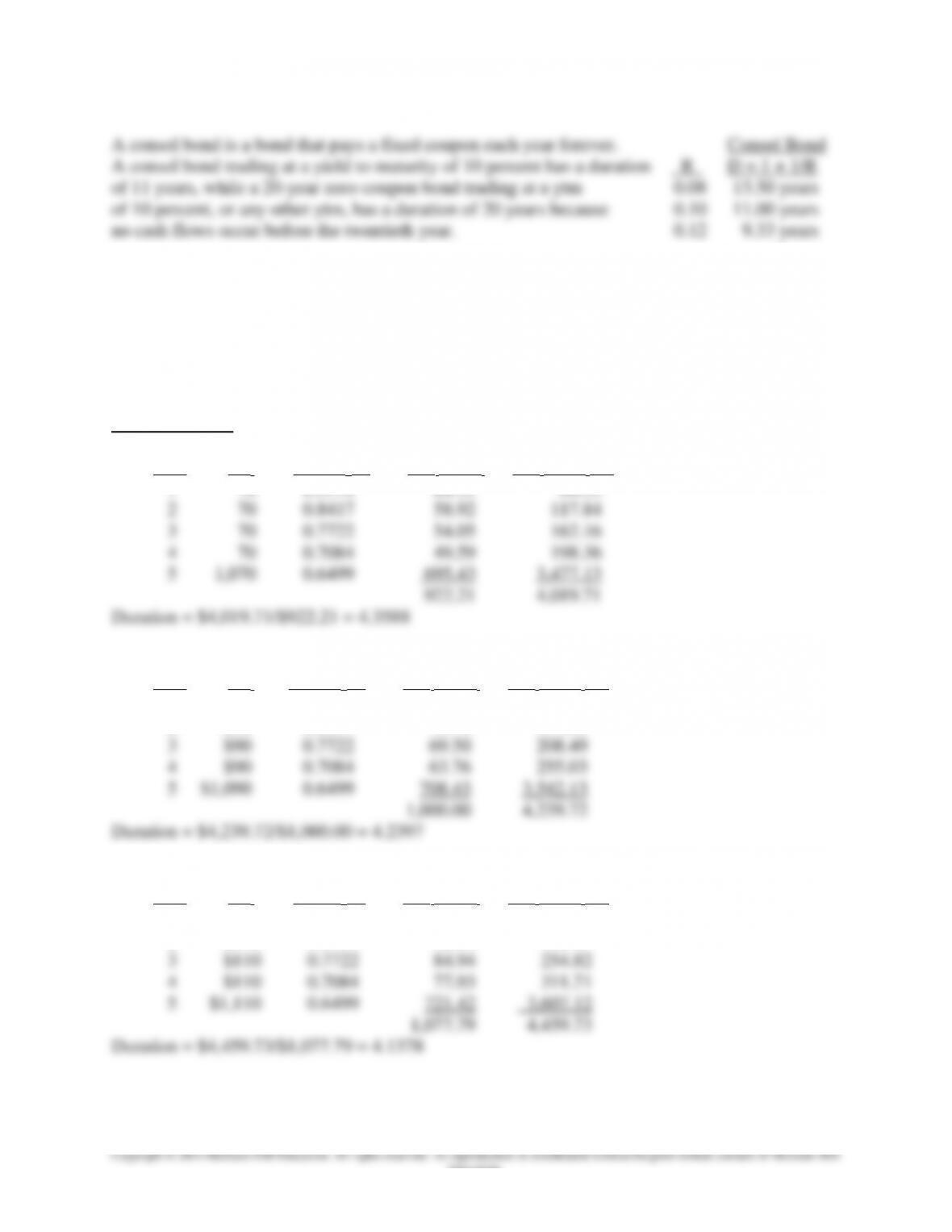

8. What is a consol bond? What is the duration of a consol bond that sells at a yield to

maturity of 8 percent? 10 percent? 12 percent? Would a consol trading at a yield to

maturity of 10 percent have a greater duration than a 20-year zero-coupon bond trading at

the same yield to maturity? Why?

Chapter 09 – Interest Rate Risk II

9-8

Education.

9. Maximum Pension Fund is attempting to manage one of the bond portfolios under its

management. The fund has identified three bonds which have five year maturities and trade

at a yield to maturity of 9 percent. The bonds differ only in that the coupons are 7 percent,

9 percent, and 11 percent.

a. What is the duration for each bond?

Five-year Bond: Par value = $1,000 Maturity = 5 years Annual payments

R = 9% Coupon rate = 7%

t CFt DFt CFt x DFt CFt x DFt x t

1 70 0.9174 64.22 64.22

R = 9% Coupon rate = 9%

t CFt DFt CFt x DFt CFt x DFt x t

1 $90 0.9174 82.57 82.57

2 $90 0.8417 75.75 151.50

R = 9% Coupon rate = 11%

t CFt DFt CFt x DFt CFt x DFt x t

1 $110 0.9174 100.92 100.92

2 $110 0.8417 92.58 185.17

Chapter 09 – Interest Rate Risk II

Education.

b. What is the relationship between duration and the amount of coupon interest that is

paid? Plot the relationship.

10. An insurance company is analyzing three bonds and is using duration as the measure of

interest rate risk. All three bonds trade at a yield to maturity of 10 percent, have $10,000

par values, and have five years to maturity. The bonds differ only in the amount of annual

coupon interest that they pay: 8, 10, and 12 percent.

a. What is the duration for each five-year bond?

Five-year Bond: Par value = $10,000 R = 10% Maturity = 5 years Annual payments

Coupon rate = 8%

t CFt DFt CFt x DFt CFt x DFt x t

Coupon rate = 10%

t CFt DFt CFt x DFt CFt x DFt x t

1 $1,000 0.9091 909.09 909.09

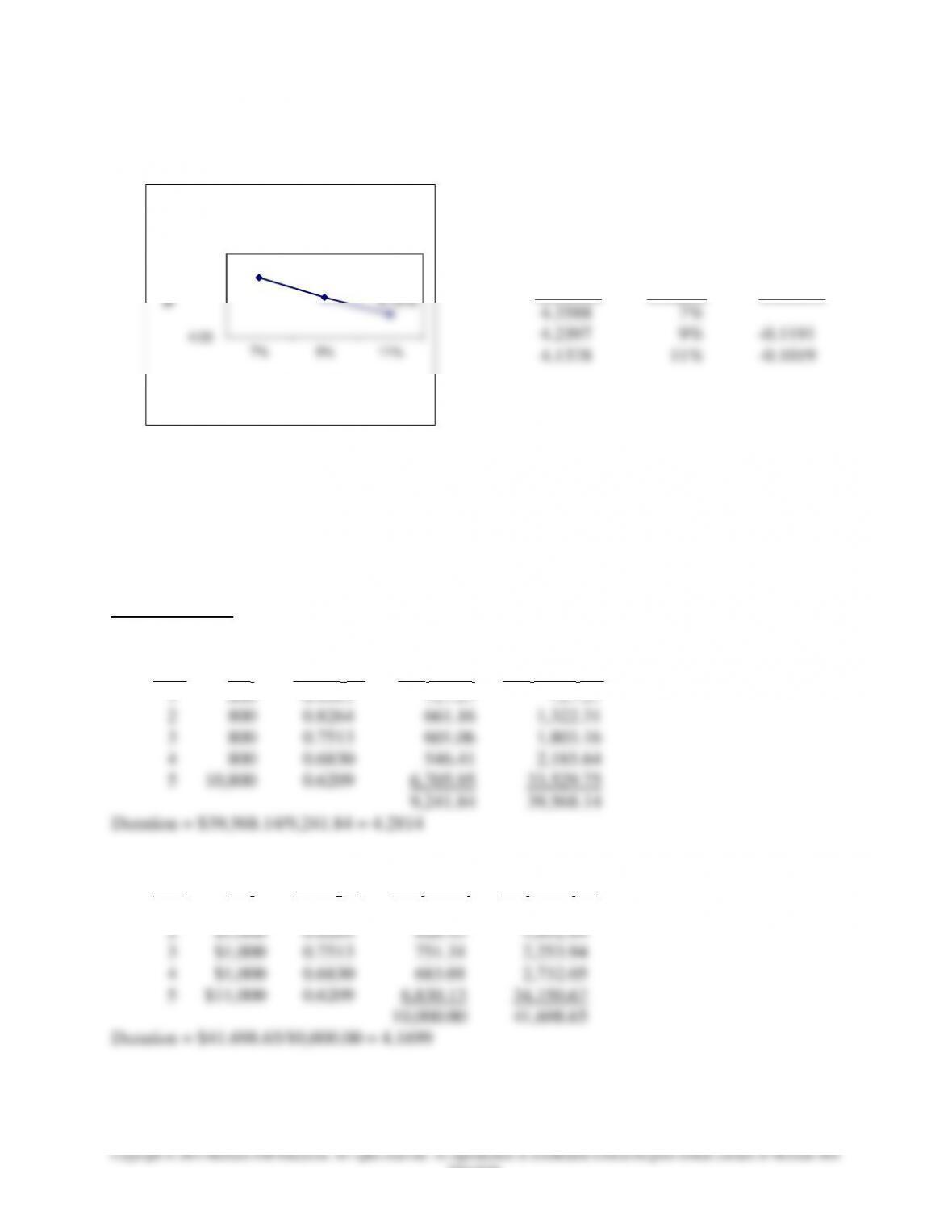

4.3588

4.2397

4.1378

4.00

7% 9% 11%

Years

Coupon Rates

Duration and Coupon Rates

Duration decreases as the amount of coupon

interest increases.

Change in

Duration Coupon Duration

4.3588 7%

4.2397 9% –0.1191

4.1378 11% –0.1019

Chapter 09 – Interest Rate Risk II

Coupon rate = 12%

t CFt DFt CFt x DFt CFt x DFt x t

1 $1,200 0.9091 1,090.91 1,090.91

2 $1,200 0.8264 991.74 1,983.47

b. What is the relationship between duration and the amount of coupon interest that is

paid?

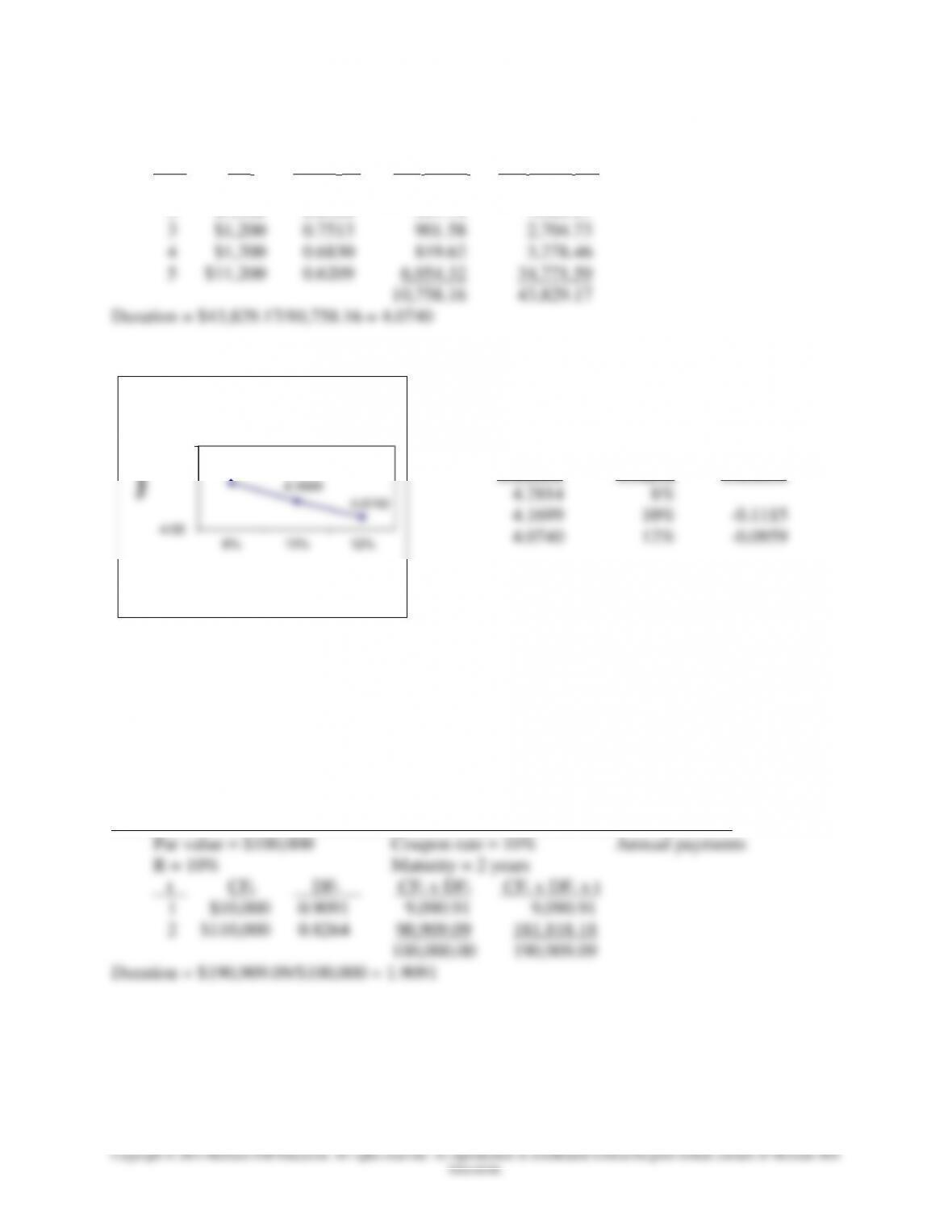

11. You can obtain a loan of $100,000 at a rate of 10 percent for two years. You have a choice

of (i) paying the interest (10 percent) each year and the total principal at the end of the

second year or (ii) amortizing the loan, that is, paying interest (10 percent) and principal in

equal payments each year. The loan is priced at par.

a. What is the duration of the loan under both methods of payment?

Two-year loan: Interest at end of year one; Principal and interest at end of year two

4.2814

4.1699

4.0740

4.00

4.50

8% 10% 12%

Years

Coupon Rates

Duration and Coupon Rates

Duration decreases as the amount of coupon

interest increases.

Change in

Duration Coupon Duration

4.2814 8%

4.1699 10% –0.1115

4.0740 12% –0.0959

Chapter 09 – Interest Rate Risk II

9-11

Two-year loan: Amortized over two years

Par value = $100,000 Coupon rate = 10% Annual amortized payments

R = 10% Maturity = 2 years = $57,619.05

t CFt DFt CFt x DFt CFt x DFt x t

b. Explain the difference in the two results

12. How is duration related to the interest elasticity of a fixed-income security? What is the

relationship between duration and the price of the fixed-income security?

13. You have discovered that the price of a bond rose from $975 to $995 when the yield to

maturity fell from 9.75 percent to 9.25 percent. What is the duration of the bond?

0975.1

005.0

)R1(

R

−

+

14. A 10-year, 10 percent annual coupon, $1,000 bond trades at a yield to maturity of 8

percent. The bond has a duration of 6.994 years. What is the modified duration of this

bond? What is the practical value of calculating modified duration? Does modified duration

change the result of using the duration relationship to estimate price sensitivity?

Chapter 09 – Interest Rate Risk II

9-12

Education.

15. What is dollar duration? How is dollar duration different from duration?

16. Calculate the duration of a two-year, $1,000 bond that pays an annual coupon of 10 percent

and trades at a yield of 14 percent. What is the expected change in the price of the bond if

interest rates fall by 0.50 percent (50 basis points)?

Two-year Bond: Par value = $1,000 Coupon rate = 10% Annual payments

R = 14% Maturity = 2 years

t CFt DFt CFt x DFt CFt x DFt x t

17. The duration of an 11-year, $1,000 Treasury bond paying a 10 percent semiannual coupon

and selling at par has been estimated at 6.763 years.

a. What is the modified duration of the bond? What is the dollar duration of the bond?

b. What will be the estimated price change on the bond if interest rates increase 0.10

percent (10 basis points)? If rates decrease 0.20 percent (20 basis points)?

Chapter 09 – Interest Rate Risk II

9-13

Education.

c. What would the actual price of the bond be under each rate change situation in part (b)

using the traditional present value bond pricing techniques? What is the amount of error

in each case?

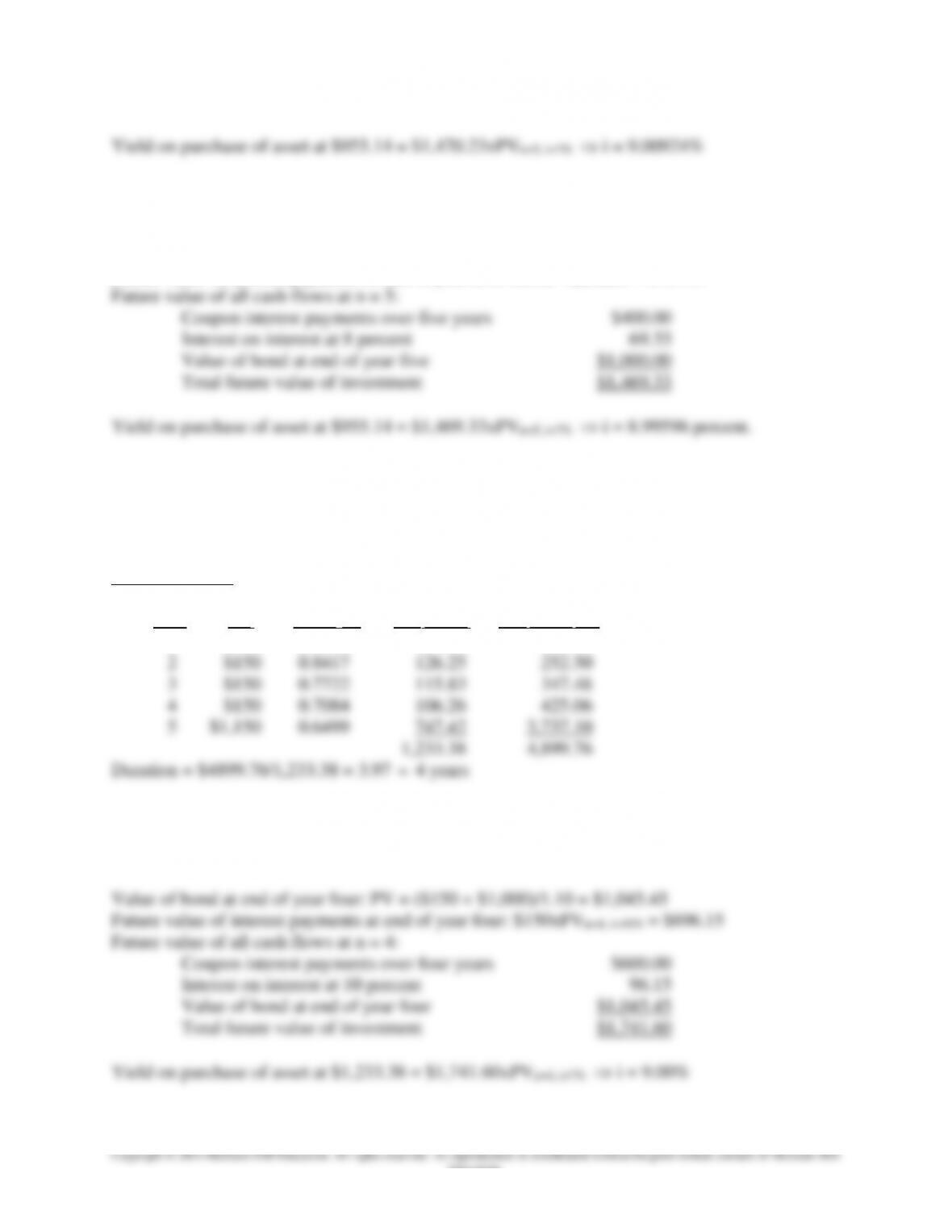

18. Suppose you purchase a six-year, 8 percent coupon bond (paid annually) that is priced to

yield 9 percent. The face value of the bond is $1,000.

a. Show that the duration of this bond is equal to five years.

Six-year Bond: Par value = $1,000 Coupon rate = 8% Annual payments

R = 9% Maturity = 6 years

t CFt DFt CFt x DFt CFt x DFt x t

1 80 0.9174 73.39 73.39

b. Show that if interest rates rise to 10 percent within the next year and your investment

horizon is five years from today, you will still earn a 9 percent yield on your

investment.

Chapter 09 – Interest Rate Risk II

9-14

Education.

c. Show that a 9 percent yield also will be earned if interest rates fall next year to 8

percent.

Value of bond at end of year five: PV = ($80 + $1,000)/1.08 = $1,000

Future value of interest payments at end of year five: $80xFVn=5, i=8% = $469.33

19. Suppose you purchase a five-year, 15 percent coupon bond (paid annually) that is priced to

yield 9 percent. The face value of the bond is $1,000.

a. Show that the duration of this bond is equal to four years.

Five-year Bond: Par value = $1,000 Coupon rate = 15% Annual payments

R = 9% Maturity = 5 years

t CFt DFt CFt x DFt CFt x DFt x t

1 $150 0.9174 137.62 137.62

b. Show that if interest rates rise to 10 percent within the next year and your investment

horizon is four years from today, you will still earn a 9 percent yield on your

investment.

Chapter 09 – Interest Rate Risk II

9-15

Education.

c. Show that a 9 percent yield also will be earned if interest rates fall next year to 8

percent.

20. Consider the case in which an investor holds a bond for a period of time longer than the

duration of the bond, that is, longer than the original investment horizon.

a. If interest rates rise, will the return that is earned exceed or fall short of the original

required rate of return? Explain.

b. What will happen to the realized return if interest rates decrease? Explain.

c. Recalculate parts (b) and (c) of problem 18 above, assuming that the bond is held for all

five years, to verify your answers to parts (a) and (b) of this problem.

Chapter 09 – Interest Rate Risk II

9-16

Education.

d. If either calculation in part (c) is greater than the original required rate of return, why

would an investor ever try to match the duration of an asset with his or her investment

horizon?

21. Two banks are being examined by regulators to determine the interest rate sensitivity of

their balance sheets. Bank A has assets composed solely of a 10-year $1 million loan with a

coupon rate and yield of 12 percent. The loan is financed with a 10-year $1 million CD

with a coupon rate and yield of 10 percent. Bank B has assets composed solely of a 7-year,

12 percent zero-coupon bond with a current (market) value of $894,006.20 and a maturity

(principal) value of $1,976,362.88. The bond is financed with a 10-year, 8.275 percent

coupon $1,000,000 face value CD with a yield to maturity of 10 percent. The loan and the

CDs pay interest annually, with principal due at maturity.

a. If market interest rates increase 1 percent (100 basis points), how do the market values

of the assets and liabilities of each bank change? That is, what will be the net affect on

the market value of the equity for each bank?

Chapter 09 – Interest Rate Risk II

9-17

Education.

b. What accounts for the differences in the changes in the market value of equity between

the two banks?

c. Verify your results above by calculating the duration for the assets and liabilities of

each bank, and estimate the changes in value for the expected change in interest rates.

Summarize your results.

Ten-year CD Bank B (values in thousands of $s)

Par value = $1,000 Coupon rate = 8.275% Annual payments

R = 10% Maturity = 10 years

t CFt DFt CFt x DFt CFt x DFt x t

1 82.75 0.9091 75.23 75.23

Chapter 09 – Interest Rate Risk II

9-18

Education.

The duration estimates for the loan and CD for Bank A are presented below:

Ten-year Loan Bank A (values in thousands of $s)

Par value = $1,000 Coupon rate = 12% Annual payments

R = 12% Maturity = 10 years

t CFt DFt CFt x DFt CFt x DFt x t

1 120 0.8929 107.14 107.14

2 120 0.7972 95.66 191.33

Ten-year CD Bank A (values in thousands of $s)

Par value = $1,000 Coupon rate = 10% Annual payments

R = 10% Maturity = 10 years

t CFt DFt CFt x DFt CFt x DFt x t

1 100 0.9091 90.91 90.91

2 100 0.8264 82.64 165.29

3 100 0.7513 75.13 225.39

Chapter 09 – Interest Rate Risk II

9-19

22. If an FI uses only duration to immunize its portfolio, what three factors affect changes in

the net worth of the FI when interest rates change?

The change in net worth for a given change in interest rates is given by the following equation:

A

L

kwhere

R

R

AkDDE LA =

+

−−= 1

**

Thus, three factors are important in determining E.

23. Financial Institution XY has assets of $1 million invested in a 30-year, 10 percent

semiannual coupon Treasury bond selling at par. The duration of this bond has been

estimated at 9.94 years. The assets are financed with equity and a $900,000, two-year, 7.25

percent semiannual coupon capital note selling at par.

a. What is the leverage adjusted duration gap of Financial Institution XY?

Chapter 09 – Interest Rate Risk II

9-20

Two-year Capital Note (values in thousands of $s)

Par value = $900 Coupon rate = 7.25% Semiannual payments

R = 7.25% Maturity = 2 years

t CFt DFt CFt x DFt CFt x DFt x t

0.5 32.625 0.9650 31.48 15.74

000,000,1$

b. What is the impact on equity value if the relative change in all market interest rates is a

decrease of 20 basis points? Note: The relative change in interest rates is R/(1+R/2) =

-0.0020.

10

2

R

1

+

c. Using the information calculated in parts (a) and (b), what can be said about the desired

duration gap for the financial institution if interest rates are expected to increase or

decrease.

d. Verify your answer to part (c) by calculating the change in the market value of equity

assuming that the relative change in all market interest rates is an increase of 30 basis

2

R

1

+

e. What would the duration of the assets need to be to immunize the equity from changes

in market interest rates?