Chapter 08 – Interest Rate Risk I

8-15

Education.

c. What will happen to the market value of the equity?

25. If a bank manager is certain that interest rates were going to increase within the next six

months, how should the bank manager adjust the bank’s maturity gap to take advantage of

this anticipated increase? What if the manager believes rates will fall? Would your

suggested adjustments be difficult or easy to achieve?

26. An insurance company has invested in the following fixed-income securities: (a)

$10,000,000 of five-year Treasury notes paying 5 percent interest and selling at par value,

(b) $5,800,000 of 10-year bonds paying 7 percent interest with a par value of $6,000,000,

and (c) $6,200,000 of 20-year subordinated debentures paying 9 percent interest with a par

value of $6,000,000.

a. What is the weighted-average maturity of this portfolio of assets?

b. If interest rates change so that the yields on all of the securities decrease 1 percent, how

does the weighted-average maturity of the portfolio change?

Chapter 08 – Interest Rate Risk I

8-16

Education.

c. Explain the changes in the maturity values if the yields increase by 1 percent.

d. Assume that the insurance company has no other assets. What will be the effect on the

market value of the company’s equity if the interest rate changes in (b) and (c) occur?

27. The following is a simplified FI balance sheet:

Assets Liabilities and Equity

Loans $1,000 Deposits $850

0 Equity $150

Total assets $1,000 Total liabilities & equity $1,000

The average maturity of loans is four years and the average maturity of deposits is two

years. Assume loan and deposit balances are reported as book value, zero-coupon items.

a. Assume that interest rate on both loans and deposits is 9 percent. What is the market

value of equity?

Chapter 08 – Interest Rate Risk I

8-17

Education.

b. What must be the interest rate on deposits to force the market value of equity to be

zero? What economic market conditions must exist to make this situation possible?

c. Assume that interest rate on both loans and deposits is 9 percent. What must be the

average maturity of deposits for the market value of equity to be zero?

28. Gunnison Insurance has reported the following balance sheet (in thousands):

Assets Liabilities and Equity

2-year Treasury note $175 1-year commercial paper $135

15-year munis 165 5-year note 160

Equity 45

Total assets $340 Total liabilities and equity $340

All securities are selling at par equal to book value. The two-year notes are yielding 5

percent, and the 15-year munis are yielding 9 percent. The one-year commercial paper pays

4.5 percent, and the five-year notes pay 8 percent. All instruments pay interest annually.

a. What is the weighted-average maturity of the assets for Gunnison?

b. What is the weighted-average maturity of the liabilities for Gunnison?

c. What is the maturity gap for Gunnison?

Chapter 08 – Interest Rate Risk I

8-18

Education.

d. What does your answer to part (c) imply about the interest rate exposure of Gunnison

Insurance?

e. Calculate the values of all four securities on Gunnison Insurance’s balance sheet

assuming that all interest rates increase 2 percent. What is the dollar change in the total

asset and total liability values? What is the percentage change in these values?

f. What is the dollar impact on the market value of equity for Gunnison? What is the

percentage change in the value of the equity?

g. What would be the impact on Gunnison’s market value of equity if the liabilities paid

interest semiannually instead of annually?

29. Scandia Bank has issued a one-year, $1million CD paying 5.75 percent to fund a one-year

loan paying an interest rate of 6 percent. The principal of the loan will be paid in two

installments, $500,000 in six months and the balance at the end of the year.

a. What is the maturity gap of Scandia Bank? According to the maturity model, what does

this maturity gap imply about the interest rate risk exposure faced by Scandia Bank?

b. Assuming no change in interest rates over the year, what is the expected net interest

income at the end of the year?

Chapter 08 – Interest Rate Risk I

8-19

Education.

c. What would be the effect on annual net interest income of a 2 percent interest rate

increase that occurred immediately after the loan was made? What would be the effect of a

2 percent decrease in rates?

If interest rates increase 2 percent, then the reinvestment benefits of cash flows in six months

will be higher:

Principal received in six months $500,000

Interest received in six months (0.03 x $1,000,000) 30,000

Total $530,000

Chapter 08 – Interest Rate Risk I

8-20

d. What do these results indicate about the ability of the maturity model to immunize

portfolios against interest rate exposure?

30. EDF Bank has a very simple balance sheet. Assets consist of a two-year, $1 million loan

that pays an interest rate of LIBOR plus 4 percent annually. The loan is funded with a two-

year deposit on which the bank pays LIBOR plus 3.5 percent interest annually. LIBOR

currently is 4 percent, and both the loan and the deposit principal will be paid at maturity.

a. What is the maturity gap of this balance sheet?

b. What is the expected net interest income in year 1 and year 2?

c. Immediately prior to the beginning of year 2, LIBOR rates increased to 6 percent. What

is the expected net interest income in year 2? What would be the effect on net interest

income of a 2 percent decrease in LIBOR?

d. What do the answers to parts (b) and (c) of this question suggest about the use of

maturity gap to immunize an FI against interest rate risk?

Chapter 08 – Interest Rate Risk I

8-21

31. What are the weaknesses of the maturity gap model?

First, the maturity gap model does not consider the degree of leverage on the balance sheet. For

32. Suppose that the current one-year rate (one-year spot rate) and expected one-year T-bill

rates over the following three years (i.e., years 2, 3, and 4, respectively) are as follows:

1R1=6% E(2r1) =7% E(3r1) =7.5% E(4r1)=7.85%

Using the unbiased expectations theory, calculate the current (long-term) rates for one-,

two-, three-, and four-year-maturity Treasury securities. Plot the resulting yield curve.

Chapter 08 – Interest Rate Risk I

8-22

33. The current one-year Treasury bill rate is 5.2 percent, and the expected one-year rate 12

months from now is 5.8 percent. According to the unbiased expectations theory, what

should be the current rate for a two-year Treasury security?

34. The Wall Street Journal reported interest rates of 6 percent, 6.35 percent, 6.65 percent, and

6.75 percent for three-year, four-year, five-year, and six-year Treasury notes, respectively.

According to the unbiased expectations theory, what are the expected one-year rates for

35. The Wall Street Journal reports that the rate on three-year Treasury securities is 5.60

percent and the rate on four-year Treasury securities is 5.65 percent. According to the

unbiased expectations hypothesis, what does the market expect the one-year Treasury rate

to be in year 4, E(4r1)?

36. How does the liquidity premium theory of the term structure of interest rates differ from the

unbiased expectations theory? In a normal economic environment, that is, an upward–

sloping yield curve, what is the relationship of liquidity premiums for successive years into

the future? Why?

8-23

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

37. Based on economists= forecasts and analysis, one-year Treasury bill rates and liquidity

premiums for the next four years are expected to be as follows:

1R1 = 5.65%

E(2r1) = 6.75% L2 = 0.05%

E(3r1) = 6.85% L3 = 0.10%

E(4r1) = 7.15% L4 = 0.12%

Using the liquidity premium hypothesis, plot the current yield curve. Make sure you label

the axes on the graph and identify the four annual rates on the curve both on the axes and

on the yield curve itself.

Chapter 08 – Interest Rate Risk I

8-24

38. The Wall Street Journal reports that the rate on three-year Treasury securities is 5.25

percent and the rate on four-year Treasury securities is 5.50 percent. The one-year interest

rate expected in year four, E(4r1), is 6.10 percent. According to the liquidity premium

hypothesis, what is the liquidity premium on the four-year Treasury security, L4?

39. You note the following yield curve in The Wall Street Journal. According to the unbiased

expectations hypothesis, what is the one-year forward rate for the period beginning two

years from today, 2f1?

Maturity Yield

One day 2.00%

Integrated Mini Case: Calculating and Using the Repricing GAP

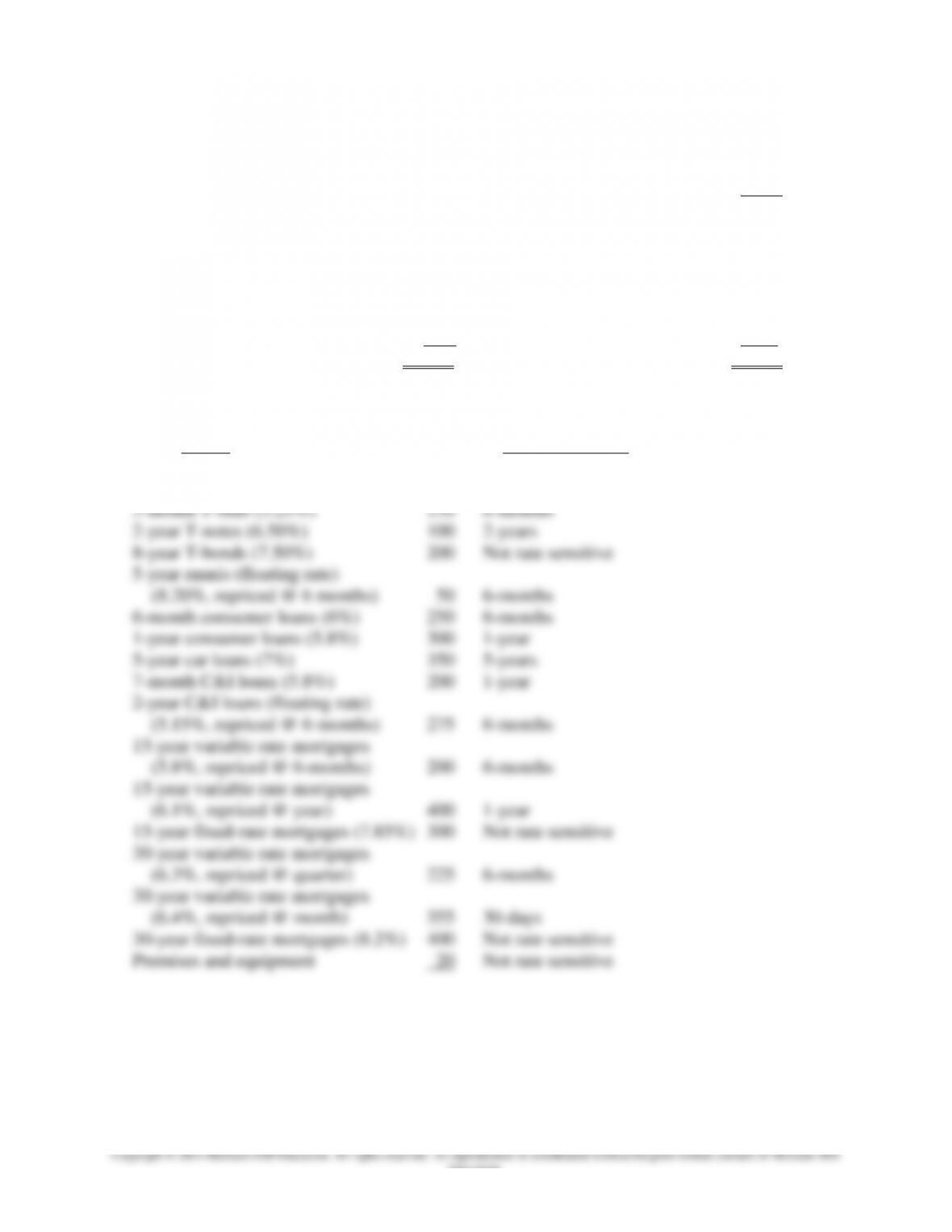

State Bank’s balance sheet is listed below. Market yields are in parenthesis, and amounts are in

millions.

Assets Liabilities and Equity

Cash $20 Demand deposits $250

Fed funds (5.05%) 150 Savings accounts (1.5%) 20

3-month T-bills (5.25%) 150 MMDAs (4.5%)

2-year T-notes (6.50%) 100 (no minimum balance requirement) 340

8-year T-bonds (7.50%) 200 3-month CDs (4.2%) 120

5-year munis (floating rate) 6-month CDs (4.3%) 220

(8.20%, repriced @ 6 months) 50 1-year CDs (4.5%) 375

6-month consumer loans (6%) 250 2-year CDs (5%) 425

1-year consumer loans (5.8%) 300 4-year CDs (5.5%) 330

5-year car loans (7%) 350 5-year CDs (6%) 350

7-month C&I loans (5.8%) 200 Fed funds (5%) 225

2-year C&I loans (floating rate) Overnight repos (5%) 290

(5.15%, repriced @ 6-months) 275 6-month commercial paper (5.05%) 300

15-year variable rate mortgages Subordinate notes:

Chapter 08 – Interest Rate Risk I

8-25

Education.

(5.8%, repriced @ 6-months) 200 3-year fixed rate (6.55%) 200

15-year variable rate mortgages Subordinated debt:

(6.1%, repriced @ year) 400 7-year fixed rate (7.25%) 100

15-year fixed-rate mortgages (7.85%) 300 Total liabilities $3,545

30-year variable rate mortgages

(6.3%, repriced @ quarter) 225

30-year variable rate mortgages

(6.4%, repriced @ month) 355

30-year fixed-rate mortgages (8.2%) 400

Premises and equipment 20 Equity 400

Total assets $3,945 Total liabilities and equity $3,945

a. What is the repricing gap if the planning period is 30 days? 6 months? 1 year? 2 years? 5

years?

Assets Repricing period

Cash $20 Not rate sensitive

Fed funds (5.05%) 150 30-days

Chapter 08 – Interest Rate Risk I

8-26

Liabilities and Equity Repricing Period

Demand deposits $250 Not rate sensitive

Savings accounts (1.5%) 20 30-days

MMDAs (4.5%)

(no minimum balance requirement) 340 30-days

30-day repricing gap: RSAs = $150m. + $355m. = $505m.

6-month repricing gap: RSAs = $505m. + $150m. + $50m. + $250m. + $275m. + $200m.

1-year repricing gap: RSAs = $1655m. + $300m. + $200m. + $400m. = $2555m.

2-year repricing gap: RSAs = $2555m. + $100m. = $2655m.

5-year repricing gap: RSAs = $2655m. + $350m. = $3005m.

b. What is the impact over the next six months on net interest income if interest rates on RSAs

increase 60 basis points and on RSLs increase 40 basis points?

Chapter 08 – Interest Rate Risk I

8-27

c. What is the impact over the next year on net interest income if interest rates on RSAs increase

60 basis points and on RSLs increase 40 basis points?