Chapter 08 – Interest Rate Risk I

8-1

Solutions for End-of-Chapter Questions and Problems: Chapter Eight

1. How do monetary policy actions made by the Federal Reserve impact interest rates?

Through its daily open market operations, such as buying and selling Treasury bonds and

2. How has the increased level of financial market integration affected interest rates?

Increased financial market integration, or globalization, increases the speed with which interest

3. What is the repricing gap? In using this model to evaluate interest rate risk, what is meant

by rate sensitivity? On what financial performance variable does the repricing model

focus? Explain.

8-2

Education.

4. What is a maturity bucket in the repricing model? Why is the length of time selected for

repricing assets and liabilities important when using the repricing model?

The maturity bucket is the time window over which the dollar amounts of assets and liabilities

5. What is the CGAP effect? According to the CGAP effect, what is the relation between

changes in interest rates and changes in net interest income when CGAP is positive? When

CGAP is negative?

6. Which of the following is an appropriate change to make on a bank’s balance sheet

when GAP is negative, spread is expected to remain unchanged and interest rates are

expected to rise?

8-3

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

d. Replace equity with demand deposits

No. This change will have no impact on either RSAs or RSLs. So, will have no impact on GAP.

e. Replace vault cash with marketable securities

Yes. This change will increase RSAs, which will increase GAP.

7. If a bank manager was quite certain that interest rates were going to rise within the next six

months, how should the bank manager adjust the bank’s six-month repricing gap to take

advantage of this anticipated rise? What if the manger believed rates would fall in the next

six months.

8. Consider the following balance sheet positions for a financial institution:

• Rate-sensitive assets = $200 million. Rate-sensitive liabilities = $100 million

• Rate-sensitive assets = $100 million. Rate-sensitive liabilities = $150 million

• Rate-sensitive assets = $150 million. Rate-sensitive liabilities = $140 million

a. Calculate the repricing gap and the impact on net interest income of a 1 percent

increase in interest rates for each position.

Chapter 08 – Interest Rate Risk I

8-4

b. Calculate the impact on net interest income on each of the above situations assuming a

1 percent decrease in interest rates.

c. What conclusion can you draw about the repricing model from these results?

9. Consider the following balance sheet for MMC Bancorp (in millions of dollars):

Assets Liabilities

1. Cash and due from $ 6.25 1. Equity capital (fixed) $25.00

2. Short-term consumer loans 62.50

(one-year maturity) 2. Demand deposits 50.00

3. Long-term consumer loans 31.25

(two-year maturity) 3. Passbook savings 37.50

4. Three-month T-bills 37.50 4. Three-month CDs 50.00

5. Six-month T-notes 43.75 5. Three-month banker’s

acceptances 25.00

6. Three-year T-bonds 75.00 6. Six-month commercial paper 75.00

7. 10-year, fixed-rate mortgages 25.00 7. One-year time deposits 25.00

8. 30-year, floating-rate

mortgages 50.00 8. Two-year time deposits 50.00

9. Premises 6.25

$337.50 $337.50

a. Calculate the value of MMC’s rate-sensitive assets, rate sensitive liabilities, and

repricing gap over the next year.

Looking down the asset side of the balance sheet, we see the following one-year rate-sensitive

assets (RSA):

Chapter 08 – Interest Rate Risk I

8-5

Education.

Summing these four items produces one-year RSA of $193.75 million. The remaining $143.75

million is not rate sensitive over the one-year repricing horizon. A change in the level of interest

rates will not affect the interest revenue generated by these assets over the next year. The $6.25

million in the cash and due from category and the $6.25 million in premises are nonearning

Looking down the liability side of the balance sheet, we see that the following liability items

clearly fit the one-year rate or repricing sensitivity test:

Summing these four items produces one-year rate-sensitive liabilities (RSL) of $175 million. The

remaining $162.50 million is not rate sensitive over the one-year period. The $25 million in

equity capital and $50 million in demand deposits do not pay interest and are therefore classified

b. Calculate the expected change in the net interest income for the bank if interest rates

rise by 1 percent on both RSAs and RSLs. If interest rates fall by 1 percent on both

RSAs and RSLs.

Chapter 08 – Interest Rate Risk I

8-6

The CGAP would project the expected annual change in net interest income ()NII) of the bank is:

10. What are the reasons for not including demand deposits as rate-sensitive liabilities in the

repricing analysis for a commercial bank? What is the subtle but potentially strong reason

for including demand deposits in the total of rate sensitive liabilities? Can the same

11. What is the gap to total assets ratio? What is the value of this ratio to interest rate risk

managers and regulators?

Chapter 08 – Interest Rate Risk I

8-7

Education.

12. Which of the following assets or liabilities fit the one-year rate or repricing sensitivity test?

3-month U.S. Treasury bills Yes

1-year U.S. Treasury notes Yes

20-year U.S. Treasury bonds No

20-year floating-rate corporate bonds with annual repricing Yes

30-year floating-rate mortgages with repricing every two years No

30-year floating-rate mortgages with repricing every six months Yes

Overnight fed funds Yes

9-month fixed-rate CDs Yes

1-year fixed-rate CDs Yes

5-year floating-rate CDs with annual repricing Yes

Common stock No

13. What is the spread effect?

The spread effect is the effect that a change in the spread between rates on RSAs and RSLs has

14. A bank manager is quite certain that interest rates are going to fall within the next six

months. How should the bank manager adjust the bank’s six-month repricing gap and

spread to take advantage of this anticipated rise? What if the manger believes rates will rise

15. Consider the following balance sheet for WatchoverU Savings, Inc. (in millions):

30-year fixed-rate loans 3-year time deposits

Chapter 08 – Interest Rate Risk I

8-8

Education.

a. What is WatchoverU’s expected net interest income at year-end?

b. What will net interest income be at year-end if interest rates rise by 2 percent?

c. Using the cumulative repricing gap model, what is the expected net interest income for

a 2 percent increase in interest rates?

d. What will net interest income be at year-end if interest rates on RSAs increase by 2

percent but interest rates on RSLs increase by 1 percent? Is it reasonable for changes in

interest rates on RSAs and RSLs to differ? Why?

16. Use the following information about a hypothetical government security dealer named M.

P. Jorgan. Market yields are in parenthesis, and amounts are in millions.

Assets Liabilities and Equity

Cash $10 Overnight repos $170

1-month T-bills (7.05%) 75 Subordinated debt

3-month T-bills (7.25%) 75 7-year fixed rate (8.55%) 150

2-year T-notes (7.50%) 50

8-year T-notes (8.96%) 100

5-year munis (floating rate)

(8.20% reset every 6 months) 25 Equity 15

Total assets $335 Total liabilities & equity $335

a. What is the repricing gap if the planning period is 30 days? 3 months? 2 years? Recall

that cash is a non-interest-earning asset.

Chapter 08 – Interest Rate Risk I

8-9

Education.

b. What is the impact over the next 30 days on net interest income if interest rates increase

50 basis points? Decrease 75 basis points?

c. The following one-year runoffs are expected: $10 million for two-year T-notes and $20

million for eight-year T-notes. What is the one-year repricing gap?

d. If runoffs are considered, what is the effect on net interest income at year-end if interest

rates increase 50 basis points? Decrease 75 basis points?

17. A bank has the following balance sheet:

Assets Avg. Rate Liabilities/Equity Avg. Rate

Rate sensitive $550,000 7.75% Rate sensitive $375,000 6.25%

Fixed rate 755,000 8.75 Fixed rate 805,000 7.50

Nonearning 265,000 Nonpaying 390,000

Total $1,570,000 Total $1,570,000

Suppose interest rates rise such that the average yield on rate-sensitive assets increases by

45 basis points and the average yield on rate-sensitive liabilities increases by 35 basis

points.

a. Calculate the bank’s repricing GAP, gap to total assets ratio, and gap ratio.

Chapter 08 – Interest Rate Risk I

8-10

Education.

b. Assuming the bank does not change the composition of its balance sheet, calculate the

resulting change in the bank’s interest income, interest expense, and net interest income.

c. Explain how the CGAP and spread effects influenced the change in net interest income.

18. A bank has the following balance sheet:

Assets Avg. Rate Liabilities/Equity Avg. Rate

Rate sensitive $550,000 7.75% Rate sensitive $575,000 6.25%

Fixed rate 755,000 8.75 Fixed rate 605,000 7.50

Nonearning 265,000 Nonpaying 390,000

Total $1,570,000 Total $1,570,000

Suppose interest rates fall such that the average yield on rate-sensitive assets decreases by

15 basis points and the average yield on rate-sensitive liabilities decreases by 5 basis

points.

a. Calculate the bank’s CGAP, gap to total asset ratio, and gap ratio.

b. Assuming the bank does not change the composition of its balance sheet, calculate the

resulting change in the bank’s interest income, interest expense, and net interest income.

Chapter 08 – Interest Rate Risk I

8-11

Education.

c. The bank’s CGAP is negative and interest rates decreased, yet net interest income

decreased. Explain how the CGAP and spread effects influenced this decrease in net

interest income.

19. The balance sheet of A. G. Fredwards, a government security dealer, is listed below.

Market yields are in parentheses, and amounts are in millions.

Assets Liabilities and Equity

Cash $20 Overnight repos $340

1-month T-bills (7.05%) 150 Subordinated debt

3-month T-bills (7.25%) 150 7-year fixed rate (8.55%) 300

2-year T-notes (7.50%) 100

8-year T-notes (8.96%) 200

5-year munis (floating rate)

(8.20% reset every 6 months) 50 Equity 30

Total assets $670 Total liabilities and equity $670

a. What is the repricing gap if the planning period is 30 days? 3 month days? 2 years?

b. What is the impact over the next three months on net interest income if interest rates on

RSAs increase 50 basis points and on RSLs increase 60 basis points?

c. What is the impact over the next two years on net interest income if interest rates on

RSAs increase 50 basis points and on RSLs increase 75 basis points?

Chapter 08 – Interest Rate Risk I

8-12

Education.

d. Explain the difference in your answers to parts (b) and (c). Why is one answer a

negative change in NII, while the other is positive?

20. A bank has the following balance sheet:

Assets Avg. Rate Liabilities/Equity Avg. Rate

Rate sensitive $225,000 6.35% Rate sensitive $300,000 4.25%

Fixed rate 550,000 7.55 Fixed rate 505,000 6.15

Nonearning 120,000 Nonpaying 90,000

Total $895,000 Total $895,000

Suppose interest rates rise such that the average yield on rate-sensitive assets increases by

45 basis points and the average yield on rate-sensitive liabilities increases by 35 basis

points.

a. Calculate the bank’s repricing GAP.

b. Assuming the bank does not change the composition of its balance sheet, calculate the

net interest income for the bank before and after the interest rate changes. What is the

resulting change in net interest income?

c. Explain how the CGAP and spread effects influenced this increase in net interest

income.

Chapter 08 – Interest Rate Risk I

8-13

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

The CGAP affect worked to decrease net interest income. That is, the CGAP was negative while

interest rates increased. Thus, interest income increased by less than interest expense. The result

is a decrease in NII. In contrast, the spread effect worked to increase net interest income. The

spread increased by 10 basis points. According to the spread affect, as spread increases, so does

net interest income. However, in this case, the increase in NII due to the spread effect was

dominated by the decrease in NII due to the CGAP effect.

21. What are some of the weakness of the repricing model? How have large banks solved the

problem of choosing the optimal time period for repricing? What is runoff cash flow, and

how does this amount affect the repricing model’s analysis?

The repricing model has four general weaknesses:

22. What is a maturity gap? How can the maturity model be used to immunize an FI’s

portfolio? What is the critical requirement that allows maturity matching to have some

success in immunizing the balance sheet of an FI?

Chapter 08 – Interest Rate Risk I

8-14

23. Nearby Bank has the following balance sheet (in millions):

Assets Liabilities and Equity

Cash $60 Demand deposits $140

5-year Treasury notes 60 1-year certificates of deposit 160

30-year mortgages 200 Equity 20

Total assets $320 Total liabilities and equity $320

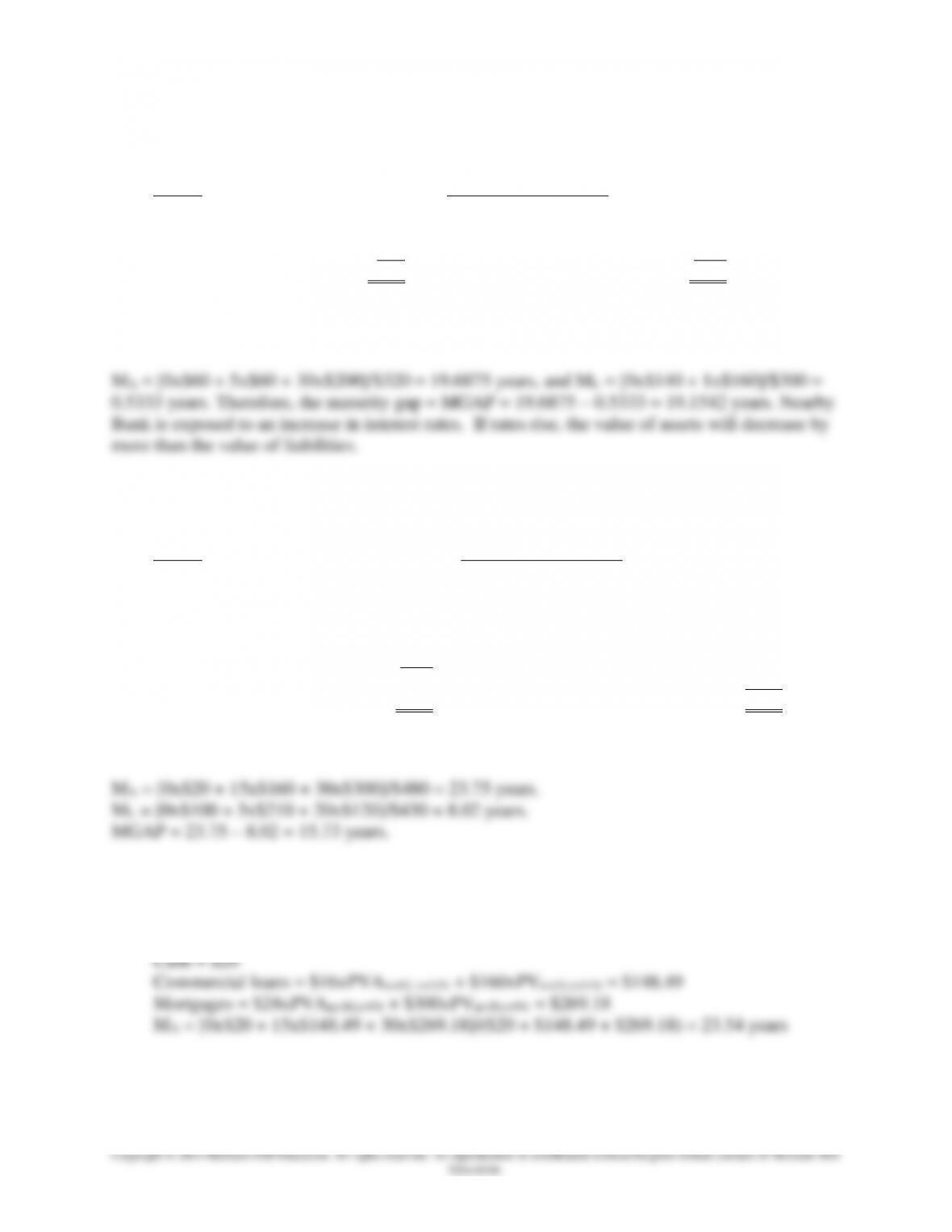

What is the maturity gap for Nearby Bank? Is Nearby Bank more exposed to an increase or

decrease in interest rates? Explain why?

24. County Bank has the following market value balance sheet (in millions, all interest at

annual rates). All securities are selling at par equal to book value.

Assets Liabilities and Equity

Cash $20 Demand deposits $100

15-year commercial loan at 10% 5-year CDs at 6% interest,

interest, balloon payment 160 balloon payment 210

30-year mortgages at 8% interest, 20-year debentures at 7% interest, 120

balloon payment 300 balloon payment

Equity 50

Total assets $480 Total liabilities & equity $480

a. What is the maturity gap for County Bank?

b. What will be the maturity gap if the interest rates on all assets and liabilities increase by

1 percent?

If interest rates increase one percent, the value and average maturity of the assets will be: