Chapter 24 – Swaps

24–15

d. How can the Swiss bank reduce that risk exposure?

e. If the US dollar is expected to appreciate against the SF to SF1.65/$, SF1.815/$, and

SF2.00/$ over the next three years, respectively, what will be the cash flows on this

transaction?

Eurodollar CD Swiss loan

t Cash Outflow (US$) (SF) cash inflow (SF) Spread (SF)

f. If the Swiss bank swaps US$ payments for SF payments at the current spot exchange

rate, what are the cash flows on the swap? What are the cash flows on the entire hedged

position? Assume that the U.S. dollar appreciates at the rates in part (e).

Net swap

t Cash flow (SF) Swap payments(SF) cash flow (SF) Total cash flow

The cash flows of the underlying cash position from part (e) are added to the net cash flows from

g. What are the cash flows on the swap and the hedged position if actual spot exchange

rates are as follows:

Chapter 24 – Swaps

24–16

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Total end of year 1 cash flows are net swap cash flows of SF0.35m plus the loan – CD spread of

SF2.65m (SF13.5m – SF10.85m). Total end of year 2 cash flows are -SF0.21m on the swap plus

SF3.21m (SF13.5m – SF10.29m). End of year 3 cash flows are -SF2.14m on the swap plus

SF5.14m on the loan – CD spread (SF163.5m – SF158.36m). The loan cash flows in SF are given

in column four of part (e).

h. What would be the bank’s risk exposure if the fixed-rate Swiss loan was financed with a

floating rate U.S. $100 million, three-year Eurodollar CD?

i. What type(s) of hedge is appropriate if the Swiss bank in part (h) wants to reduce its

risk exposure?

j. If the annual Eurodollar CD rate is set at LIBOR and LIBOR at the end of years 1, 2,

and 3 is expected to be 7 percent, 8 percent, and 9 percent, respectively, what will be

the cash flows on the bank’s unhedged cash position? Assume no change in exchange

rates.

Eurodollar CD Swiss loan

t cash outflow (US$) (SF) cash inflow (SF) Spread (SF)

k. What are the cash flows on the bank’s unhedged cash position if exchange rates are as

follows:

Eurodollar CD Swiss loan

t cash outflow (US$) (SF) cash inflow (SF) Spread (SF)

Chapter 24 – Swaps

24–17

Education.

Without the swap, the cost to the bank of meeting the Eurodollar CD payments at the end of year

1 would be SF10.85m (US$7m x 1.55). At the end of year 2 the cost would be SF11.76m

(US$8m x 1.47). At the end of year 3, the cost would be SF161.32m (US$109m x 1.48).

l. What are both the swap and total hedged position cash flows if the bank swaps out its

floating rate US$ CD payments in exchange for 7.75 percent fixed-rate SF payments at

the current spot exchange rate of SF1.50/$?

Net swap

t Cash flow (SF) Swap payments(SF) cash flow (SF) Total cash flow

The total cash flows are:

m. If forecasted interest rates are 7 percent, 10.14 percent, and 10.83 percent over the next

three years, respectively, and exchange rates over the next years are those in part (k),

calculate the cash flows on an 8.75 percent fixed-floating-rate swap of U.S. dollars to

Swiss francs at SF1.50/$.

Net swap

t Cash flow (SF) Swap payments(SF) cash flow (SF) Total cash flow

15. Bank A has the following balance sheet information (in millions):

Assets Liabilities and Equity

Rate-sensitive assets $50 Rates-sensitive liabilities $75

Chapter 24 – Swaps

24–18

Education.

Fixed-rate assets 150 Fixed-rate liabilities 100

Net worth 25

Total assets $200 Total liabilities and equity $200

Rate-sensitive assets are repriced quarterly at the 91-day Treasury bill rate plus 150 basis

points. Fixed-rate assets have five years until maturity and are paying 9 percent annually.

Rate-sensitive liabilities are repriced quarterly at the 91-day Treasury bill rate plus 100

basis points. Fixed-rate liabilities have two years until maturity and are paying 7 percent

annually. Currently, the 91-day Treasury bill rate is 6.25 percent.

a. What is the bank’s current net interest income? If Treasury bill rates increase 150 basis

points, what will be the change in the bank’s net interest income?

b. What is the bank’s repricing or funding gap? Use the repricing model to calculate the

change in the bank’s net interest income if interest rates increase 150 basis points.

c. How can swaps be used as an interest rate hedge in this example?

16. Use the following information to construct a swap of asset cash flows for the bank in

problem 15. The bank is a price taker in both the fixed-rate market at 9 percent and the

rate-sensitive market at the T-bill rate plus 1.5 percent. A securities dealer has a large

portfolio of rate sensitive assets funded with fixed-rate liabilities. The dealer is a price taker

in a fixed-rate asset market paying 8.5 percent and a floating-rate asset market paying the

91-day T-bill rate plus 1.25 percent. All interest is paid annually.

a. What is the interest rate risk exposure to the securities dealer?

Chapter 24 – Swaps

b. How can the bank and the securities dealer use a swap to hedge their respective interest

rate risk exposures?

c. What are the total potential gains to the swap?

d. Consider the following two-year swap of asset cash flows: An annual fixed-rate asset

cash flow of 8.6 percent in exchange for a floating-rate asset cash flow of T-bill plus

125 basis points. The swap intermediary fee is 5 basis points. How are the swap gains

apportioned between the bank and the securities dealer if they each hedge their interest

rate risk exposures using this swap?

Bank Securities Dealer

Variable-rate Fixed-rate swap payments Fixed-rate

liabilities 8.6% liabilities

T-bill+1.25%

Variable-rate swap payments

Cash

Financing

Fixed-rate Markets Variable-rate

assets @ 9.0% assets @ T-bill+1.25%

Swap Cash Flows

Chapter 24 – Swaps

24–20

Education.

e. What are the realized cash flows if T-bill rates at the end of the first year are 7.75

percent and at the end of the second year are 5.5 percent? Assume that the notional

value is $107.14 million.

At the end of the first year (in millions of dollars):

Bank Cash Flows Securities Dealer Cash Flows

f. What are the sources of the swap gains to trade?

g. What are the implications for the efficiency of cash markets?

17. Consider the following currency swap of coupon interest on the following assets:

Chapter 24 – Swaps

24–21

Education.

a. What is the face value of the SF bond if the investments are equivalent at spot rates?

b. What are the realized cash flows, assuming no change in spot exchange rates? What are

the net cash flows on the swap?

c. What are the cash flows if the spot exchange rate falls to SF0.50/$? What are the net

cash flows on the swap?

d. What are the cash flows if the spot exchange rate rises to SF2.25/$? What are the net

cash flows on the swap?

e. Describe the underlying cash position that would prompt the FI to hedge by swapping

dollars in exchange for Swiss francs.

18. Consider the following fixed-floating-rate currency swap of assets: 5 percent (annual

coupon) fixed-rate U.S. $1 million bond and floating-rate SF1.5 million bond set at LIBOR

annually. Currently LIBOR is 4 percent. The face value of the swap is SF1.5 million. The

spot exchange rate is SF1.5/$.

a. What are the realized cash flows on the swap at the spot exchange rate?

Chapter 24 – Swaps

24–22

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

equivalent to $40,000. The net cash flows on the swap are $10,000, or SF15,000. The

counterparty that swaps in U.S. dollar bond payments receives the cash flows. The counterparty

that swaps in the Swiss franc payments makes the payments.

b. If the 1-year forward rate is SF1.538 per US$, what are the realized net cash flows on

the swap? Assume LIBOR is unchanged.

c. If LIBOR increases to 6 percent, what are the realized cash flows on the swap?

Evaluate at the forward rate.

19. Give two reasons why credit swaps have been the fastest-growing form of swaps in recent

years?

20. What is a total return swap?

21. How does a pure credit swap differ from a total return swap? How does it differ from a

digital default option?

Chapter 24 – Swaps

24–23

Education.

22. Why is the credit risk on a swap lower that the credit risk on a loan?

The credit risk on a swap is lower than that of a loan for the following reasons:

23. What is netting by novation?

24. What role did the swap market play in the financial crisis of 2008-2009?

Chapter 24 – Swaps

24–24

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Global funding market pressures were also evident in the virtual shut-down of the FX

swap market during the financial crisis. This risk was driven by demand for dollar funding from

global financial institutions, particularly European financial institutions. As many of these

institutions increasingly struggled to obtain funding in the unsecured cash markets, they turned to

the FX swap market as a primary channel for raising dollar funding. This extreme demand for

dollar funding led a sizable shift in FX forward prices, with the implied dollar funding rate

observed in FX swaps on many major currencies rising sharply above that suggested by the other

relative interest measures such as the dollar OIS (overnight index swap) rate and the dollar Libor.

Dealers reported that bid-ask spreads on FX swaps increased to as much as 10 times the levels

that had prevailed before August 2007. During the quarter, the spread of the three month FX

swap-implied dollar rate from euro and sterling—US dollar FX forward points—over the dollar

Libor fixing rate widened to around 330 and 260 basis points, respectively, in early October after

the Lehman failure.

The following problem refers to material in Appendix 24A.

25. The following information is available on a three-year swap contract. One-year maturity

zero coupon discount yields are currently priced at par and pay a coupon rate of 5 percent.

Two-year maturity zero-coupon discount yields are currently 5.51 percent. Three-year

maturity zero-coupon discount yields are currently 5.775 percent. The terms of a three-year

swap of $100 million notional value are 5.45 percent annual fixed-rate payments in

exchange for floating-rate payments tied to the annual discount yield.

a. If an insurance company buys this swap, what can you conclude about the interest rate

risk exposure of the company’s underlying cash position?

b. What are the realized cash flows expected over the three-year life of the swap?

Chapter 24 – Swaps

24–25

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Cash outflow -$5.45 million + Cash inflow $5.775 million = $0.325 million net cash inflow

c. What are the realized cash flows that occur over the three-year life of the swap if d2 =

4.95 percent and d3 = 6.1 percent?

Integrated Mini Case: Hedging Interest Rate Risk with Futures versus Options versus Swaps

On January 4, 2015, an FI has the following balance sheet (rates = 8 percent)

Assets Liabilities/Equity

A 450m DA = 8 years L 396m DL = 4 years

E 54m

DGAP = [8 – (396/450)4] = 4.48 years > 0

Chapter 24 – Swaps

24–26

The FI manager thinks rates will increase by 0.55 percent in the next three months. If this

happens, the equity value will change by:

mE 450)]4(8[ 450

396

−−=

667,266,10$

08.1

0055.0 −=

The FI manager will hedge this interest rate risk with either futures contracts, option contracts, or

swap contracts.

If the FI uses futures, it will select June T-bonds to hedge. The duration on the T-bonds

underlying the contract is 14.5 years, and the T-bond futures are selling at a price of $110.53125

per $100, or $110,531.25. T-bond futures rates, currently 5 percent, are expected to increase by

0.75 percent over the next three months.

Chapter 24 – Swaps

24–27

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Loss on balance sheet Gain off balance sheet (options)

08.1

005.0

450

396 450)]4(8[ mE −−=

=

0525.1

0066.0

25.781,115)5.14)(85.0(7536.081,10 −−=

=

-$9,333,333 $9,680,000

The net gain is $9,333,333 – $9,680,000 = $346,667

For a hedge with swap contracts:

000,000,288$

18

450]4)

450

396

(8[ == −

−m

s

N

buy swap

On April 4, 2015, as the FI gets out of the swap hedge:

If by April 4, 2015, balance sheet rates actually fall by 0.25 percent, futures rates fall by 0.35

percent, and T-bond rates underlying the option contract fall by 0.34 percent, calculate the on

and off-balance-sheet cash flows to the FI when using futures contracts, option contracts, and

swap contracts as its hedge instrument.

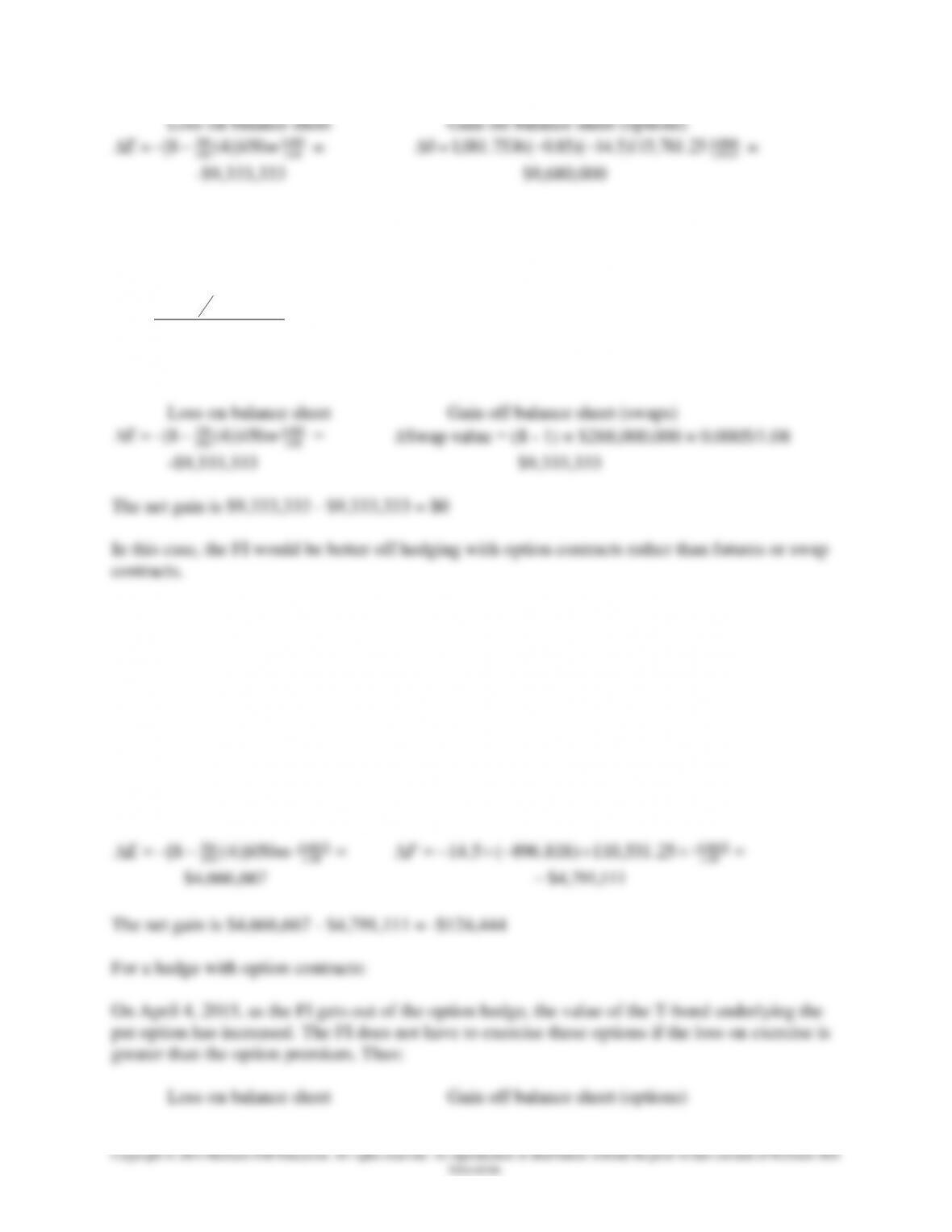

On April 4, 2015, as the FI gets out of the futures hedge:

Loss on balance sheet Gain off balance sheet (futures)

0025.0

396 450)]4(8[ mE

0035.0

08.1

005.0

450

396 450)]4(8[ mE −−=

Chapter 24 – Swaps

24–28

0025.0

396 450)]4(8[ −

0034.0