Chapter 20 – Capital Adequacy

20–15

Education.

commercial paper 100 100 $30 million

27. How does the leverage ratio test impact the stringency of regulatory monitoring of DI

capital positions?

28. Third Bank has the following balance sheet (in millions), with the risk weights in

parentheses.

Assets Liabilities and Equity

Cash (0%) $21 Deposits $176

OECD interbank deposits (20%) 25 Subordinated debt (5 years) 2

Mortgage loans (50%) 70 Cumulative preferred stock 2

Consumer loans (100%) 70 Equity 5

Reserve for loan losses (1)

Total Assets $185 Total liabilities and equity $185

The cumulative preferred stock is qualifying and perpetual. In addition, the bank has $30

million in performance-related standby letters of credit (SLCs) to a public corporation, $40

million in two-year forward FX contracts that are currently in the money by $1 million, and

$300 million in six-year interest rate swaps that are currently out of the money by $2

million. Credit conversion factors follow:

Performance-related standby LCs 50%

1- to 5-year foreign exchange contracts 5%

1- to 5-year interest rate swaps 0.5%

5- to 10-year interest rate swaps 1.5%

a. What are the risk-adjusted on-balance-sheet assets of the bank as defined under the

Basel Accord?

Chapter 20 – Capital Adequacy

20–16

Education.

Risk-adjusted assets:

b. To be adequately capitalized, what are the CET1, Tier I, and total capital required for

both off- and on-balance-sheet assets?

c. Disregarding the capital conservation buffer, does the bank have enough capital to meet

the Basel requirements? If not, what minimum CET1, additional Tier 1, or total capital

does it need to meet the requirement?

Chapter 20 – Capital Adequacy

20–17

New balance sheet:

Cash $22.01 Deposits $176

d. Does the bank have enough capital to meet the Basel requirements, including the capital

conservation buffer requirement? If not, what minimum CET1, additional Tier 1, or total

capital does it need to meet the requirement?

No, the bank does not have sufficient total capital to meet the Basel requirements. It needs CET1

capital of $9.345 million, Tier I capital of $11.3475 million, and total capital of $14.0175

million. The bank has $5 million of CET1 capital, $7 million of Tier I capital, and $10 million of

total capital.

Chapter 20 – Capital Adequacy

20–18

Education.

29. Third Fifth Bank has the following balance sheet (in millions), with the risk weights in

parentheses.

Assets Liabilities and Equity

Cash (0%) $21 Deposits $133

Mortgage loans (50%) 50 Subordinated debt (> 5 years) 1

Consumer loans (100%) 70 Equity 6

Reserve for loan losses (1)

Total assets $140 Total Liabilities and equity $140

In addition, the bank has $20 million in commercial direct-credit substitute standby letters

of credit to a public corporation and $40 million in 10-year FX forward contracts that are in

the money by $1 million.

a. What are the risk-adjusted on-balance-sheet assets of the bank as defined under the

Basel III?

b. What is the CET1, Tier I, and total capital required for both off- and on-balance-sheet

assets?

c. Disregarding the capital conservation buffer, does the bank have sufficient capital to

meet the Basel requirements? How much in excess? How much short?

Chapter 20 – Capital Adequacy

20–19

Education.

d. Does the bank have enough capital to meet the Basel requirements, including the capital

conservation buffer requirement? If not, what minimum CET1, additional Tier 1, or total

capital does it need to meet the requirement?

Total risk-adjusted on- and off-balance-sheet assets = $118

Chapter 20 – Capital Adequacy

20–20

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

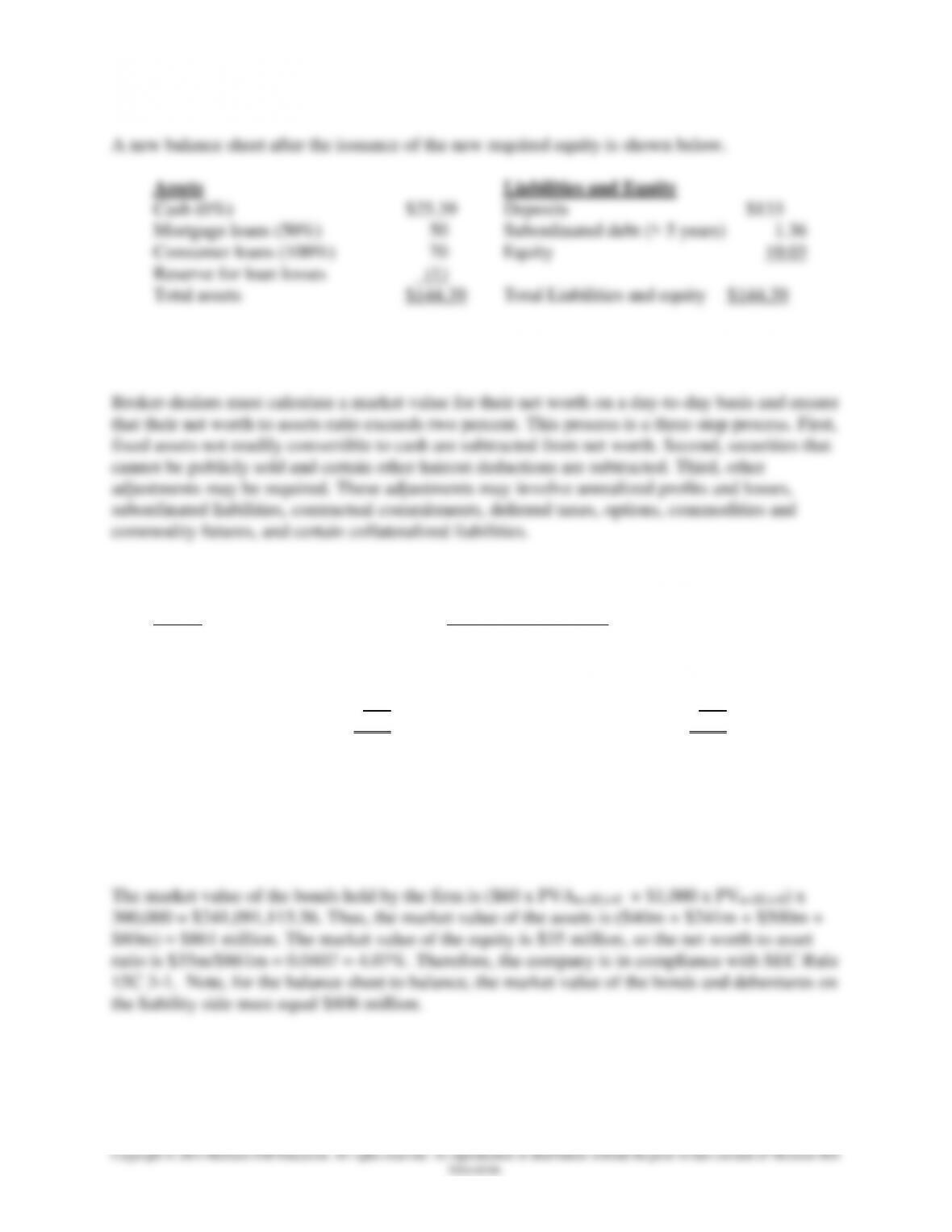

A new balance sheet after the issuance of the new required equity is shown below.

Assets Liabilities and Equity

Cash (0%) $25.39 Deposits $133

Mortgage loans (50%) 50 Subordinated debt (> 5 years) 1.36

Consumer loans (100%) 70 Equity 10.03

Reserve for loan losses (1)

Total assets $144.39 Total Liabilities and equity $144.39

30. According to SEC Rule 15C 3-1, what adjustments must securities firms make in the

calculation of the book value of net worth?

31. A securities firm has the following balance sheet (in millions):

Assets Liabilities and Equity

Cash $40 Five-day commercial paper $20

Debt securities 300 Bonds 550

Equity securities 500 Debentures 300

Other assets 60 Equity 30

Total assets $900 Total liabilities and equity $900

The debt securities have a coupon rate of 6 percent, 20 years remaining until maturity, and

trade at a yield of 8 percent. The equity securities have a market value equal to book value,

and the other assets represent building and equipment which was recently appraised at $80

million. The company has 1 million shares of stock outstanding and its price is $35 per

share. Is this company in compliance with SEC Rule 15C 3-1?

Chapter 20 – Capital Adequacy

20–21

Education.

32. An investment bank specializing in fixed-income assets has the following balance sheet (in

millions). Amounts are in market values, and all interest rates are annual unless indicated

otherwise.

Assets Liabilities and Equity

Cash $0.5 5% 1-year Eurodollar deposits $5.0

8% 10-year Treasury-notes 6% 2-year subordinated debt

semi-annual (par = $16.0) 15.0 (par = $10.0) 10.0

Equity 0.5

Total assets $15.5 Total liabilities and equity $15.5

Assume that the haircut for all assets is 15 basis points and for all liabilities, 25 basis points

(per year).

a. Does the investment bank have sufficient liquid capital to cushion any unexpected

losses per the net capital rule?

b. What should the FI do to maintain the net minimum required liquidity?

c. How does the net capital rule for investment banks differ from the capital requirements

imposed on commercial banks and other depository institutions?

Chapter 20 – Capital Adequacy

20–22

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

The differences between depository institutions and securities firms are:

(a) No netting is done for depository institutions. In securities firms, both assets and

liabilities are netted.

(b) In securities firms, cash is the cushion. With DIs it is the capital (CET1, Tier I, and Tier

II).

(c) Haircuts are based on years to maturity, liquidity, ratings, and other factors.

33. Identify and define the five risk categories incorporated into the life insurance risk-based

capital model.

a. Asset risk–affiliate is the risk of default of assets for affiliated investments.

34. A life insurance company has estimated capital requirements for each of the following risk

classes: asset risk-affiliate (C0) = $2 million, asset risk-other (C1) = $5 million, insurance

risk (C2) = $4 million, interest rate, credit, market risk (C3) = $1 million, and business risk

(C4) = $3 million.

a. What is the required risk-based capital for the life insurance company?

b. If the total surplus and capital held by the company is $11.34 million, does it meet the

minimum requirements?

c. How much capital must be raised to meet the minimum requirements?

Chapter 20 – Capital Adequacy

20–23

Education.

35. How do the risk categories in the risk-based capital model for property-casualty insurance

companies differ from those of life insurance companies? What are the assumed

relationships between the risk categories in the model?

36. A property-casualty insurance company has estimated the following required charges for its

various risk classes (in millions):

Risk Description RBC Charge

R0 Affiliated P/C $2

R1 Fixed income 3

R2 Common stock 4

R3 Reinsurance 3

R4 Loss adjustment expense 2

R5 Written premiums 3

Total $17

a. What is the RBC charge as per the model recommended by the NAIC?

b. If the firm currently has $7 million in capital, what should be its surplus to meet the

minimum capital requirement?

Chapter 20 – Capital Adequacy

20–24

Education.

Integrated Mini Case: Calculating Capital Requirements

A bank’s balance sheet information is shown below (in $000).

Used for answers to 1-4

On Balance Sheet Items Face Value Weight Value

Cash $121,600 0% $0

Short-term government securities (<92 days.) 5,400 0% $0

Long-term government securities (>92 days) 414,400 0% $0

Federal Reserve stock 9,800 0% $0

Repos secured by federal agencies 159,000 20% $31,800

Claims on U.S. depository institutions 937,900 20% $187,580

Loans to foreign banks, OECD CRC rated 2 1,640,000 20% $328,000

General obligations municipals 170,000 20% $34,000

Claims on or guaranteed by federal agencies 26,500 20% $5,300

Municipal revenue bonds 112,900 50% $56,450

Residential mortgages,

category 1, loan-to-value ratio 75% 5,000,000 50% $2,500,000

Commercial loans 4,667,669 100% $4,667,669

Loans to sovereigns, OECD CRC rated 3. 11,600 50% $5,800

Premises and equipment 455,000 100% $455,000

Conversion Face Credit-Equivalent Risk-Adjusted

Off Balance Sheet Items: Factor Value Amount Asset Value

U.S. Government Counterparty

Loan commitments:

< 1 year 20% $300 $60 $0

1-5 year 50% 1,140 570 0

Standby letters of credit:

Performance-related 50% 200 100 0

Direct-credit substitute 100% 100 100 0

U.S. Depository Institutions Counterparty

Loan commitments:

< 1 year. 20% 100 20 4

> 1 year 50% 3,000 1,500 1300

Standby letters of credit:

Performance-related 50% 200 100 20

Direct-credit substitute 100% 56,400 56,400 11,280

Commercial letters of credit: 20% 400 80 16

Chapter 20 – Capital Adequacy

20–25

State and Local Government Counterparty

(revenue municipals)

Loan commitments:

>1 year 50% 100 50 25

Standby letters of credit:

Performance-related 50% 135,400 67,700 33,850

Corporate Customer Counterparty

Loan commitments:

< 1 year 20% 3,212,400 642,480 642,480

>1 year 50% 3,046,278 1,523,139 1,523,139

Standby letters of credit:

Performance-related 50% 101,543 50,772 50,772

Direct-credit substitute 100% 490,900 490,900 490,9000

Commercial letters of credit: 20% 78,978 15,796 15,796

Sovereign Counterparty

Loan commitments, OECD CRC rated 1:

< 1 year 20% 110,500 22,100 0

>1 year 50% 1,225,400 612,700 0

Sovereign Counterparty

Loan commitments, OECD CRC rated 2:

< 1 year 20% 85,000 17,000 3,400

>1 year 50% 115,500 57,750 11,500

Sovereign Counterparty

Loan commitments, OECD CRC rated 7:

>1 year. 50% 30,000 15,000 22,500

Interest rate market contracts:

(current exposure assumed to be zero.)

< 1 year (notional amount) 0% 2,000 0 0

> 1-5 year (notional amount) 0.5% 5,000 25 25

1. What is the bank’s risk-adjusted asset base under Basel III?

The risk-adjusted asset base under Basel III is:

Chapter 20 – Capital Adequacy

20–26

Education.

2. To be adequately capitalized, what are the bank’s CET1, Tier I, and total risk-based capital

requirements under Basel III?

3. Using the leverage ratio requirement, what is the minimum regulatory capital required to

keep the bank in the well-capitalized zone?

4. Disregarding the capital conservation buffer, what is the bank’s capital adequacy level

(under Basel III) if the par value of its equity is $225,000, surplus value of equity is

$200,000, retained earnings is $565,545, qualifying perpetual preferred stock is $50,000,

subordinate debt is $50,000, and loan loss reserve is $85,000? Does the bank meet Basel

(CET1, Tier I, and Tier II) adequate capital standards? Does the bank comply with the

well-capitalized leverage ratio requirement?

5. Does the bank have enough capital to meet the Basel requirements, including the capital

conservation buffer requirement?

6. The bank’s various lines of business produced the following gross income:

Chapter 20 – Capital Adequacy

20–27

What is the add-on to capital for operational risk? Does the bank have sufficient capital to

cover this add-on and remain adequately capitalized, while meeting the capital

conservation buffer?