Chapter 19 – Deposit Insurance and Other Liability Guarantees

19-1

Solutions for End-of-Chapter Questions and Problems: Chapter Nineteen

1. What is a contagious run? What are some of the potentially serious adverse social welfare

effects of a contagious run? Do all types of FIs face the same risk of contagious runs?

2. How does federal deposit insurance help mitigate the problem of bank runs. What other

elements of the safety net are available to DIs in the United States?

3. What major changes did the Financial Institutions Reform, Recovery, and Enforcement Act

of 1989 make to the FDIC and the FSLIC?

4. Contrast the two views on, or reasons why, depository institution insurance funds can

become insolvent.

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19-2

5. What is moral hazard? How did the fixed-rate deposit insurance program of the FDIC

contribute to the moral hazard problem of the savings association industry? What other

changes in the savings association environment during the 1980s encouraged the developing

instability of the industry?

6. How does a risk-based insurance program solve the moral hazard problem of excessive risk

taking by FIs? Is an actuarially fair premium for deposit insurance always consistent with a

competitive banking system?

7. What are three suggested ways a deposit insurance contract could be structured to reduce

moral hazard behavior?

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19-3

Education.

8. What are some ways of imposing stockholder discipline to prevent FI managers from

engaging in excessive risk taking?

9. How is the provision of deposit insurance by the FDIC similar to the FDIC’s writing a put

option on the assets of a DI that buys the insurance? What two factors drive the premium of

the option?

10. What four factors were provided by FDICIA as guidelines to assist the FDIC in the

establishment of risk-based deposit insurance premiums? What happened to the level of

deposit insurance premiums in the late 1990s and early 2000s? Why?

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19-4

Education.

11. What is capital forbearance? How does a policy of forbearance potentially increase the

costs of financial distress to the insurance fund as well as the stockholders?

12. Under what conditions may the implementation of minimum capital guidelines, either risk-

based or non-risk-based, fail to impose stockholder discipline as desired by the regulators?

13. Why did the fixed-rate deposit insurance system fail to induce insured and uninsured

depositors to impose discipline on risky DIs in the United States in the 1980s?

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19-5

Education.

The fixed-rate deposit insurance system understandably provided no incentives to depositors to

discipline the actions of DIs since they were completely insured for deposits of up to $100,000

per account per DI. Uninsured depositors also had few incentives to monitor the activities of DIs

because regulators had been reluctant to close down failing DIs, especially larger DIs. This is

because of the anticipated widespread social implications. As a result, both insured and

uninsured depositors were usually protected against DI losses, reducing the incentives to monitor

the actions of DIs.

a. How is it possible to structure deposits in a DI to reduce the effects of the insured

ceiling?

b. What are brokered deposits? Why are brokered deposits considered more risky than

nonbrokered deposits by DI regulators?

c. What trade-offs were weighed in the decision to leave the deposit insurance ceiling at

$100,000 in 2005 and then increase the ceiling to $250,000?

14. What changes did the Federal Deposit Insurance Reform Act of 2005 make to the deposit

insurance cap?

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19-6

Education.

15. What is the too-big-to-fail doctrine? What factors caused regulators to act in a way that

caused this doctrine to evolve?

16. What are some of the essential features of the FDICIA of 1991 with regard to the resolution

of failing DIs?

The FDICIA of 1991 made it very difficult for regulators to delay the closing of failing DIs

unless the danger of a systemic risk can be shown. They are expected to use the least cost

resolution (LCR) strategy to close down DIs, and shareholders and uninsured depositors are

expected to bear the brunt of the loss. Unlike in prior years, the FDIC only subsidizes if the

liquidated assets are not sufficient to cover the insured deposits. The General Accounting Office

has also been authorized to audit failure resolutions used by regulators to ensure that the least

cost strategy has been adopted.

a. What is the least-cost resolution (LCR) strategy?

b. When can the systemic risk exemption be used as an exception to the LCR policy of DI

closure methods?

c. What procedural steps must be taken to gain approval for using the systemic risk

exemption?

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19-7

Education.

d. What are the implications to the other DIs in the economy of the implementation of this

exemption?

17. What is the primary goal of the FDIC when employing the LCR strategy?

a. How is the insured depositor transfer method implemented in the process of failure

resolution?

b. Why does this method of failure resolution encourage uninsured depositors to more

closely monitor the strategies of DI managers?

18. The following is a balance sheet of a commercial bank (in millions of dollars).

Assets Liabilities and Equity

Cash $ 5 Insured deposits $30

Loans 40 Uninsured deposits 10

Equity 5

Total assets $45 Total liabilities and equity $45

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19-8

Education.

The bank experiences a run on its deposits after it declares it will write off $10 million of

its loans as a result of nonpayment. The bank has the option of meeting the withdrawals by

first drawing down its cash and then by selling off its loans. A fire sale of the remaining

loans in one day can be accomplished at a 10 percent discount. They can be sold at a 5

percent discount if sold in two days. The full market value will be obtained if they are sold

after two days.

a. What is the amount of loss to the insured depositors if a run on the bank occurs on the

first day? On the second day?

b. What amount do the uninsured depositors lose if the FDIC uses the insured depositor

transfer method to close the bank immediately? The assets will be sold in two days.

19. A bank with insured deposits of $55 million and uninsured deposits of $45 million has

assets valued at only $75 million. What is the cost of failure resolution to insured

depositors, uninsured depositors, and the FDIC if an insured depositor transfer method is

used?

20. A commercial bank has $150 million in assets at book value. The insured and uninsured

deposits are valued at $75 million and $50 million, respectively, and the book value of

equity is $25 million. As a result of loan defaults, the market value of the assets has

decreased to $120 million. What is the cost of failure resolution to insured depositors,

uninsured depositors, shareholders, and the FDIC if an insured depositor transfer method is

used.

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19-9

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Under the insured depositor transfer method, all losses will be borne by shareholders, followed

by uninsured depositors, before the FDIC takes any loss. Thus, in this example, neither the

insured depositors nor the FDIC lose under the insured depositor transfer method. Uninsured

depositors receive $45 million (= $120m – $75m) equal to the cash (received from the sale of the

bank’s assets) remaining after insured depositors have been paid in full. This results in a loss of

$5 million (= $50m – $45m) for the uninsured depositors. Shareholders will lose $25 million.

21. In what ways did FDICIA enhance the regulatory discipline to help reduce moral hazard

behavior? What has the operational impact of these directives been?

22. Match the following policies with their intended consequences:

Policies:

a. Lower FDIC insurance levels

b. Stricter reporting standards

c. Risk-based deposit insurance

Consequences:

1. Increased stockholder discipline

2. Increased depositor discipline

3. Increased regulator discipline

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19–10

Education.

23. How does the Federal Reserve’s discount window serve as an alternative to deposit

insurance as a lender of last resort facility to financial institutions? What changes occurred

in 2008 that expanded the scope of coverage for the Fed’s discount window?

Traditionally, the Fed has provided a discount window facility to meet the short-term,

nonpermanent liquidity needs of DIs. For example, suppose a DI has an unexpected deposit drain

close to the end of a reserve requirement period and cannot meet its reserve target. It can seek to

borrow from the Fed’s discount window facility. However, in January 2003, the Fed

implemented changes to its discount window lending that increased the cost of borrowing but

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19–11

24. Why is access to the discount window of the Fed less of a deterrent to bank runs than

deposit insurance?

Although banks have access to the discount window in the event of DI runs, this is less effective

than deposit insurance because:

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19–12

Education.

d. If the DI ultimately fails, the Fed will have to compensate the FDIC for incremental losses.

25. How do insurance guaranty funds differ from deposit insurance? What impact do these

differences have on the incentive for insurance policyholders to engage in a contagious run

on an insurance company?

26. What was the purpose of the establishment of the Pension Benefit Guaranty Corporation

(PBGC)?

a. How does the PBGC differ from the FDIC in its ability to control risk?

b. How were the 1994 Retirement Protection Act and the Deficit Reduction Act of 2005

expected to reduce the deficits experienced by the PBGC?

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19–13

27. What changes did the Federal Deposit Insurance Reform Act of 2005 make to the deposit

insurance assessment scheme for DIs?

The Federal Deposit Insurance Reform Act of 2005 instituted a deposit insurance premium

scheme, effective January 1, 2007 and revised in April 2009 and April 2011, that combined

examination ratings, financial ratios, and for large banks (with total assets greater than $10

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19–14

28. Under the Federal Deposit Insurance Reform Act of 2005, how is a Category I deposit

insurance premium determined?

Within Risk Category I, the final rule combines CAMELS component ratings with financial ratios

to determine an institution’s assessment rate. For Risk Category I institutions, each of six

financial ratios component ratings is multiplied by a corresponding pricing multiplier, as listed in

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19–15

Education.

29. Webb Bank has a composite CAMELS rating of 2, a total risk-based capital ratio of 10.2

percent, a Tier I risk-based capital ratio of 5.2 percent, and a Tier I leverage ratio of 4.8

percent. What deposit insurance risk category does the bank fall into, and what is the

bank’s deposit insurance assessment rate?

30. Million Bank has a composite CAMELS rating of 2, a total risk-based capital ratio of 9.8

percent, a Tier I risk-based capital ratio of 5.8 percent, and a Tier I leverage ratio of 4.9

percent. The average total assets of the bank equal $500 million and average Tier I equity

equal $24.5 million. What deposit insurance risk category does the bank fall into? What is

the bank’s deposit insurance assessment rate and the dollar value of deposit insurance

premiums?

31. Two depository institutions have composite CAMELS ratings of 1 or 2 and are “well

capitalized.” Thus, each institution falls into the FDIC Risk Category I deposit insurance

assessment scheme. Further, the institutions have the following financial ratios and

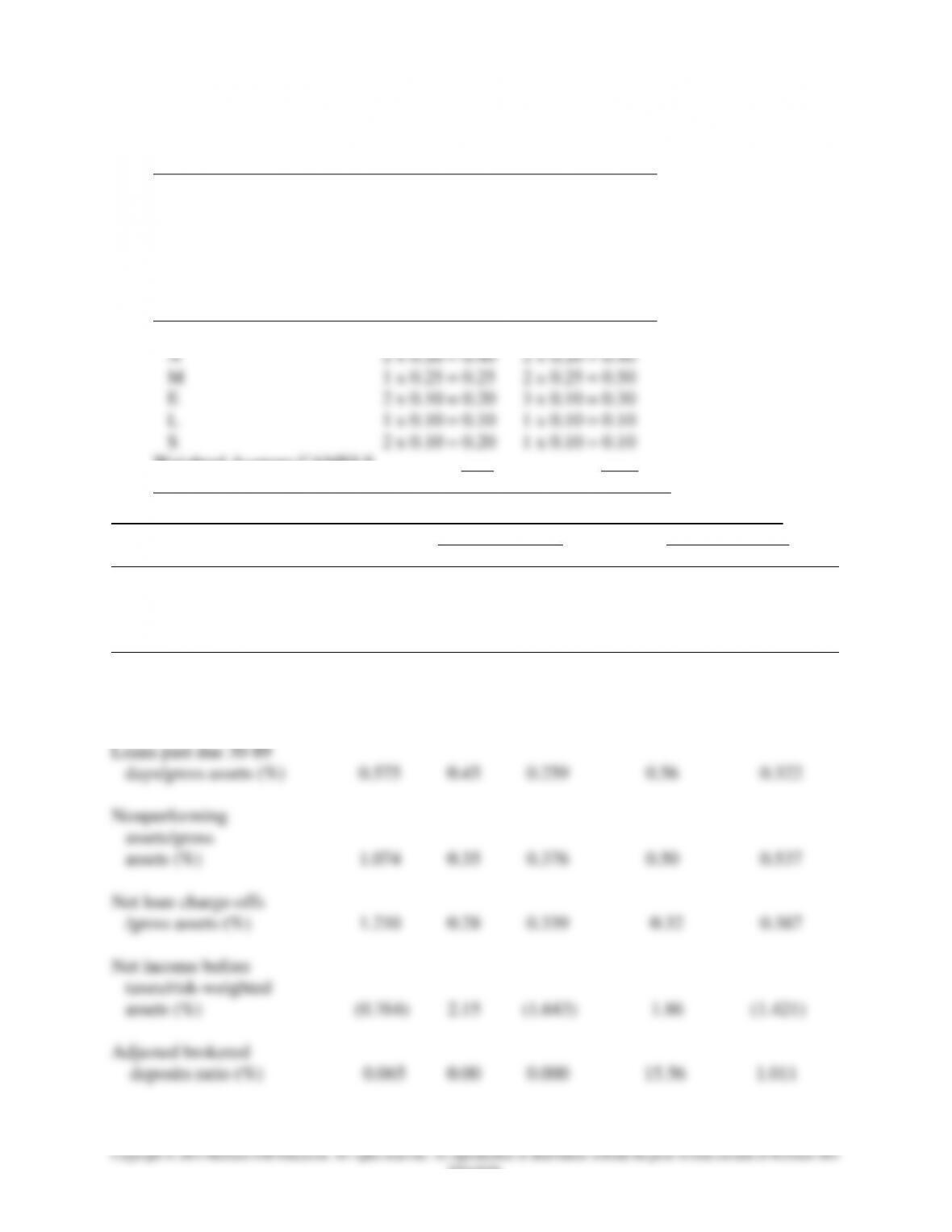

CAMELS ratings:

Institution A Institution B

Tier I leverage ratio (%) 8.62 7.75

Loans past due 30-89

pays/gross assets (%) 0.45 0.56

Nonperforming

assets/gross

assets (%) 0.35 0.50

Net loan charge-offs

/gross assets (%) 0.28 0.32

Net Income before

taxes/risk-weighted

assets (%) 2.15 1.86

Adjusted brokered

deposits ratio (%) 0.00 15.56

CAMELS Components:

C 1 1

A 2 2

M 1 2

E 2 3

L 1 1

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19–16

Education.

S 2 1

Calculate the initial deposit insurance assessment for each institution.

To determine the deposit insurance assessment for each institution, we set up the following

tables:

CAMELS Components:

C 1 x 0.25 = 0.25 1 x 0.25 = 0.25

Weighted Average CAMELS .

Component 1.40 1.65

Base Assessment Rates for Two Institutions

A B C D E F

Institution A Institution B

Contribution Contribution

Risk to Risk to

Pricing Measure Assessment Measure Assessment

Multiplier Value Rate Value Rate

Uniform Amount 4.861 4.861 4.861

Tier I leverage ratio (%) (0.056) 8.62 (0.483) 7.75 (0.434)

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19–17

Education.

32. Two depository institutions have composite CAMELS ratings of 1 or 2 and are “well

capitalized.” Thus, each institution falls into the FDIC Risk Category I deposit insurance

assessment scheme. Institution A has average total assets of $750 million and average Tier

I equity of $75 million. Institution B has average total assets of $1 billion and average Tier

I equity of $110 million. Institution A has no unsecured debt or brokered deposits.

Institution B has no unsecured debt and an asset growth rate over the last four years of 8

percent. Further, the institutions have the following financial ratios and CAMELS ratings:

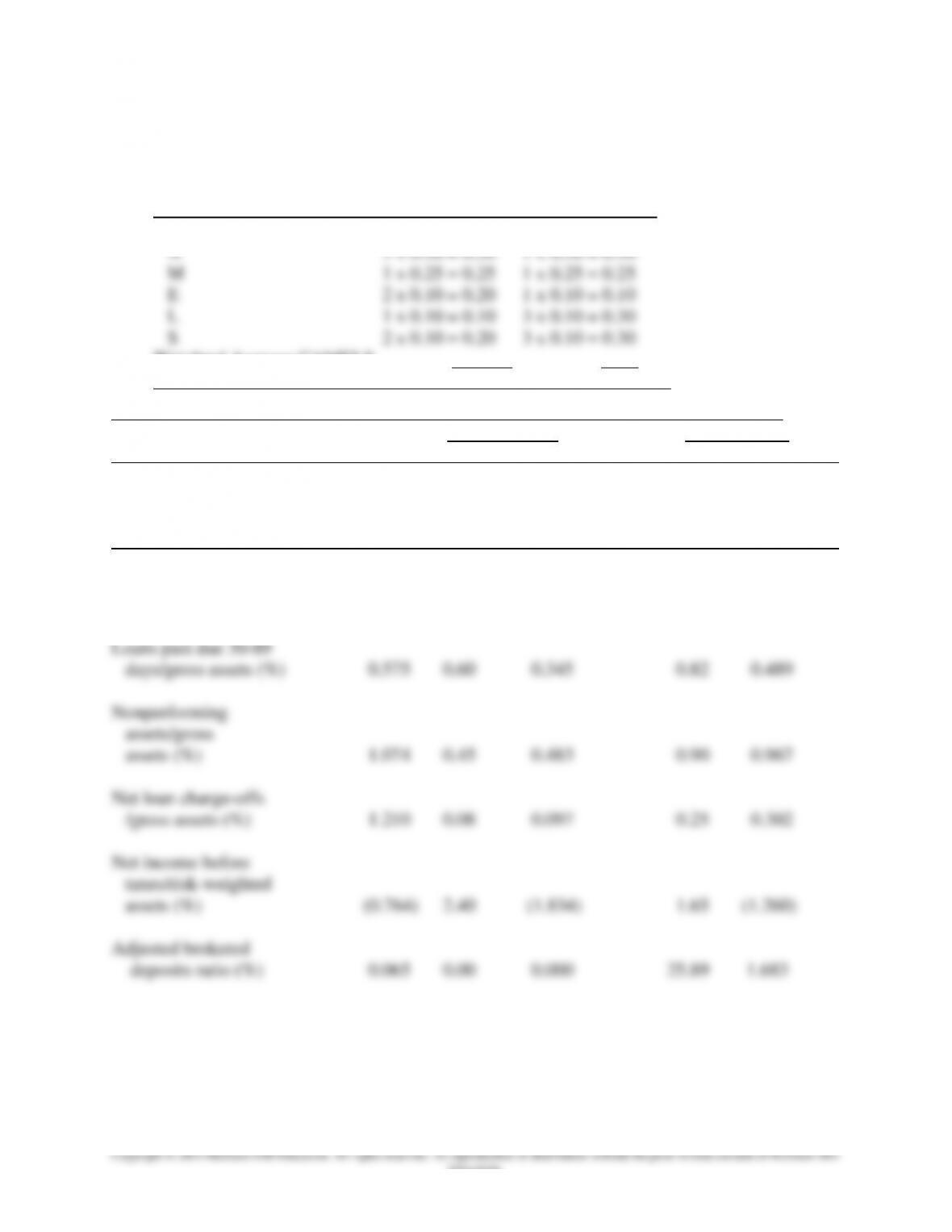

Institution A Institution B

Tier I leverage ratio (%) 10.25 7.00

Loans past due 30-89

days/gross assets (%) 0.60 0.82

Nonperforming

assets/gross

assets (%) 0.45 0.90

Net loan charge-offs

/gross assets (%) 0.08 0.25

Net income before

taxes/risk-weighted

assets (%) 2.40 1.65

Adjusted brokered

deposits ratio (%) 0.00 25.89

CAMELS Components:

C 1 2

A 1 1

M 1 1

E 2 1

L 1 3

S 2 3

Calculate the deposit insurance assessment and the dollar value of the deposit insurance

premium for each institution.

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19–18

Education.

To determine the deposit insurance assessment for each institution, we set up the following

tables:

CAMELS Components:

C 1 x 0.25 = 0.25 2 x 0.25 = 0.50

Weighted Average CAMELS .

Component 1.20 1.65

Base Assessment Rates for Two Institutions

A B C D E F

Institution A Institution B

Contribution Contribution

Risk to Risk to

Pricing Measure Assessment Measure Assessment

Multiplier Value Rate Value Rate

Uniform Amount 4.861 4.861 4.861

Tier I leverage ratio (%) (0.056) 10.25 (0.574) 7.00 (0.392)

Chapter 19 – Deposit Insurance and Other Liability Guarantees

19–19

Weighted average