Chapter 12 – Liquidity Risk

12-1

Solutions for End-of-Chapter Questions and Problems: Chapter Twelve

1. How does the degree of liquidity risk differ for different types of financial institutions?

2. What are the two reasons liquidity risk arises? How does liquidity risk arising from the

liability side of the balance sheet differ from liquidity risk arising from the asset side of the

balance sheet? What is meant by fire-sale prices?

Liquidity risk occurs because of situations that develop from economic and financial transactions

3. What are core deposits? What role do core deposits play in predicting the probability

distribution of net deposit drains?

4. The probability distribution of the net deposit drains of a DI has been estimated to have a

mean of 2 percent and a standard deviation of 1 percent. Is this DI increasing or decreasing

in size? Explain.

Chapter 12 – Liquidity Risk

12-2

5. How is the DI’s distribution pattern of net deposit drains affected by the following?

a. The holiday season.

b. Summer vacations.

c. A severe economic recession.

d. Double-digit inflation.

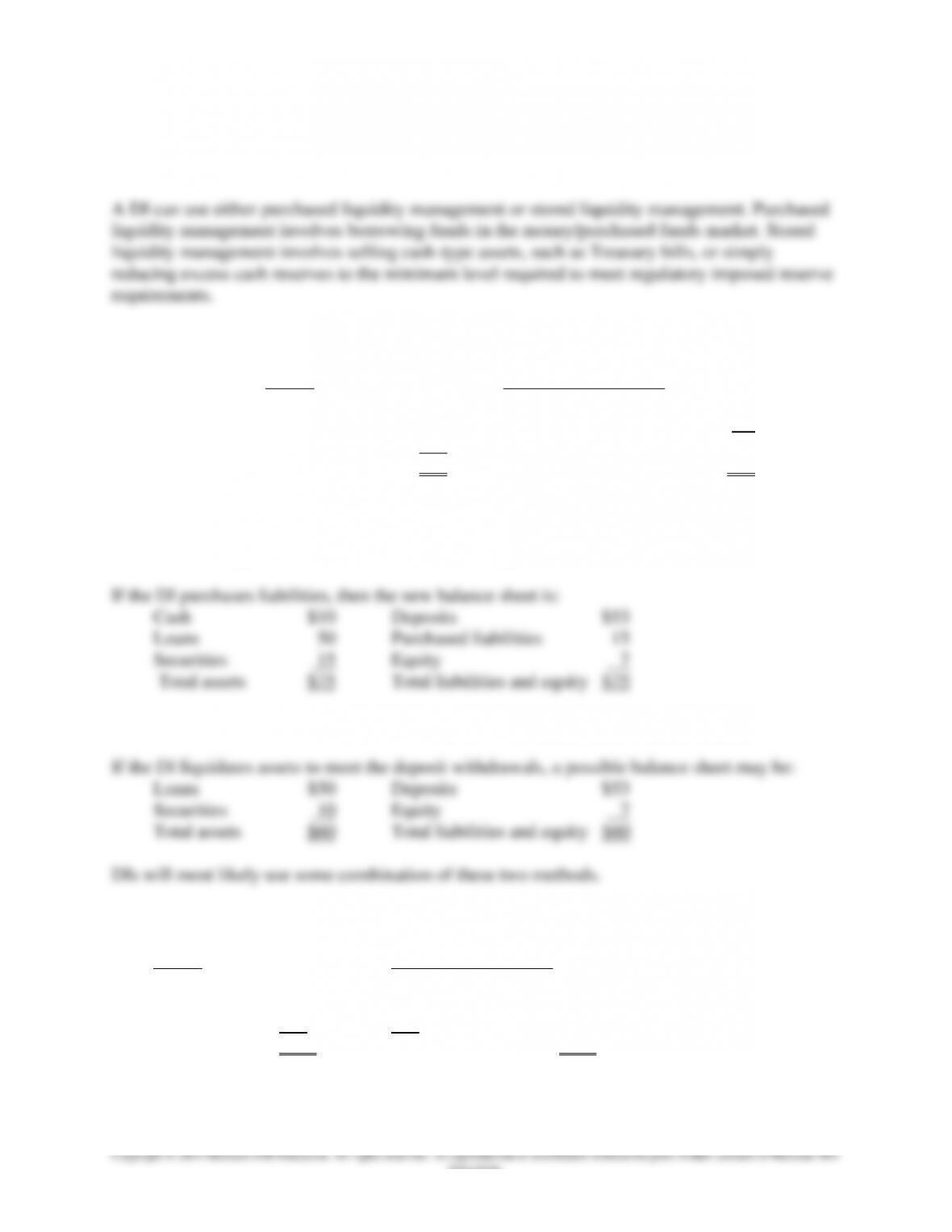

6. What are two ways a DI can offset the liquidity effects of a net deposit drain of funds?

How do the two methods differ? What are the operational benefits and costs of each

method?

Chapter 12 – Liquidity Risk

12-3

Education.

7. What are two ways a DI can offset the effects of asset-side liquidity risk such as the

drawing down of a loan commitment?

8. A DI with the following balance sheet (in millions) expects a net deposit drain of $15

million.

Assets Liabilities and Equity

Cash $10 Deposits $68

Loans 50 Equity 7

Securities 15

Total assets $75 Total liabilities and equity $75

Show the DI’s balance sheet if the following conditions occur:

a. The DI purchases liabilities to offset this expected drain.

b. The stored liquidity management method is used to meet the expected drain.

9. AllStarBank has the following balance sheet (in millions):

Assets Liabilities and Equity

Cash $30 Deposits $110

Loans 90 Borrowed funds 40

Securities 50 Equity 20

Total assets $170 Total liabilities and equity $170

Chapter 12 – Liquidity Risk

12-4

Education.

AllStarBank’s largest customer decides to exercise a $15 million loan commitment. How will the

new balance sheet appear if AllStar uses the following liquidity risk strategies?

a. Stored liquidity management.

b. Purchased liquidity management.

10. A DI has assets of $10 million consisting of $1 million in cash and $9 million in loans. The

DI has core deposits of $6 million, subordinated debt of $2 million, and equity of $2

million. Increases in interest rates are expected to cause a net drain of $2 million in core

deposits over the year?

a. The average cost of deposits is 6 percent and the average yield on loans is 8 percent.

The DI decides to reduce its loan portfolio to offset this expected decline in deposits.

What will be the effect on net interest income and the size of the DI after the

implementation of this strategy?

b. If the interest cost of issuing new short-term debt is expected to be 7.5 percent, what

would be the effect on net interest income of offsetting the expected deposit drain with

an increase in interest-bearing liabilities?

c. What will be the size of the DI after the drain if the DI uses this strategy?

Chapter 12 – Liquidity Risk

12-5

d. What dynamic aspects of DI management would support a strategy of replacing the

deposit drain with interest-bearing liabilities?

11. Define each of the following four measures of liquidity risk. Explain how each measure

would be implemented and utilized by a DI.

a. Sources and uses of liquidity.

b. Peer group ratio comparisons.

c. Liquidity index.

d. Financing gap and financing requirement.

12-6

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

12. A DI has $10 million in T-bills, a $5 million line of credit to borrow in the repo market,

and $5 million in excess cash reserves (above reserve requirements) with the Fed. The DI

currently has borrowed $6 million in fed funds and $2 million from the Fed’s discount

window to meet seasonal demands.

a. What is the DI’s total available (sources of) liquidity?

b. What is the DI’s current total uses of liquidity?

c. What is the net liquidity of the DI?

d. What conclusions can you derive from the result?

13. A DI has the following assets in its portfolio: $10 million in cash reserves with the Fed,

$25 million in T-bills, and $65 million in mortgage loans. If the DI has to liquidate the

assets today, it will receive only $98 per $100 of face value of the T-bills and $90 per $100

of face value of the mortgage loans. Liquidation at the end of one month (closer to

maturity) will produce $100 per $100 of face value of the T-bills and $97 per $100 of face

value of the mortgage. Calculate the one-month liquidity index for this DI using the above

information.

14. A DI has the following assets in its portfolio: $20 million in cash reserves with the Fed,

$20 million in T-bills, and $50 million in mortgage loans. If the assets need to be liquidated

at short notice, the DI will receive only 99 percent of the fair market value of the T-bills

and 90 percent of the fair market value of the mortgage loans. Liquidation at the end of one

month (closer to maturity) will produce $100 per $100 of face value of the T-bills and the

mortgage loans. Calculate the liquidity index using the above information.

Chapter 12 – Liquidity Risk

12-7

Education.

15. Conglomerate Corporation has acquired Acme Corporation. To help finance the takeover,

Conglomerate will liquidate the overfunded portion of Acme’s pension fund. The face

values and current and one-year future liquidation values of the assets that will be

liquidated are given below:

Liquidation Values

Asset Face Value t = 0 t = 1 year

IBM stock $10,000 $9,900 $10,500

GE bonds 5,000 4,000 4,500

Treasury securities 15,000 13,000 14,000

Calculate the one-year liquidity index for these securities.

16. Plainbank has $10 million in cash and equivalents, $30 million in loans, and $15 in core

deposits.

a. Calculate the financing gap.

b. What is the financing requirement?

c. How can the financing gap be used in the day-to-day liquidity management of the

bank?

17. How can an FI’s liquidity plan help reduce the effects of liquidity shortages? What are the

components of a liquidity plan?

A liquidity plan requires forward planning so that an optimal mix of funding can be implemented

to reduce costs and unforeseen withdrawals. In general, a plan could incorporate the following:

Chapter 12 – Liquidity Risk

12-8

Education.

18. Central Bank has the following balance sheet (in millions of dollars).

Liquidity Run-off

Assets level Liabilities and Equity factor

Cash $ 20 Level 1 Stable retail deposits $190 3%

Deposits at the Fed 30 Level 1 Less stable retail deposits 70 10

Treasury bonds 145 Level 1 CDs maturing in 6 months 100 0

Qualifying marketable securities 50 Level 1 Unsecured wholesale funding from:

GNMA bonds 60 Level 2A Stable small business deposits 125 5

Loans to AA- corporations 540 Level 2A Less stable small business deposits 100 10

Mortgages 285 Nonfinancial corporates 450 75

Premises 35 Equity 130

Total $1,165 Total $1,165

Cash inflows over the next 30 days from the bank’s performing assets are $7.5 million.

Calculate the LCR for Central Bank.

The liquidity coverage ratio for Central Bank is calculated as follows:

Level 1 assets = $20 + $30 + $145 + $50 = 245

Level 2 assets = ($60 + $540) x 0.85 = $510.00 Capped at 40% of Level 1 = $245 x 0.40 = 98

Stock of highly liquid assets $343

Chapter 12 – Liquidity Risk

12-9

19. WallsFarther Bank has the following balance sheet (in millions of dollars).

Liquidity Run-off

Assets level Liabilities and Equity factor

Cash $ 12 Level 1 Stable retail deposits $ 55 3%

Deposits at the Fed 19 Level 1 Less stable retail deposits 20 10

Treasury securities 125 Level 1 Unsecured wholesale funding from:

GNMA securities 94 Level 2A Stable small business deposits 80 5

Loans to AA rated corporations 138 Level 2A Less stable small business deposits 49 10

Loans to BB rated corporations 106 Level 2B Nonfinancial corporates 250 75

Premises 20 Equity 60

Total $514 Total $514

Cash inflows over the next 30 days from the bank’s performing assets are $5.5 million.

Calculate the LCR for WallsFarther Bank.

The liquidity coverage ratio for WallsFarther Bank is calculated as follows:

Chapter 12 – Liquidity Risk

12–10

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Total cash inflows over next 30 days 5.50

Total net cash outflows over next 30 days $194.55

Liquidity coverage ratio = $218.4m/$194.55m = 112.26%. The bank is in compliance with

liquidity requirements based on the LCR.

20. FirstBank has the following balance sheet (in millions of dollars).

Required stable Available stable

Funding funding

Assets factor Liabilities and Equity factor

Cash $ 12 0% Stable retail deposits $ 55 90%

Deposits at the Fed 19 5 Less stable retail deposits 20 80

Treasury securities 125 5 Unsecured wholesale funding from:

GNMA securities 94 20 Stable small business deposits 80 90

Loans to A rated corporations 138 65 Less stable small business deposits 49 80

(maturity > 1 year) Nonfinancial corporates 250 50

Loans to B rated corporations 106 50

(maturity < 1 year)

Premises 20 100 Equity 60 100

Total $514 Total $514

Calculate the NSFR for FirstBank.

Chapter 12 – Liquidity Risk

12–11

21. BancTwo has the following balance sheet (in millions of dollars).

Required stable Available stable

funding funding

Assets factor Liabilities and Equity factor

Cash $ 20 0% Stable retail deposits $190 90%

Deposits at the Fed 30 5 Less stable retail deposits 70 80

Treasury bonds 145 5 CDs maturing in 6 months 100 0

Qualifying marketable securities 50 0 Unsecured wholesale funding from:

(maturity < 1 year) Stable small business deposits 125 90

FNMA bonds 60 20 Less stable small business deposits 100 80

Loans to AA- corporations 540 65 Nonfinancial corporates 450 50

(maturity > 1 year) Equity 130 100

Mortgages (unencumbered) 285 65 Total $1,165

Premises 35 100

Total $1,165

Calculate the NSFR for BancTwo.

22. What is a bank run? What are some possible withdrawal shocks that could initiate a bank

run? What feature of the demand deposit contract provides deposit withdrawal momentum

that can result in a bank run?

Chapter 12 – Liquidity Risk

12–12

23. The following is the balance sheet of a DI (in millions):

Assets Liabilities and Equity

Cash $ 2 Demand deposits $50

Loans 50

Premises and equipment 3 Equity 5

Total $55 Total $55

The asset-liability management committee has estimated that the loans, whose average

interest rate is 6 percent and whose average life is three years, will have to be discounted at

10 percent if they are to be sold in less than two days. If they can be sold in 4 days, they

will have to be discounted at 8 percent. If they can be sold later than a week, the DI will

receive the full market value. Loans are not amortized; that is, principal is paid at maturity.

a. What will be the price received by the DI for the loans if they have to be sold in two

days. In four days?

b. In a crisis, if depositors all demand payment on the first day, what amount will they

receive? What will they receive if they demand to be paid within the week? Assume no

deposit insurance.

24. What government safeguards are in place to reduce liquidity risk for DIs?

Chapter 12 – Liquidity Risk

12–13

Education.

25. What are the levels of defense against liquidity risk for a life insurance company? How

does liquidity risk for a property-casualty insurer differ from that for a life insurance

company?

The initial defense against liquidity risk for life insurance companies is the amount of premium

26. How is the liquidity problem faced by investment funds different from that faced by DIs

and insurance companies? How does the liquidity risk of an open-end mutual fund compare

with that of a closed-end fund?

27. A mutual fund has the following assets in its portfolio: $40 million in fixed-income

securities and $40 million in stocks at current market values. In the event of a liquidity

crisis, the fund can sell the assets at a 96 percent of market value if they are disposed of in

two days. The fund will receive 98 percent if the assets are disposed of in four days. Two

shareholders, A and B, own 5 percent and 7 percent of equity (shares), respectively.

a. Market uncertainty has caused shareholders to sell their shares back to the fund. What

will the two shareholders receive if the mutual fund must sell all of the assets in two

days? In four days?

Chapter 12 – Liquidity Risk

12–14

b. How does this situation differ from a bank run? How have bank regulators mitigated

the problem of bank runs?

28. A mutual fund has $1 million in cash and $9 million invested in securities. It currently has 1

million shares outstanding.

a. What is the net asset value (NAV) of this fund?

b. Assume that some of the shareholders decide to cash in their shares of the fund. How

many shares at its current NAV can the fund take back without resorting to a sale of

assets?

c. As a result of anticipated heavy withdrawals, the fund sells 10,000 shares of IBM stock

currently valued at $40. Unfortunately, it receives only $35 per share. What is the net

asset value after the sale? What are the cash assets of the fund after the sale?

Chapter 12 – Liquidity Risk

12–15

d. Assume that after the sale of IBM shares, 100,000 shares are sold back to the fund.

What is the current NAV? Is there a need to sell more securities to meet this

redemption?

Integrated Mini Case: Measuring Liquidity Risk

A DI has the following balance sheet (in millions).

Assets Liabilities and Equity

Cash $9 Deposits $75

Loans 95 Purchased funds 40

Securities 26 Equity 15

Total assets $130 Total liabilities and equity $130

The DI’s securities portfolio includes $16 million in T-bills and $10 million in GNMA securities.

The DI has a $20 million line of credit to borrow in the repo market and $5 million in excess

cash reserves (above reserve requirements) with the Fed. The DI currently has borrowed $22

million in Fed funds and $18 million from the Fed discount window to meet seasonal demands.

1. What is the DI’s total available (sources of) liquidity?

2. What is the DI’s current total uses of liquidity?

3. What is the net liquidity of the DI?

4. Calculate the financing gap.

5. What is the financing requirement?

Chapter 12 – Liquidity Risk

12–16

6. The DI expects a net deposit drain of $20 million. Show the DI’s balance sheet if the

following conditions occur:

a. The DI purchases liabilities to offset this expected drain.

If the DI purchases liabilities, then the new balance sheet is:

b. The stored liquidity management method is used to meet the expected drain (the DI

does not want the cash balance to fall below $5 million, and securities can be sold at

their fair value).

If the DI uses reserve asset adjustment, a possible balance sheet may be:

7. In the event of an unexpected and severe drain on deposits in the next 3 days, and 10

days, the DI will liquidate assets in the following manner:

Liquidation Values ($ millions)

Asset Fair Value t = 3 days t = 10 days

Cash $ 9 $ 9 $ 9

Treasury bills 16 14 15.5

GNMAs 10 8 9

Loans 95 65 75

Calculate the 3-day and 10-day liquidity index for the DI.