Chapter 10 – Credit Risk: Individual Loan Risk

10–15

Education.

b. What is the implied probability of default on A-rated bonds over the next 93 days?

Over 175 days?

c. What is the implied default probability on an 82-day A-rated bond to be issued in 93

days?

33. What is the mortality rate of a bond or loan? What are some of the problems with using a

mortality rate approach to determine the probability of default of a given bond issue?

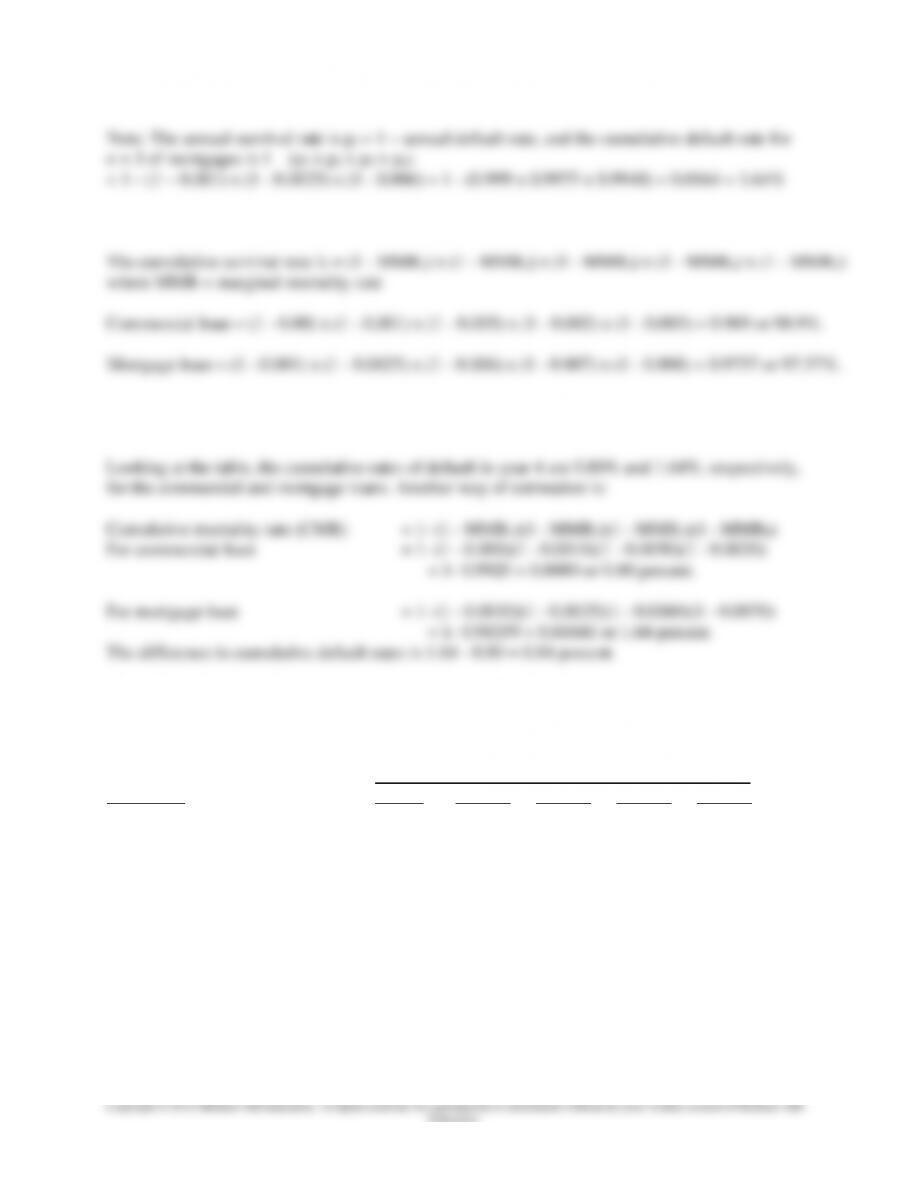

34. The following is a schedule of historical defaults (yearly and cumulative) experienced by

an FI manager on a portfolio of commercial and mortgage loans.

Years after Issuance

Loan Type 1 Year 2 Years 3 Years 4 Years 5 Years

Commercial:

Annual default 0.00% ______ 0.50% ______ 0.30%

Cumulative default ______ 0.10% ______ 0.80% ______

Mortgage:

Annual default 0.10% 0.25% 0.60% ______ 0.80%

Cumulative default ______ ______ ______ 1.64% ______

a. Complete the blank spaces in the table.

Chapter 10 – Credit Risk: Individual Loan Risk

10–16

Education.

b. What are the probabilities that each type of loan will not be in default after 5 years?

c. What is the measured difference between the cumulative default (mortality) rates for

commercial and mortgage loans after four years?

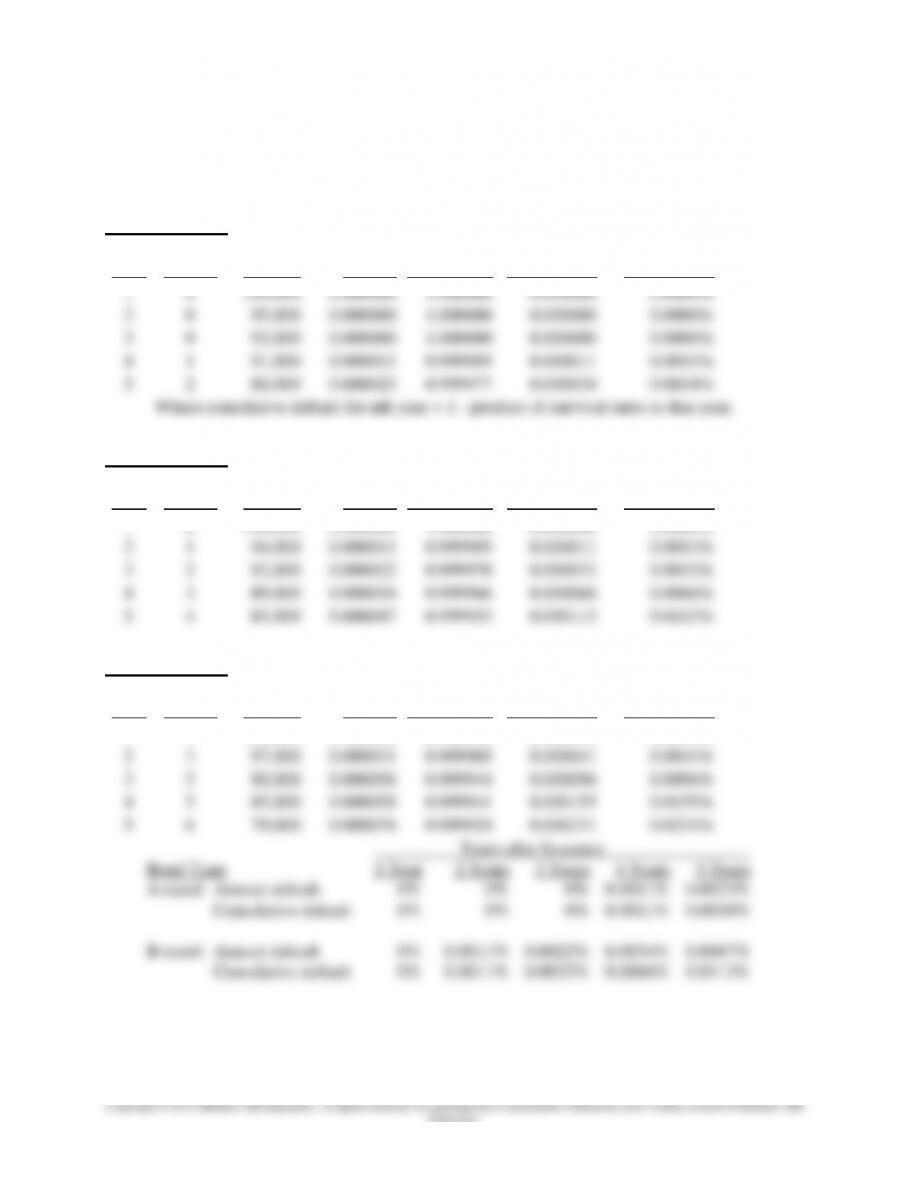

35. The table below shows the dollar amounts of outstanding bonds and corresponding default

amounts for every year over the past five years. Note that the default figures are in

millions, while those outstanding are in billions. The outstanding figures reflect default

amounts and bond redemptions.

Years after Issuance

Loan Type 1 Year 2 Years 3 Years 4 Years 5 Years

A-rated: Annual default (millions) 0 0 0 $ 1 $ 2

Outstanding (billions) $100 $95 $93 $91 $88

B-rated: Annual default (millions) 0 $ 1 $ 2 $ 3 $ 4

Outstanding (billions) $100 $94 $92 $89 $85

Chapter 10 – Credit Risk: Individual Loan Risk

10–17

Education.

C-rated: Annual default (millions) $ 1 $ 3 $ 5 $ 5 $ 6

Outstanding (billions) $100 $97 $90 $85 $79

a. What are the annual and cumulative default rates of the above bonds?

A-rated Bonds

Millions

Millions

Annual

Survival =

Cumulative

% Cumulative

Year

Default

Balance

Default

1 – An. Def.

Default Rate

Default Rate

1

0

100,000

0.000000

1.000000

0.000000

0.0000%

2

0

95,000

0.000000

1.000000

0.000000

0.0000%

3

0

93,000

0.000000

1.000000

0.000000

0.0000%

4

1

91,000

0.000011

0.999989

0.000011

0.0011%

5

2

88,000

0.000023

0.999977

0.000034

0.0034%

Where cumulative default for nth year = 1 – product of survival rates to that year.

B-rated Bonds

Millions

Millions

Annual

Survival =

Cumulative

% Cumulative

Year

Default

Balance

Default

1 – An. Def.

Default Rate

Default Rate

1

0

100,000

0.000000

1.000000

0.000000

0.0000%

2

1

94,000

0.000011

0.999989

0.000011

0.0011%

3

2

92,000

0.000022

0.999978

0.000032

0.0032%

4

3

89,000

0.000034

0.999966

0.000066

0.0066%

5

4

85,000

0.000047

0.999953

0.000113

0.0113%

C-rated Bonds

Millions

Millions

Annual

Survival =

Cumulative

% Cumulative

Year

Default

Balance

Default

1 – An. Def.

Default Rate

Default Rate

1

1

100,000

0.000010

0.999990

0.000010

0.0010%

2

3

97,000

0.000031

0.999969

0.000041

0.0041%

3

5

90,000

0.000056

0.999944

0.000096

0.0096%

4

5

85,000

0.000059

0.999941

0.000155

0.0155%

5

6

79,000

0.000076

0.999924

0.000231

0.0231%

Chapter 10 – Credit Risk: Individual Loan Risk

10–18

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

C-rated: Annual default 0.0010% 0.0031% 0.0056% 0.0059% 0.0076%

Cumulative default 0.0010% 0.0041% 0.0096% 0.0155% 0.0231%

Note: These percentage values seem very small. More reasonable values can be obtained

by increasing the default dollar values by a factor of ten, or by decreasing the outstanding

balance values by a factor of 0.10. Either case will give the same answers that are shown

below. While the percentage numbers seem somewhat more reasonable, the true values of

the problem are (a) that default rates are higher on lower rated assets, and (b) that the

cumulative default rate involves more than the sum of the annual default rates.

C-rated Bonds

Test with 10x default.

Millions

Millions

Annual

Survival =

Cumulative

% Cumulative

Year

Default

Balance

Default

1 – An. Def.

Default Rate

Default Rate

1

10

100,000

0.000100

0.999900

0.000100

0.0100%

2

30

97,000

0.000309

0.999691

0.000409

0.0409%

3

50

90,000

0.000556

0.999444

0.000965

0.0965%

4

50

85,000

0.000588

0.999412

0.001552

0.1552%

5

60

79,000

0.000759

0.999241

0.002311

0.2311%

More meaningful to use 0.10x balance, will get same result.

36. What is RAROC? How does this model use the concept of duration to measure the risk

exposure of a loan? How is the expected change in the credit risk premium measured?

What precisely is LN in the RAROC equation?

Chapter 10 – Credit Risk: Individual Loan Risk

10–19

Education.

37. An FI wants to evaluate the credit risk of a $5 million loan with a duration of 4.3 years to a

AAA borrower. There are currently 500 publicly traded bonds in that class (i.e., bonds

issued by firms with a AAA rating). The current average level of rates (R) on AAA bonds

is 8 percent. The largest increase in credit risk premiums on AAA loans, the 99 percent

worst-case scenario, over the last year was equal to 1.2 percent (i.e., only 6 bonds out of

500 had risk premium increases exceeding the 99 percent worst case). The projected (one-

year) spread on the loan is 0.3 percent and the FI charges 0.25 percent of the face value of

the loan in fees. Calculate the capital at risk and the RAROC on this loan.

The estimate of loan (or capital) risk is:

38. A bank is planning to make a loan of $5,000,000 to a firm in the steel industry. It expects to

charge a servicing fee of 50 basis points. The loan has a maturity of 8 years with a duration

of 7.5 years. The cost of funds (the RAROC benchmark) for the bank is 10 percent. The

bank has estimated the maximum change in the risk premium on the steel manufacturing

sector to be approximately 4.2 percent, based on two years of historical data. The current

market interest rate for loans in this sector is 12 percent.

a. Using the RAROC model, determine whether the bank should make the loan?

Chapter 10 – Credit Risk: Individual Loan Risk

10–20

Education.

b. What should be the duration in order for this loan to be approved?

c. Assuming that duration cannot be changed, how much additional interest and fee

income will be necessary to make the loan acceptable?

d. Given the proposed income stream and the negotiated duration, what adjustment in the

loan rate would be necessary to make the loan acceptable?

39. Calculate the value of and interest rate on a loan using the option model and the following

information.

Face value of loan (B) = $500,000

Length of time remaining to loan maturity (τ) = 4 years

Risk-free rate (i) = 4%

Borrower’s leverage ratio (d) = 60%

Standard deviation of the rate of change in the value of the underlying assets = 15%

Chapter 10 – Credit Risk: Individual Loan Risk

10–21

Substituting these values into the equations for h1 and h2 and solving for the areas under the

standardized normal distribution, we find that:

40. A firm is issuing a two-year loan in the amount of $200,000. The current market value of

the borrower’s assets is $300,000. The risk-free rate is 4 percent and the standard deviation

of the rate of change in the underlying assets of the borrower is 20 percent. Using an

options framework, determine the following:

a. The current market value of the loan.

b. The risk premium to be charged on the loan.

Chapter 10 – Credit Risk: Individual Loan Risk

10–22

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

The risk premium, ϕ = k(τ) – i = (-1/τ) ln[N(h2) + (1/d)N(h1)]

= (-½)ln[0.94265 + 1.62493 x 0.031654] = 0.002966 = 0.2966%

41. A firm has assets of $200,000 and total debts of $175,000. With an option pricing model,

the implied volatility of the value of the firm’s assets is estimated at $10,730. Under the

Moody’s Analytics method, what is the expected default frequency (assuming a normal

distribution for assets)?

42. Carman County Bank (CCB) has a $5 million face value outstanding adjustable-rate loan to

a company that has a leverage ratio of 80 percent. The current risk-free rate is 6 percent and

the time to maturity on the loan is exactly ½ year. The asset risk of the borrower, as

measured by the standard deviation of the rate of change in the value of the underlying

assets, is 12 percent. The normal density function values are given below.

h N(h) h N(h)

-2.55 0.0054 2.50 0.9938

-2.60 0.0047 2.55 0.9946

-2.65 0.0040 2.60 0.9953

-2.70 0.0035 2.65 0.9960

-2.75 0.0030 2.70 0.9965

a. Use the Merton option valuation model to determine the market value of the loan.

b. What should be the interest rate for the last six months of the loan?

Chapter 10 – Credit Risk: Individual Loan Risk

10–23

Education.

43. Suppose you are a loan officer at Carbondale Local Bank. Joan Doe listed the following

information on her mortgage application.

Characteristic Value

Chapter 10 – Credit Risk: Individual Loan Risk

10–24

Use the information below to determine whether or not Joan Doe should be approved for a mortgage from your bank.

Characteristic Characteristic Values and Weights

Annual gross <$10,000 $10,000-$25,000 $25,000-$50,000 $50,000-$100,000 >$100,000

income

Score 0 10 20 35 60

TDS >50% 35%-50% 15%-35% 5%-15% <5%

Score -10 0 20 40 60

Relations None Checking account Savings account Both

Chapter 10 – Credit Risk: Individual Loan Risk

10–25

Jane Doe=s credit score is calculated as follows:

44. What are some of the special risks and considerations when lending to small businesses

rather than large businesses?

45. How does ratio analysis help to answer questions about the production, management, and

marketing capabilities of a prospective borrower?

Although financial ratios are normally thought to represent financial health, they also

Chapter 10 – Credit Risk: Individual Loan Risk

10–26

Education.

46. Consider the following company balance sheet and income statement.

Balance Sheet:

Assets Liabilities and Equity

Cash $4,000 Accounts payable $30,000

Accounts receivable 52,000 Notes payable 12,000

Inventory 40,000 Total current liabilities 42,000

Total current assets 96,000 Long-term debt 36,000

Fixed assets 44,000 Equity 62,000

Total assets $140,000 Total liabilities and equity $140,000

Income Statement

Sales (all on credit) $200,000

Cost of goods sold 130,000

Gross margin 70,000

Selling and administrative expenses 20,000

Depreciation 8,000

EBIT 42,000

Interest expense 4,800

Earning before tax 37,200

Taxes 11,160

Net income $26,040

For this company, calculate the following:

a. Current ratio.

96,000/42,000 = 2.2857X

47. Industrial Corporation has an income-to-sales (profit margin) ratio of 0.03, a sales to assets

(asset utilization) ratio of 1.5, and a debt to asset ratio of 0.66. What is Industrial’s return

on equity?

Chapter 10 – Credit Risk: Individual Loan Risk

10–27

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ROE = NI/Equity = NI/Sales x Sales/Total assets x Total assets/Equity = PM AU EM

= 0.03 x 1.5 x (1/(1 – 0.66)) = 0.1324 = 13.24%

Answer to Integrated Mini Case: Loan Analysis

Loan:

1. PD = -0.08(2.15) + 0.15(0.45) + 1.25(0.13) – 0.45(0.12) = 0.004 = 0.4% < 0.5% => accept the loan