Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

CHAPTER 07

7-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

CAPITAL ASSET PRICING AND ARBITRAGE PRICING THEORY

1. The required rate of return on a stock is related to the required rate of return on the stock market

via beta. Assuming the beta of Google remains constant, the increase in the risk of the market

2. An example of this scenario would be an investment in the SMB and HML. As of yet, there are

no vehicles (index funds or ETFs) to directly invest in SMB and HML. While they may prove

3. a. False. According to CAPM, when beta is zero, the “excess” return should be zero.

b. False. CAPM implies that the investor will only require risk premium for systematic risk.

c. False. We can construct a portfolio with the beta of .75 by investing .75 of the investment

4. E(r) = rf + β [E(rM) – rf ] , rf = 4%, rM = 6%

5. $1 Discount Store is overpriced; Everything $5 is underpriced.

6. a. 15%. Its expected return is exactly the same as the market return when beta is 1.0.

7. Statement a is most accurate.

Statement c is incorrect. Lower beta means the stock carries less systematic risk.

8. The APT may exist without the CAPM, but not the other way. Thus, statement a is possible, but

9. E(rp) = rf + β [E(rM) – rf ] Given rf = 5% and E(rM)= 15%, we can calculate

10. If the beta of the security doubles, then so will its risk premium. The current risk premium for

7-2

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

11. The cash flows for the project comprise a 10-year annuity of $10 million per year plus an

additional payment in the tenth year of $10 million (so that the total payment in the tenth year is

$20 million). The appropriate discount rate for the project is:

rf + β [E(rM) – rf ] = 9% + 1.7 (19% – 9%) = 26%

Using this discount rate:

1.

a. The beta is the sensitivity of the stock’s return to the market return, or, the change in the

stock return per unit change in the market return. We denote the aggressive stock A and

the defensive stock D, and then compute each stock’s beta by calculating the difference

in its return across the two scenarios divided by the difference in market return.

2 - 32

5 - 20

D =

3.5 - 14

5 - 20

= 0.70

a. With the two scenarios equally likely, the expected rate of return is an average of the

two possible outcomes:

b. The SML is determined by the following: Expected return is the T-bill rate = 8% when

beta equals zero; beta for the market is 1.0; and the expected rate of return for the market

is:

7-3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

Thus, we graph the SML as following:

E(r)

8%

12.5%

1.0

2.0

A

SML

M

.7

D

D

a. The aggressive stock has a fair expected rate of return of:

E(rA) = 8% + 2.0 (12.5% – 8%) = 17%

b. The hurdle rate is determined by the project beta (i.e., 0.7), not by the firm’s beta.

The correct discount rate is therefore 11.15%, the fair rate of return on stock D.

2. Not possible. Portfolio A has a higher beta than Portfolio B, but the expected return for

Portfolio A is lower.

3. Possible. If the CAPM is valid, the expected rate of return compensates only for systematic

4. Not possible. The reward-to-variability ratio for Portfolio A is better than that of the market,

which is not possible according to the CAPM, since the CAPM predicts that the market portfolio

is the most efficient portfolio. Using the numbers supplied:

7-4

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

As a first pass, we note that large standard deviation of the beta estimates. None of the

subperiod estimates deviate from the overall period estimate by more than two standard

deviations. That is, the t-statistic of the deviation from the overall period is not significant

for any of the subperiod beta estimates. Looking beyond the aforementioned observation,

the differences can be attributed to different alpha values during the subperiods. The case of

6. Since the stock’s beta is equal to 1.0, its expected rate of return should be equal to that of the

market, that is, 18%.

E(r) =

0

01

P

PPD

100

100P9

1

7. If beta is zero, the cash flow should be discounted at the risk-free rate, 8%:

PV = $1,000/0.08 = $12,500

8. Using the SML: 6% = 8% + β(18% – 8%) β= –2/10 = –0.2

9. We denote the first investment advisor 1, who has r1 = 19% and 1 = 1.5, and the second

a. Without information about the parameters of this equation (i.e., the risk-free rate and

b. If rf = 6% and rM = 14%, then (using alpha for the abnormal return):

7-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

c. If rf = 3% and rM = 15%, then:

10.

a. Since the market portfolio, by definition, has a beta of 1.0, its expected rate of return

is 12%.

b. β= 0 means the stock has no systematic risk. Hence, the portfolio’s expected rate of

c. Using the SML, the fair rate of return for a stock with β = –0.5 is:

The expected rate of return, using the expected price and dividend for next year:

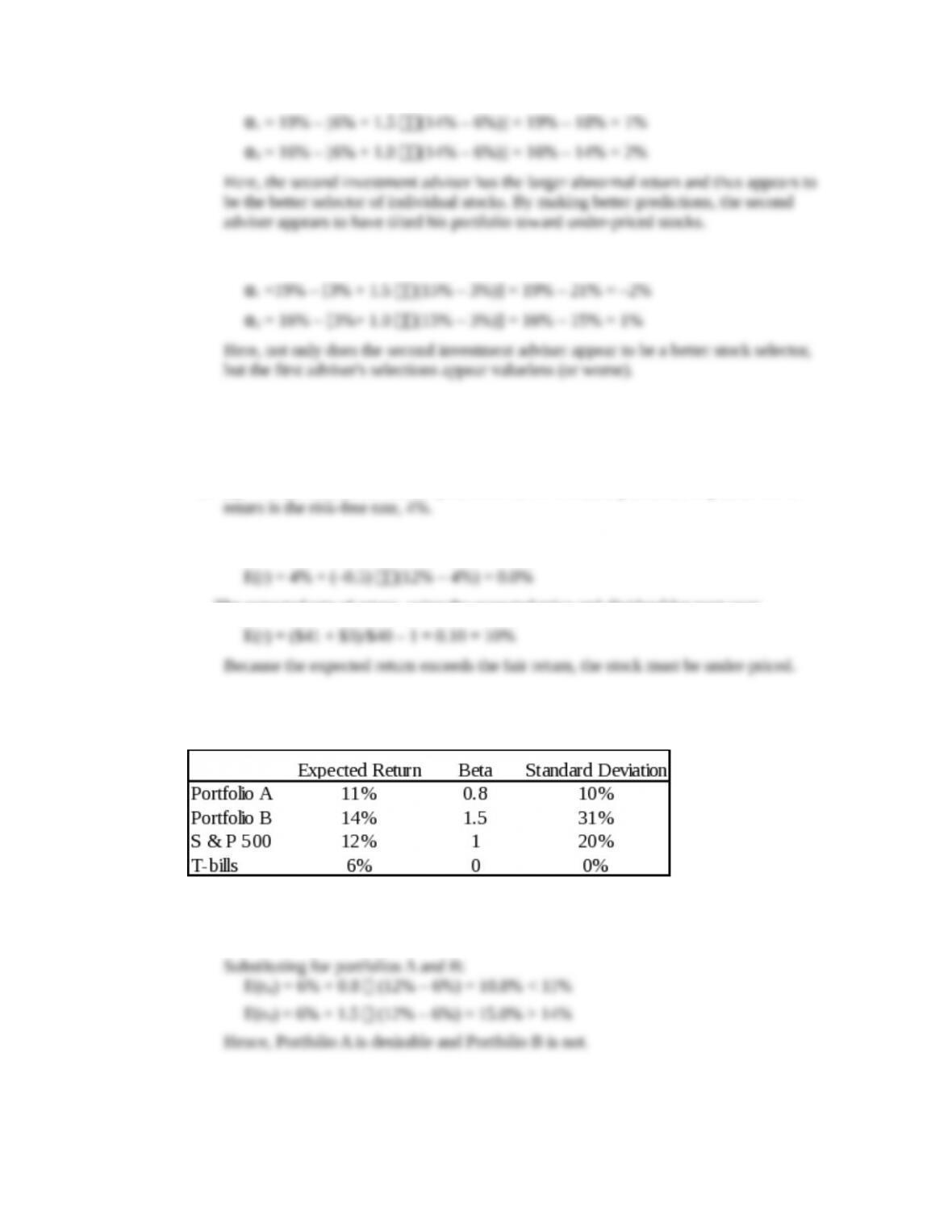

11. The data can be summarized as follows:

a. Using the SML, the expected rate of return for any portfolio P is:

E(rP) = rf + [E(rM) –rf ]

b. The slope of the CAL supported by a portfolio P is given by:

7-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

S =

E( rP ) - r f

P

Computing this slope for each of the three alternative portfolios, we have:

12. Since the beta for Portfolio F is zero, the expected return for Portfolio F equals the risk-free

rate.

For Portfolio A, the ratio of risk premium to beta is: (10 4)/1 = 6

The ratio for Portfolio E is higher: (9 4)/(2/3) = 7.5

Portfolio Weight In Asset Contribution to β

Contribution to Excess

Return

-1 Portfolio A -1 x βA = -1.0 -1.0 x (10%- 4%) = -6%

1.5 Portfolio E 1.5 x βE = 1.0 1.5 x (9% – 4%) = 7.5%

-0.5 Portfolio F -0.5 x 0 = 0 0

Investment = 0 βArbitrage = 0 α = 1.5%

13. Substituting the portfolio returns and betas in the mean-beta relationship, we obtain two equations

in the unknowns, the risk-free rate (rf) and the factor return (F):

14.

7-8

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

a. Shorting equal amounts of the 10 negative-alpha stocks and investing the proceeds equally

in the 10 positive-alpha stocks eliminates the market exposure and creates a zero-investment

portfolio. Using equation 7.5 and denoting the market factor as RM, the expected dollar

return is [noting that the expectation of residual risk (e) in equation 7.8 is zero]:

b. If n = 50 stocks (i.e., 25 long and 25 short), $40,000 is placed in each position, and the

variance of dollar returns is:

5

15. Any pattern of returns can be “explained” if we are free to choose an indefinitely large number

16. The APT factors must correlate with major sources of uncertainty, i.e., sources of uncertainty

that are of concern to many investors. Researchers should investigate factors that correlate with

17. The revised estimate of the expected rate of return of the stock would be the old estimate plus

the sum of the unexpected changes in the factors times the sensitivity coefficients, as follows:

7-9

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

18. Equation 7.11 applies here:

E(rP) = rf + P1 [E(r1) rf] + P2 [E(r2) – rf]

19. The first two factors (the return on a broad-based index and the level of interest rates) are most

promising with respect to the likely impact on Jennifer’s firm’s cost of capital. These are both

macro factors (as opposed to firm-specific factors) that cannot be diversified away;

20. Since the risk free rate is not given, we assume a risk free rate of 0%. The APT required (i.e.,

equilibrium) rate of return on the stock based on rf and the factor betas is:

CFA 1

Answer:

a, c, and d are true; b is incorrect because the SML doesn’t require all investors to invest in the

market portfolio but provides a benchmark to evaluate investment performance for both

portfolios and individual assets.

Answer:

b.

i. For an investor who wants to add this stock to a well-diversified equity

7-10

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

ii. For an investor who wants to hold this stock as a single-stock portfolio, Kay

should recommend Stock Y, because it has higher forecasted return and lower

standard deviation than Stock X. Stock Y’s Sharpe ratio is:

However, given the choice between Stock X and Y, Y is superior. When a stock is

held in isolation, standard deviation is the relevant risk measure. For assets held in

Answer:

a. McKay should borrow funds and invest those funds proportionally in

Murray’s existing portfolio (i.e., buy more risky assets on margin). In

b. McKay should substitute low beta stocks for high beta stocks in order

to reduce the overall beta of York’s portfolio. By reducing the overall

portfolio beta, McKay will reduce the systematic risk of the portfolio

and therefore the portfolio’s volatility relative to the market. The

CFA 4

Answer:

a. “Both the CAPM and APT require a mean-variance efficient market portfolio.” This

7-11

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

b. “The CAPM assumes that one specific factor explains security returns but APT does

CFA 5

Answer:

CFA 6

Answer:

d. They expect return on the market, rM:

CFA 7

Answer:

CFA 8

Answer:

d. Insufficient data given. We need to know the risk-free rate.

CFA 9

Answer:

Under the CAPM, the only risk that investors are compensated for bearing is the risk that

cannot be diversified away (i.e., systematic risk). Because systematic risk (measured by beta) is

CFA 10

Answer:

b. Offer an arbitrage opportunity:

rf = 8% and E(rM) = 16%

Answer:

c. Positive alpha investment opportunities will quickly disappear, because once such

Answer:

CFA 13

Answer:

c. Investors will take on as large a position as possible only if the mispricing opportunity

7-12

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 07 – Capital Asset Pricing and Arbitrage Pricing Theory

d. APT does not require the restrictive assumptions concerning the market portfolio. It

.

7-13

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.