Chapter 06 – Efficient Diversification

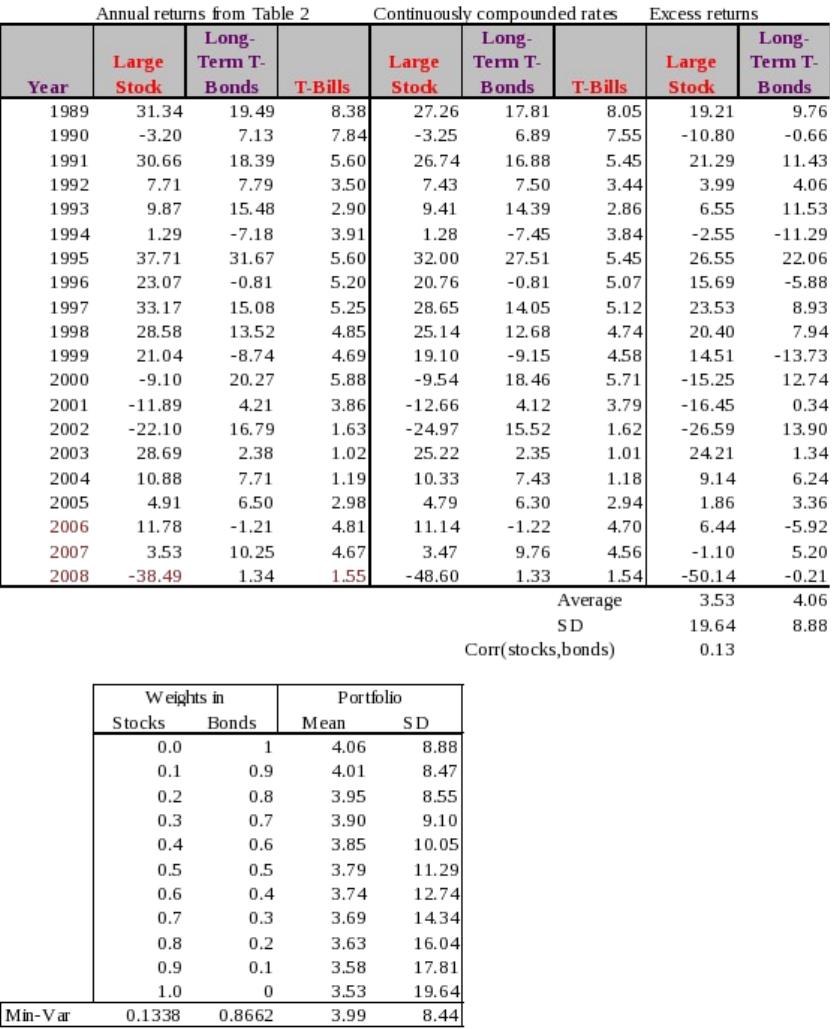

The bond portfolio is less risky as represented by its lower standard deviation. Yet, as the

portfolio table shows, mixing .87% of bonds with 13% stocks would have produced a portfolio

less risky than bonds. In this sample of these 20 years, the average return on the less risky

portfolio of bonds was higher than that of the riskier portfolio of stocks. This is exactly what is

meant by “risk.” Expectation will not always be realized.

6-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 06 – Efficient Diversification

1. If the lending and borrowing rates are equal and there are no other constraints on portfolio

choice, then the optimal risky portfolios of all investors will be identical. However, if the

2. No, it is not possible to get such a diagram. Even if the correlation between A and B were 1.0,

3. In the special case that all assets are perfectly positively correlated, the portfolio standard

deviation is equal to the weighted average of the component-asset standard deviations.

4. The probability distribution is:

Probability Rate of Return

.7 100%

.3 -50%

= 0.6874 or 68.74%

5. The expected rate of return on the stock will change by beta times the unanticipated change in

the market return: 1.2 ( .08 – .10) = –2.4%

6.

a. The risk of the diversified portfolio consists primarily of systematic risk. Beta measures

systematic risk, which is the slope of the security characteristic line (SCL). The two figures

b. The undiversified investor is exposed primarily to firm-specific risk. Stock A has

higher firm-specific risk because the deviations of the observations from the SCL are

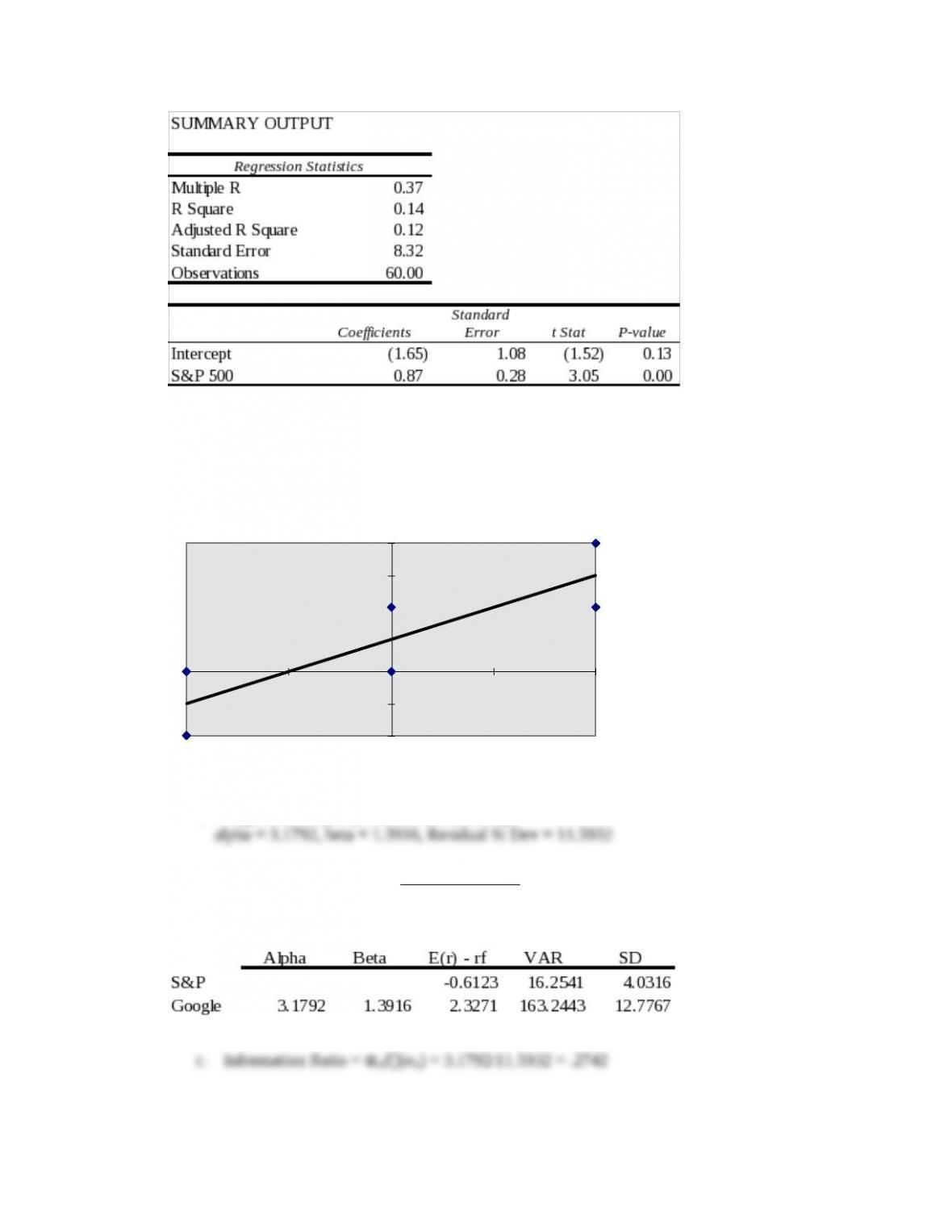

7.Using “Regression” command from Excel’s Data Analysis menu, we can run a regression of

GM’s excess returns against those of S&P 500, and obtain the following data. The Beta of GM

is .87.

6-2

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 06 – Efficient Diversification

8. A scatter plot results in the following diagram. The slope of the regression line is 2.0 and

intercept is 1.0.

y = 1.0 + 2.0 x

-2

-1

0

1

2

3

4

-1 -0.5 0 0.5 1

Market Return, Percent

Generic

Return,

Percent

9.

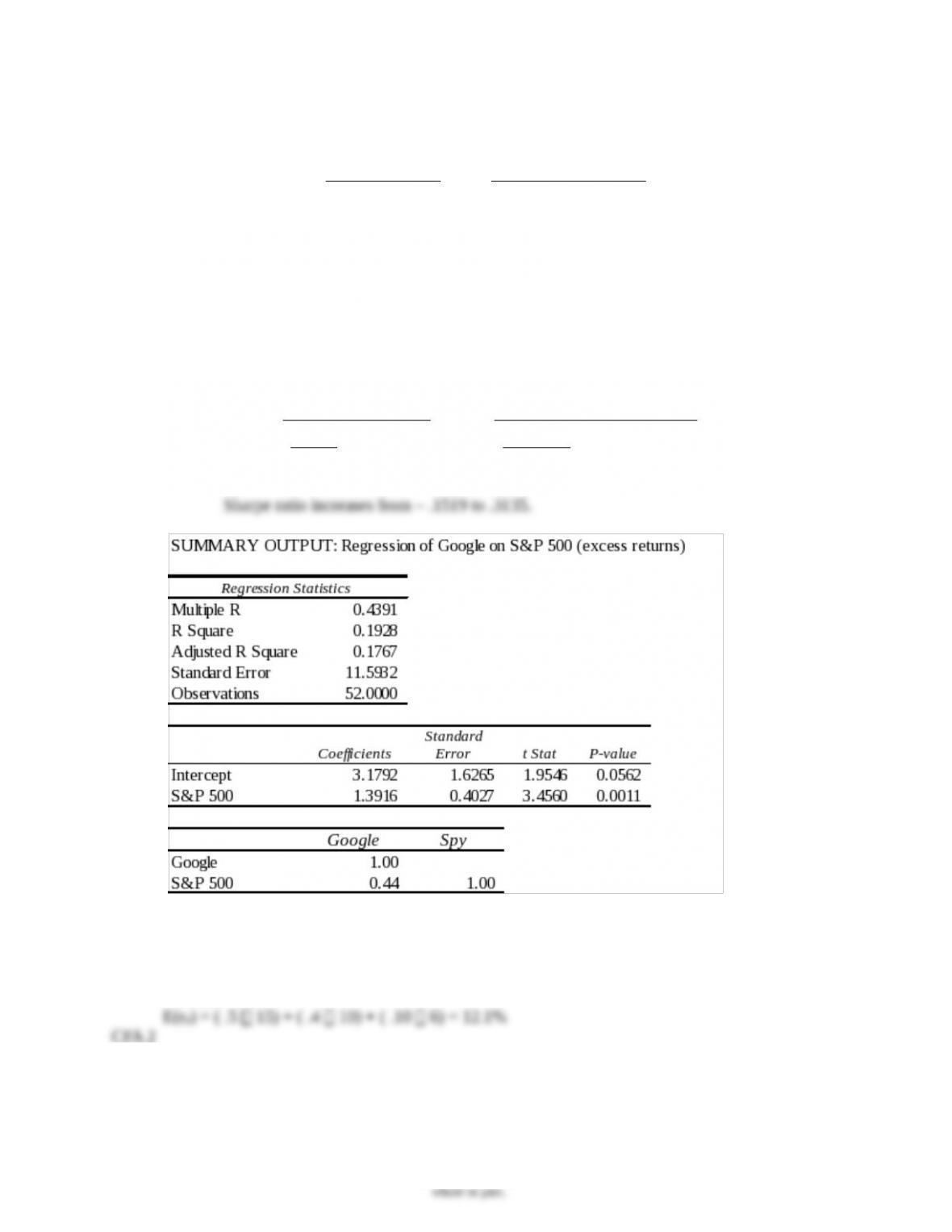

a. Regression output produces the following:

b. Sharpe Ratio of S&P =

E( rS&P) - r f

S &P

= – .6123/4.0316 = – .1519

6-3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 06 – Efficient Diversification

d. We use Equation 6.16 to compute

wG

O

wG

O

=

α G / 2 (e G )

R S&P / 2 S&P

=

3.1792/ (11 .59 32 2)

– .6123/(4.0316 2 )

= –62.79%

wG

O

e. SO =

√

(

αG

(e G )

)

2

+ ( SM )2

=

√

(

3.1 792

1 1. 5932

)

2

+ (– .1519 )2

= .3135

CFA 1

Answer:

CFA 2

Answer:

Fund D represents the single best addition to complement Stephenson’s current portfolio, given

his selection criteria. First, Fund D’s expected return (14.0 percent) has the potential to increase

6-4

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 06 – Efficient Diversification

The other three funds have shortcomings in terms of either expected return enhancement or

volatility reduction through diversification benefits. Fund A offers the potential for increasing

the portfolio’s return, but is too highly correlated to provide substantial volatility reduction

CFA 3

Answer:

a. Subscript OP refers to the original portfolio, ABC to the new stock, and NP to the

new portfolio.

i. E(rNP) = wOP E(rOP ) + wABC E(rABC ) = ( .9 .67) + ( .1 1.25) = .7280%

b. Subscript OP refers to the original portfolio, GS to government securities, and NP to the

new portfolio.

i. E(rNP) = wOP E(rOP ) + wGS E(rGS ) = ( .9 .67) + ( .1 .42) = .6450%

c. Adding the risk-free government securities would result in a lower beta for the new

d. The comment is not correct. Although the respective standard deviations and expected

returns for the two securities under consideration are identical, the identical coefficients

between each security and the original portfolio are unknown, making it impossible to

6-5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 06 – Efficient Diversification

e. Grace clearly expressed the sentiment that the risk of loss was more important to her than

the opportunity for return. Using variance (or standard deviation) as a measure of risk in

CFA 4

Answer:

a. Restricting the portfolio to 20 stocks, rather than 40 to 50, will very likely increase the

b. Hennessy could contain the increase in risk by making sure that he maintains

reasonable diversification among the 20 stocks that remain in his portfolio. This entails

Answer:

Risk reduction benefits from diversification are not a linear function of the number of issues in

CFA 6

Answer:

The point is well taken because the committee should be concerned with the volatility of the

CFA 7

Answer:

a. Systematic risk refers to fluctuations in asset prices caused by macroeconomic factors

that are common to all risky assets; hence systematic risk is often referred to as market

b. Trudy should explain to the client that picking only the five best ideas would most

likely result in the client holding a much more risky portfolio. The total risk of a

portfolio, or portfolio variance, is the combination of systematic risk and firm-specific

risk.

6-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 06 – Efficient Diversification

6-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.