Chapter 21 – Taxes, Inflation, and Investment Strategy

CHAPTER 21

21-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 21 – Taxes, Inflation, and Investment Strategy

TAXES, INFLATION, AND INVESTMENT STRATEGY

1. Moral hazard. The owner now has an incentive to cause a loss and file a claim.

2. The owner will suffer from adverse selection. The owner will attract cargo that

3. Passive investors who are not sophisticated and looking for reduced fees. These

4. The social security annuity is paid out for the balance of your life, regardless of

how long you live. The amount is determined based on the calculation of a

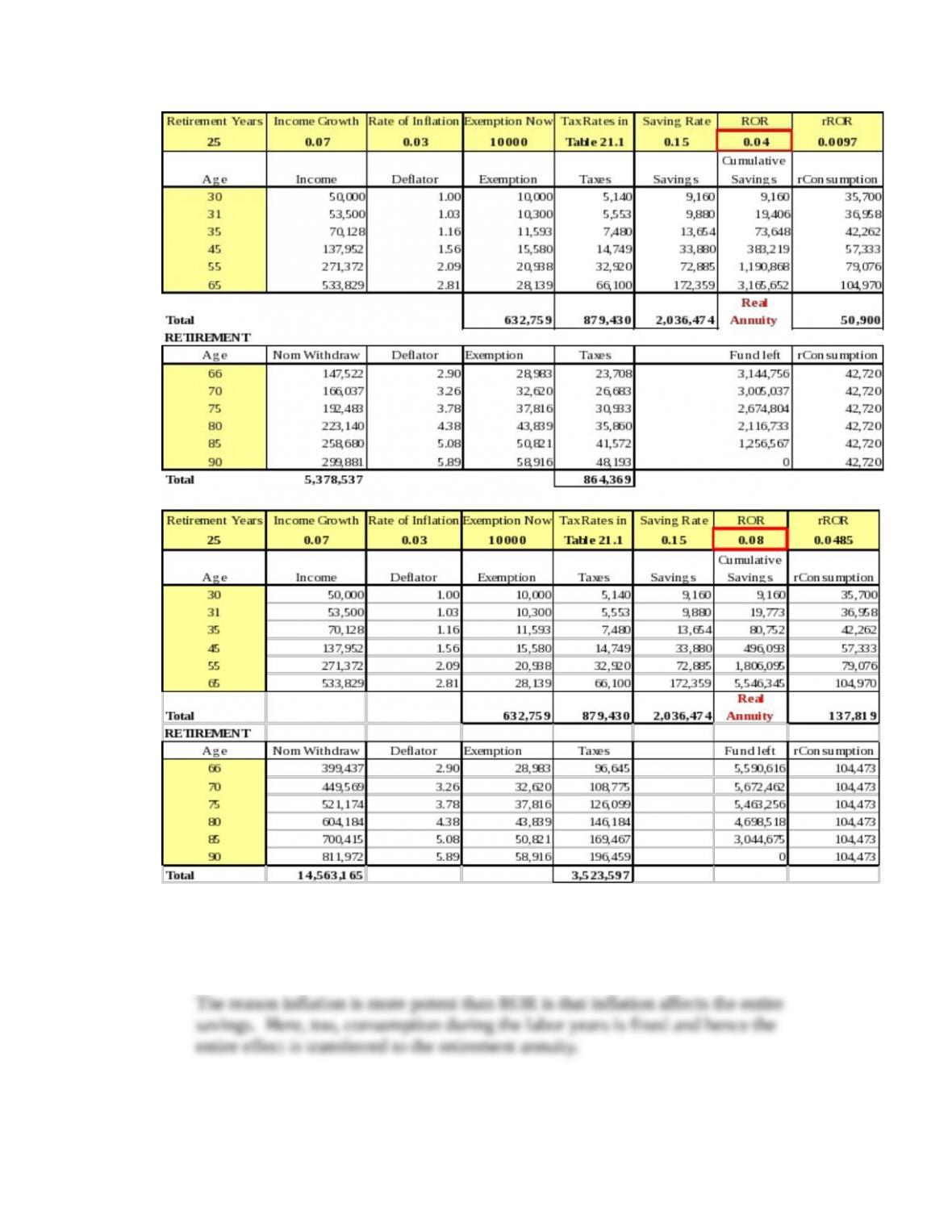

5. The progressive tax code sharpens the importance of taxes during the retirement

years. High tax rates during retirement reduce the effectiveness of a tax shelter. In

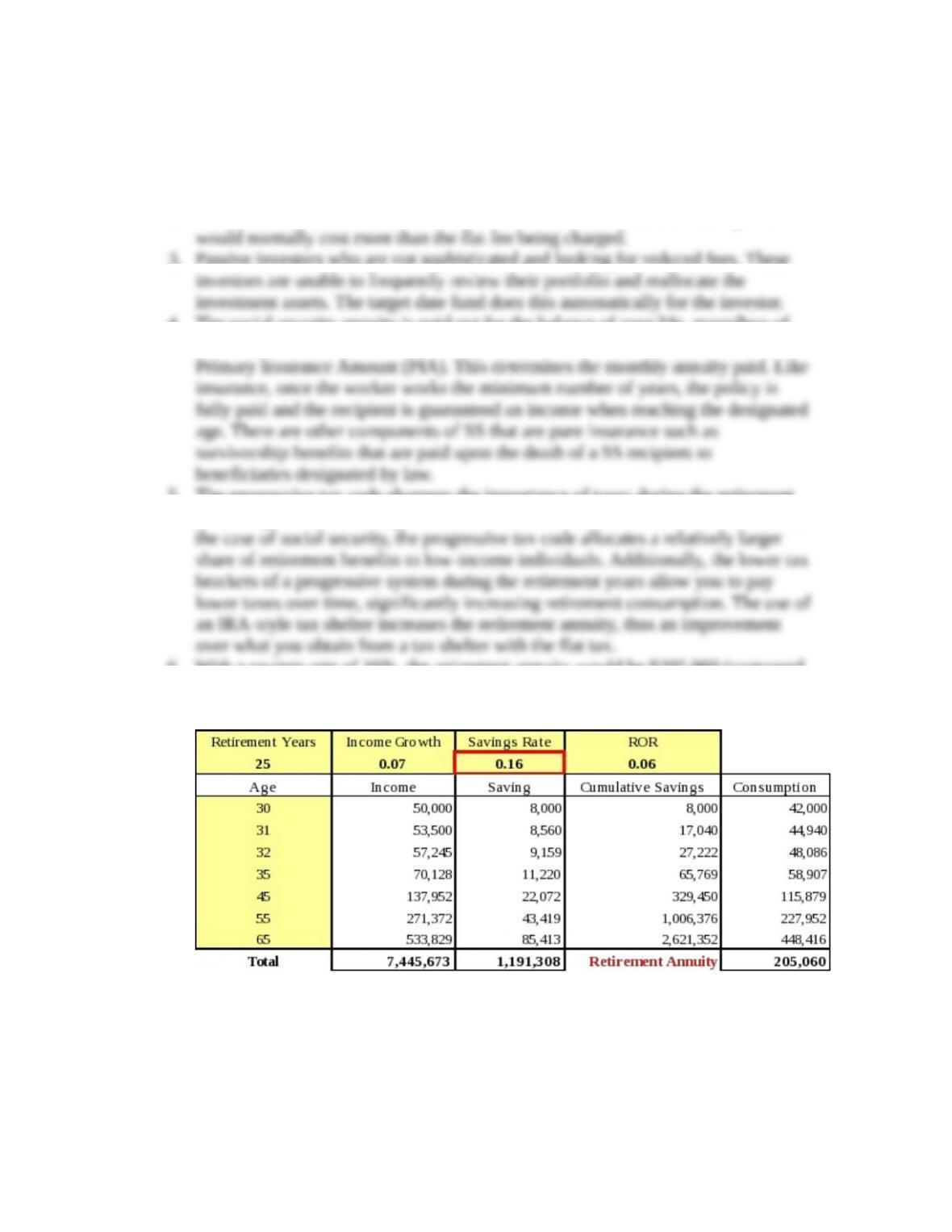

6. With a savings rate of 16%, the retirement annuity would be $205,060 (compared

to $192,244 with the 15% savings rate).

Spreadsheet 21.1: Adjusted for Change in Savings Rate

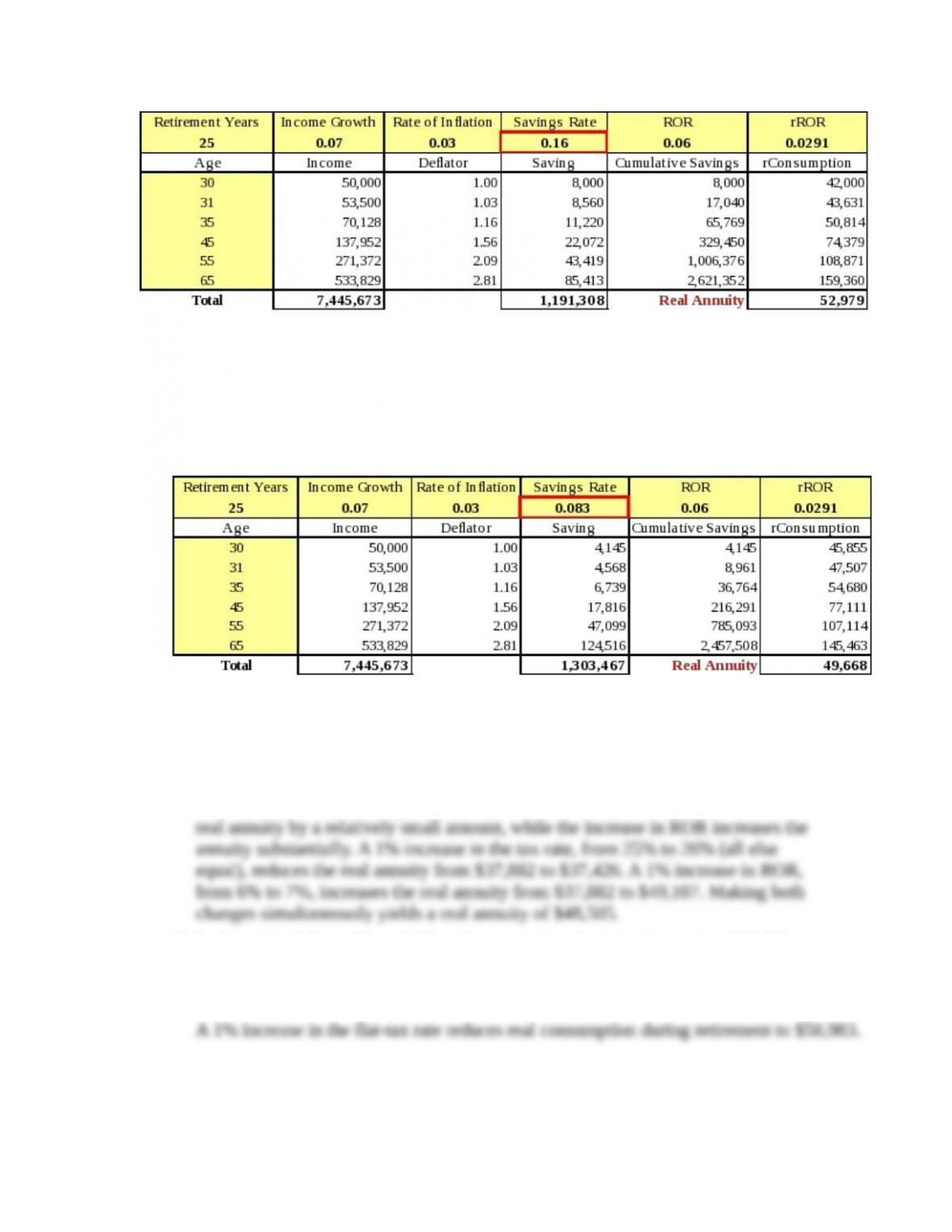

7. With a savings rate of 16%, the retirement annuity will be $52,979 (vs. $49,668).

The growth in the real retirement annuity (6.67%) is the same as with the case of

no inflation.

Spreadsheet 21.2: Adjusted for Change in Savings Rate

21-2

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 21 – Taxes, Inflation, and Investment Strategy

8. The objective is to obtain a real retirement annuity of $49,668, as in Spreadsheet

21.2. In Spreadsheet 21.3: Backloading the Real Savings Plan,select Data/Solver

from the menu bar. Set the objective value of Real Annuity to 49,668; Assign the

value of Saving Rate as the variable. Then we can solve for the saving rate from

real income:

Spreadsheet 21.3: With Objective Valueof Desired Real Annuity

We find that a savings rate of 8.3% from real income yields the desired real

retirement annuity.

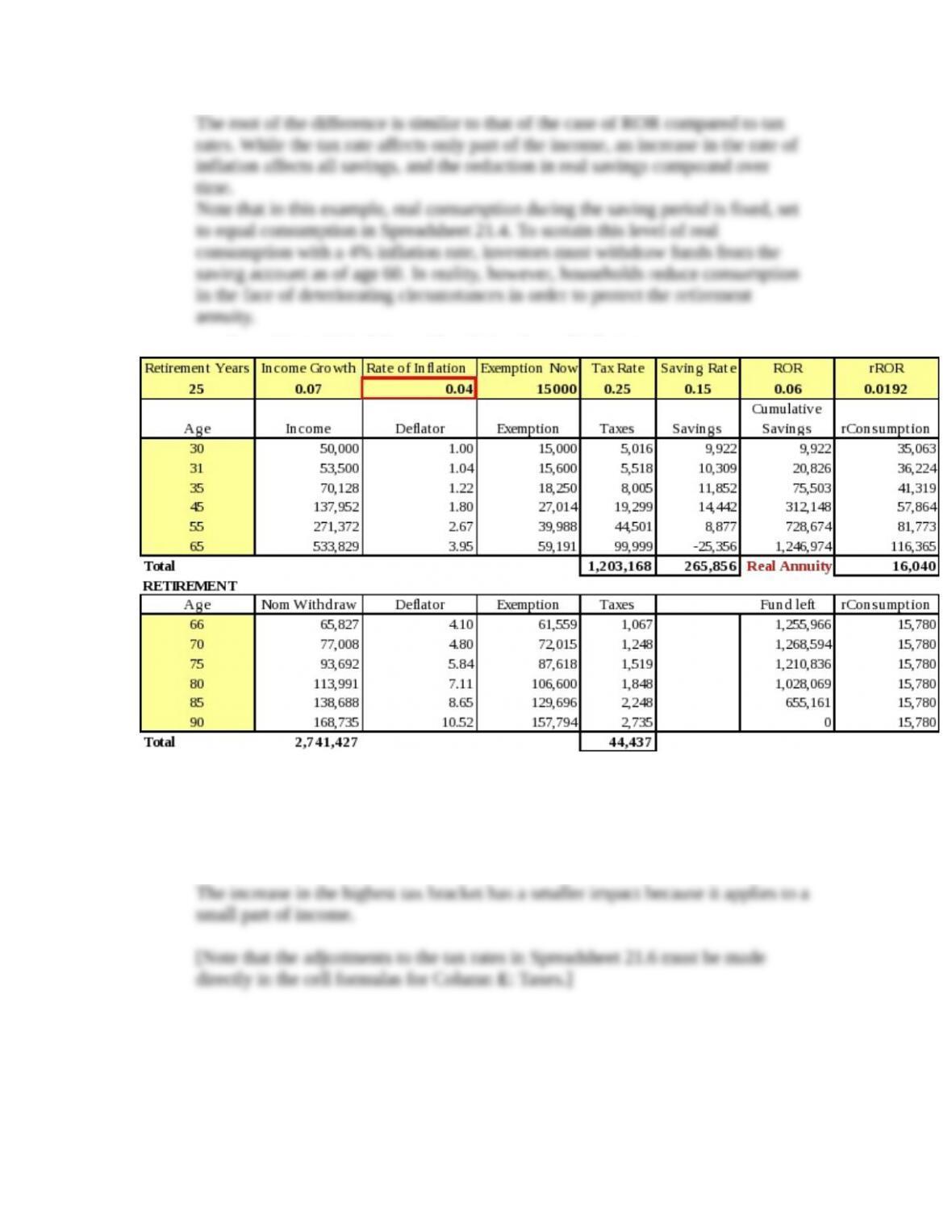

9. Because of the exemption from taxable income, only part of income is subject to

tax, while a change in ROR affects all savings.

As a result, we find from Spreadsheet 21.4 that the increase in tax rate reduces the

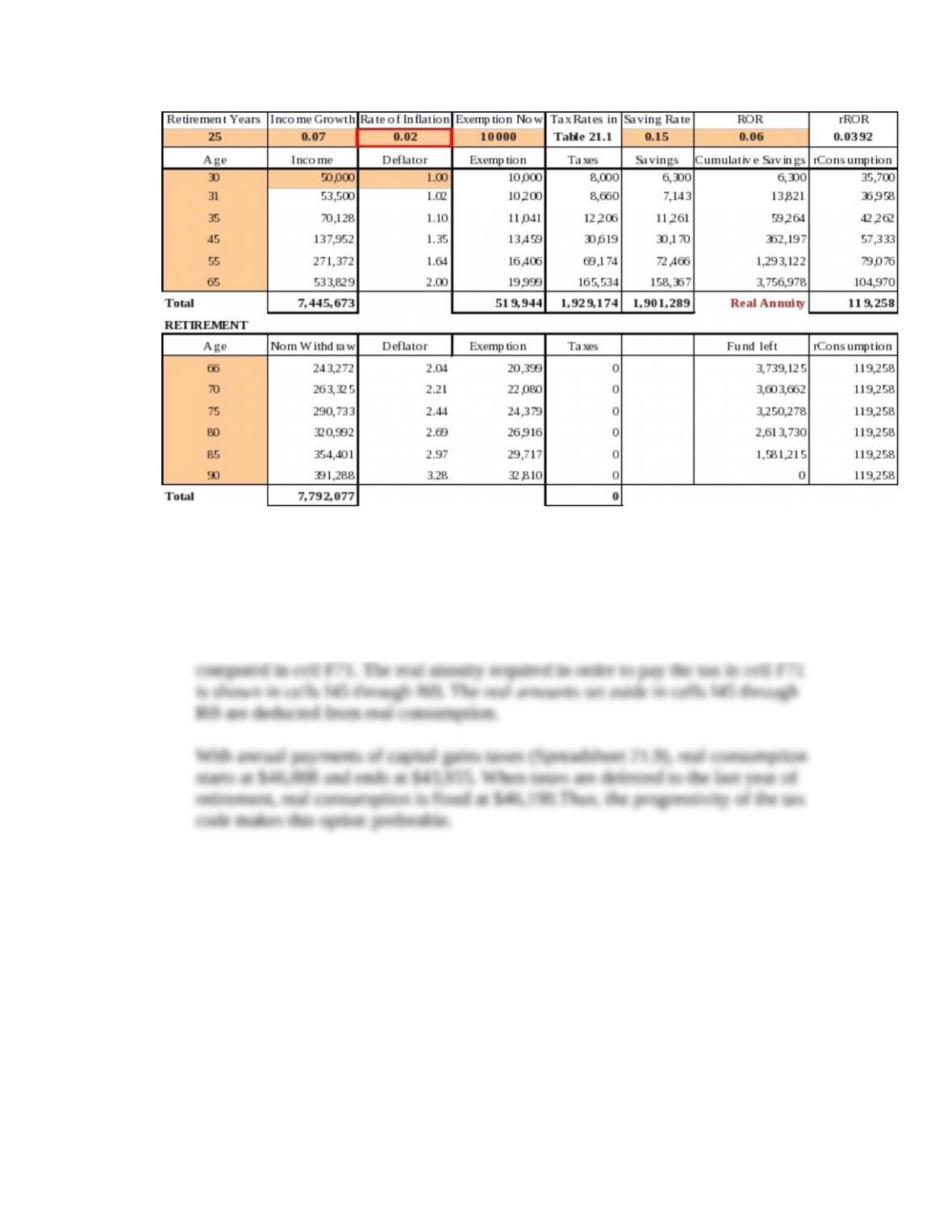

10. In the original Spreadsheet 21.5, real consumption during retirement is $60,789.

A 1% increase in the rate of inflation will reduce real consumption during

retirement to $15,780.

21-3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 21 – Taxes, Inflation, and Investment Strategy

Spreadsheet 21.5: Adjusted for Higher Rate of Inflation

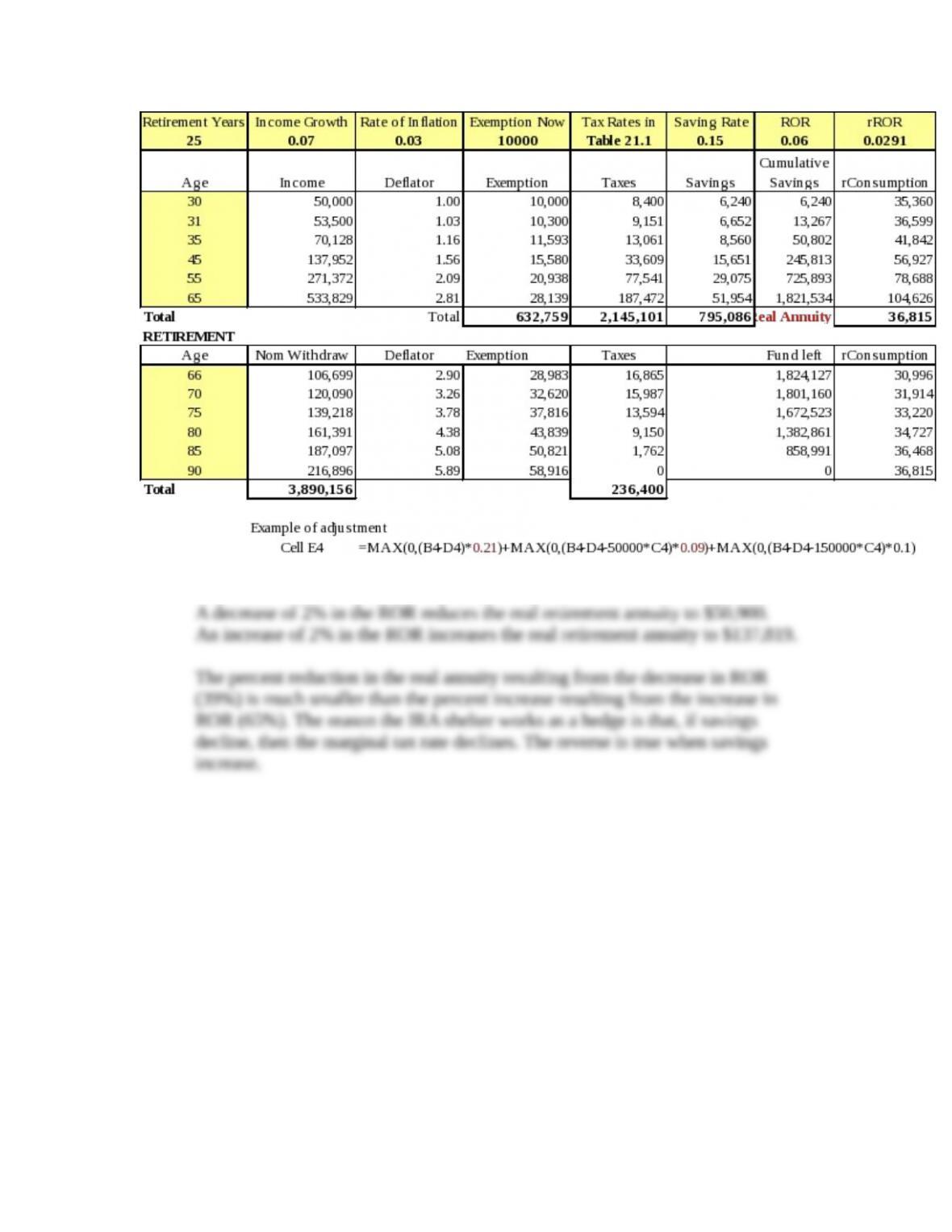

11. In Spreadsheet 21.6, the real retirement annuity is $37,059.

A 1% increase in the lowest tax bracket reduces the real retirement annuity to $36,815.

A 1% increase in the highest tax bracket reduces the real retirement annuity to

$37,033.

21-4

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 21 – Taxes, Inflation, and Investment Strategy

12. The real retirement annuity in Spreadsheet 21.7 is $83,380.

21-5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 21 – Taxes, Inflation, and Investment Strategy

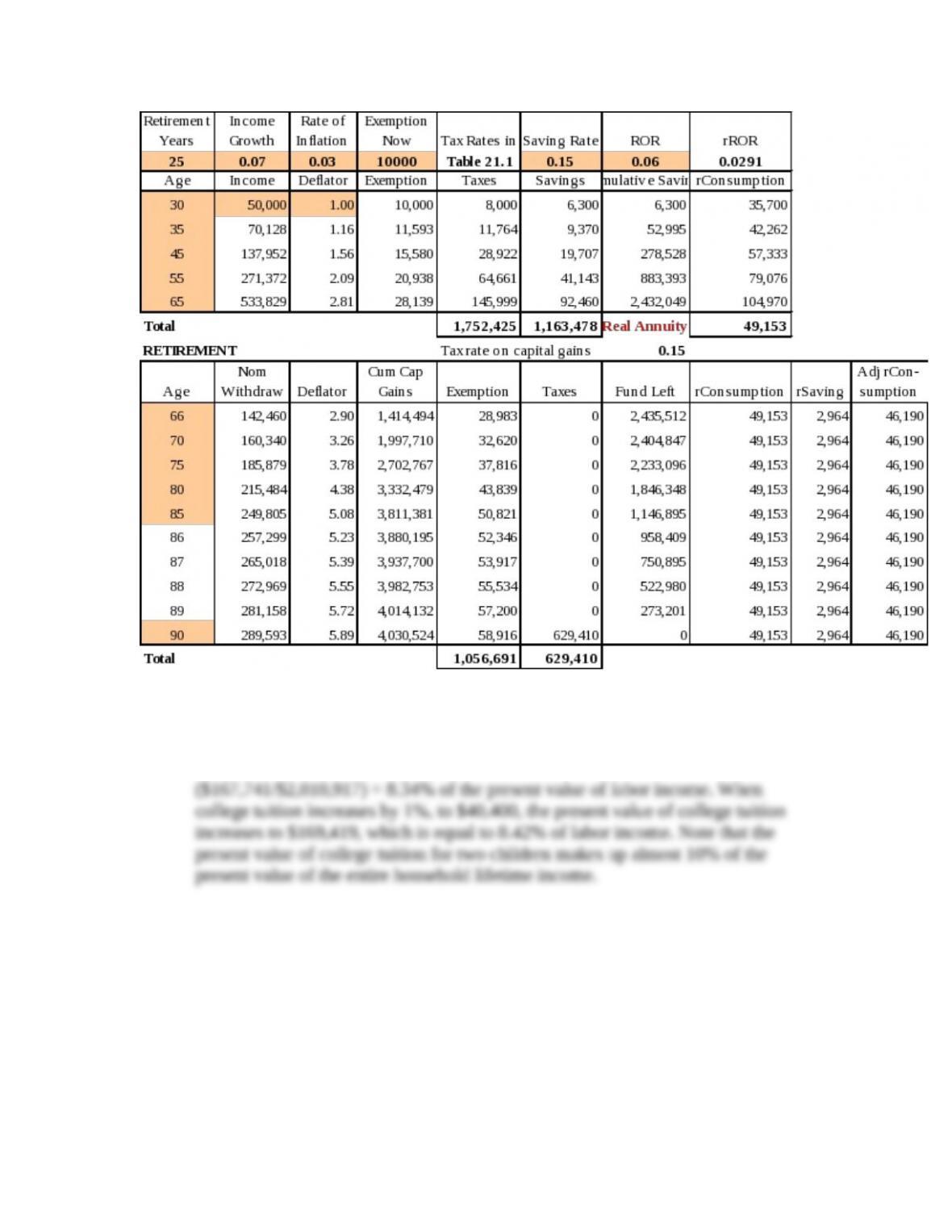

13. The real retirement annuity in Spreadsheet 21.8 is $ 49,153.

A 1% increase in ROR increases the real retirement annuity to $63,529.

A 1% decrease in the rate of inflation increases the real retirement annuity to $119,258.

21-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 21 – Taxes, Inflation, and Investment Strategy

14. When deferring taxes to the last year of retirement, you must set money aside

every year in order to accumulate a fund sufficient to pay the capital gains tax in a

lump sum. To leave consumption fixed in real terms, a fixed real amount is set

aside each year.

We calculate the cumulative capital gains in cells D45 through D69. The nominal

capital gains tax due in the final year appears in cell F69, and its real value is

21-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 21 – Taxes, Inflation, and Investment Strategy

15. Answers will vary.

16. The present value of labor income is $ 2,010,917 (at the rate of the applicable

ROR). The present value of college tuition is $167,741. This is equal to:

21-8

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 21 – Taxes, Inflation, and Investment Strategy

17. attempts to price an insurance contract based on the average characteristics of a

population, but, in the case of life insurance, for example, those whose health is

worse than average are more likely to buy the policy that is priced in terms of the

company’s average risk of loss because this price is a bargain for the person with

above-average risk. On the other hand, the person in good health will regard the

18. In general, moral hazard is a term associated with insurance contracts and with

government programs that essentially function as insurance. When an individual

or a business entity insures against loss of property due to fire, theft or other

21-9

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.