Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 19 - Globalization and International Investing

CHAPTER 19

19-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 19 - Globalization and International Investing

GLOBALIZATION AND INTERNATIONAL INVESTING

1. False. Investments made in a local currency have the added risk associated with

2. False. In almost all cases the statement is true, however, such diversification benefit is

3. False. Evidence shows that the minimum-variance portfolio is not the efficient choice.

4. True. By hedging, it is possible to virtually eliminate exchange rate risk. The result is a

set of returns based on the foreign stocks and not the currency fluctuations.

5.

a. $10,000/$2 = £5,000

b. To fill in the table, we use the relation:

Price per Pound-Denominated

Dollar-Denominated Return (%)

for Year-End Exchange Rate

Share (£)

Return (%)

$1.80/£

$2.00/£

$2.20/£

£35

–12.5%

–21.25%

–12.5%

–3.75%

6. The standard deviation of the pound-denominated return (using 3 degrees of freedom)

a. First we calculate the dollar value of the 125 shares of stock in each scenario.

Then we add the profits from the forward contract in each scenario.

Price per

Dollar Value of Stock

at Given Exchange Rate

Share (£)

Exchange Rate:

$1.80/£

$2.00/£

$2.20/£

19-2

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 19 - Globalization and International Investing

£35

7,875

8,750

9,625

£40 9,000 10,000 11,000

£45 10,125 11,250 12,375

Profits on Forward Exchange:

[ = 5000 (2.10 – E1)]

1,500 500 –500

Price per

Total Dollar Proceeds

at Given Exchange Rate

Share (£)

Exchange Rate:

$1.80/£

$2.00/£

$2.20/£

£35

9,375

9,250

9,125

£40 10,500 10,500 10,500

£45 11,625 11,750 11,875

Finally, calculate the dollar-denominated rate of return, recalling that the initial

investment was $10,000:

Price per

Rate of return (%)

at Given Exchange Rate

Share (£)

Exchange Rate:

$1.80/£

$2.00/£

$2.20/£

£35

–6.25%

–7.50%

–8.75%

£40 5.00% 5.00% 5.00%

£45 16.25% 17.50% 18.75%

b. The standard deviation is now 10.24%. This is lower than the unhedged

7. Currency Selection

Country Selection

Stock Selection

8. 1 + r(US) = [1 + rf (UK)] (F0/E0) = 1.08 (1.85/1.75) = 1.1417 r(US) = 14.17%

9. You can now purchase: $10,000/$1.75 = £5,714.29

19-3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 19 - Globalization and International Investing

10. The relationship between the spot and forward exchange rates indicates that the U.S.

11.

a. Using the relationship:

F0 = E0

1 + r f(US)

1 + r f(U K )

=

515.1

03.1

04.1

50.1

b. If the forward rate is 1.53 dollars per pound, then the forward rate is overpriced. To

create an arbitrage profit, use the following strategy:

Action Initial Cash Flow Cash Flow at Time T

Enter a contract to sell £1.03 at a

(futures price) of F0 = $1.53 0 1.03 (1.53 – E1)

Chapter 19 - Globalization and International Investing

14. See the results below.

19-5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 19 - Globalization and International Investing

CFA 1

Answer:

a. We exchange $1 million for foreign currency at the current exchange rate and

sell forward the amount of foreign currency we will accumulate 90 days from

now. For the yen investment, we initially receive:

19-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 19 - Globalization and International Investing

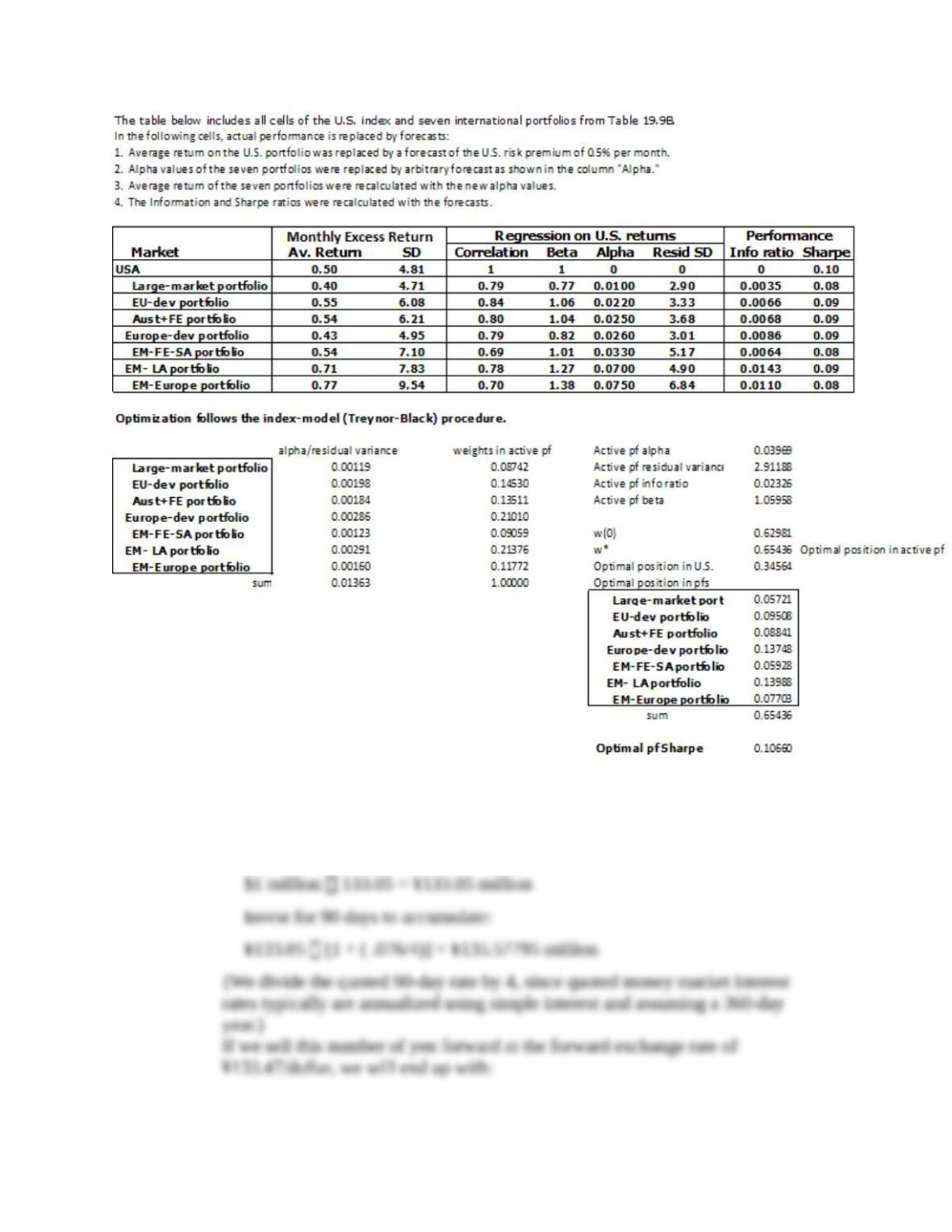

$ 135.57795 million

133.47

= $1.015793 million

The 90-day dollar interest rate is 1.5793%.

Similarly, the dollar proceeds from the 90-day Swiss franc investment will be:

[$1 million 1.526]

5348.1

)4/086(.1

= $1.015643 million

The 90-day dollar interest rate is 1.5643%, almost the same as that in the yen

investment.

b. The nearly identical results in either currency are expected and reflect the

c. The dollar-hedged rate of return on default-free government securities in Japan

is 1.5793% and in Switzerland is 1.5643%. Therefore, the 90-day interest rate

available on U.S. government securities must be between 1.5643% and

1.5793%. This corresponds to an annual rate between 6.2572% and 6.3172%,

CFA 2

a. The primary rationale is the opportunity for diversification. Factors that

contribute to low correlations of stock returns across national boundaries are:

b. Obstacles to international investing are:

i. Availability of information, including insufficient data on which to base

19-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 19 - Globalization and International Investing

ii. Liquidity, in terms of the ability to buy or sell, in size and in a timely

iii. Transaction costs, particularly when viewed as a combination of

iv. Political risk.

v. Foreign currency risk, although to a great extent, this can be hedged.

c. The asset-class performance data for this particular period reveal that non-U.S.

dollar bonds provided a small incremental return advantage over U.S. dollar bonds,

but at a considerably higher level of risk. Each category of fixed income assets

Answer:

The return on the Canadian bond is equal to the sum of:

coupon income +

Chapter 19 - Globalization and International Investing

CFA 4

Answer:

a. The following arguments could be made in favor of active management:

Economic diversity: the diversity of the Otunian economy across various sectors

may offer the opportunity for the active investor to employ "top down" sector

timing strategies.

19-9

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.