Chapter 17 – Futures Markets and Risk Management

CHAPTER 17

17-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 17 – Futures Markets and Risk Management

FUTURES MARKETS AND RISK MANAGEMENT

1. Selling a contract is a short position. If the price rises, you lose money.

2. Futures price = S0 (1+ rf− d)T = $1,200 (1 + .01 – .02) = $1,188

3. The theoretical futures price = S0 (1+ rf)T = $1,700 (1 + .02) = $1,734. At $1,641, the

4. Margin = $115,098 .15 = $17,264.70

5.

a. The required margin is 1,164.50$250 .10 = $29,112.50

b. Total Return = (1,200 – 1,164.50) $250 = $8,875

c. Total Loss = [1,164.5 (1 – .01)]– 1,164.5) $250 = –$2,911.25

6. The ability to buy on margin is one advantage of futures. Another is the ease with

7. Short selling results in an immediate cash inflow, whereas the short futures position

does not:

Action Initial Cash Flow Cash Flow at Time T

Short sale

+S0

–ST

Short futures 0 F0 – ST

8. F0 = S0 (1 + rf – d) = $1,200 (1 + .03 – .02) = $1,212

9. According to the parity relationship, the proper price for December futures is:

The listed futures price for December is too low relative to the June price. We could

10.

17-2

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 17 – Futures Markets and Risk Management

a.

Action Initial Cash Flow Cash Flow at Time T

Buy stock

–S0

ST + D

Short futures 0 F0 – ST

Borrow S0–S0(1 + r)

Total

0

F0 + D – S0(1 + r)

b. The net initial investment is zero, whereas the final cash flow is not zero.

Therefore, in order to avoid arbitrage opportunities, the equilibrium futures

c. Noting that D = (d S0), we substitute and rearrange to find that:

11.

a. F0 = S0 (1 + rf)T = $150 1.03 = $154.50

12.

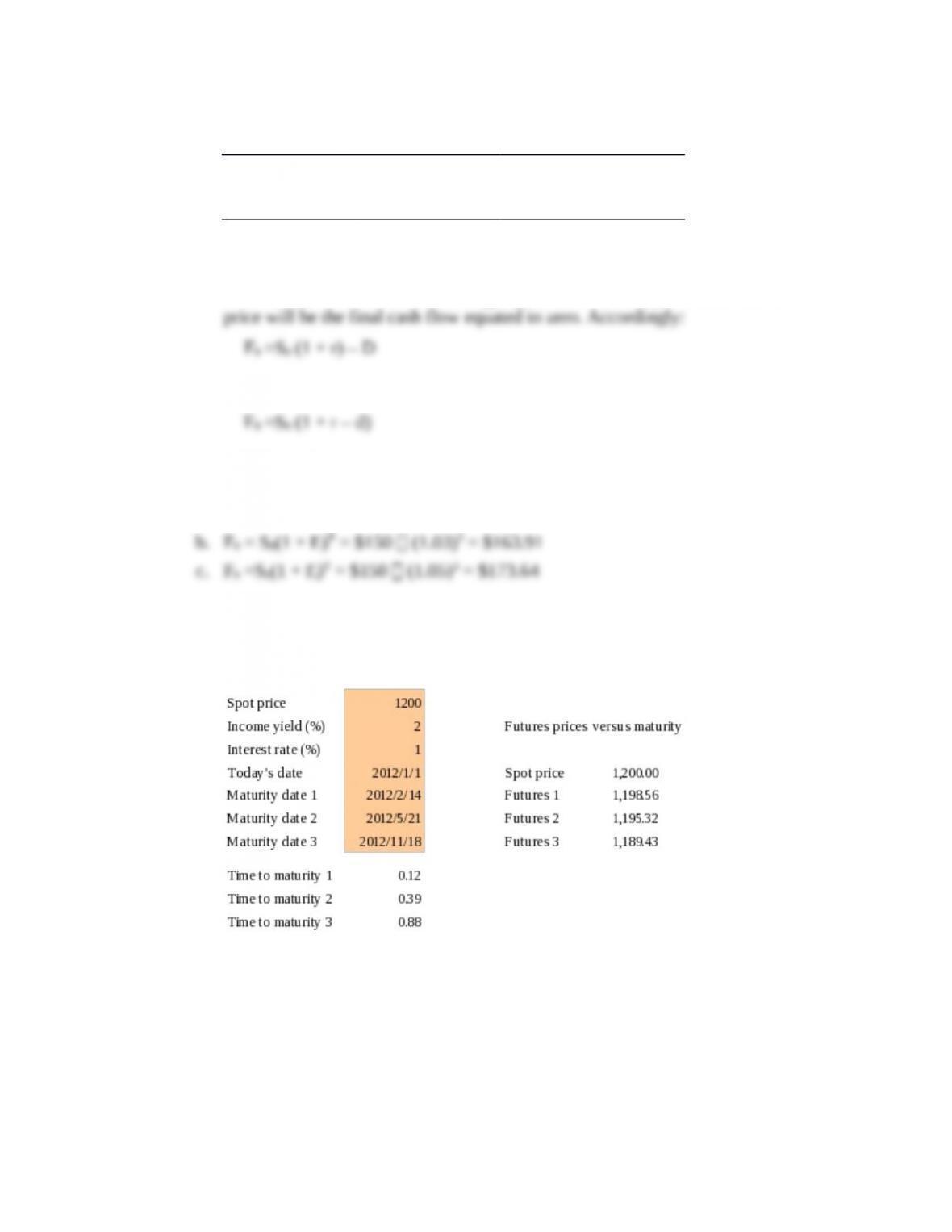

a. Use the spreadsheet template from www.mhhe.com/bkm, input spot price,

dividend yield, interest rate, and the dates, and get the expected future prices of

each maturity dates.

b. If the risk-free rate is higher than the dividend yield, the future price with longer

maturity will be higher than those with shorter maturities.

13.

a. F0 = S0 (1 + rf) = $120 1.06 = $127.20

17-3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 17 – Futures Markets and Risk Management

b. The stock price falls to: $120 (1 – .03) = $116.40

c. The percentage return is: –$3,816/$12,000 = –31.8%

14.

a. The initial futures price is:

b. The holding period return is: $1,962.50/$10,000 = .1963 = 19.63%

15. The parity value of F0 is:S0 (1 + rf – d) =1,200 (1 + .03 – .02) = 1,212

The actual futures price is 1,233, overpriced by 21.

Action Initial Cash Flow Cash Flow at Time T (one year)

Buy index

–1,200

ST + (.02 × 1,200) [CF includes 2% dividend]

Chapter 17 – Futures Markets and Risk Management

20.

a. The initial futures price is: F0 = 1,000 (1 + .002 – .001)12 = 1,012.07

b. The holding period return is: $4,802.50/$10,000 = .48025 = 48.03%

21. The Treasurer would like to buy the bonds today, but cannot. As a proxy for this

22. She must sell:

8. $

10

8

million 1$

million of T-bond

23. If yield changes on the bond and the contracts are each 1 basis point, then the bond

value will change by:

24.

a. Each contract is for $250 times the index, currently valued at 1,200. Therefore,

b. The parity value of the futures price = 1,200 (1 + .02 – .01) = 1,212

Action Initial Cash Flow Cash Flow at Time T

Short 20 futures contracts

0

20 × $250 (1,212 – ST)

17-5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 17 – Futures Markets and Risk Management

c. Now, the stock swings only .6 as much as the market index. Hence, we need .6 as

many contracts as in part (a): .60 20 = 12 contracts

25. The firm should enter a swap in which it pays a 7% fixed rate and receives LIBOR on

$10 million of notional principal. Its total payments will be as follows:

26.

a. From parity: F0 = S0 (1 + rf – d) = [1,200 (1 + .03)] – 15 = 1,221

b. Buy the relatively cheap futures and sell the relatively expensive stock.

Action Initial Cash Flow Cash Flow at Time T

Short stock

+1,200

–(ST + 15)

Short stock

+1,200

–(ST + 15)

Short stock

+1,200

–(ST + 15)

Chapter 17 – Futures Markets and Risk Management

Therefore, F0can be as low as 1,185 without giving rise to an arbitrage

opportunity. On the other hand, if F0 is higher than the parity value (1,218) an

arbitrage opportunity (buy stocks, sell futures) will open up. There is no

short-selling cost in this case. Therefore, the no-arbitrage region is:1,185 F0

1,218CFA 1

Answer:

a.Contrasts

CFA 2

Answer:

d. Maintenance margin

CFA 3

Answer:

Total losses may amount to $3,500 before a margin call is received. Each contract calls

for delivery of 5,000 ounces. Before a margin call is received, the price per ounce can

CFA 4

Answer:

a. Take a short position in T-bond futures, to offset interest rate risk. If rates

b. Again, a short position in T-bond futures will offset the bond price risk.

c. If bond prices increase, you will need extra cash to purchase the bond with the

CFA 5

Answer:

The important distinction between a futures contract and an options contract is that the

futures contract is an obligation. When an investor purchases or sells a futures contract,

CFA 6

Answer:

17-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 17 – Futures Markets and Risk Management

a. The strategy that would take advantage of the arbitrage opportunity is a Reverse

Cash and Carry. A Reverse Cash and Carry arbitrage opportunity results when

the following relationship does not hold true:F0, t ≥ S0 (1+ C)

b.

Opening Transaction Now

Sell the spot commodity short +$120.00

Buy the commodity futures expiring in 1 year 0.00

Closing Transaction One Year from Now

Accept delivery on expiring futures –$125.00

Cover short commodity position 0.00

CFA 7

Answer:

a. In an interest rate swap, one firm exchanges (or “swaps”) a fixed payment for

another payment that is tied to the level of interest rates. One party in the swap

agreement pays a fixed interest rate on the notional principal of the swap. The other

Therefore, if LIBOR exceeds 8%, then this firm receives a payment; if LIBOR is

less than 8%, then the firm makes a payment.

b. There are several applications of interest rate swaps. For example, suppose that a

portfolio manager is holding a portfolio of long-term bonds, but is worried that

17-8

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 17 – Futures Markets and Risk Management

However, the fund manager might believe that such short-term assets are

inappropriate for the portfolio. The fund can hold these securities and enter a

CFA 8

Answer:

a. Delsing should sell stock index futures contracts and buy bond futures contracts.

This strategy is justified because buying the bond futures and selling the stock

index futures provides the same exposure as buying the bonds and selling the

b. Compute the number of contracts in each case as follows:

CFA 9

Answer:

a. Short the contract. As rates rise, prices will fall. Selling the futures contract will

benefit from falling prices.

b. In 6 months the bond will accrue $25 of interest, which, when subtracted from

the price of 978.40, leaves a bond value of 953.40. This implies a YTM of

c. The contract drops in price by 47.98, while the bond drops in price 46.60. Both

17-9

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.