Chapter 16 – Option Valuation

1.

a. Choice A: Calls have higher elasticity than shares. For equal dollar

b. Choice B: Calls have hedge ratios less than 1.0. For equal numbers of shares

2. Step 1: Calculate the option values at expiration. The two possible stock prices are: S+ =

Step 2: Calculate the hedge ratio: (Cu – Cd)/(uS0 – dS0) = (20 – 0)/(120 – 80) = .5

3. Step 1: Calculate the option values at expiration. The two possible stock prices are: S+

= $130 and S– = $70. Therefore, since the exercise price is $100, the corresponding two

possible call values are: Cu = $30 and Cd = $0.

4. We start by finding the value of Pu . From this point, the put can fall to an expiration-date

value of Puu = $0 (since at this point the stock price is uuS0 = $121) or rise to a final value

of Pud = $5.50 (since at this point the stock price is udS0 = $104.50, which is less than the

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

Thus, the following portfolio will be worth $121 at option expiration regardless of the

ultimate stock price:

Riskless portfolio udS0 = $104.50 uuS0 = $121

Buy 1 share at price uS0 = $110 $104.50 $121.00

Next we find the value of Pd . From this point (at which dS0 = $95), the put can fall to an

expiration-date value of Pdu = $5.50 (since at this point the stock price is

duS0 = $104.50) or rise to a value of Pdd = $19.75 (since at this point, the stock price is

Chapter 16 – Option Valuation

Buy 0.5344 share at price S = $100 $50.768 $58.784

Buy 1 put at price P 9.762 1.746

5.

S0 = 100 (current value of portfolio)

X = 100 (floor promised to clients, 0% return)

a. The put delta is: N(d1) – 1 = 0.7422 – 1 = –.2578

b. At the new portfolio value, the put delta becomes –.2779, so that the amount

6.

a.

Stock price 110 90

b. The cost of the protective put portfolio is the cost of one share plus the cost of

one put: $100 + $2.38 = $102.38

16-3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

c. The goal is a portfolio with the same exposure to the stock as the hypothetical

7. u = exp(

t

); d = exp(–

t

)

a. 1 period of one year

1

1

b. 4 subperiods, each 3 months

4/1

4/1

c. 12 subperiods, each 1 month

12/1

12/1

8. u = 1.5 = exp(

t

) = exp(

1

)

9. Given S0= X when the put and the call are at-the-money, the relationship of put-call

parity, P = C – S0 + PV(X)can be written as: P = C – S0 + PV(S0).

S0

10. We first calculate the risk neutral probability that the stock price will increase:

16-4

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

p =

1+ r f - d

u -d

=

1 + .1 -.8

1.2 -.8

= .75

Then use the probability to find the expected cash flow at expiration, and discount it by

the risk free rate:

E(CF) = .75 $20 + .25 0 = $15

C =

E(CF)

1 + r f

=

$ 15

1.1

=$13.64

It matches the value we found in problem 35.

11. We first calculate the risk neutral probability that the stock price will increase:

p =

1 + r f - d

u -d

=

1 + .05 -. 95

1.1 -.95

= .6667

Then use the probability to find the expected cash flows at expiration, and discount it

by the risk free rate to find Puand Pd:

uE(CF) = .6667 0 + .3333 $5.5 = $1.8333

Pu =

E(CF)

1 + r f

=

$1 .8333

1.05

=$1.7460

dE(CF) = .6667 $5.5 + .3333 $19.75 = $10.25

Pd =

E(CF)

1 + r f

=

$ 10.25

1.05

=$9.7619

Finally, compute the expected cash flow in 6 month, and discount the E(CF) by the 6

month risk free rate:

E(CF) = .6667 1.7460 + .3333 $9.7619 = $4.4180

P =

E(CF)

1 + r f

=

$4. 4180

1.05

=$4.208

It matches the value we found in problem 37.

CFA 1

Answer:

a. i. The combined portfolio will suffer a loss. The written calls will expire in the

money. The protective put purchased will expire worthless. Each short call will

16-5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

ii. Both options expire out of the money, and are thus not exercised. The

iii. The calls will expire worthless and the portfolio will retain the short call

option price. The put option will be exercised and the proceeds used to offset

the purchase price of the put and the decline in value of the portfolio.

b. i. The delta of the call will approach 1.0 as the stock goes deep into the money,

ii. Both options expire out of the money. Delta of each will approach zero as

iii. The call is out of the money as expiration approaches. Delta approaches

c. The call sells at an implied volatility (20.00%) that is less than recent historical

volatility (21.00%); the put sells at an implied volatility (22.00%) that is greater

CFA 2

Answer:

a. i. The option price will decline.

ii. The option price will increase.

b. i. Besides Weber’s belief thatthe implied volatility may differ from the market,

ii. An American option may be exercised early, and the value of early exercise

CFA 3

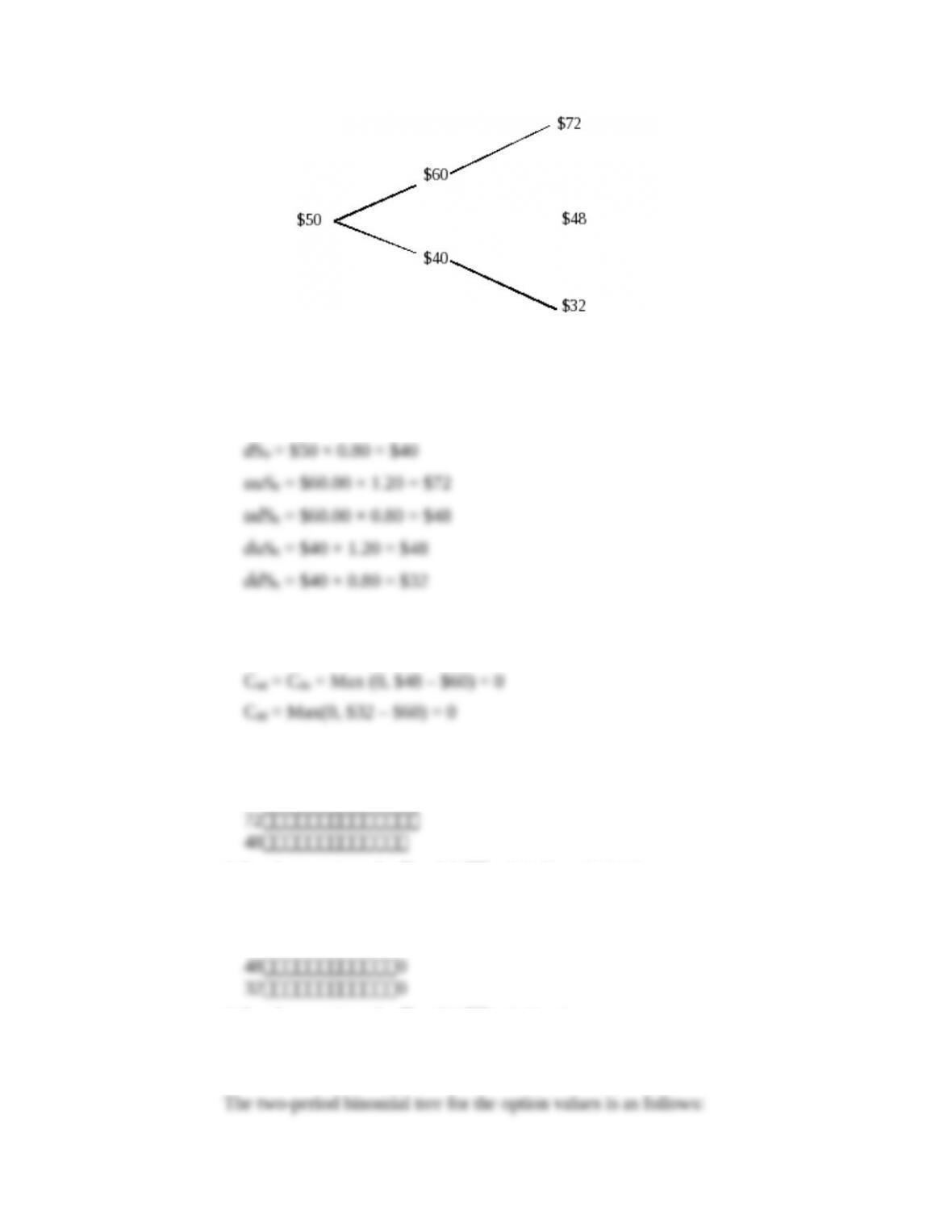

Answer:

a. Over two periods, the stock price must follow one of four patterns: up-up,

up-down, down-down, or down-up.

The binomial parameters are:

The two-period binomial tree is as follows:

16-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

The calculations for the values shown above are as follows:

uS0 = $50 × 1.20 = $60

a. The value of a call option at expiration is: Max(0, S – X)

Cuu = Max (0, $72 – $60) = $12

We use a portfolio combining the underlying stock and bond to replicate the

payoffs: ST rf)Payoff

Solve the equations for and B = 0.5, B = –22.6415

Therefore, the Cu = 60

Solve the equations for and B = 0, B = 0

Therefore, the Cd = 40

16-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

607.3585

400

b. The value of a call option at expiration is: Max(0, X – S)

We use a portfolio combining the underlying stock and bond to replicate the

payoffs: ST rf)Payoff

16-8

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

603.9623

40

Solve the equations for and B = –0.6321, B = 39.5158

Therefore, the C = 50

c. The put-call parity relationship is:

16-9

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.