Chapter 16 – Option Valuation

CHAPTER 16

16-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

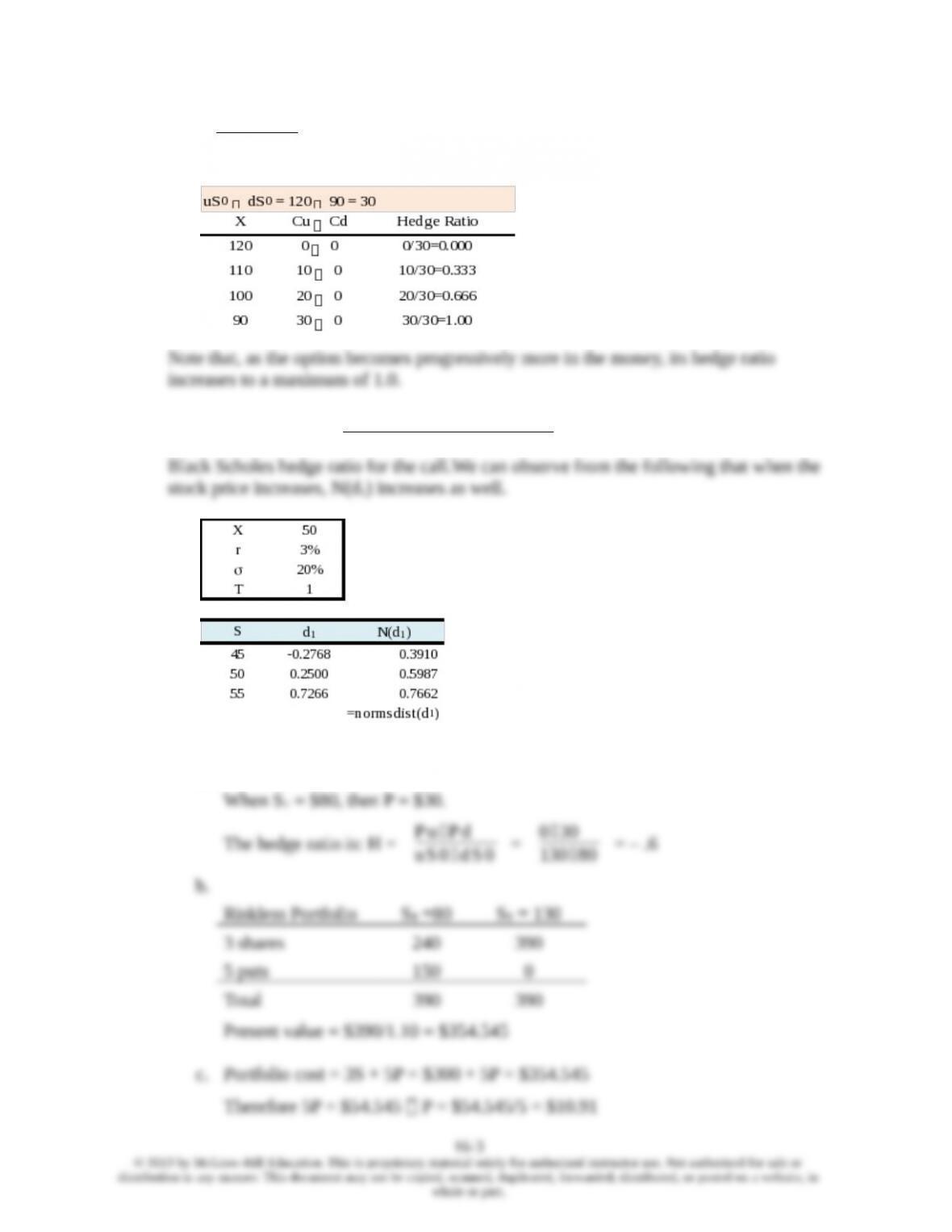

Chapter 16 – Option Valuation

OPTION VALUATION

1. Intrinsic value = S0– X= $55 – $50 = $5.00

2. Using put-call parity: Put = C–S0 + PV(X) + PV(Dividends)

3. Using put-call parity: Put = C–S0 + PV(X) + PV(Dividends)

4. Put values also increase as the volatility of the underlying stock increases. We see this

from the parity relationship as follows:

Numerical example:

Suppose you have a put with exercise price 100, and that the stock price can take on

one of three values: 90, 100, 110. The payoff to the put for each stock price is:

Now suppose the stock price can take on one of three alternate values also centered

around 100, but with less volatility: 95, 100, 105. The payoff to the put for each stock

price is:

The payoff to the put in the low volatility example has one-half the expected value of

the payoff in the high volatility example.

5.

a. (1) Put A must be written on the lower-priced stock. Otherwise, given the lower

volatility of stock A, put A would sell for less than put B.

b. (2) Put B must be written on the stock with lower price. This would explain its

c. (2) Call B. Despite the higher price of stock B, call B is cheaper than call A.

d. (2) Call B. This would explain its higher price.

e. (3) Not enough information. The call with the lower exercise price sells for

16-2

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

6. H =

C u - Cd

u S 0 - d S 0

7. We first calculate d1=

ln (S 0 /X ) + ( r -- -+ - 2 /2)T

-

, and then find N(d1), which is the

8.

a. When ST = $130, then P = 0.

Chapter 16 – Option Valuation

9. The hedge ratio for the call is: H =

C u - Cd

u S 0 - d S 0

=

20 -0

130 -80

= .4

10. a. A delta-neutral portfolio is perfectly hedged against small price changes in the

11. a. Delta is the change in the option price for a given instantaneous change in the stock

12. The best estimate for the change in price of the option is: Change in asset price × delta

13. The number of call options necessary to delta hedge is

51,750 75, 000

0.69 =

options or 750

14. A delta-neutral portfolio can be created with any of the following combinations: long

15. d1=

ln (S0 /X ) + ( r -- -+ - 2 /2)T

-

=

ln (50 / 50 ) + (.03 - -- +.5 2 /2) × .5

.5×

= 0.2192

N(d1) = 0.5868

16-4

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

16. P = Xe–rT[1N(d2)] S0 e–T[1 N(d1)] =$6.60

17. Use the Black-Scholes spreadsheet and change the input for each of the followings:

a. Time to expiration = 3 months = .25 yearC falls to $5.14

b. Standard deviation = 25% per year C falls to $3.88

c. Exercise price = $55 C falls to $5.40

d. Stock price = $55 C rises to $10.54

e. Interest rate = 5% C rises to $7.56

18. A straddle is a call and a put. The Black-Scholes value is:

19. The call price will decrease by less than $1. The change in the call price would be $1

20. Holding firm-specific risk constant, higher beta implies higher total stock volatility.

21. Holding beta constant, the stock with high firm-specific risk has higher total volatility.

22. The call option with a high exercise price has a lower hedge ratio. Both d1 and N(d1)

23. The call option is more sensitive to changes in interest rates. The option elasticity

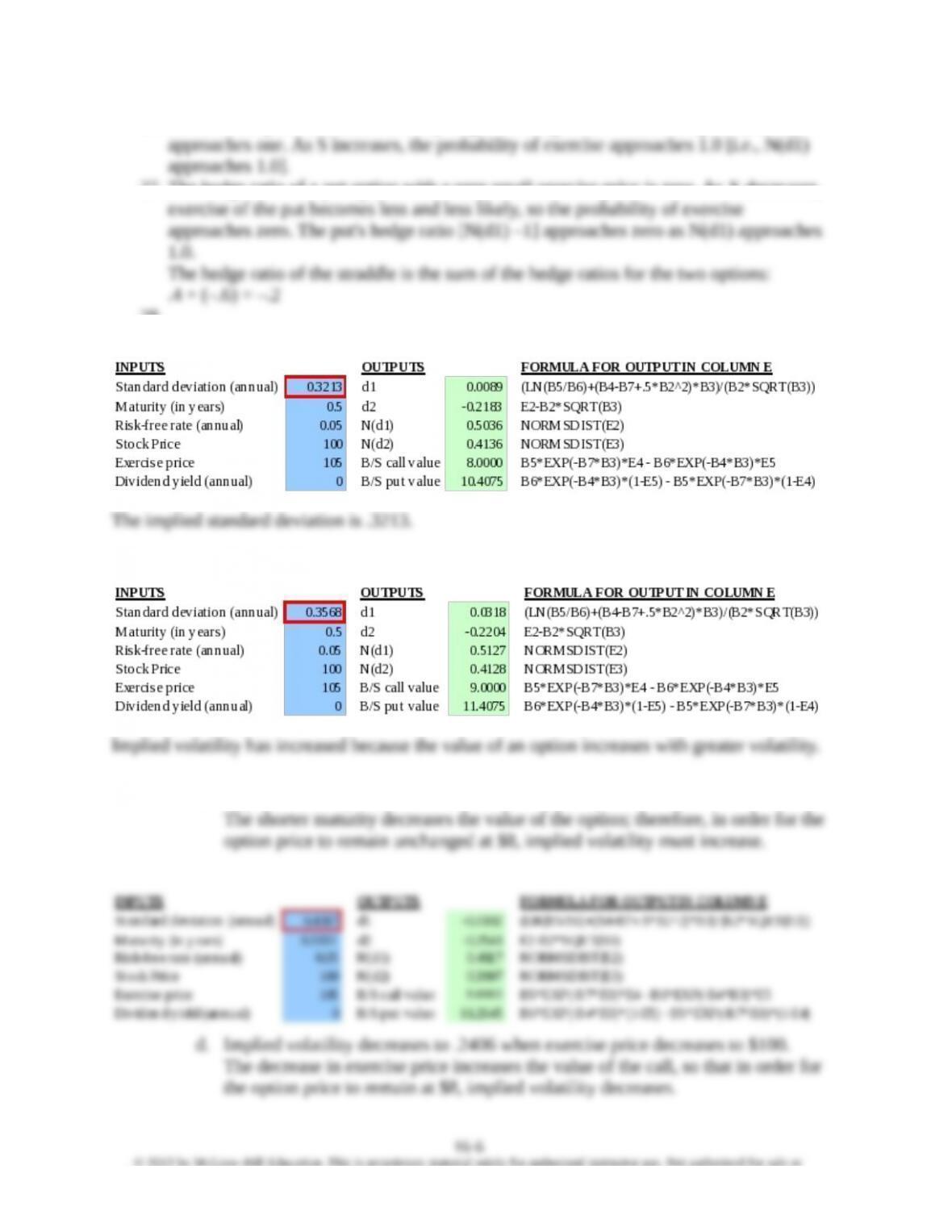

24. The call option’s implied volatility has increased. If this were not the case, then the call

25. The put option’s implied volatility has increased. If this were not the case, then the put

16-5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

26. As the stock price becomes infinitely large, the hedge ratio of the call option [N(d1)]

27. The hedge ratio of a put option with a very small exercise price is zero. As X decreases,

28.

a. The spreadsheet appears as follows:

b. The spreadsheet below shows the standard deviation has increased to: .3568

c. Implied volatility increases to .4087 when maturity decreases to four months.

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

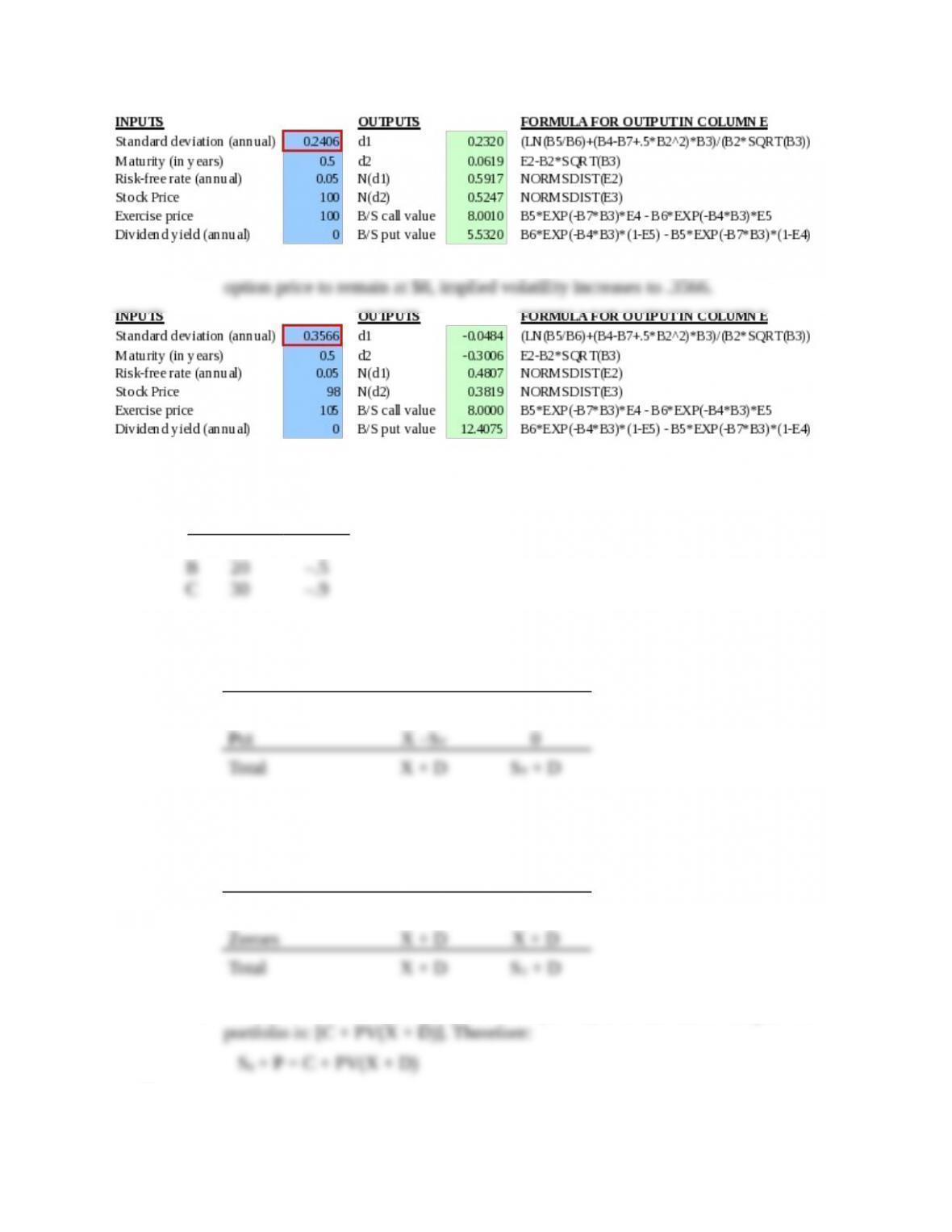

e. The decrease in stock price decreases the value of the call. In order for the

29. A put is more in the money, and has a hedge ratio closer to –1, when its exercise price is

higher:

Put X Delta

A

10

–.1

30.

a.

Position ST< X ST> X

Stock ST + D ST + D

b. The total value for each of the two strategies is the same, regardless of the stock

price (ST).

Position ST< X ST> X

Call 0 ST – X

c. The cost of the stock-plus-put portfolio is (S0 + P). The cost of the call-plus-zero

31.

16-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 16 – Option Valuation

a. The delta of the collar is calculated as follows:

Delta

Stock 1.0