Chapter 15 – Options Markets

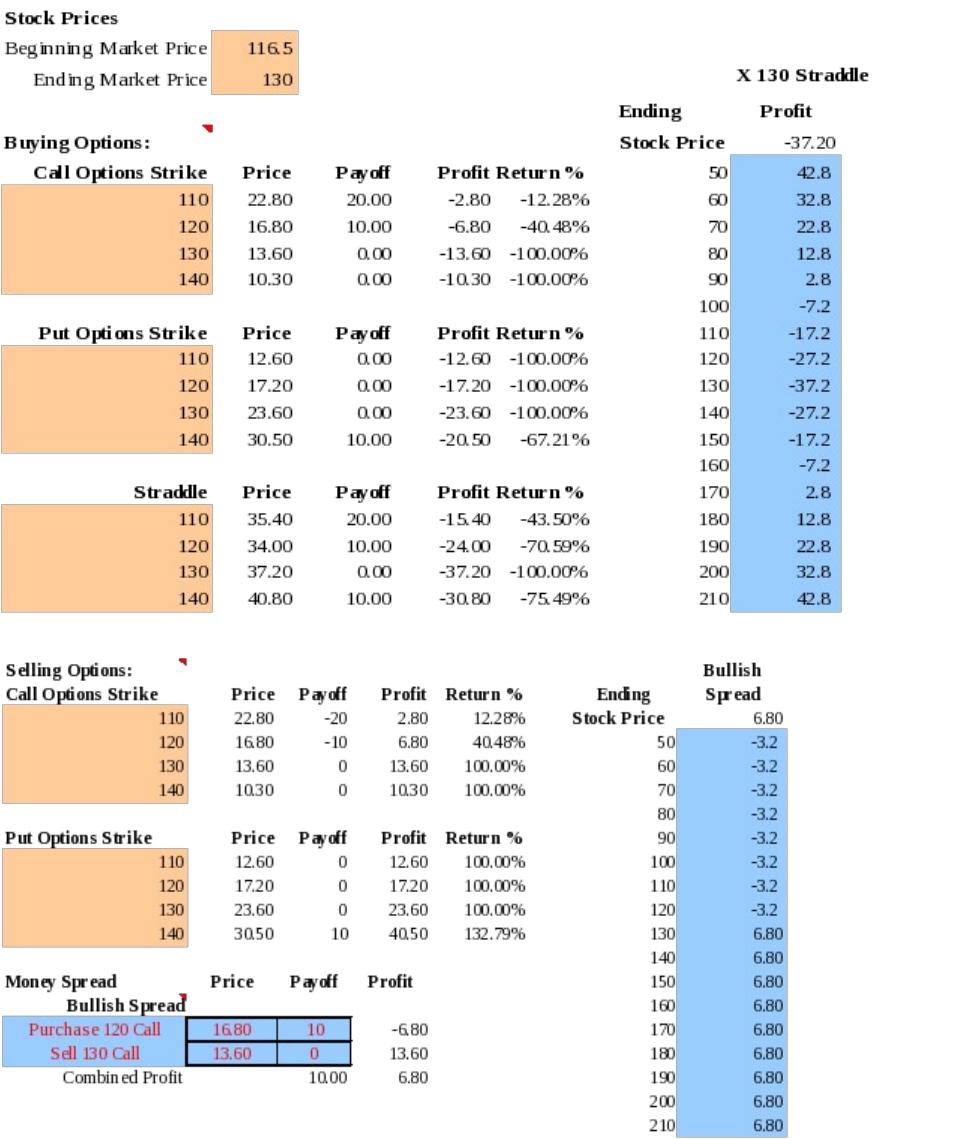

19. The Excel spreadsheet for both parts (a) and (b) is shown on the next page, and the

profit diagrams are on the following page.

a. & b.

15-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 – Options Markets

40 60 80 100 120 140 160 180 200 220

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

Bullish Spread

130 Straddle

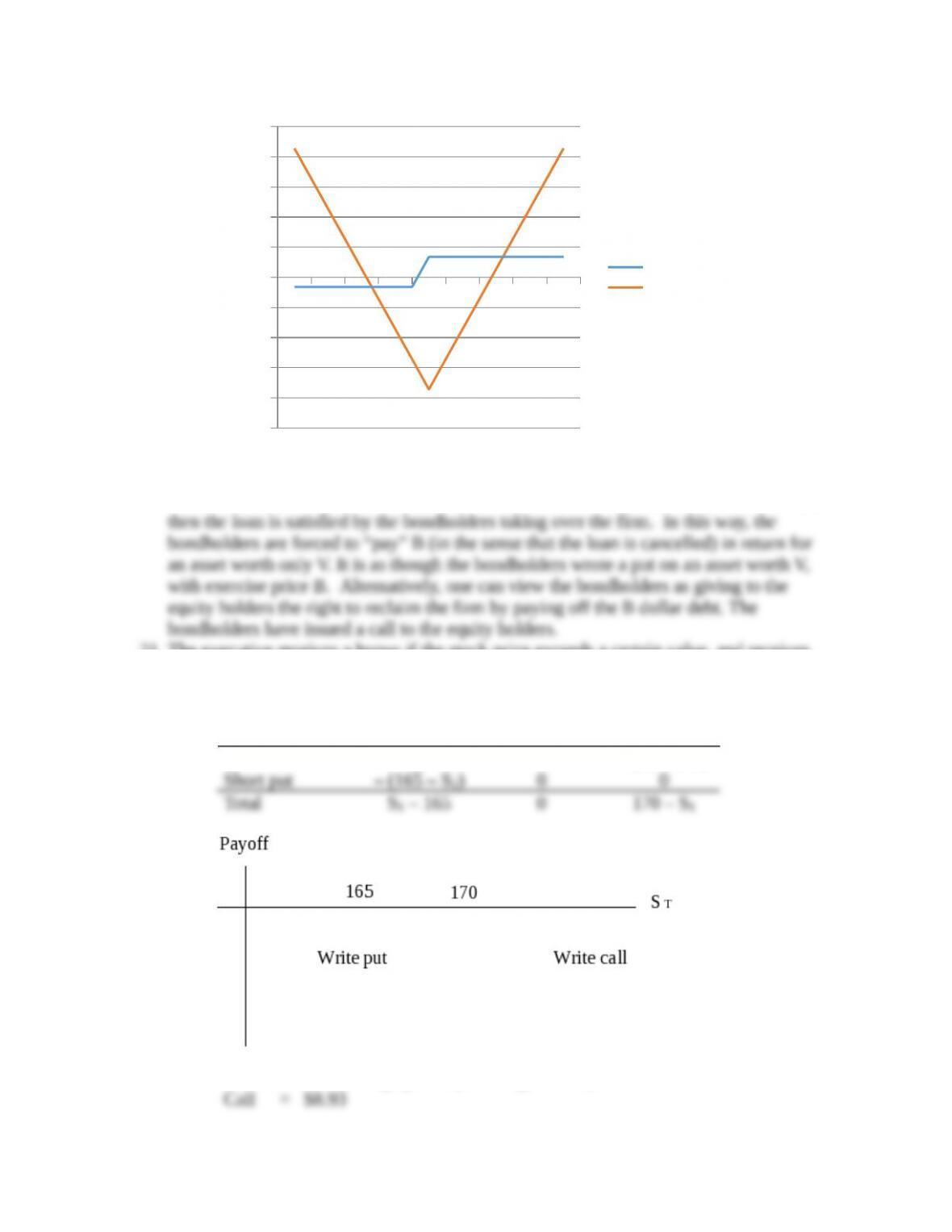

20. The bondholders have, in effect, made a loan which requires repayment of B dollars,

where B is the face value of bonds. If, however, the value of the firm (V) is less than B,

21. The executive receives a bonus if the stock price exceeds a certain value, and receives

nothing otherwise. This is the same as the payoff to a call option.

22.

a.

Position ST < 165 165 < ST < 170 ST > 170

Short call 0 0 – (ST – 170)

b. Proceeds from writing options (from Figure 15.1):

15-2

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 – Options Markets

c. You will break even when either the short position in the put or the short

position in the call results in a cash outflow of $19.78. For the put, this requires

that:

d. The investor is betting that the IBM stock price will have low volatility.

23.

a.

b. The put with the higher exercise price must cost more. Therefore, the net outlay

to establish the portfolio is positive.

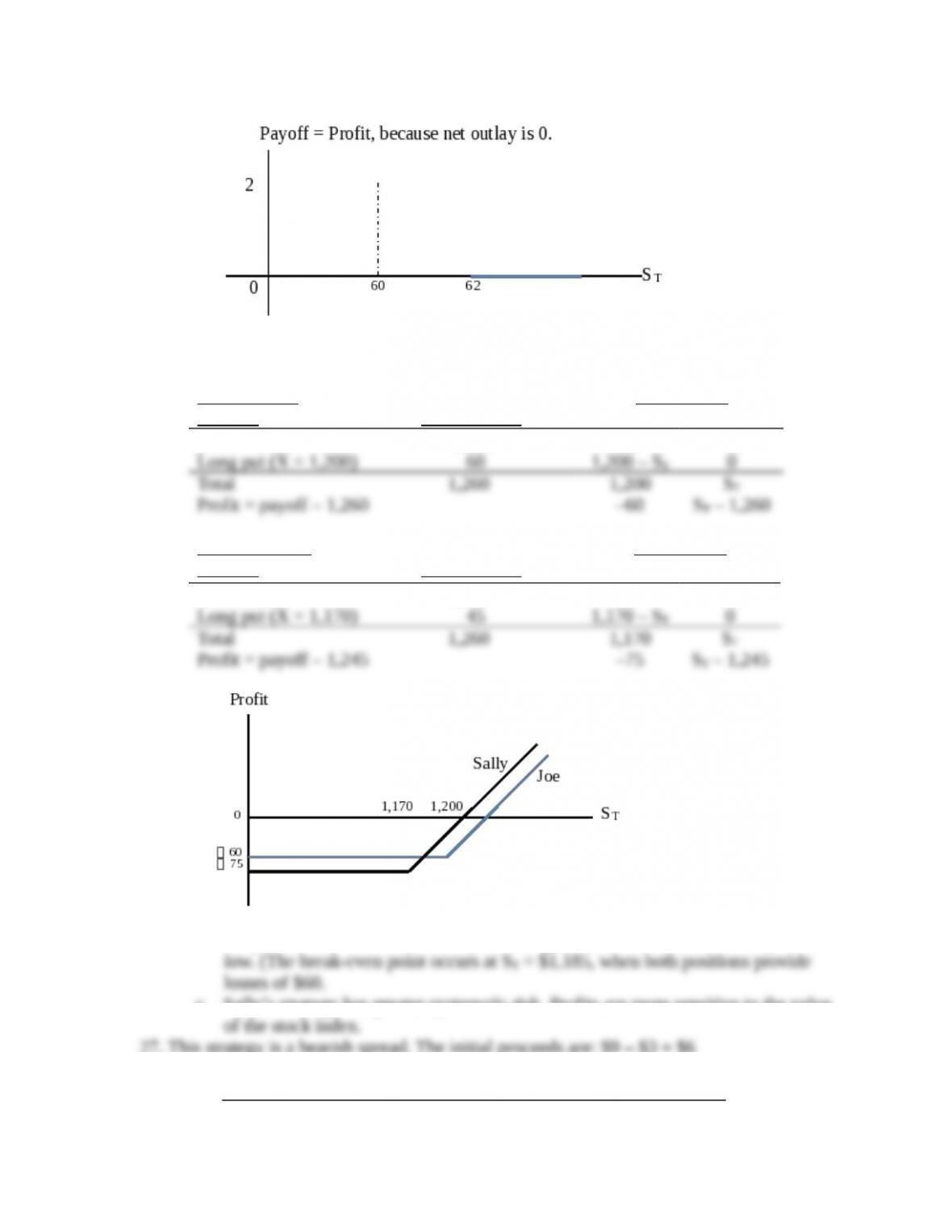

24. Buy the X = 62 put (which should cost more than it does) and write the X = 60 put.

Since the options have the same price, the net outlay is zero. The proceeds at maturity

will be between 0 and 2 and will never be negative.

Position ST < 60 60 < ST < 62 ST > 62

15-3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 – Options Markets

26.

a.

Joe’s strategy Final Payoff

Position Initial Outlay ST < 1200 ST > 1200

Stock index

1,200

ST

ST

1,260

ST

Stock index

1,200

ST

1,260

Chapter 15 – Options Markets

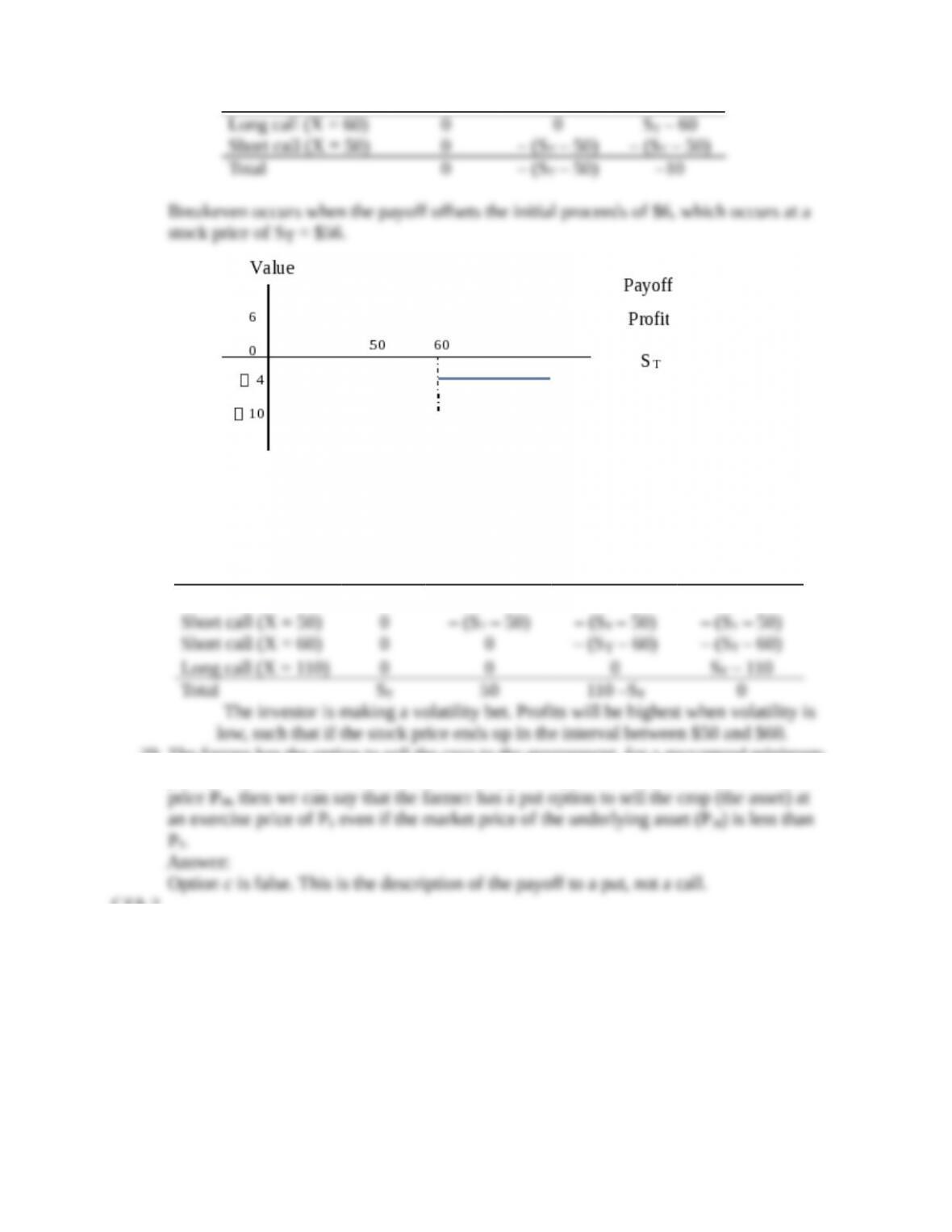

28. Buy a share of stock, write a call with X = 50, write a call with X = 60, and buy a call

with X = 110.

Position ST < 50 50 < ST < 60 60 < ST < 110 ST > 110

Buy stock STSTSTST

29. The farmer has the option to sell the crop to the government, for a guaranteed minimum

price, if the market price is too low. If the supported price is denoted PS and the market

CFA 2

Answer:

15-5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 – Options Markets

a. Donie should choose the long strangle strategy. A long strangle option strategy

consists of buying a put and a call with the same expiration date and the same

underlying asset, but different exercise prices. In a strangle strategy, the call has

b. i. The maximum possible loss per share is $9.00, which is the total cost of the

ii. The maximum possible gain is unlimited if the stock price keeps moving

iii. The breakeven prices are $46.00 and $69.00. The put will just cover costs if

CFA 3

Answer:

a. If an investor buys a call option and writes a put option on a T-bond, then, at

maturity, the total payoff to the position is (ST – X), where ST is the price of the

b. Such a position would increase the portfolio duration, just as adding a T-bond

c. Futures can be bought and sold very cheaply and quickly. They give the manager

CFA 4

Answer:

a. Conversion value of a convertible bond is the value of the security if it is

b. Market conversion price is the price that an investor effectively pays for the

common stock if the convertible bond is purchased:

15-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 – Options Markets

Market conversion price = market price of the convertible bond/conversion ratio

CFA 5

Answer:

a. i. The current market conversion price is computed as follows:

Market conversion price = market price of the convertible bond/conversion ratio

ii. The expected one-year return for the Ytel convertible bond is:

iii. The expected one-year return for the Ytel common equity is:

b. The two components of a convertible bond’s value are:

i. In response to the increase in Ytel’s common equity price, the straight bond value

should stay the same and the option value should increase.

ii. In response to the increase in interest rates, the straight bond value should

decrease and the option value should increase.

15-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.