Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 15 - Options Markets

CHAPTER 15

15-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 - Options Markets

OPTIONS MARKETS

1. Options provide numerous opportunities to modify the risk profile of a portfolio. The

simplest example of an option strategy that increases risk is investing in an ‘all options’

portfolio of at-the-money options (as illustrated in the text). The leverage provided by

2. Options at the money have the highest time premium and thus the highest potential for

gain. Since the highest potential gain is at the money, the logical conclusion is that they

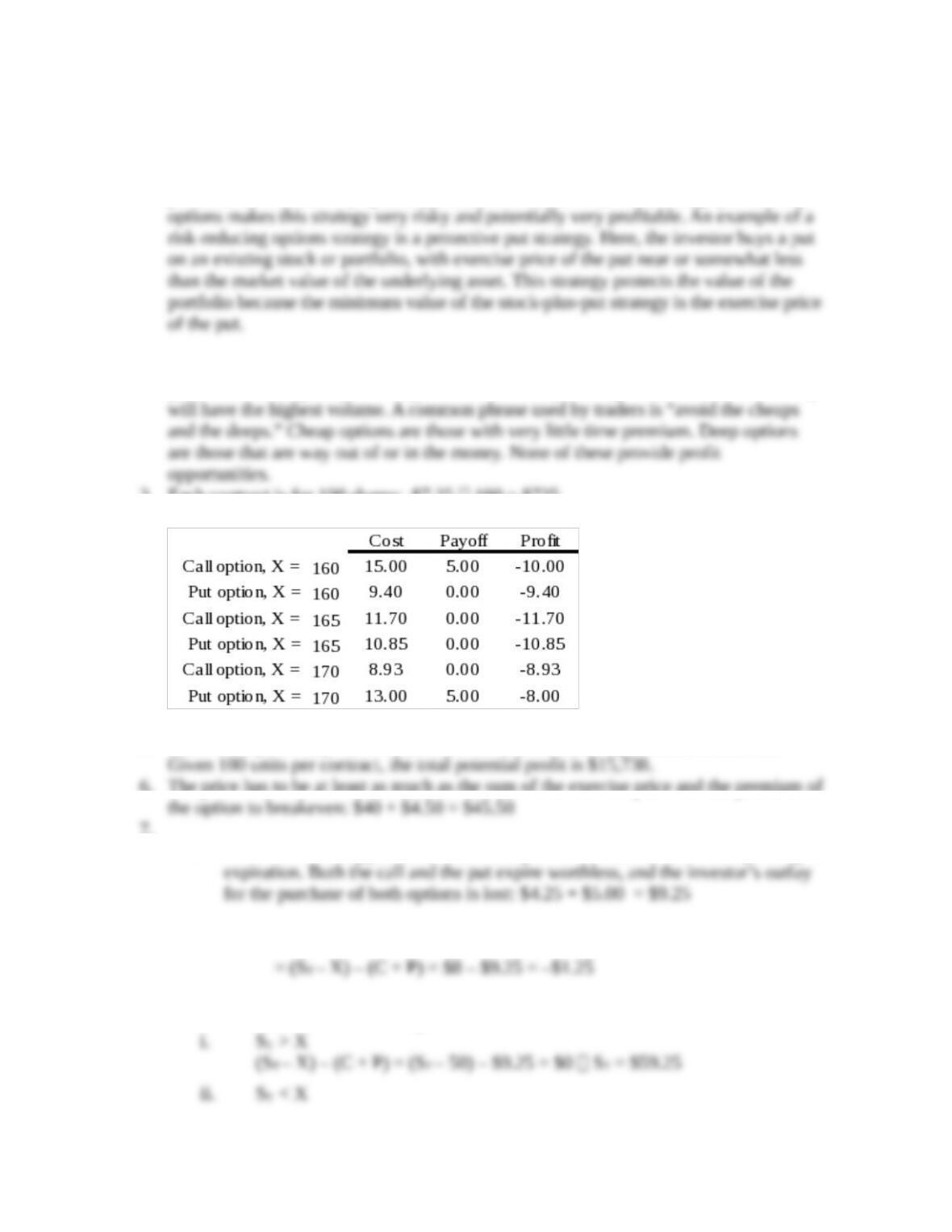

3. Each contract is for 100 shares: $7.25 100 = $725

4.

5. If the stock price drops to zero, you will make $160 – $2.62 per stock, or $157.38.

6. The price has to be at least as much as the sum of the exercise price and the premium of

7.

a. Maximum loss happens when the stock price is the same to the strike price upon

b. Loss: Final value – Original investment

c. There are two break even prices:

15-2

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 - Options Markets

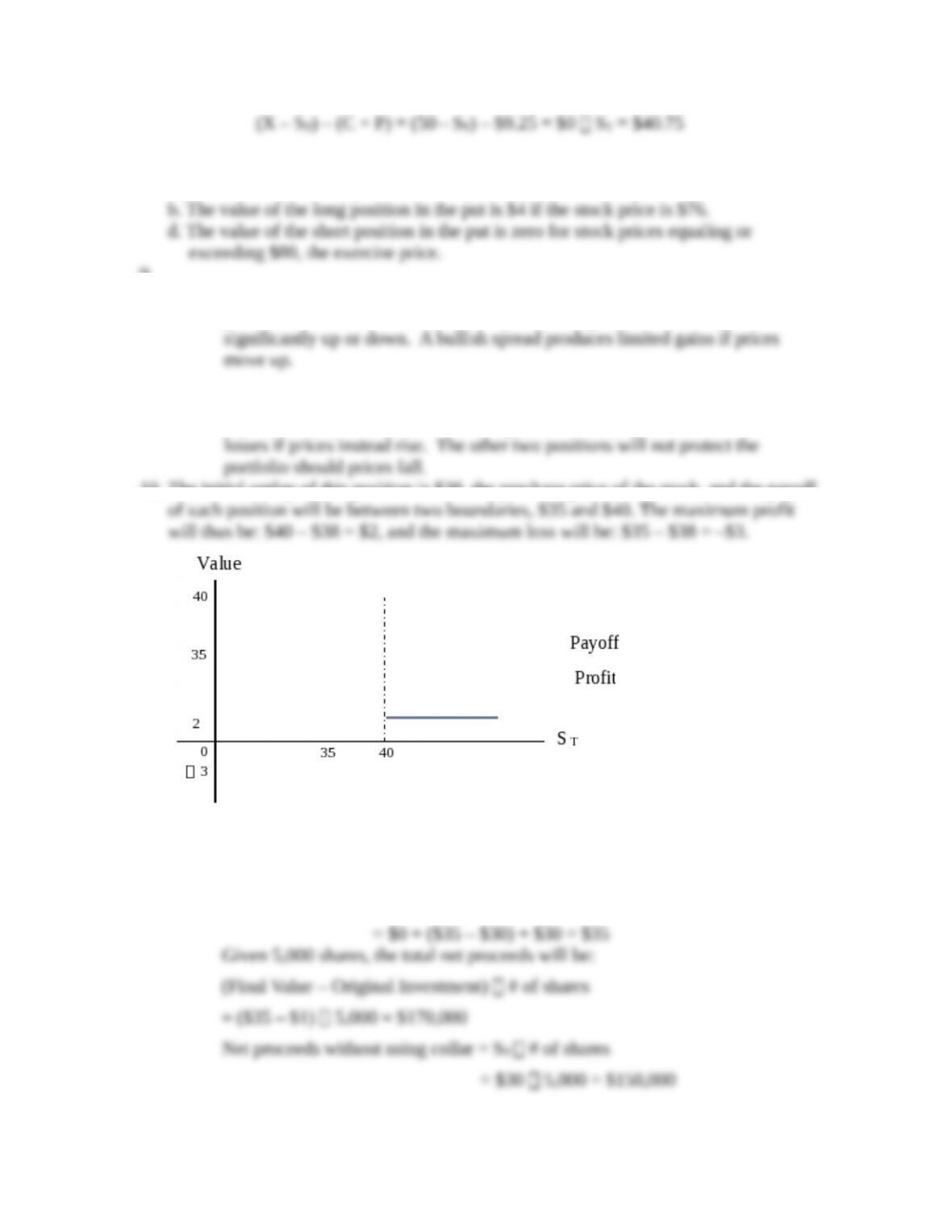

8. Option c is the only correct statement.

a. The value of the short position in the put is –$4 if the stock price is $76.

9.

a. i. A long straddle produces gains if prices move up or down and limited losses if

prices do not move. A short straddle produces significant losses if prices move

b. i. Long put positions gain when stock prices fall and produce very limited losses

if prices instead rise. Short calls also gain when stock prices fall but create

10. The initial outlay of this position is $38, the purchase price of the stock, and the payoff

11. The collar involves purchasing a put for $3 and selling a call for $2. The initial outlay is

$1.

a. ST = $30

Value at expiration = Value of call + Value of put + Value of stock

15-3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 - Options Markets

b. ST = $40

Value at expiration = Value of call + Value of put + Value of stock

= 0 + 0 + $40 = $40

c. ST = $50

Value at expiration = Value of call + Value of put + Value of stock

= ($45 – $50) + 0 + $50 =$45

With the initial outlay of $1, the collar locks the net proceeds per share in between the

lower bound of $34 and the upper bound of $44. Given 5,000 shares, the total net

12. In terms of dollar returns:

Price of Stock Six Months from Now

Stock price:

$80

$100

$110

$120

a. All stocks (100 shares)

8,000

10,000

11,000

12,000

In terms of rate of return, based on a $10,000 investment:

Price of Stock Six Months from Now

Stock price:

$80

$100

$110

$120

a. All stocks (100 shares)

–20%

0%

10%

20%

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 - Options Markets

0 20 40 60 80 100 120 140

-150%

-100%

-50%

0%

50%

100%

150%

a. All stocks (100 shares) b. All options (1,000 shares) c. Bills + 100 options

13.

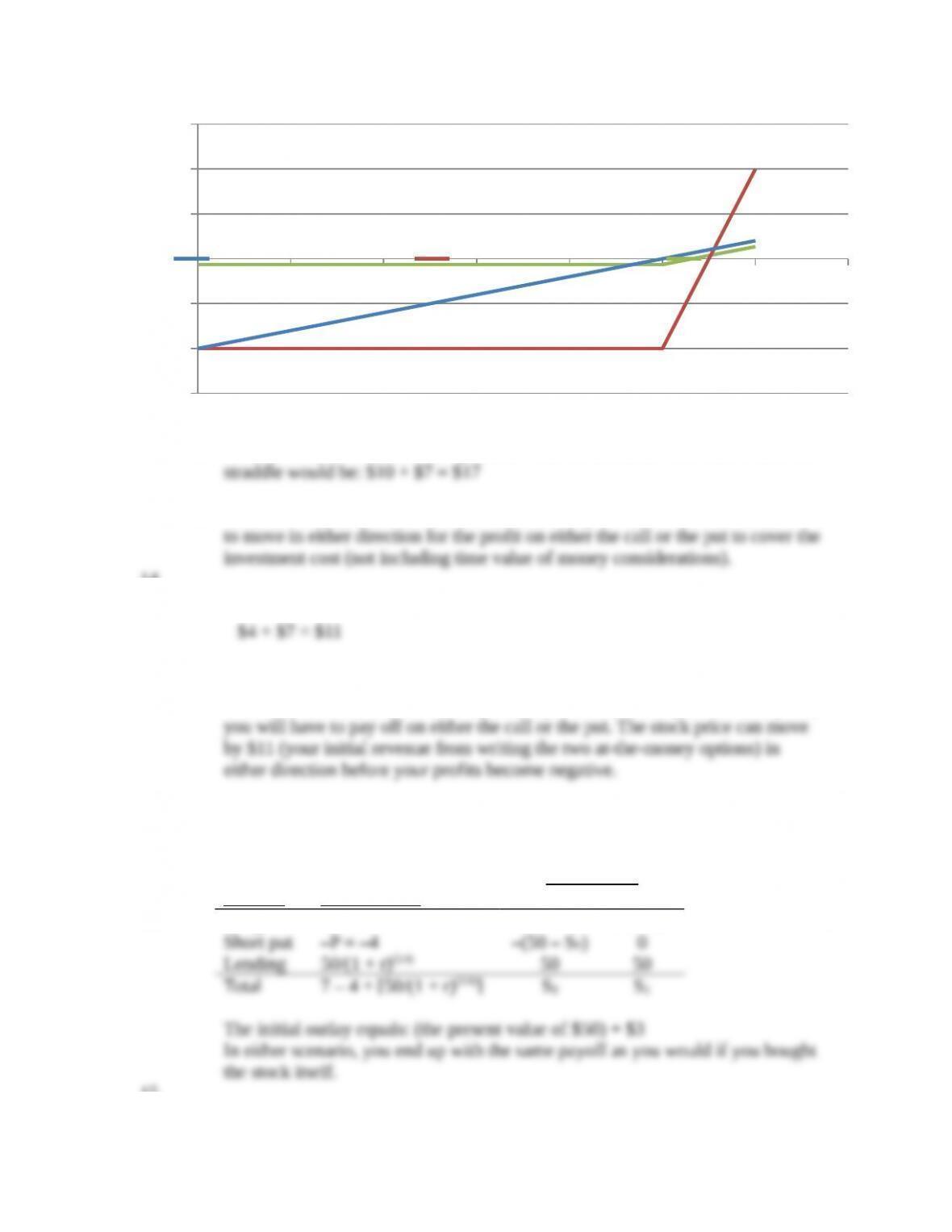

a. Purchase a straddle, i.e., both a put and a call on the stock. The total cost of the

b. Since the straddle costs $17, this is the amount by which the stock would have

14.

a. Sell a straddle, i.e., sell a call and a put to realize premium income of:

b. If the stock ends up at $50, both of the options will be worthless and the profit

will be $11. This is the maximum possible profit since, at any other stock price,

c. Buy the call, sell (write) the put, lend the present value of $50. The payoff is as

follows:

Final Payoff

Position Initial Outlay ST < X ST > X

Long call

C = 7

0

ST – 50

15.

15-5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 - Options Markets

a. By writing covered call options, Jones receives premium income of $30,000. If,

in January, the price of the stock is less than or equal to $45, he will keep the

stock plus the premium income. Since the stock will be called away from him if

its price exceeds $45 per share, the most he can have is:

(We are ignoring interest earned on the premium income from writing the option

over this short time period.) The payoff structure is:

Stock Price PortfolioValue

Less than $45 (10,000 times stock price) + $30,000

Greater than $45 $450,000 + $30,000 = $480,000

This strategy offers some premium income but leaves the investor with

b. By buying put options with a $35 strike price, Jones will be paying $30,000 in

premiums in order to insure a minimum level for the final value of his position.

This strategy allows for upside gain, but exposes Jones to the possibility of a

moderate loss equal to the cost of the puts. The payoff structure is:

Stock Price Portfolio Value

c. The net cost of the collar is zero. The value of the portfolio will be as follows:

Stock Price Portfolio Value

Less than $35 $350,000

The best strategy in this case is (c) since it satisfies the two requirements of

preserving the $350,000 in principal while offering a chance of getting $450,000.

Strategy (a) should be ruled out because it leaves Jones exposed to the risk of

substantial loss of principal.

Our ranking is: (1) c (2) b (3) a

15-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 - Options Markets

16.

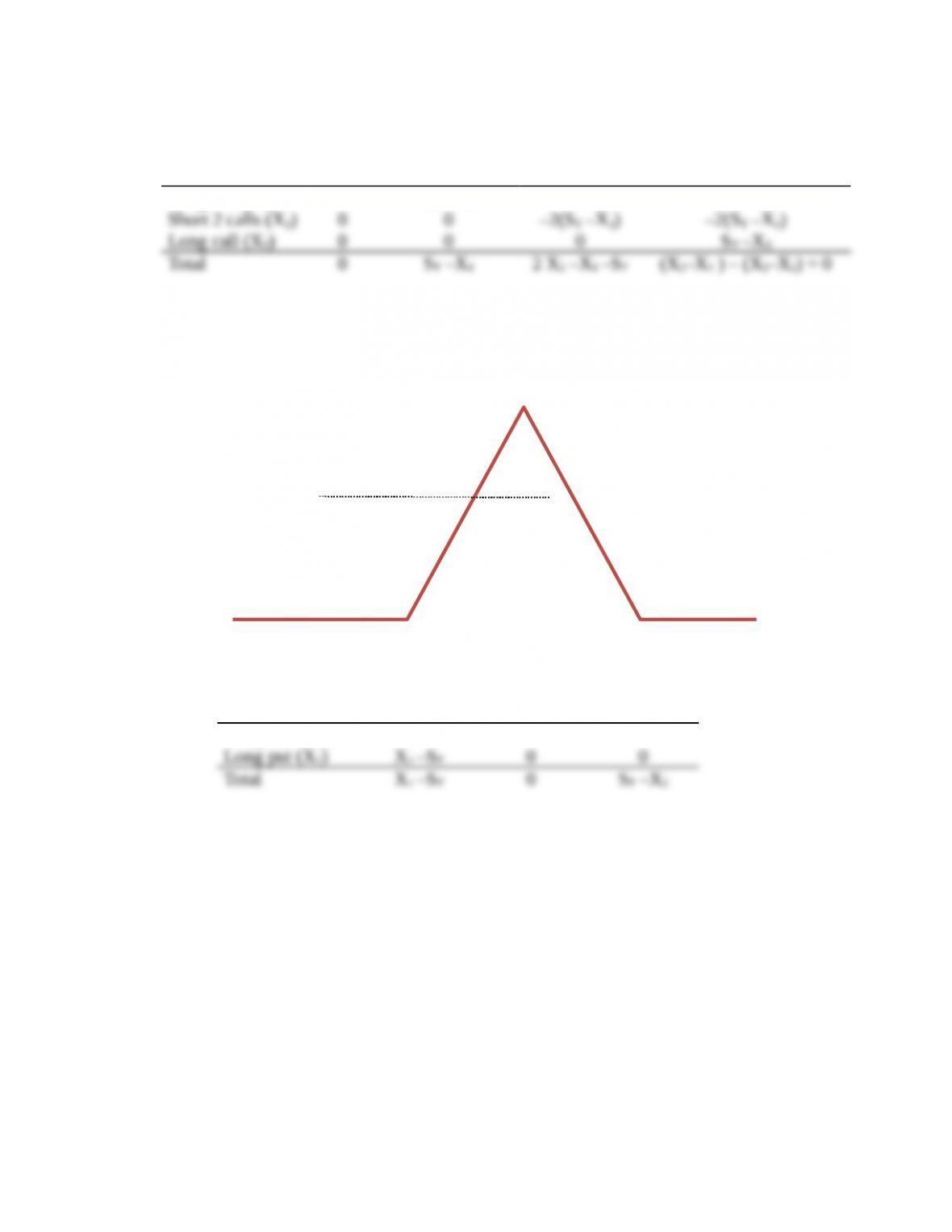

a. Butterfly Spread

Position ST < X1X1 < ST < X2X2 < ST < X3X3 < ST

Long call (X1) 0 ST –X1ST –X1ST –X1

Payof

b. Vertical combination

Position ST < X1X1 < ST < X2ST > X2

Long call (X2) 0 0 ST –X2

15-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 - Options Markets

Payof

17. Bearish spread

Position ST < X1X1 < ST < X2ST > X2

Long call (X2) 0 0 ST –X2

Payof

In the bullish spread, the payoff either increases or is unaffected by stock price

increases. In the bearish spread, the payoff either increases or is unaffected by stock

price decreases.

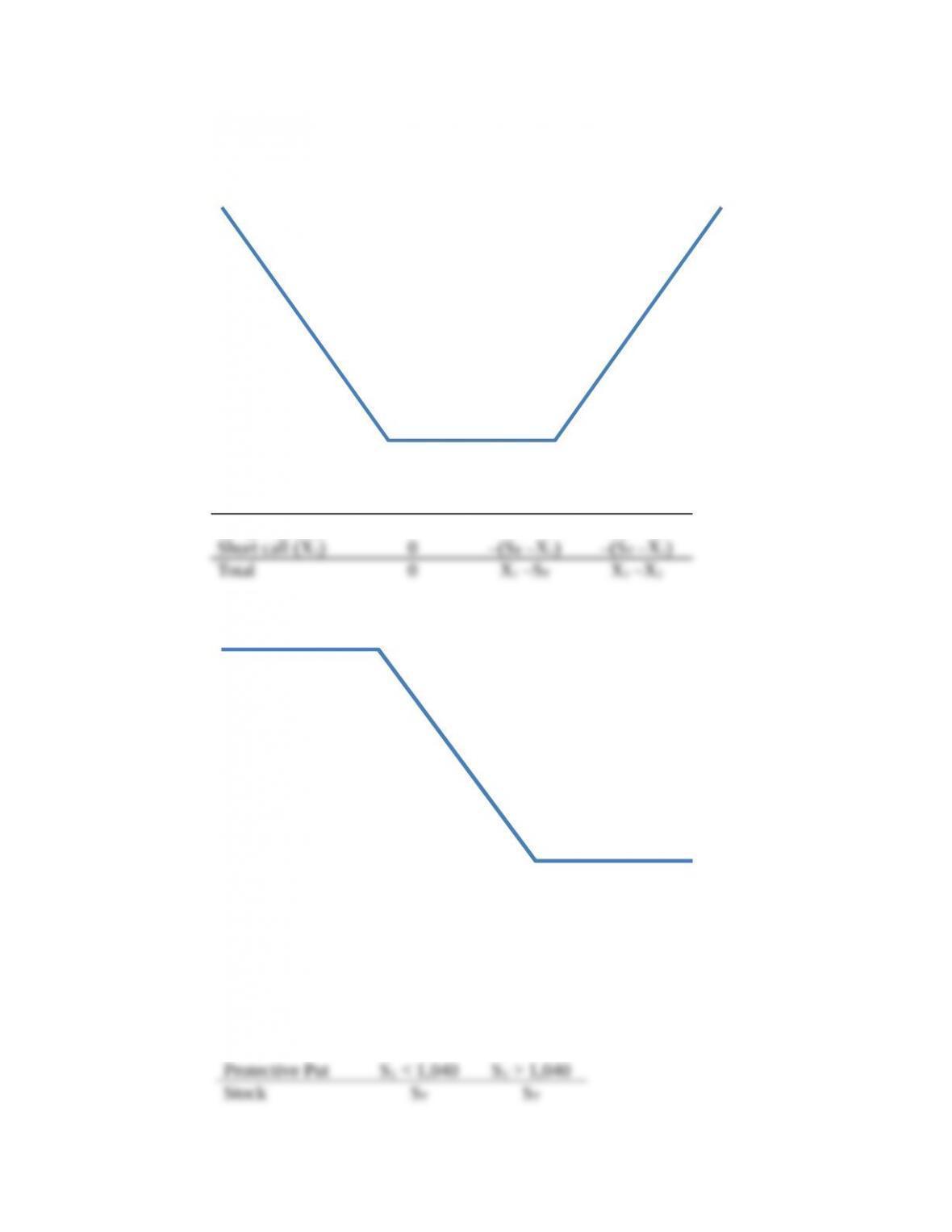

18.

a. Strategy one: Protective put

15-8

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 - Options Markets

Put 1,040 – ST0

Total 1,040 ST

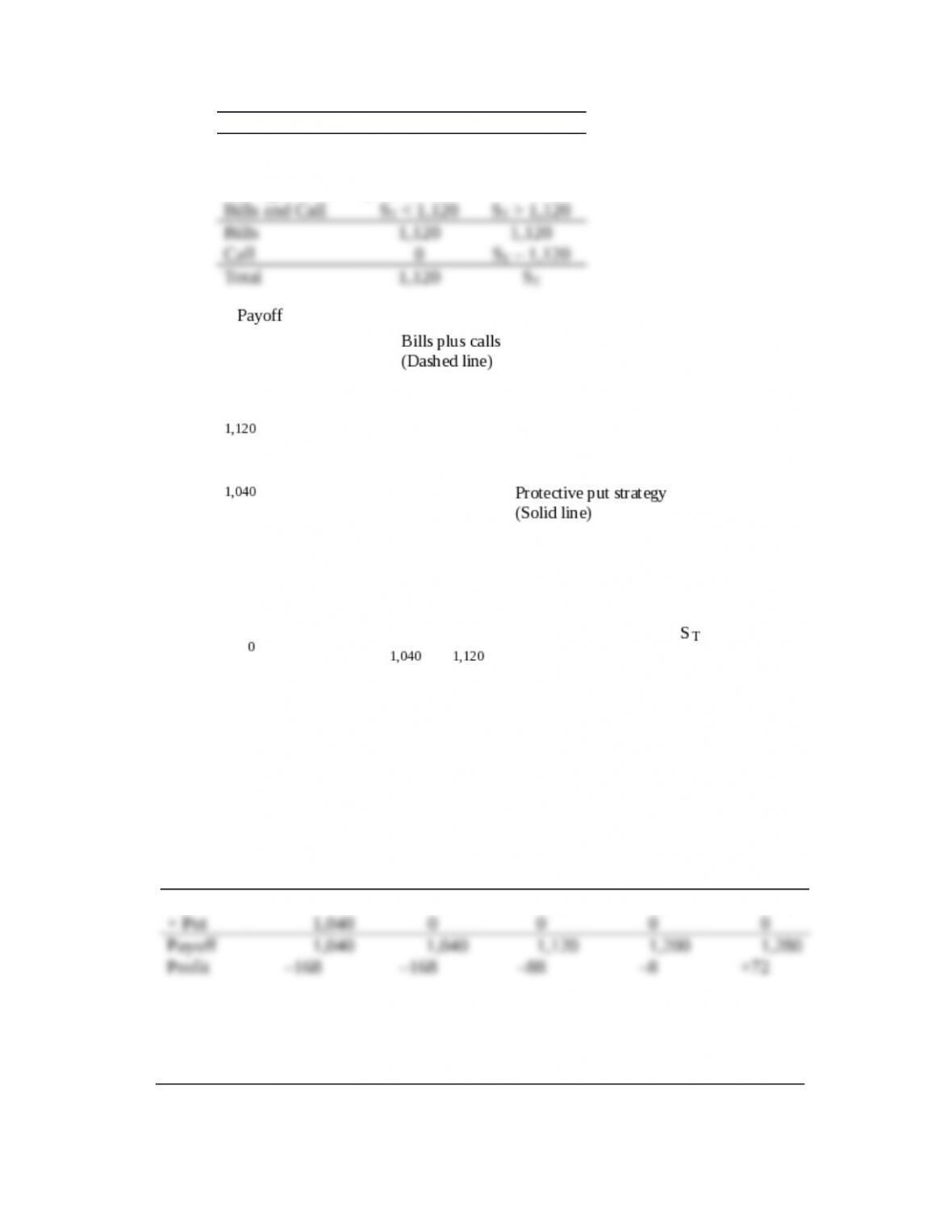

Strategy two: Bills plus calls

b. The bills plus call strategy has a greater payoff for some values of ST and never

a lower payoff. Since its payoffs are always at least as attractive and sometimes

greater, it must be more costly to purchase.

c. The initial cost of the stock plus put position is $1,208 and the cost of the bills plus

call position is $1,240.

Strategy one: Protective put

Position ST = 0 ST = 1,040 ST = 1,120 ST = 1,200 ST = 1,280

Stock 0 1,040 1,120 1,200 1,280

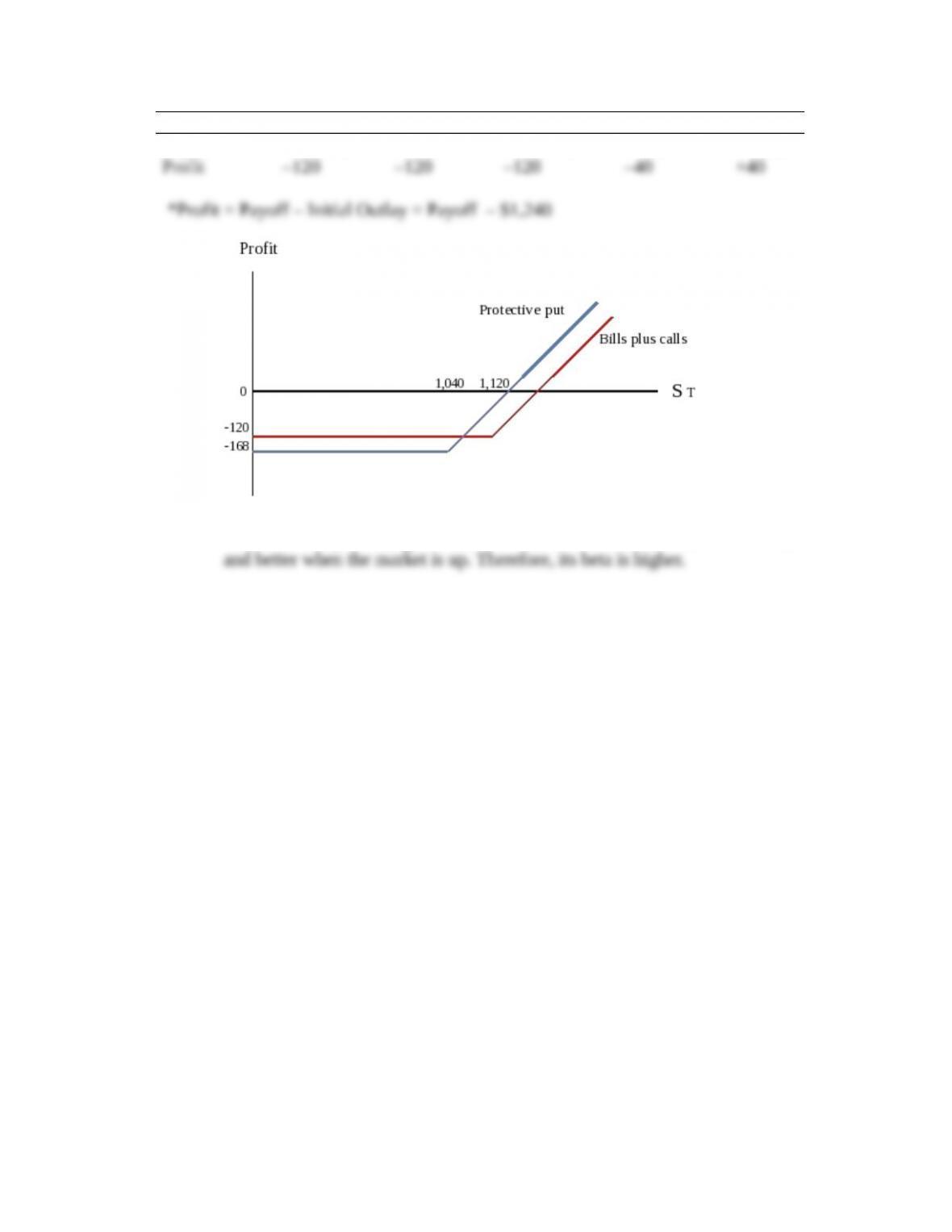

*Profit = Payoff – Initial Outlay = Payoff – $1,208

Strategy two: Bills plus calls

Position ST = 0 ST = 1,040 ST = 1,120 ST = 1,200 ST = 1,280

Bill 1,120 1,120 1,120 1,120 1,120

15-9

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 - Options Markets

+ Call 0 0 0 80 160

Payoff 1,120 1,120 1,120 1,200 1,280

d. The stock and put strategy is riskier. It does worse when the market is down,

15-10

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.