Chapter 13 – Equity Valuation

CFA 1

Answer:

a. This director is confused. In the context of the constant growth model, it is true

b. i. An increase in dividend payout reduces the sustainable growth rate as fewer

funds are reinvested in the firm.

CFA 2

Answer:

a. It is true that NewSoft sells at higher multiples of earnings and book value than

Capital. But this difference may be justified by NewSoft’s higher expected

b. The most important weakness of the constant-growth dividend discount model in

c. NewSoft should be valued using a multi-stage DDM, which allows for rapid

CFA 3

Answer:

a. The industry’s estimated P/E can be computed using the following model:

P0/E1 = payout ratio/(r g)

Therefore:

13-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 13 – Equity Valuation

b.

i. Forecast growth in real GDP would cause P/E ratios to be

ii. Government bond yield would cause P/E ratios to be generally

iii. Equity risk premium would cause P/E ratios to be generally

CFA 4

Answer:

a. k = rf + β [E(rM) – rf ] = 0.045 + 1.15 (0.145 0.045) = 0.16 or 16%

b.

Year Dividends

2010 $1.72

Present value of dividends paid in years 2011 to 2013:

Year PV of Dividends

2011 $1.93/1.16 = $1.66

c. The table presented in the problem indicates that QuickBrush is selling below

intrinsic value, while we have just shown that SmileWhite is selling somewhat

13-2

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 13 – Equity Valuation

b. Strengths of two-stage DDM compared to constant growth DDM:

The two-stage model allows for separate valuation of two distinct periods in

The two-stage model allows for an initial period of above-sustainable

A weakness of all DDMs is that they are all very sensitive to input values.

CFA 5

Answer:

a. The value of a share of Rio National equity using the Gordon growth model and

the capital asset pricing model is $22.40, as shown below.

Chapter 13 – Equity Valuation

ii. Add net borrowing: CFO does not take into account the amount of

capital supplied to the firm by lenders (e.g., bondholders). The new

borrowings, net of debt repayment, are cash flows available to equity holders

Note 2: A piece of equipment that was originally purchased for $10 million was

sold for $7 million at year-end, when it had a net book value of $3 million.

Note 3: The decrease in long-term debt represents an unscheduled principal

repayment; there was no new borrowing during the year.

Adjustment: Negative $5 million

Note 4: On 1 January 2012, the company received cash from issuing 400,000

No adjustment

Note 5: A new appraisal during the year increased the estimated market value of

land held for investment by $2 million, which was not recognized in 2012

income.

No adjustment

13-4

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 13 – Equity Valuation

Million $ Explanation

NI = $30.16 From Table 13.6

NCC = +$67.17 $71.17 (depreciation and amortization from Table 13.6)

– $4.00* (gain on sale from Note 2)

FCINV = –$68.00 $75.00 (capital expenditures from Note 1)

– $7.00* (cash on sale from Note 2)

WCINV = –$24.00 –$3.00 (increase in accounts receivable from Table 13.5) +

–$20.00 (increase in inventory from Table 13.5) +

–$1.00 (decrease in accounts payable from Table 13.5)

Net Borrowing = +(–$5.00) –$5.00 (decrease in long-term debt from Table 13.5)

FCFE = $0.33

*Supplemental Note 2 in Table 13.7 affects both NCC and FCINV

CFA 7

Answer:

Rio National

Industry

CFA 8

Answer:

Using a two-stage dividend discount model, the current value of a share of Sundanci is

calculated as follows:

2

3

2

2

1

1

0

)k1(

)gk(

D

)k1(

D

)k1(

D

V

13-5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 13 – Equity Valuation

98.43$

14.1

)13.014.0(

5623.0$

14.1

4976.0$

14.1

3770.0$

221

where:

E0 = $0.952

D0 = $0.286

E1 = E0 (1.32)1 = $0.952 1.32 = $1.2566

D1 = E1 0.30 = $1.2566 0.30 = $0.3770

E2 = E0 (1.32)2 = $0.952 (1.32)2 = $1.6588

D2 = E2 0.30 = $1.6588 0.30 = $0.4976

E3 = E0 (1.32)2 1.13 = $0.952 (1.32)3 1.13 = $1.8744

D3 = E3 0.30 = $1.8744 0.30 = $0.5623

CFA 9

Answer:

a. Free cash flow to equity (FCFE) is defined as the cash flow remaining after

meeting all financial obligations (including debt payment) and after covering

capital expenditure and working capital needs. The FCFE is a measure of how

much the firm can afford to pay out as dividends, but in a given year may be

more or less than the amount actually paid out.

b. The FCFE model requires forecasts of FCFE for the high growth years (2014

and 2015) plus a forecast for the first year of stable growth (2016) in order to

13-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 13 – Equity Valuation

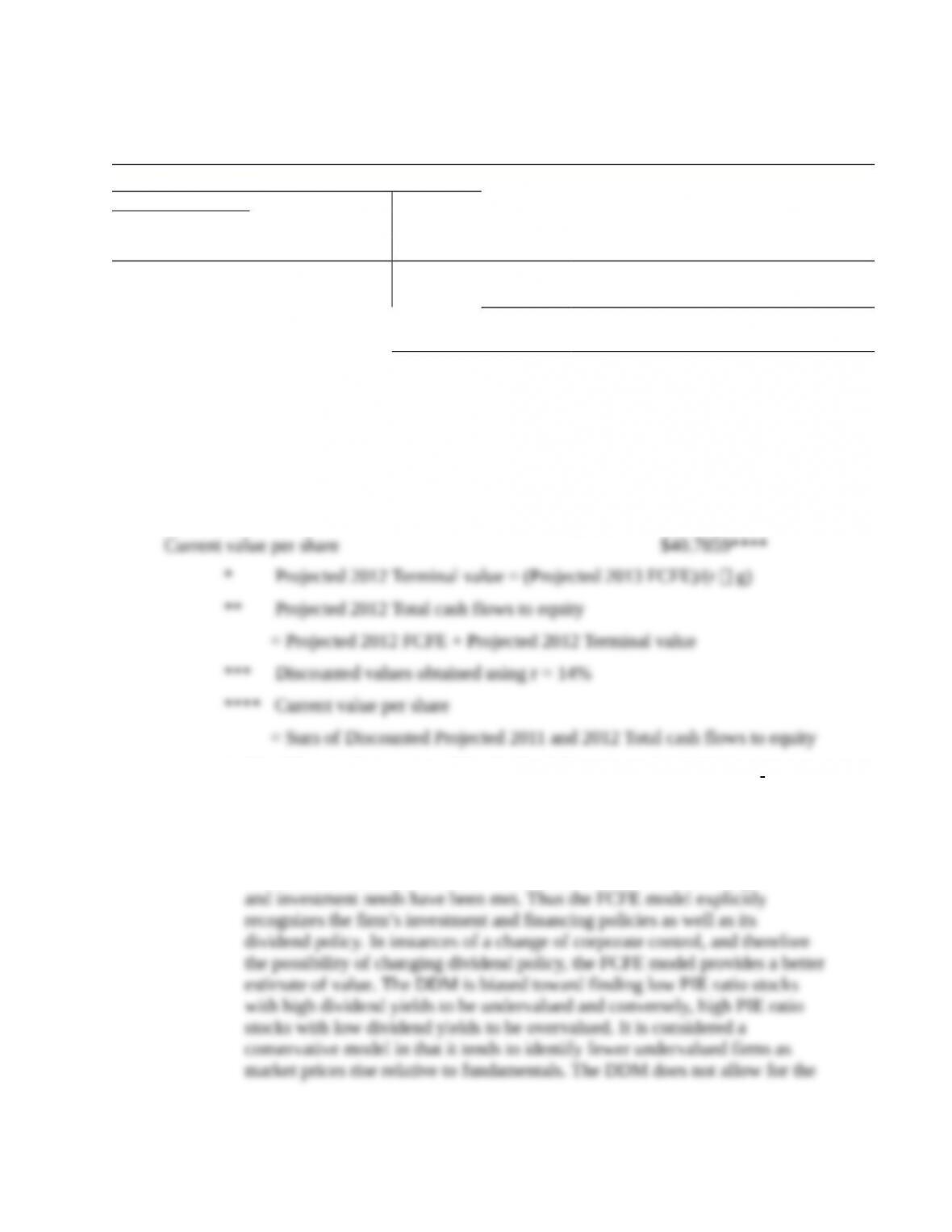

The following table shows the process for estimating Sundanci’s current value

on a per share basis:

Free Cash Flow to Equity

Base Assumptions

Shares outstanding: 84 millions

Required return on equity (r): 14%

Actual

2013

Projected

2014

Projected

2015

Projected

2016

Growth rate (g) 27% 27% 13%

Total Per share

Earnings after tax $80 $0.952 $1.2090 $1.5355 $1.7351

Plus: Depreciation expense $23 $0.274 $0.3480 $0.4419 $0.4994

Less: Capital expenditures $38 $0.452 $0.5740 $0.7290 $0.8238

Less: Increase in net working capital $41 $0.488 $0.6198 $0.7871 $0.8894

Equals: FCFE $24 $0.286 $0.3632 $0.4613 $0.5213

Terminal value $52.1300*

Total cash flows to equity $0.3632 $52.5913**

Discounted value $0.3186*** $40.4673***

c. i. The following limitations of the dividend discount model (DDM) are

addressed by the FCFE model. The DDM uses a strict definition of cash

flows to equity, i.e. the expected dividends on the common stock. In fact,

taken to its extreme, the DDM cannot be used to estimate the value of a stock

that pays no dividends. The FCFE model expands the definition of cash flows

to include the balance of residual cash flows after all financial obligations

13-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 13 – Equity Valuation

ii. The following limitations of the DDM are not addressed by the FCFE model.

Both two-stage valuation models allow for two distinct phases of growth, an

initial finite period where the growth rate is abnormal, followed by a stable

CFA 11

Answer:

a. The formula for calculating a price earnings ratio (P/E) for a stable growth firm

is the dividend payout ratio divided by the difference between the required rate

of return and the growth rate of dividends. If the P/E is calculated based on

trailing earnings (year 0), the payout ratio is increased by the growth rate. If the

P/E is calculated based on next year’s earnings (year 1), the numerator is the

payout ratio.

b. The P/E ratio is a decreasing function of riskiness; as risk increases the P/E ratio

decreases. Increases in the riskiness of Sundanci stock would be expected to

lower the P/E ratio.

13-8

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 13 – Equity Valuation

13-9

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.