Chapter 12 – Macroeconomic and Industry Analysis

CHAPTER 12

12-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 12 – Macroeconomic and Industry Analysis

MACROECONOMIC AND INDUSTRY ANALYSIS

1. A top-down approach to security valuation begins with an analysis of the global and

domestic economy. Analysts who follow a top-down approach then narrow their

attention to an industry or sector likely to perform well, given the expected

performance of the broader economy. Finally, the analysis focuses on specific

companies within an industry or sector that has been identified as likely to perform

2. The yield curve, by definition, incorporates future interest rates. As such, it reflects

3. c. A defensive firm.Defensive firms and industries have below-average sensitivity to

4. It would be considered a supply shock which affects production capacity and costs.

5.

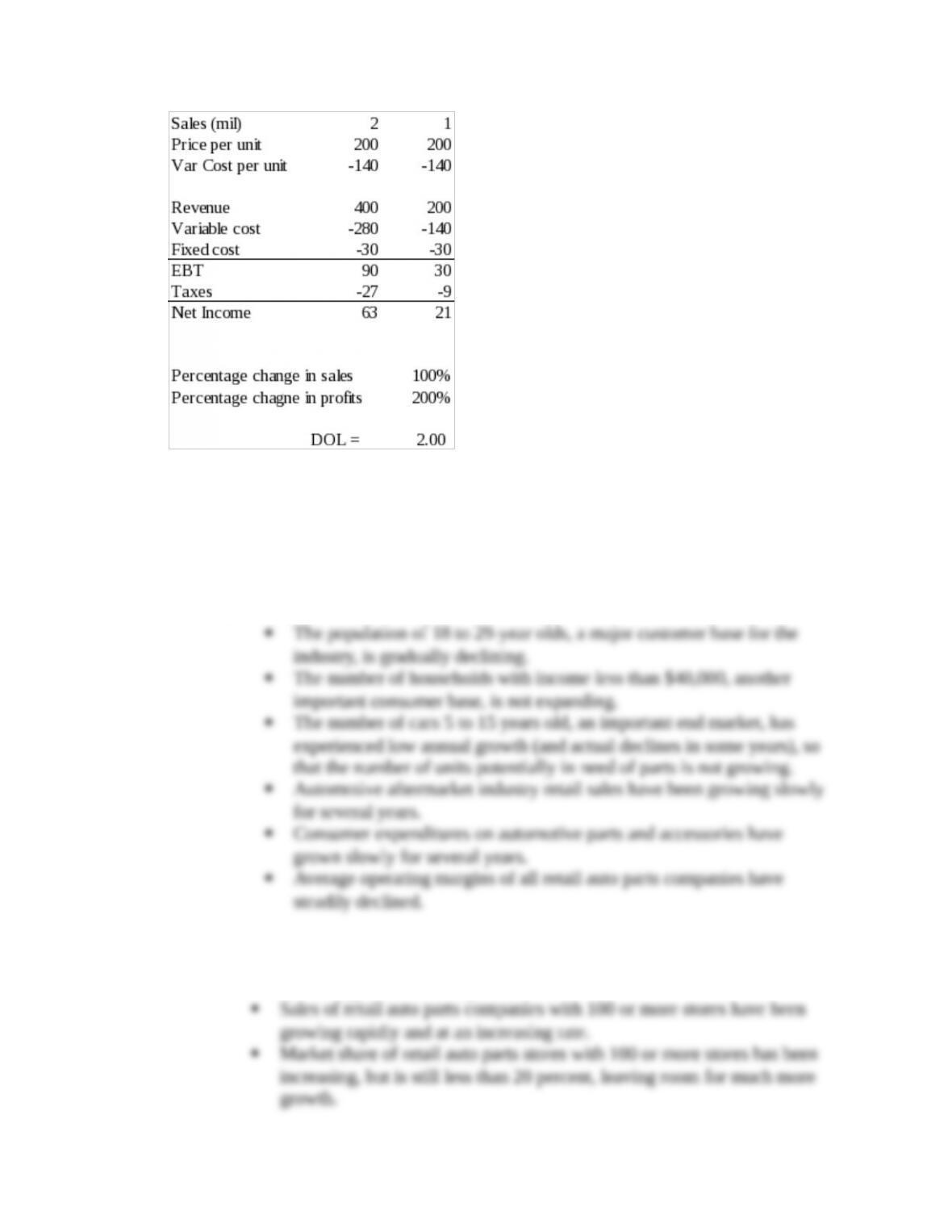

a. Financial leverage increases the sensitivity of profits in the business cycle

b. Firms with high fixed costs are said to have high operating leverage.As small

6. d.Asset play. Some of the valuable assets of the company are not currently reflected

in the present value.

7. A peak is the transition from the end of an expansion to the start of a contraction. A

8. a. Monetary policy is expansive and fiscal policy is expansive. This is consistent

9. a. A redistributive tax system is a demand-side management approach.

12-2

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 12 – Macroeconomic and Industry Analysis

10. Companies tend to pay very low, if any, dividends early in their business life cycle

11. 1+ Real Interest Rate =

1+ Nominal Interest Rate

1+ Inflation Rate

Fixed Costs

Chapter 12 – Macroeconomic and Industry Analysis

a. General Autos. Pharmaceutical purchases are less discretionary than automobile

purchases.

b. Friendly Airlines. Travel expenditures are more sensitive to the business cycle

than movie consumption.

a. Oil well equipment Decline (environmental pressures, decline

in easily-developed oil fields)

b. Computer hardware Consolidation stage

20. The index of consumer expectations is a useful leading economic indicator because,

21. Labor cost per unit of output is a lagging indicator because wages typically start

22.

a. Because of the very short average maturity (30 days), the rate of return on the

b. If you are relatively neutral on rates, the one-year CD might be a reasonable

c. The long-term bond is the best choice for an investor who wants to speculate on

a decrease in rates.

23. The expiration of the patent means that General Weedkillers will soon face

considerably greater competition from its competitors. We would expect prices and

24. Equity prices are positively correlated with job creation or longer work weeks, as

12-4

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 12 – Macroeconomic and Industry Analysis

25. a. Stock prices are one of the leading indicators. One possible explanation is that

stock prices anticipate future interest rates, corporate earnings and dividends.

26. a. Industrial production is a coincident indicator; the others are leading.

27. a. Foreign exchange rates can significantly affect the competitiveness and

28. Determinants of buyer power include buyer concentration, buyer volume, buyer

information, available substitutes, switching costs, brand identity, and product

29. a. Product differentiation can be based on the product itself, the method of delivery,

30. A firm with a strategic planning process not guided by their generic competitive

1. The strategic plan is a list of unrelated action items that does not lead to a sustainable

competitive advantage.

33.

12-5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 12 – Macroeconomic and Industry Analysis

If the economy enters a recession, the firm will have $21 million after-tax profit.

CFA 1

Answer:

a. Relevant data items from the table that support the conclusion that the retail

auto parts industry as a whole is in the maturity phase of the industry life cycle

are:

b. Relevant items of data from the table that support the conclusion that Wigwam

Autoparts Heaven, Inc. (WAH) and its major competitors are in the

consolidation stage of their life cycle are:

12-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 12 – Macroeconomic and Industry Analysis

Because of industry fragmentation (i.e., most of the market share is distributed among

many companies with only a few stores), the retail auto parts industry apparently is

undergoing marketing innovation and consolidation. The industry is moving toward the

CFA 2

Answer:

a. The concept of an industrial life cycle refers to the tendency of most industries

to go through various stages of growth. The rate of growth, the competitive

environment, profit margins and pricing strategies tend to shift as an industry

moves from one stage to the next, although it is difficult to pinpoint exactly

when one stage has ended and the next begun.

The start-up stage is characterized by perceptions of a large potential market and

by high optimism for potential profits. In this stage, however, there is usually a

high failure rate. In the second stage, often called rapid growth or consolidation,

Product pricing, profitability, and industry competitive structure often vary by

phase. Thus, for example, the first phase usually encompasses high product

prices, high costs (R&D, marketing, etc.) and a (temporary) monopolistic

12-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 12 – Macroeconomic and Industry Analysis

b. The passenger car business in the United States has probably entered the final

stage in the industrial life cycle because normalized growth is quite low. The

c. Cars: In the final phases of the life cycle, demand tends to be price sensitive.

Thus, Universal can not raise prices without losing volume. Moreover, given the

Idata:Idata should have much more pricing flexibility given that it is in an

earlier phase of the industrial life cycle. Demand is growing faster than supply,

CFA 3

Answer:

a. A basic premise of the business cycle approach to investing is that stock prices

anticipate fluctuations in the business cycle. For example, there is evidence that

stock prices tend to move about six months ahead of the economy.In fact, stock

prices are a leading indicator for the economy.

Over the course of a business cycle, this approach to investing would work

roughly as follows. As the top of a business cycle is perceived to be

Abnormal returns will generally be earned only if these asset allocation switches

are timed better than those of other investors. Switches made after the turning

points may not lead to excess returns.

b. Based on the business cycle approach to investment timing, the ideal time to

invest in a cyclical stock like a passenger car company would be just before the

12-8

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 12 – Macroeconomic and Industry Analysis

CFA 4

Answer:

a.

The industry-wide ROE is leveling off, indicating that the industry may be

approaching a later stage of the life cycle.

Average P/E ratios are declining, suggesting that investors are becoming less

b.

Industry growth rate is still forecast at 10 15%, higher than would be true

of a mature industry.

CFA 5

Answer:

a. (4) Government deficits are planned during the economic recessions, and

surpluses are utilized to restrain inflationary booms.

b. (2) Higher marginal tax rates promote economic inefficiency and thereby retard

12-9

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.