Chapter 11 – Managing Bond Portfolios

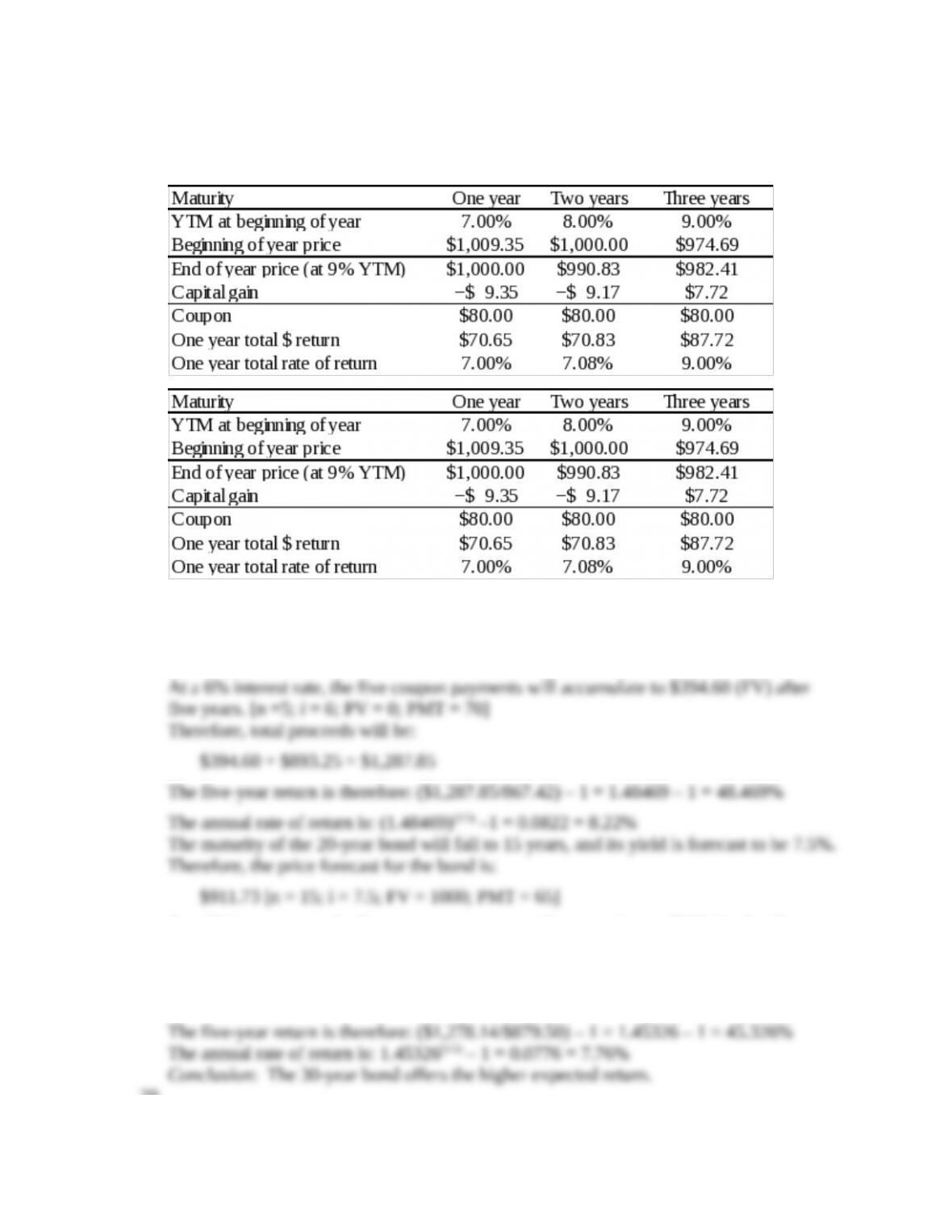

27. You should buy the three-year bond because it will offer a 9% holding-period return

over the next year, which is greater than the return on either of the other bonds, as

shown below:

28. The maturity of the 30-year bond will fall to 25 years, and the yield is forecast to be 8%.

Therefore, the price forecast for the bond is:

$893.25 [n = 25; i = 8; FV = 1,000; PMT = 70]

At a 6% interest rate, the five coupon payments will accumulate to $366.41 after five years.

[n=15; i = 6; PV = 0; PMT = 65]

Therefore, total proceeds will be:

$366.41 + $911.73 = $1,278.14

29.

11-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 11 – Managing Bond Portfolios

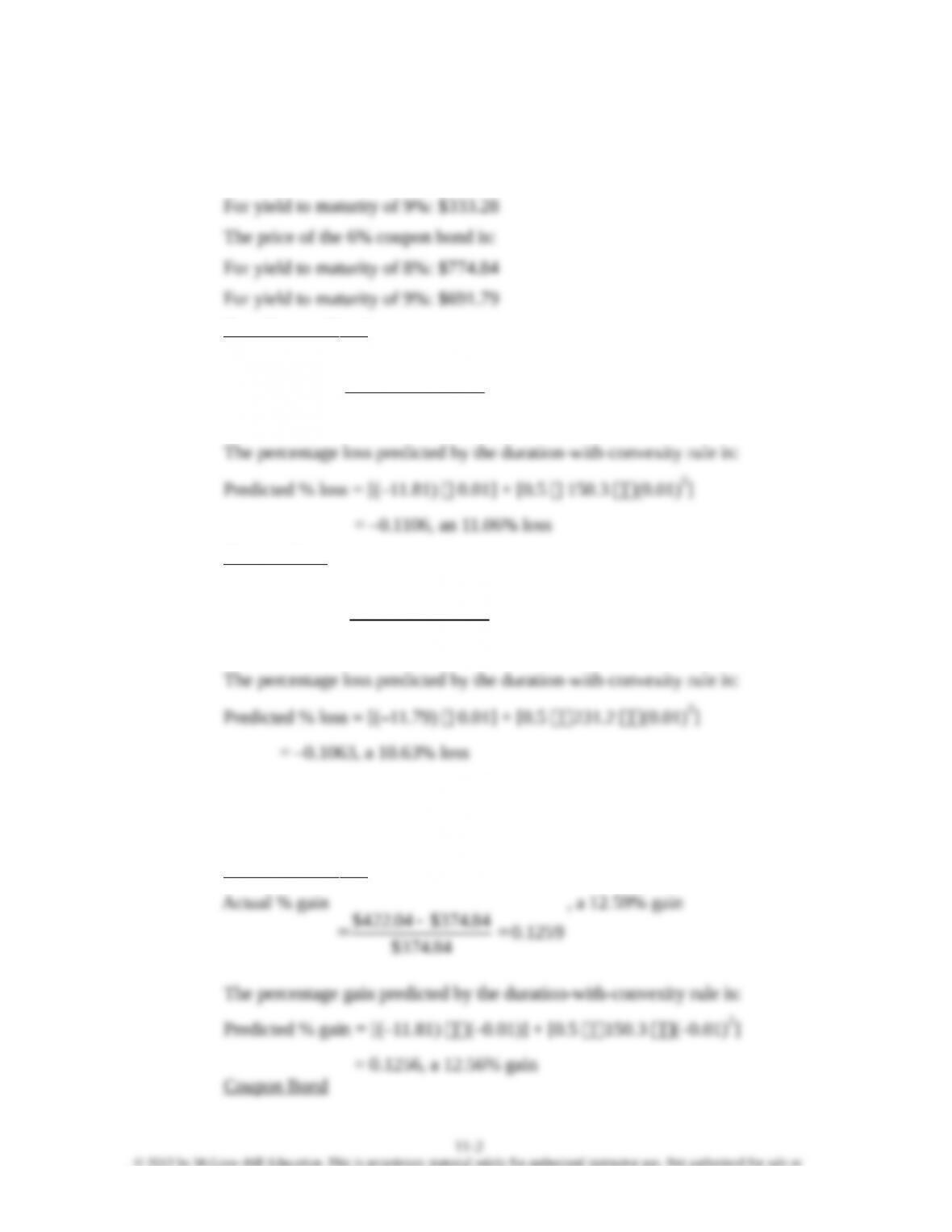

a. Using a financial calculator, we find that the price of the zero-coupon bond

(with $1000 face value) is:

For yield to maturity of 8%: $374.84

Zero C oupon B ond

Actual % loss

1109.0

84.374$

84.374$28.333$

, an 11.09% loss

Coupon B ond

Actual % loss

1072.0

84.774$

84.774$79.691$

, a 10.72% loss

b. Now assume yield to maturity falls to 7%. The price of the zero increases to

$422.04, and the price of the coupon bond increases to $875.91.

Zero C oupon B ond

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 11 – Managing Bond Portfolios

Actual % gain

1304.0

84.774$

84.774$91.875$

, a 13.04% gain

The percentage gain predicted by the duration-with-convexity rule is:

c. The 6% coupon bond (which has higher convexity) outperforms the zero

regardless of whether rates rise or fall. This is a general property which can be

understood by first noting from the duration-with-convexity formula that the

d. This situation cannot persist. No one would be willing to buy the lower

convexity bond if it always underperforms the other bond. The price of the

CFA 1

Answer:

C: Highest maturity, zero coupon

CFA 2

Answer:

a. Modified duration =

YTM1

durationMacaulay

If the Macaulay duration is 10 years and the yield to maturity is 8%, then the

modified duration is: 10/1.08 = 9.26 years

b. For option-free coupon bonds, modified duration is better than maturity as a

measure of the bond’s sensitivity to changes in interest rates. Maturity considers

only the final cash flow, while modified duration includes other factors such as

11-3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 11 – Managing Bond Portfolios

the size and timing of coupon payments and the level of interest rates (yield to

maturity). Modified duration, unlike maturity, tells us the approximate

proportional change in the bond price for a given change in yield to maturity.

c. i. Modified duration increases as the coupon decreases.

CFA 3

Answer:

a. Scenario (i): Strong economic recovery with rising inflation expectations.

Interest rates and bond yields will most likely rise, and the prices of both bonds

will fall. The probability that the callable bond will be called declines, so that it

Scenario (ii): Economic recession with reduced inflation expectations. Interest

rates and bond yields will most likely fall. The callable bond is likely to be called.

b. If yield to maturity (YTM) on Bond B falls by 75 basis points:

Projected % change in price = – (Modified duration) (Change in YTM)

c. For Bond A (the callable bond), bond life and therefore bond cash flows are

uncertain. If one ignores the call feature and analyzes the bond on a “to maturity”

basis, all calculations for yield and duration are distorted. Durations are too long

CFA 4

Answer:

11-4

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 11 – Managing Bond Portfolios

a. The Aa bond initially has the higher yield to maturity (yield spread of 40 b.p.

versus 31 b.p.), but the Aa bond is expected to have a widening spread relative

to Treasuries. This will reduce rate of return. The Aaa spread is expected to be

stable. Calculate comparative returns as follows:

b. Other variables that one should consider:

Potential changes in issue-specific credit quality: If the credit quality of the

bonds changes, spreads relative to Treasuries will also change.

Changes in relative yield spreads for a given bond rating: If quality spreads

CFA 5

Answer:

∆P/P = −D* ∆y

For Strategy I:

5-year maturity: ∆P/P = −4.83 × (−0.75%) = 3.6225%

CFA 6

Answer:

a. For an option-free bond, the effective duration and modified duration are

approximately the same. The duration of the bond described in Table 22A is

calculated as follows:

b. The total percentage price change for the bond described in Table 22A is

estimated as follows:

11-5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 11 – Managing Bond Portfolios

CFA 7

Answer:

a. i. Effective duration = (116.887 – 100.00)/(2 × 100 × 0.01) = 15.26

ii. Effective duration = (50/98.667) × 15.26 + (48.667/98.667) × 2.15 = 8.79

CFA 8

Answer:

a. The two risks are price risk and reinvestment rate risk. The former refers to

b. Immunization is the process of structuring a bond portfolio in such a manner that

c. Duration matching is superior to maturity matching because bonds of equal

Answer:

The economic climate is one of impending interest rate increases. Hence, we will want

a. Choose the short maturity (2017) bond.

b. The Arizona bond likely has lower duration. Coupons are about equal, but the

c. Choose the 9⅜ % coupon bond. Maturities are about equal, but the coupon is much

d. The duration of the Shell bond will be lower if the effect of the higher yield to

e. The floating rate bond has a duration that approximates the adjustment period,

CFA 10

11-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 11 – Managing Bond Portfolios

Answer:

a. (4) A low coupon and a long maturity

Answer:

a. A manager who believes that the level of interest rates will change should

b. A change in yield spreads across sectors would call for an inter-market spread swap,

c. A belief that the yield spread on a particular instrument will change calls for a

CFA 12

Answer:

a. This swap would have been made if the investor anticipated a decline in long-term

interest rates and an increase in long-term bond prices. The deeper discount, lower

b. This swap was probably done by an investor who believed the 24 basis point yield

spread between the two bonds was too narrow. The investor anticipated that, if the

spread widened to a more normal level, either a capital gain would be experienced

on the Treasury note or a capital loss would be avoided on the Phone bond, or both.

c. This swap would have been made if the investor were bearish on the bond market.

The zero coupon note would be extremely vulnerable to an increase in interest rates

11-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 11 – Managing Bond Portfolios

d. These two bonds are similar in most respects other than quality and yield. An

investor who believed the yield spread between Government and Al bonds was too

e. The principal differences between these two bonds are the convertible feature of the

Z mart bond, and, for the Lucky Duck debentures, the yield and coupon advantage,

11-8

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.