Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 10 - Bond Prices and Yields

CHAPTER 10

10-1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 10 - Bond Prices and Yields

BOND PRICES AND YIELDS

1.

a. Catastrophe bond: Typically issued by an insurance company. They are similar to an

insurance policy in that the investor receives coupons and par value, but takes a loss in part or all of the

b. Eurobond: They are bonds issued in the currency of one country but sold in other national

c. Zero-coupon bond: Zero-coupon bonds are bonds that pay no coupons but do pay a par

d. Samurai bond:Yen-denominated bonds sold in Japan by non-Japanese issuers are called

e. Junk bond: Those rated BBB or above (S&P, Fitch) or Baa and above (Moody’s) are

f. Convertible bond: Convertible bonds may be exchanged, at the bondholder’s discretion,

g. Serial bond: A serial bond is an issue in which the firm sells bonds with staggered

h. Equipment obligation bond: A bond that is issued with specific equipment pledged as

i. Original issue discount bonds: Original issue discount bonds are less common than

j. Indexed bond: Indexed bonds make payments that are tied to a general price index or the

2. Callable bonds give the issuer the option to extend or retire the bond at the call date, while the

3.

a. YTM will drop since the company has more money to pay the interest on its bonds.

b. YTM will increase since the company has more debt and the risk to the existing

c. YTM will decrease since the firm has either fewer current liabilities or an increase in

10-2

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 10 - Bond Prices and Yields

Accrued Interest =

Annual Coupon Payment

2

Day s since Last Coupon Payment

Days Separating Coupon Payment

= $30 (30/182) = $4.945

At a price of 117, the invoice price is:$1,170 + $4.945 = $1,174.95

5. Using a financial calculator, PV = –746.22, FV = 1,000, n=5, PMT = 0.

The YTM is 6.0295%.

Using a financial calculator, PV = –730.00, FV = 1,000,n=5, PMT = 0.

The YTM is 6.4965%.

6. A bond’s coupon interest payments and principal repayment are not affected by changes in

market rates. Consequently, if market rates increase, bond investors in the secondary markets are

7. The bond callable at 105 should sell at a lower price because the call provision is more

valuable to the firm. Therefore, its yield to maturity should be higher.

8. The bond price will be lower. As time passes, the bond price, which is now above par value,

9. Current yield =

Annual Coupon

Bond Price

=

$ 1,000 4.8 %

$970

= 4.95%

10. a. The purchase of a credit default swap. The investor believes the bond may increase in credit

11. c. When credit risk increases, the swap premium increases because of higher chances of default

12. The current yield and the annual coupon rate of 6% imply that the bond price was at par a year

ago.

Using a financial calculator, FV = 1,000, n=7, PMT = 60, and i=7 gives us a selling price

13. Zero coupon bonds provide no coupons to be reinvested. Therefore, the final value of the investor's

14.

10-3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 10 - Bond Prices and Yields

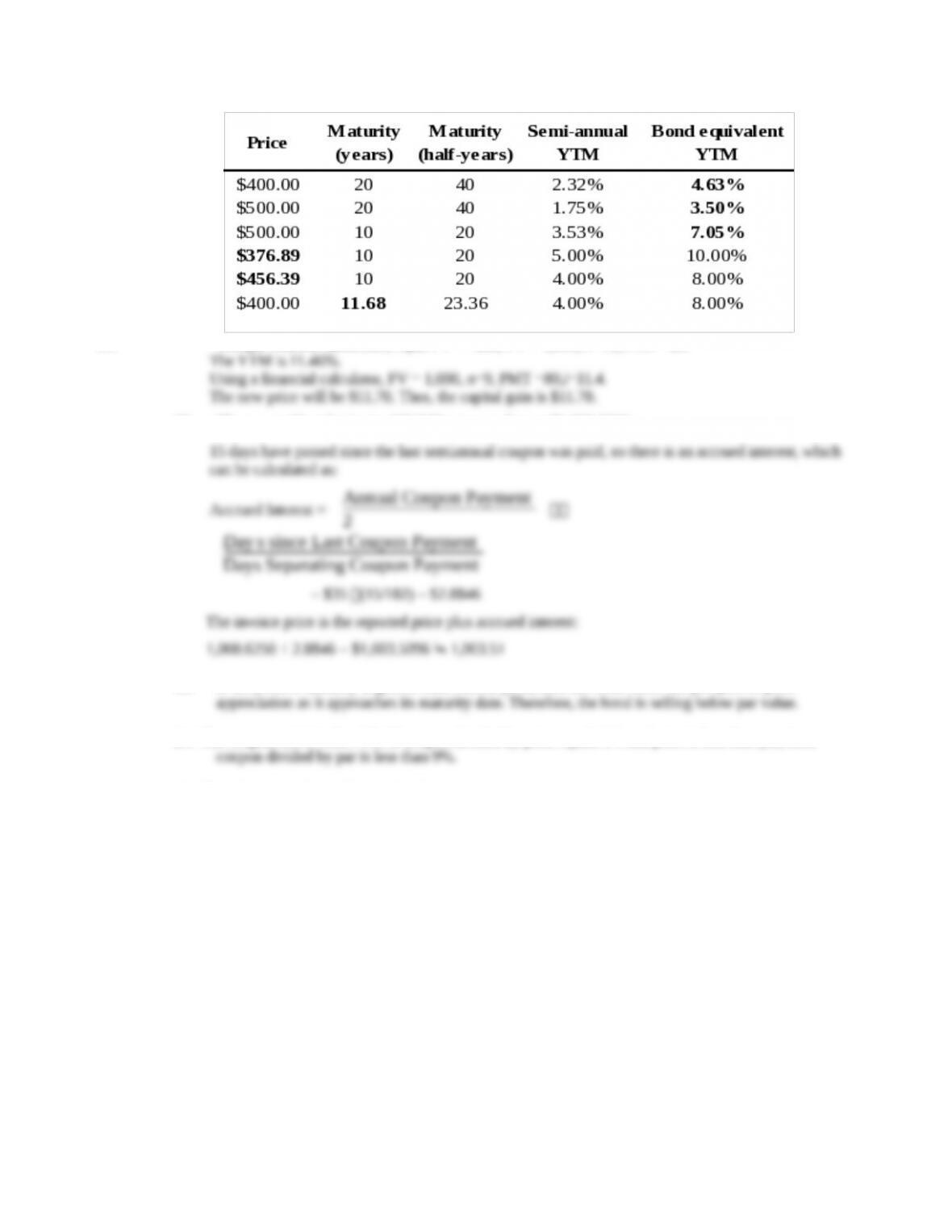

a. Effective annual rate on a three-month T-bill:

(

$100,000

$97,645

)

4

– 1 = (1.02412)4 –1 = 0.1000 = 10%

b. Effective annual interest rate on coupon bond paying 5% semiannually:

15. The effective annual yield on the semiannual coupon bonds is (1.04)2 = 8.16%. If the annual

16.

a. The bond pays $50 every six months.

b. Rate of Return =

$ 50 + ($1,044.52- $ 1,052.42 )

$ 1,052.42

=

$ 5 0 -$7.90

$ 1,052.42

17.

a. Use the following inputs: n = 40, FV = 1,000, PV = –950, PMT = 40. We will find that

b. Since the bond is selling at par, the yield to maturity on a semi-annual basis is the same

c. Keeping other inputs unchanged but setting PV = –1,050, we find a bond equivalent yield

18. Since the bond payments are now made annually instead of semi-annually, the bond

equivalent yield to maturity is the same as the effective annual yield to maturity. The inputs

10-4

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 10 - Bond Prices and Yields

The yields computed in this case are lower than the yields calculated with semi-annual coupon

payments. All else equal, bonds with annual payments are less attractive to investors because more

time elapses before payments are received. If the bond price is the same with annual payments, then

the bond's yield to maturity is lower.

19.

Nominal Return =

Interest + Price Appr eciation

Initial Price

1+ Nominal Return

1 + In flationRate

The second year

Nominal Return =

$ 42.02 +$ 30 . 6 0

$ 1,020.00

= 0.071196 = 7.12%

1+ 0 .071196

1.071196

Chapter 10 - Bond Prices and Yields

21. Using a financial calculator, input PV = –800, FV = 1,000, n=10, PMT =80.

22. The reported bond price is: 100 2/32 percent of par = $1,000.6250

23. If the yield to maturity is greater than current yield, then the bond offers the prospect of price

24. The coupon rate is below 9%. If coupon divided by price equals 9% and price is less than par, then

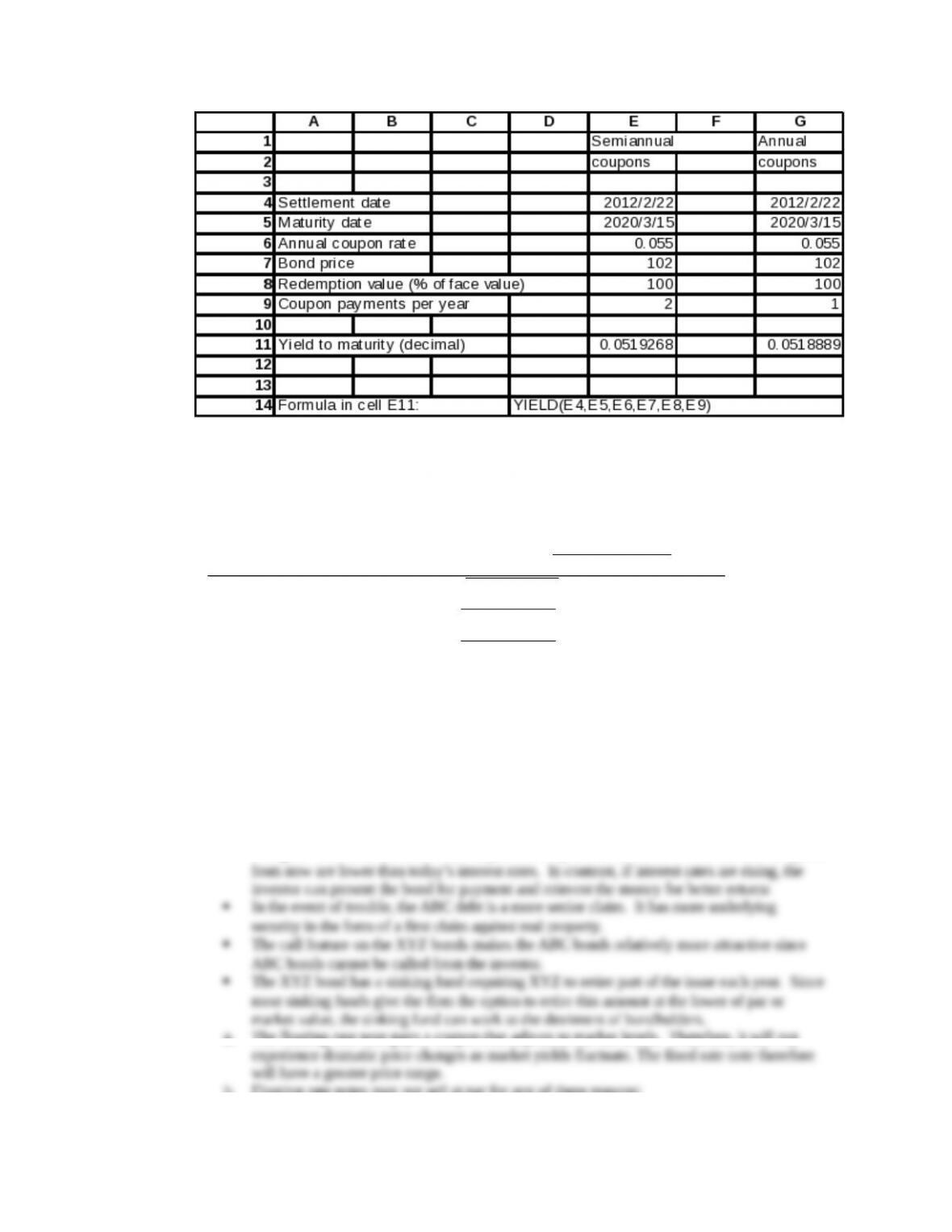

25. The solution is obtained using Excel:

26. The solution is obtained using Excel:

10-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 10 - Bond Prices and Yields

27. Using financial calculator, n = 10; PV = –900; FV = 1,000; PMT = 140

The stated yield to maturity equals 16.075%

Based on expected coupon payments of $70 annually, the expected yield to maturity is: 8.5258%.

28. The bond is selling at par value. Its yield to maturity equals the coupon rate, 10%. If the first-year

coupon is reinvested at an interest rate of r percent, then total proceeds at the end of the second

year will be: [100 (1 + r) + 1100]. Therefore, realized compound yield to maturity will be a

function of r as given in the following table:

rTotal proceeds Realized YTM =

√

Proceeds/1,000

= 1

8% $1,208

√

1,208/1,000

– 1 = 0.0991 = 9.91%

10% $1,210

√

1,210/1,000

– 1 = 0.1000 = 10.00%

12% $1,212

√

1,210/1,000

– 1 = 0.1009 = 10.09%

1. April 15 is midway through the semi-annual coupon period. Therefore, the invoice price will be

higher than the stated ask price by an amount equal to one-half of the semiannual coupon. The ask

price is 101.125 percent of par, so the invoice price is:

$1,011.25 + (1/2 $50) = $1,036.25

1. Factors that might make the ABC debt more attractive to investors, therefore justifying a lower

coupon rate and yield to maturity, are:

The ABC debt is a larger issue and therefore may sell with greater liquidity.

An option to extend the term from 10 years to 20 years is favorable if interest rates ten years

a. The floating-rate note pays a coupon that adjusts to market levels. Therefore, it will not

b. Floating rate notes may not sell at par for any of these reasons:

10-7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 10 - Bond Prices and Yields

c. The risk of call is low. Because the bond will almost surely not sell for much above par

d. The fixed-rate note currently sells at only 93% of the call price, so that yield to maturity

e. The 9% coupon notes currently have a remaining maturity of fifteen years and sell at a

f. Because the floating rate note pays a variable stream of interest payments to maturity, its

yield-to-maturity is not a well-defined concept. The cash flows one might want to use to

a. The bond sells for $1,124.7237 based on the 3.5% yield tomaturity:

[n = 60; i = 3.5; FV = 1,000; PMT = 40]

b. If the call price were $1,050, we would set FV = 1,050 and redo part (a) to find that yield to

call is 2.9763% semi-annually,5.9525% annually.With a lower call price, the yield to call is

lower.

c. Yield to call is 3.0312% semiannually, 6.0625% annually:

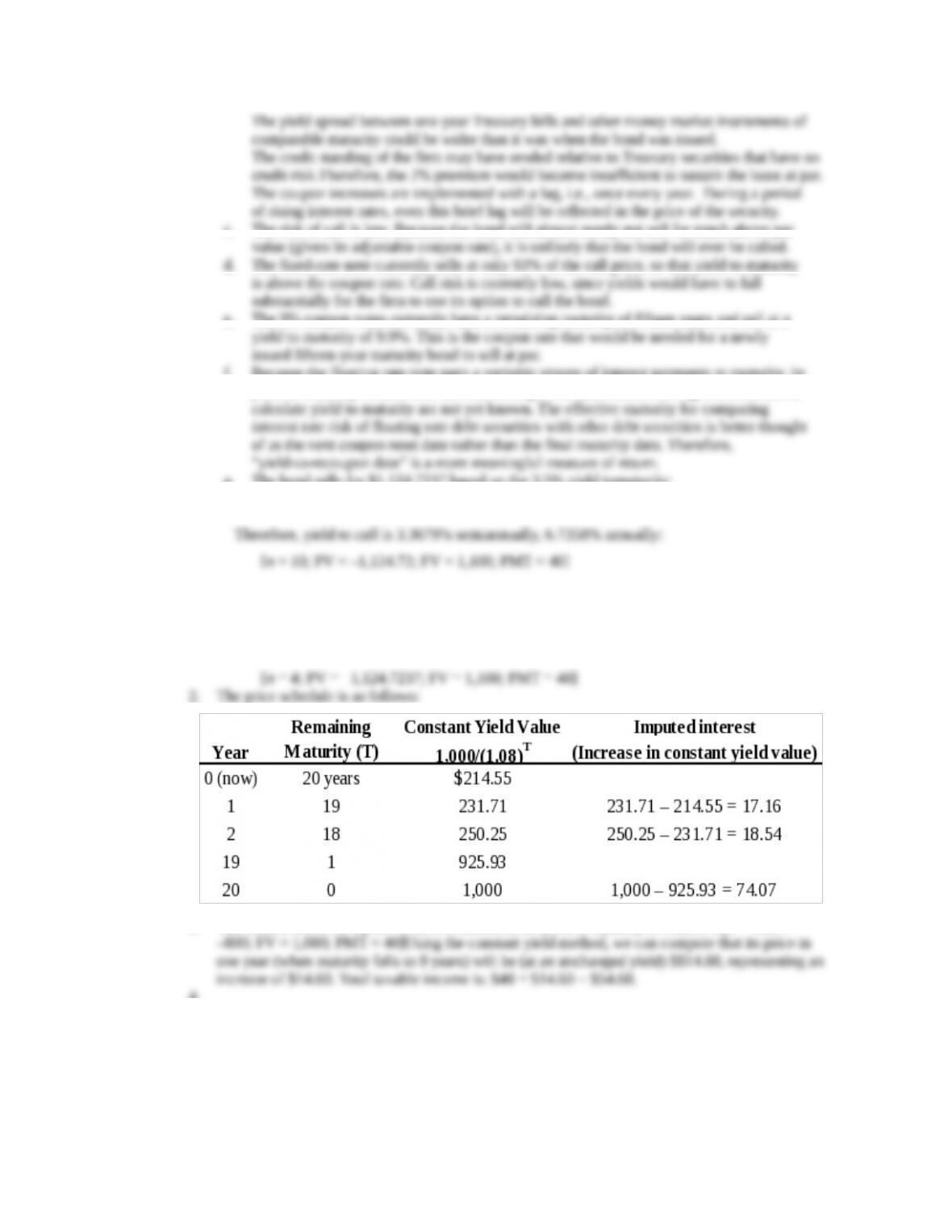

2. The price schedule is as follows:

3. The bond is issued at a price of $800. Therefore, its yield to maturity is 6.8245%.[n = 10;PV=

4.

10-8

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 10 - Bond Prices and Yields

a. The yield to maturity of the par bond equals its coupon rate, 8.75%. All else equal, the

b. If an investor expects rates to fall substantially, the 4% bond offers a greater expected

return.

c. Implicit call protection is offered in the sense that any likely fall in yields would not be

nearly enough to make the firm consider calling the bond. In this sense, the call feature is

almost irrelevant.

5. True. Under the expectations hypothesis, there are no risk premia built into bond prices. The

6. If the yield curve is upward sloping, we cannot conclude that investors expect short-term interest

7.

8. Uncertain. Lower inflation usually leads to lower nominal interest rates. Nevertheless, if the

liquidity premium is sufficiently great, long-term yields can exceed short-term yields despite

expectations of falling short rates.

9.

a. We summarizethe forward rates and current prices in the following table:

Maturity

(years) YTM Forward rate Price (for part c)

1 10.0% $909.09

2 11.0% 12.01% $811.62

3 12.0% 14.03% $711.78

Year 1

b. We obtain next year’s prices and yields by discounting each zero’s face value at the

forward rates derived in part (a):

Maturity

(years) Price YTM

10-9

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 10 - Bond Prices and Yields

c. Next year, the two-year zero will be a one-year zero, and it will therefore sell at:

Chapter 10 - Bond Prices and Yields

c. After-tax HPR =

$ 50+($ 793.29 - $ 705.4 6) -$ 46.99

$ 70 5.46

d. Value of the bond after two years equals $798.82 [using n = 18; i = 7]

CFA 1

Answer:

a. (3) The yield on the callable bond must compensate the investor for the risk of call.

10-11

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 10 - Bond Prices and Yields

b. (3)

c. (2)

d. (3

CFA 2

Answer:

a. The maturity of each bond is 10 years, and we assume that coupons are paid semiannually.

b. If rates are expected to fall, the Sentinal bond is more attractive: Since it is not subject to

c. An increase in the volatility of rates increases the value of the firm’s option to call back the

CFA 3

Answer

Market conversion value = Value if converted into stock

= 20.83 $28 = $583.24

CFA 4

Answer:

a. The call provision requires the firm to offer a higher coupon (or higher promised yield to

maturity) on the bond in order to compensate the investor for the firm's option to call

b. The call option reduces the expected life of the bond. If interest rates fall substantially so

10-12

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.

Chapter 10 - Bond Prices and Yields

c. The advantage of a callable bond is the higher coupon (and higher promised yield to

maturity) when the bond is issued. If the bond is never called, then an investor will earn a

CFA 5

Answer:

a.

(1) Current yield = Coupon/Price = $70/$960 = 0.0729 = 7.29%

(2) YTM = 3.993% semiannually or 7.986% annual bond equivalent yield

(3) Realized compound yield is 4.166% (semiannually), or 8.332% annual bond

equivalent yield. To obtain this value, first calculate the future value of reinvested

b. Shortcomings of each measure:

(1) Current yield does not account for capital gains or losses on bonds bought at prices

(2) Yield to maturity assumes that the bond is held to maturity and that all coupon

(3) Realized compound yield (horizon yield) is affected by the forecast of reinvestment

10-13

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part.