C01-10-0008

Graeme Rankine

Smart Union Group (Holdings) Limited—

A (Short) Toy Story

Teaching Note

Case Abstract

change, which netted HK$55 million. From 2003 to 2007, the company’s sales revenues increased from HK$479

million to over HK$953 million. The company’s rapid growth was financed by issuing equity and obtaining

Teaching Objectives

company’s financial performance,

3. To analyze a company’s growth, its ability to generate cash flows, and its financial performance,

4. To evaluate a company’s financing needs, the possible financing methods it has available, and how it might

choose a preferred plan.

Specifically, students are asked to consider several issues in the case. First, students are asked to explain how

Smart Union makes money, to evaluate its business strategy for accomplishing this objective, and to evaluate

how successful execution of this strategy is likely to be observable from the company’s performance indicators.

Second, students are asked to analyze the risk faced by the company from fluctuations in commodity prices,

exchange rates, and interest rates, as well as operational risks faced in manufacturing, selling, and distributing its

products. Third, students are asked to evaluate the company’s rapid growth, its cash flow situation, and recent

financial performance, including its profitability, asset management, and leverage. Finally, students are asked to

evaluate Smart Union’s cash flows, and how it will fund the bank loan due within the next year.

The case has been used successfully in MBA programs to cover corporate financial reporting issues, and in

bank training programs focused on credit analysis and quality of earnings issues.

Suggested Case Questions

1. How does Smart Union make money? What are the key success factors in Smart Union’s business? What are

2 C01-10-0008

management, leverage, and liquidity performance?

4. Will the company be able to repay the short-term bank debt due within 12 months? What should the com-

pany do if the bank debt is not refinanced?

Case Analysis

Question 1

Smart Union manufactures toys and recreational and educational products at its facilities in China for OEMs,

such as Mattel, Hasbro, and others, whose sales are mainly generated in the U.S. and Europe. Thus, Smart

Union’s value chain of activities could be described as follows:

Toy Design and

Development

Manufacturing and

Logistics

Sales and

Marketing Distribution Servicing?

The company’s strategy was to be a low-cost and high-quality producer, maintain close relationships with

OEMs, and produce a broad array of products.

Smart Union’s success would be expected to be observable from revenue growth, as the quality of its

nated in U.S. dollars, would increase the company’s manufacturing and distribution costs. The company was

also exposed to labor cost increases, which the case mentioned occurred because of labor shortages in China, and

because of efforts by Chinese companies to attract workers with offers of better wages and working conditions.

The company was also exposed to interest rate increases, since it had financed its growth heavily with short-term

euro appreciated against the HK dollar; thus, Europe-based sales would generate more HK dollars. Finally, the

Chinese renminbi appreciated relative to the HK dollar; thus, with Chinese-based manufacturing facilities, the

company had costs that were adversely exposed to appreciation in the renminbi. On balance, this suggests that

Smart Union was squeezed in the middle, since it was exposed to both rising costs in HK dollars, and declin-

thereby incur dollar-and euro-based interest costs.

The investment in a silver mine to hedge silver costs incurred in the manufacture of its toy products was

likely to be a diversification move that decreased shareholder value. A toy manufacturer is unlikely to know much

about silver mining, and there are more effective ways to hedge silver cost exposure. It seemed a reckless move

as the company struggled to meet debt repayment obligations. One certainly wonders if the move was a related

C01-10-0008 3

Question 2

Smart Union grew rapidly, increasing sales revenue from HK$479 million in 2003 to over HK$953 million

in 2007, or a compound growth rate of 19% per year over the four-year period. Profit increased from HK$26

million in 2003 to peak at over HK$36 million in 2005, before declining to HK$5.4 million in 2007. Working

labor and commodity costs mentioned in the case, as well as the effects of price discounting to move inventory.

By 2007, the company’s operating profit percentage was less than 3%, while “bottom-line” profit was less than

1% of revenues in 2007, down from 4.2% in 2006.

The company’s return on assets at less than 1% was very weak. The company’s return on equity was a mere

1.7% in 2007, much less than the 18.3% achieved in 2006. The company’s day’s receivable increased from 52

days in 2006 to over 63 days in 2007, while the company’s day’s inventory increased from 145 days in 2006 to

165 days in 2007. And, overall, the company’s assets were less productive, with asset turnover decreasing from

1.5 times to 1.2 times. While the company’s total debt increased in amount, the company’s debt ratio remained

around 0.80, but the company’s interest coverage declined from over 4% in 2006 to around 1.45% in 2007.

The company’s liquidity measures remained steady.

The overall conclusion is that the company’s profitability fell off the edge, the company was now bloated

with inventory, and there seemed to be a receivable collection problem. Thus, the firm’s financial risk has increased

with the decline in the firm’s interest coverage.

Question 3

The instructor can ask students to prepare a cash flow statement based on the financial statements provided in

the case. A cash flow statement worksheet for 2007 is provided in Exhibit TN-2 Panel A. The resulting cash flow

statement is provided in Exhibit TN-2 Panel B. For MBA classes, this provides students with an opportunity

to practice preparing a cash flow statement. Alternatively, particularly with executive education programs, the

instructor can provide Smart Union’s actual cash flow statement, provided in Exhibit TN-3, and use that as a

basis for class discussion. The two cash flow statements are similar enough so that either one may be used for

analysis.

The cash flow statement in Exhibit TN-3 indicates that the drop off in profits reduced cash flow in 2007.

But the build up in inventories and receivables dramatically reduced cash flow from operations, and the invest-

ment in these two working capital items was only modestly offset by increases in trade payables and other accruals

and payables. Thus, Smart Union generated a negative cash flow from operations of $148 million. In addition,

capital expenditures and other such items further reduced cash from investing by $73 million. How was the hole

of $221 million plugged? The financing section shows that Smart Union increased debt by $107 million and

equity by $160 million, which resulted in a $37 million increase in cash holdings.

Question 4

The principal on the bank loan is listed under current liabilities on the company’s balance sheet as HK$239.7

million. To determine whether Smart Union can pay down the debt or would be forced to refinance or possibly

obtain additional equity financing, a forecasted cash flow statement for 2008 is needed. For the purposes of this

calculation, we’ll assume that the cash flow from operations (CFO) in 2008 was the same in 2007. Forecasted

cash flows could be determined by making additional assumptions about what assets could be liquidated, and

for how much, and what other liabilities could be increased. We’ll assume that the company spends nothing on

capital expenditures, i.e., cash flow from investing is zero.

4 C01-10-0008

2008

Cash flow from operations (assumed same as last year) -142,646

Liquidation of inventories 200,000

Collection or sale of trade receivables 100,000

Reduction in cash balances 50,000

Sale of convertible bonds 30,000

Liquidation of available-for-sale financial assets 2,342

Net cash flow 239,696

Bank debt due 239,768

Thus, Smart Union could generate enough cash to cover the principal repayment only under the very

best of conditions. The assumptions built into the forecast above are very optimistic. In order to survive, Smart

Union would likely need either an equity infusion from its principal shareholders, or would have to refinance

its debt. Would the principal shareholder be willing to kick in more equity? That depends on whether they

believed the business was a viable going concern that needed to be nursed through a transitory downturn. In all

likelihood, with a more apparent and sizeable recession in process, the owners would not be willing to invest in

new equity. Would the bank or other lenders be willing to refinance the company’s debt? Again, for the same

reasons, a bank would be unlikely to refinance the company in the deepening recession, and with an impending

credit squeeze.

Post-Case Developments

On October 18, 2008, Smart Union announced that it had appointed provisional liquidators to wind up the

toy and recreational products company and its subsidiaries.1 On October 21, 2008, it was reported that Smart

Union’s Chief Executive Officer had signed on as managing director at a rival toymaker, a company he worked

for prior to joining Smart Union.2 Selected items from Smart Union’s Interim Report for June 30, 2008, are

reported in Exhibit TN-5.

1 “Chinese Toy Firm Becomes Casualty of Global Crisis,” The Wall Street Journal, October 18, 2008.

2 “Toymaker Fails…Chief Jumps Ship,” South China Morning Post, October 21, 2008.

C01-10-0008 5

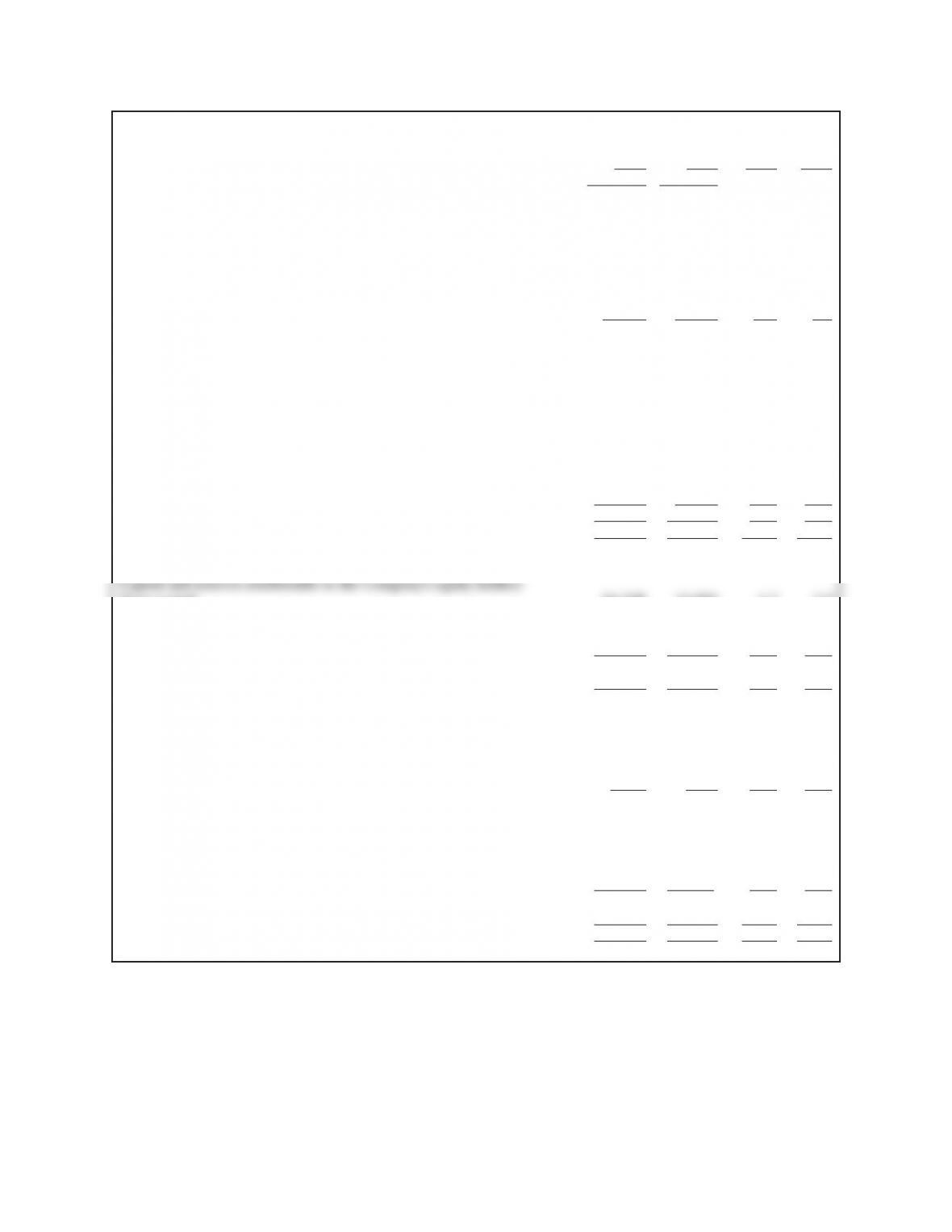

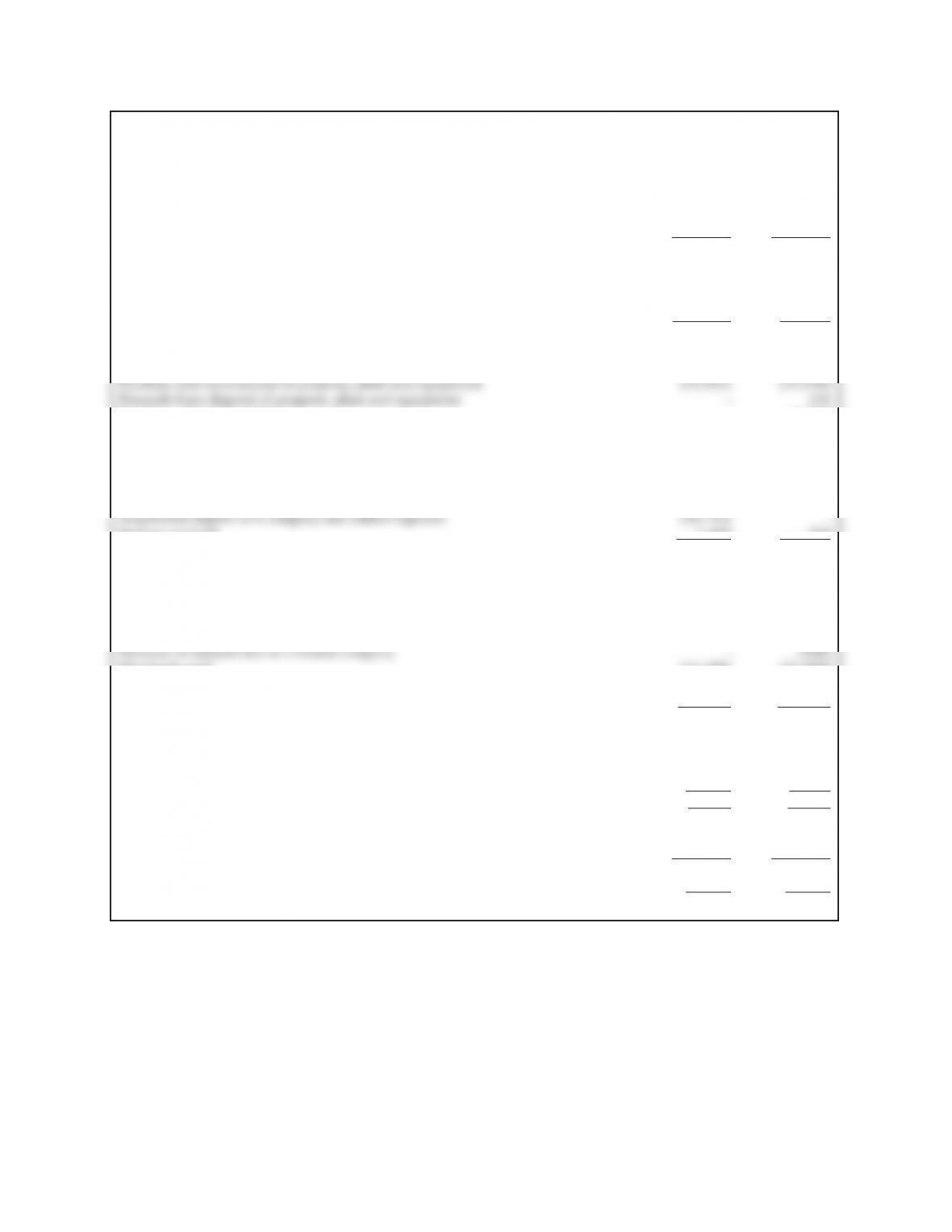

Exhibit TN-1.

Balance Sheet 2007 2006 2007 2006

HK$’000 HK$’000

ASSETS

Non-current assets

Property, plant and equipment 66,408 43,245 8.3 8.9

Land use rights 4,849 4,516 0.6 0.9

Intangible assets 2,967 632 0.4 0.1

Available-for-sale financial assets 2,342 5,120 0.3 1.1

Prepayments, deposits and other receivables 11,261 276 1.4 0.1

Deferred income tax assets 749 134 0.1 0.0

88,576 53,923 11.1 11.2

Current assets

Inventories 379,440 240,322 47.4 49.7

Trade receivables 165,438 104,029 20.7 21.5

Prepayments, deposits and other receivables 19,022 12,857 2.4 2.7

Derivative financial instruments 213 1,247 0.0 0.3

Convertible bonds 40,000 –5.0 0.0

Current income tax recoverable 1,046 737 0.1 0.2

Pledged bank deposits 5,234 5,267 0.7 1.1

Cash and cash equivalents 101,584 64,882 12.7 13.4

711,977 429,341 88.9 88.8

Total Assets 800,553 483,264 100.0 100.0

EQUITY

Share capital 34,248 24,000 4.3 5.0

Share premium 177,137 30,742 22.1 6.4

Other reserves 29,293 25,830 3.7 5.3

Retained earnings 76,112 85,832 9.5 17.8

316,790 166,404 39.6 34.4

Minority interest 1,370 607 0.2 0.1

Total equity 318,160 167,011 39.7 34.6

LIABILITIES

Non-current liabilities

Borrowings 201 2,749 0.0 0.6

Provision for long service payment 1,104 – 0.1 0.0

1,305 2,749 0.2 0.6

Current liabilities 0.0 0.0

Trade payables 195,631 158,837 24.4 32.9

Other payables and accruals 43,333 24,113 5.4 5.0

Borrowings 239,768 130,554 30.0 27.0

Derivative financial instruments 2,356 0.3 0.0

481,088 313,504 60.1 64.9

Total liabilities 482,393 316,253 60.3 65.4

Total equity and liabilities 800,553 483,264 100.0 100.0

6 C01-10-0008

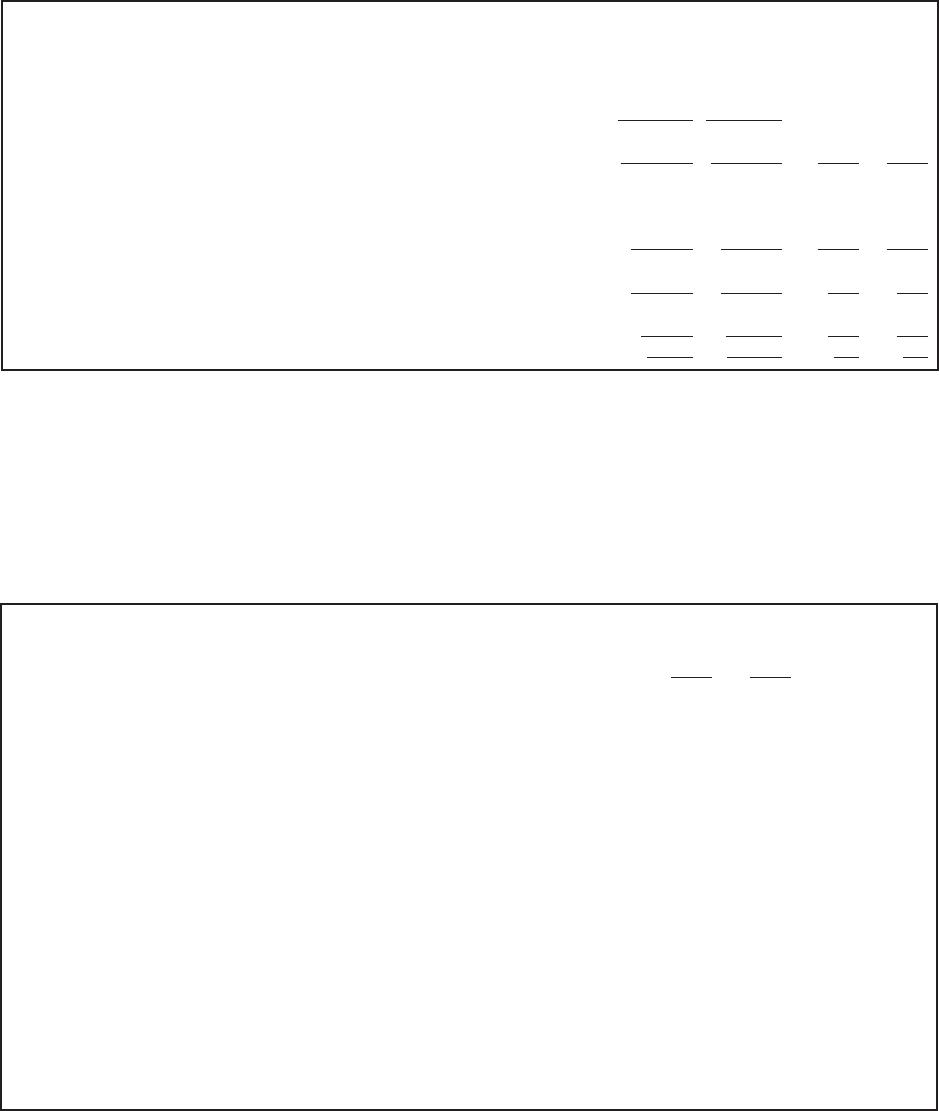

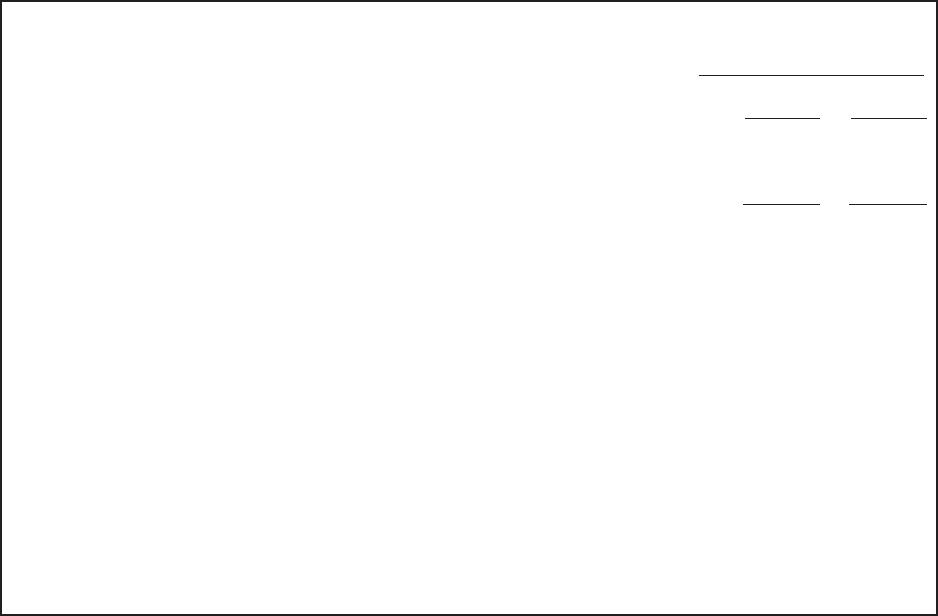

Exhibit TN-2

2007 2006

Profitability

Gross profit margin 11.9% 16.8%

Operating profit margin 2.9% 6.5%

Return on sales 0.6% 4.2%

Return on assets 0.7% 6.3%

Return on equity 1.7% 18.3%

Asset Management

Day’s receivable 63.3 52.2

Day’s inventory 164.9 145.0

Asset turnover 1.2 1.5

Leverage

Debt-equity 0.75 0.80

Interest coverage 1.45 4.18

Liquidity

Quick ratio 0.56 0.54

Current ratio 1.48 1.37

Exhibit TN-1 (cont.)

Income Statement

2007 2006 2007 2006

HK$’000 HK$’000

Sales 953,623 727,225 100.0 100.0

Cost of sales -839,734 -604,952 -88.1 -83.2

Gross profit 113,889 122,273 11.9 16.8

Other income 12,320 1,906 1.3 0.3

Other (losses)/gains, net -1,893 1,804 -0.2 0.2

Administrative expenses -96,704 -78,973 -10.1 -10.9

Operating profit 27,612 47,010 2.9 6.5

Finance costs -19,035 -11,242 -2.0 -1.5

Profit before tax 8,577 35,768 0.9 4.9

Income tax expense -3,134 -5,136 -0.3 -0.7

Profit for the year 5,443 30,632 0.6 4.2

C01-10-0008 7

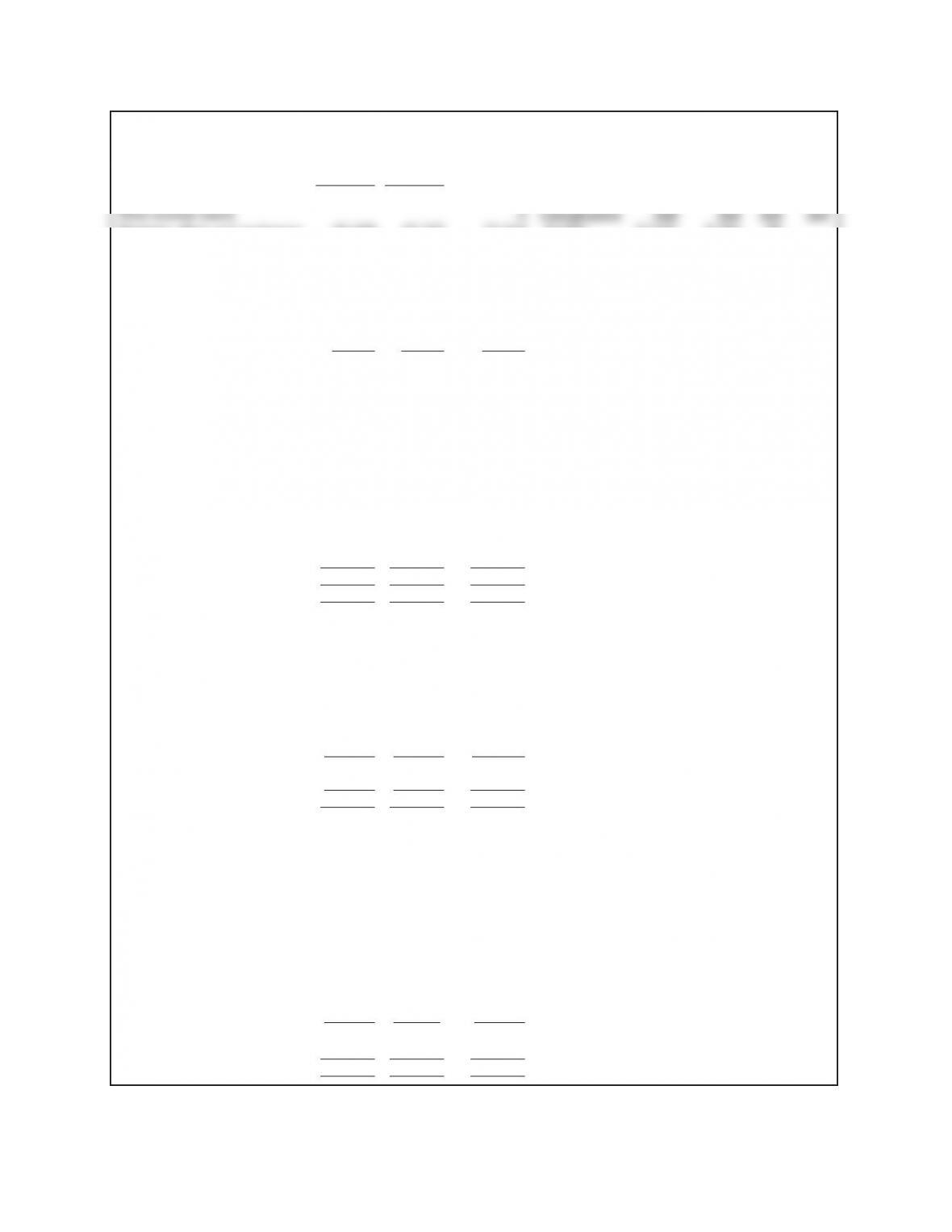

Exhibit TN-3. Panel A

2007 2006

HK$’000 HK$’000

ASSETS

Property, plant and equipment 66,408 43,245 23,163 Inv/Op 32,037 8,784 90

Land use rights 4,849 4,516 333 Inv/Op 402 69

Intangible assets 2,967 632 2,335 Inv/Op 3,396 144 567 350

Available-for-sale financial

assets 2,342 5,120 (2,778) Inv

Prepayments, deposits and

other receivables 11,261 276 10,985 Op

Deferred income tax assets 749 134 615 Op

88,576 53,923 34,653

Current assets

Inventories 379,440 240,322 139,118 Op

Trade receivables 165,438 104,029 61,409 Op

Prepayments, deposits and

other receivables 19,022 12,857 6,165 Op

Derivative financial

instruments 213 1,247 (1,034) Op

Convertible bonds 40,000 40,000 Inv

Current income tax

recoverable 1,046 737 309 Op

Pledged bank deposits 5,234 5,267 (33) Fin

Cash and cash equivalents 101,584 64,882 36,702 Cash

711,977 429,341 282,636

Total Assets 800,553 483,264 317,289

EQUITY

Capital and reserves

attributable to the

Company’s equity holders

Share capital 34,248 24,000 10,248 Fin

Share premium 177,137 30,742 146,395 Fin

Other reserves 29,293 25,830 3,463 Fin

Retained earnings 76,112 85,832 (9,720) Op/Fin 4,680 (14,400)

316,790 166,404 150,386

Minority interest 1,370 607 763 Op

Total equity 318,160 167,011 151,149

LIABILITIES

Non-current liabilities

Borrowings 201 2,749 (2,548) Fin

Provision for long service

payment 1,104 1,104 Op

1,305 2,749 (1,444)

Current liabilities

Trade payables 195,631 158,837 36,794 Op

Other payables and accruals 43,333 24,113 19,220 Op

Borrowings 239,768 130,554 109,214 Fin

Derivative financial

instruments 2,356 2,356 Op

481,088 313,504 167,584

Total liabilities 482,393 316,253 166,140

Total equity and liabilities 800,553 483,264 317,289

8 C01-10-0008

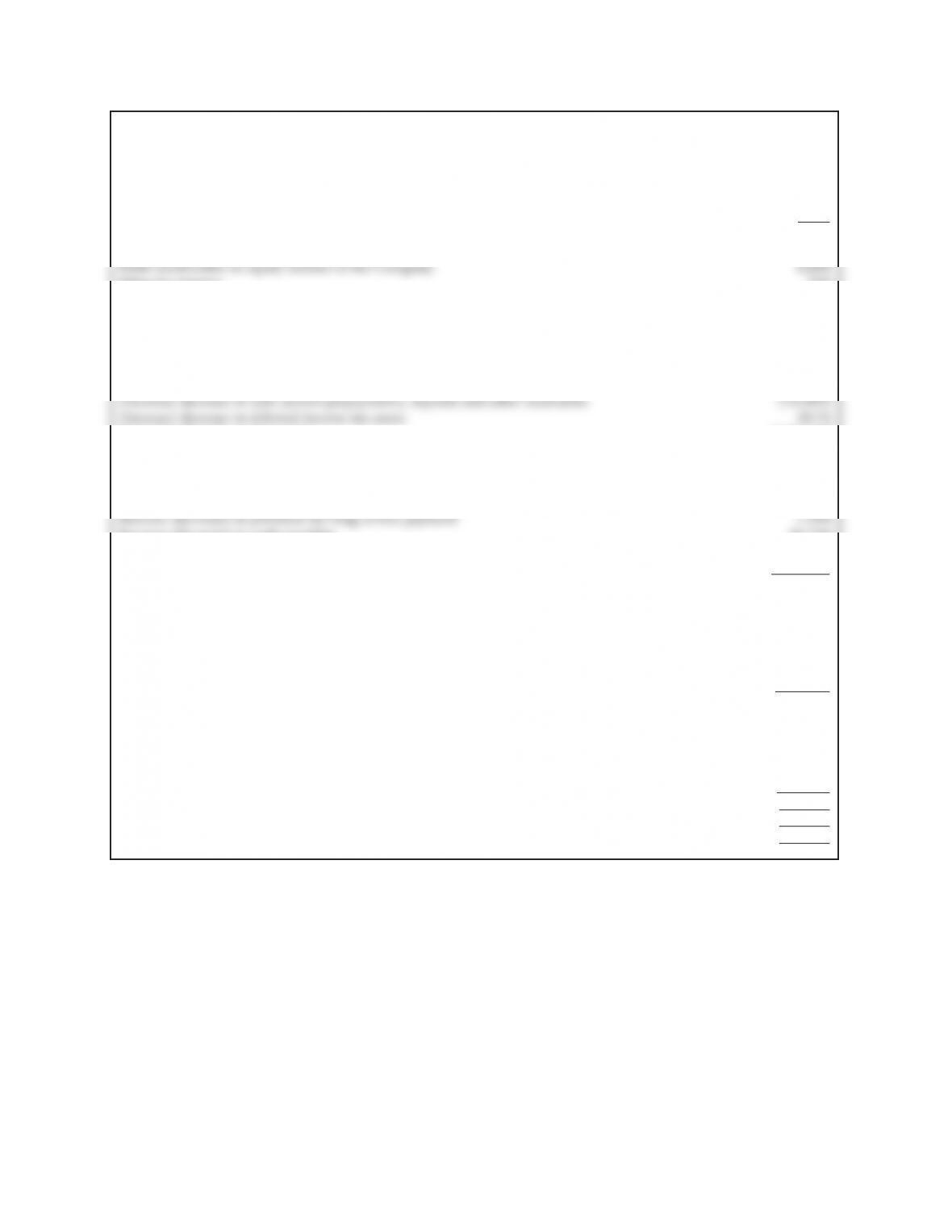

Exhibit TN-3. Panel B

CONSOLIDATED CASH FLOW STATEMENT

For the year ended 31st December 2007

2007

Statement of Cash Flows

Operating activities

Minority interest 763

Depreciation on property, plant and equipment 8,784

Loss on disposal of property, plant and equipment 90

Amortization of land use rights 69

Amortization of intangible assets 567

Impairment of intangible assets 350

Loss on disposal of intangible assets 144

(Increase) decrease in inventories (139,118)

(Increase) decrease in trade receivables (61,409)

(Increase) decrease in current prepayments, deposits and other receivables (6,165)

(Increase) decrease in derivative financial instruments 1,034

(Increase) decrease in income tax recoverable (309)

Increase (decrease) in trade payables 36,794

Increase (decrease) in other payables and accruals 19,220

Increase (decrease) in derivative financial instruments 2,356

Cash flow from operations (142,646)

Investing activities

Acquisition of convertible bonds (40,000)

Acquisitions of property, plant and equipment (32,037)

Acquisitions of land use rights (402)

Acquisitions of intangible assets (3,396)

Sale of available-for-sale investments 2,778

Cash flow from investing activities (73,057)

Financing activities

(Increase) decrease in pledged bank deposits 33

Increase (decrease) in short and long-term borrowings 106,666

Increase (decrease) in equity 160,106

Dividends (14,400)

Cash flow from financing activities 252,405

Net cash flow 36,702

Change in cash and cash equivalents 36,702

C01-10-0008 9

Exhibit TN-4

CONSOLIDATED CASH FLOW STATEMENT

For the year ended 31st December 2007

2007

HK$’000

2006

HK$’000

Cash flows from operating activities

Cash (used in)/generated from operations (108,626) 6,277

Interest paid (19,035) (11,242)

Profits tax paid (4,617) (8,866)

Profits tax refund 561 18

Net cash used in operating activities (131,717) (13,813)

Cash flows from investing activities

Purchase of land use rights – (4,593)

Increase in intangible sales (3,396) (886)

Purchase of available-for-sale financial assets – (2,000)

Proceeds from disposal of available-for-sale financial assets 2,999

Decrease/(increase) in pledged deposits 33 (2,430)

Investments in convertible bonds (40,000) –

Interest received 1,345 764

Net cash used in investing activities (78,879) (30,964)

Cash flows from financing activities

Proceeds from new borrowings 1,129,131 357,626

Repayment of borrowings (1,022,152) (293,683)

Decrease in amounts due to directors – (3,456)

Dividends paid (14,400) (21,000)

Issue of shares 160,055 66,000

Payment of share issuance expenses (3,438) (12,758)

Net cash generated from financing activities 249,196 92,463

Net increase in cash and cash equivalents 38,600 47,686

Cash and cash equivalents at 1st January 56,738 9,110

Exchange losses on cash and cash equivalents (1,585) (58)

Cash and cash equivalents at 31st December 93,753 56,738

From Note 18 2007 2006

HK$’000 HK$’000

Bank balances and cash 101,584 64,882

Less: bank overdrafts (Note 21) (7,831) (8,144)

Cash and cash equivalents 93,753 56,738

10 C01-10-0008

Exhibit TN-5

Six months ended 30th June

2008 2007

HK$’000 HK$’000

(Unaudited) (Unaudited)

Income Statement items

Sales 386,809 375,793

Cost of sales (525,936) (325,397)

Gross profit (139,127) 50,396

Operating (loss) profit (191,815) 4,498

Loss for the period (200,561) (2,803)

Balance Sheet items

Inventories 301,649 379,440

Trade receivables 103,215 165,438

Bank balances and cash 13,207 101,584

Trade payables 218,252 195,631

Borrowings 234,467 239,987

Cash Flow Statement items

Net cash flow from operating activities 2,298 (128,474)

Net cash flow from investing activities (21,053) (23,492)

Net cash flow from financing activities (85,214) (11,343)