UVA-F-1578TN

Rev. Aug. 11, 2010

School Foundation, Charlottesville, VA. All rights reserved. To order copies, send an e-mail to

sales@dardenbusinesspublishing.com. No part of this publication may be reproduced, stored in a retrieval system,

used in a spreadsheet, or transmitted in any form or by any means—electronic, mechanical, photocopying,

recording, or otherwise—without the permission of the Darden School Foundation. Rev. 8/10.

Perpetual Growth Valuation

The case leads students to conduct their enterprise valuations using a multiple for the

terminal value. Students are also likely to have learned to develop valuations using a perpetual

growth assumption. This section of the teaching note discusses how this may be accomplished. It

can be considered supplemental analysis.

The perpetual growth approach used in this note is to forecast an additional year under

steady-state (long-term growth) assumptions and then use this to calculate a terminal value in the

final year of the planning period. This steady state is, in most cases, no different from the last

year’s except that the long-term growth rate is applied to financial statement items. It is this

growth rate that will be the focus of our discussion.

If one considers the base case where all markets are assumed to be in parity, then it is

easy to see that a growth rate in the cash flows of one currency will imply a specific growth rate

in the exchange rate converted cash flows. In fact, that implied rate can be calculated exactly as

we had previously calculated a foreign currency discount rate! In particular, we make the

following adjustment:

1

1

1

)1(

domestic

foreign

domesticforeign r

r

gg

where g is the growth rate.

growth rate is 0.98%. The value of Milagrol using either approach is the same.

The 10% perpetual BRL growth rate is probably a bit high (depends on inflation

assumptions), but what is interesting is that lower assumptions will yield a negative USD growth

1

1

Again, we note that the sovereign spread inflates the interest differential relative to parity making the

adjustment more severe.

-2- UVA-F-1578TN

illustrated.

Inflation and valuation

As noted, if inflation affects nominal values and not real values, and if that effect is

properly captured in discount rates, inflation becomes irrelevant. This is a point students may

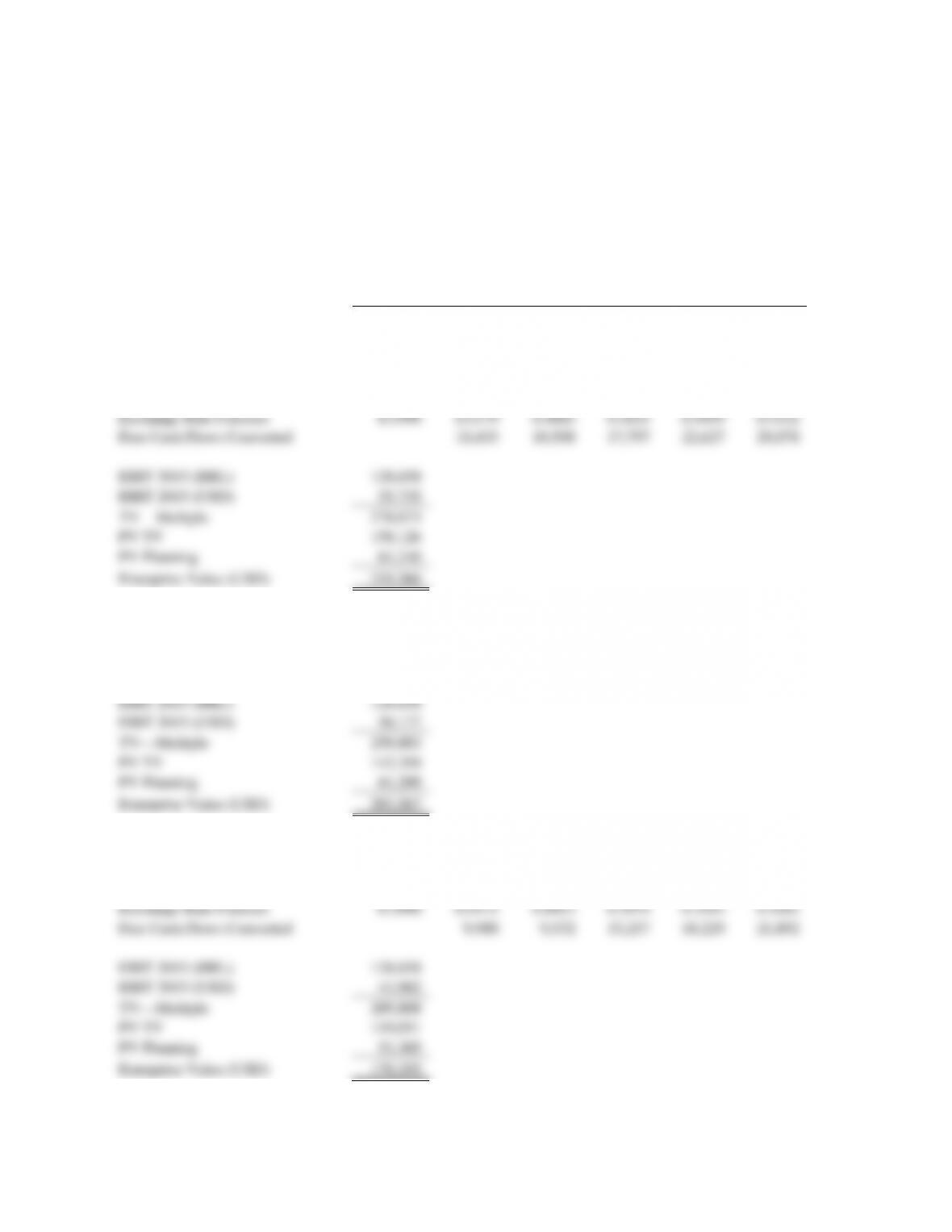

MILAGROL LTDA.

Valuation Analysis—Baseline Approaches

(numbers in thousands of USD or BRL)

2010

2011

2012

2013

2014

2015

Free Cash Flow (BRL)

20,144

21,601

38,397

50,739

67,124

Valuation BRL Discount Rate

Interest U.S.—10-Year T-Bill

3.22%

BRL Interest

12.44%

US Discount Rate

12.00%

BR Implied Discount

22.00%

EBIT Multiple

5.00

EBIT 2015 (BRL)

128,658

TV—Multiple

643,289

PV TV

237,975

PV Plan

99,898

Enterprise Value

337,873

Enterprise Value (USD)

185,492

Valuation USD Cash Flows

Interest U.S.—10-Year T-Bill

3.22%

-3- UVA-F-1578TN

BRL Interest less Sovereign Spread

12.44%

Implied Future Spot Rates

0.5490

0.5040

0.4627

0.4247

0.3899

0.3579

Converted Free Cash Flows

10,152

9,994

16,308

19,783

24,025

EBIT 2015 (BRL)

128,658

EBIT 2015 (USD)

46,049

(Convert at forecast exchange rate for 2015)

TV—Multiple

230,247

(USD EBIT times multiple)

PV TV

130,648

PV Planning

54,844

Enterprise Value (USD)

185,492

Source: Created by case writer.

-4- UVA-F-1578TN

Exhibit TN2

MILAGROL LTDA.

Valuation Analysis—Alternate Exchange Rate Forecasts

(numbers in thousands of USD or BRL)

2010

2011

2012

2013

2014

2015

Free Cash Flow (BRL)

20,144

21,601

38,397

50,739

67,124

Exchange Rates Based on Inflation Rates

BRL Inflation Expectations

6.00%

7.00%

6.00%

5.50%

5.00%

U.S. Inflation Expectation

0.00%

0.50%

1.00%

1.50%

2.00%

Exchange Rate Forecast

0.5490

0.5179

0.4865

0.4635

0.4459

0.4332

Free Cash Flows Converted

10,433

10,508

17,797

22,627

29,078

EBIT 2015 (BRL)

128,658

EBIT 2015 (USD)

55,735

TV—Multiple

278,673

PV TV

158,126

PV Planning

61,240

Enterprise Value (USD)

219,366

Exchange Rates From Econo-Metrics

Exchange Rate Forecast

0.5490

0.5600

0.5400

0.4800

0.4300

0.3900

Free Cash Flows Converted

11,281

11,665

18,430

21,818

26,178

EBIT 2015 (BRL)

128,658

EBIT 2015 (USD)

50,177

TV—Multiple

250,883

PV TV

142,358

PV Planning

61,209

Enterprise Value (USD)

203,567

Exchange Rates from Yield Curve (missing years linearly interpolated)

USD Interest

0.26%

0.73%

1.20%

1.61%

2.01%

BRL Interest

12.00%

12.19%

12.38%

12.38%

12.37%

Exchange Rate Forecast

0.5490

0.4915

0.4413

0.3974

0.3593

0.3261

Free Cash Flows Converted

9,900

9,532

15,257

18,229

21,892

EBIT 2015 (BRL)

128,658

EBIT 2015 (USD)

41,962

TV—Multiple

209,808

PV TV

119,051

PV Planning

51,305

Enterprise Value (USD)

170,355

Source: Created by case writer.

-5- UVA-F-1578TN

Exhibit TN3

MILAGROL LTDA.

Valuation Analysis—Political Risk, Sovereign Spread Adjustment

(numbers in thousands of USD or BRL)

2010

2011

2012

2013

2014

2015

Free Cash Flow (BRL)

20,144

21,601

38,397

50,739

67,124

Sovereign Spread Adjustment of the Discount Rate

Sovereign Spread

1.63%

Adjusted Discount Rate

13.63%

(Sum of discount rate and spread)

Exchange Rate Forecast

0.5490

0.5040

0.4627

0.4247

0.3899

0.3579

Free Cash Flow (USD)

10,152

9,994

16,308

19,783

24,025

Note: Cash flows same as forecast with interest rate-based exchange rates (Exhibit TN1)

EBIT 2015 (BRL)

128,658

EBIT 2015 (USD)

46,049

TV—Multiple

230,247

PV TV

121,543

PV Planning

52,339

Enterprise Value (USD)

173,881

Source: Created by case writer.

-6- UVA-F-1578TN

Exhibit TN4

MILAGROL LTDA.

Valuation Analysis—Political Risk, Devaluation or Expropriation

(numbers in thousands of USD or BRL)

2010

2011

2012

2013

2014

2015

Free Cash Flow (BRL)

20,144

21,601

38,397

50,739

67,124

Major Devaluation in 2013

Amount of Devaluation

20%

(assumed)

Probability of Devaluation

15%

(assumed)

Exchange Rate Forecast

0.5490

0.5040

0.4627

0.4247

0.3899

0.3579

Exchange Rate with Devaluation

0.5490

0.5040

0.4627

0.3398

0.3119

0.2863

Probability Weighted Exch. Rate

0.5040

0.4627

0.4120

0.3782

0.3472

Free Cash Flow (USD)

10,152

9,994

15,819

19,189

23,304

EBIT 2015 (BRL)

128,658

EBIT 2015 (USD)

44,668

TV—Multiple

223,339

PV TV

126,729

PV Planning

53,710

Enterprise Value (USD)

180,438

Serious Expropriation of Terminal Value

(effect is captured by adjusting the present value of terminal value)

Probability of Expropriation

10%

Proportion Expropriated

50%

Implied Future Spot Rates

0.5490

0.5040

0.4627

0.4247

0.3899

0.3579

Converted Free Cash Flows

10,152

9,994

16,308

19,783

24,025

EBIT 2015 (BRL)

128,658

EBIT 2015 (USD)

46,049

TV—Multiple

230,247

Expropriation Adjusted TV

218,734

PV TV

124,116

PV Planning

54,844

Enterprise Value (USD)

178,960

Source: Created by case writer.

-7- UVA-F-1578TN

Exhibit TN5

MILAGROL LTDA.

Valuation Analysis—Political Risk, Devaluation

(numbers in thousands of USD or BRL)

Long-Term Growth (BRL)

8.00%

2010

2011

2012

2013

2014

2015

2016

Net Operating Profit after Tax (BRL)

42,730

52,579

65,849

81,687

90,060

99,066

Less: Change in NWC

5,647

7,817

6,927

7,809

5,788

6,225

Less: Change in NPPE

16,938

23,161

20,525

23,139

17,149

18,446

Free Cash Flow

20,144

21,601

38,397

50,739

67,124

74,396

Net Working Capital

28,265

33,913

41,730

48,657

56,466

62,254

68,479

Net Property, Plant, and Equip.

83,544

100,482

123,643

144,168

167,307

184,456

202,901

BRL Discount Rate

Discount Rate

22.00%

Terminal Value (BRL)

619,743

PV Terminal Value

229,264

PV Planning

99,898

Enterprise Value

329,162

Enterprise Value (USD)

180,710

USD Discount Rate

Exchange Rate

0.5040

0.4627

0.4247

0.3899

0.3579

0.3286

Free Cash Flow (USD)

10,152

9,994

16,308

19,783

24,025

24,444

Long-Term Growth (USD)

0.98%

(implied by interest rates and BRL growth)

Terminal Value

221,819

PV Terminal Value

125,866

(same as above converted at spot rate)

PV Planning

54,844

(same as above converted at spot rate)

Enterprise Value

180,710

Alternate Consistent Assumptions for Terminal Value

USD

BRL

Typical 10-Year Interest

5.00%

8.00%

(both given)

Discount Rate

12.00%

15.20%

(USD given, BRL implied)

Growth Rate

4.00%

6.97%

(USD given, BRL implied)

Exchange Rate 2015

0.3579

(given)

Exchange Rate Implied 2016

0.3480

(implied)

Analysis BRL

Analysis USD

Free Cash Flow 2016 (BRL)

74,396

Free Cash Flow 2016 (USD)

25,888

Terminal Value 2015

904,112

Terminal Value 2015 (USD)

323,601

Terminal Value 2015 (USD)

323,601

Source: Created by case writer.

-8- UVA-F-1578TN

Exhibit TN6

MILAGROL LTDA.

Valuation Analysis—Irrelevance of Inflation When Markets Are in Parity

(numbers in thousands of USD or BRL)

Choose Inflation First Year

4%

Analysis assumes BRL inflation declines 2% in 2012

Analysis assumes risk-free cash flows—so cash flows discounted at interest rates

2011

2012

2013

Inflation BRL

4.00%

2.00%

2.00%

Real Rate of Return

2.00%

2.00%

2.00%

Interest Rate (Properly compounded)

6.08%

4.04%

4.04%

Interest Rate on USD

3.22%

3.22%

3.22%

Cash Flows Real (BRL)

100,000

100,000

100,000

Cash Flows Nominal (BRL)

104,000

106,080

108,202

Current Spot Rate

0.5490

Forecast Exchange Rate

0.5342

0.5300

0.5258

(1) Discount then Convert

Present Value—Nominal at Nominal (BRL)

288,388

Dollar Value

158,325

Present Value—Real at Real (BRL)

288,388

Dollar Value

158,325

(2) Convert then Discount

Cash Flows (USD)

55,557

56,221

56,894

PV

158,325

Note: Whatever rate is chosen for inflation, value never changes; the key is that PV of real cash flows at real

rate is unchanged.

Source: Created by case writer.