The CASE Journal Volume 5, Issue 2 (Spring 2009)

admonishes firms to have the “discipline needed to set priorities for which markets to serve with

which benefits and features” (p. 11). Day also points out the importance of a customer focus.

Krill and her staff spent time with the ANN customers in 2005 when she was spearheading the

brand book development. (See Case Section 6: Ann Taylor’s Brand Identity.) How much time is

being spent with the customers now?

AS AN OPTIONAL ASSIGNMENT OR IN-CLASS EXERCISE: Although not mentioned in

the case, ANN’s Q1 2008 earnings conference call in May 2008, available for students to read at

http://seekingalpha.com/article/78473-ann-taylor-stores-corp-q1-2008-earnings-call-transcript,

and listen to at http://investor.anntaylor.com, is informative because Krill admits that ANN had

lost touch with its customer, especially the AT client.

What should Krill do as of mid-2008? There is no right or wrong answer to this final question.

Hence, the only difference between better and average students in terms of their content will lie

in their ability to make inferential leaps and propose reasonable recommendations for future

action.

Some of those recommendations might include the following:

• Discontinue the beauty business (this becomes a hard trade-off if the fragrance line is

working).

• Combine both LOFT and AT merchandise in one Factory concept store, marketed as

“off-the-rack” discounted items (saves on the need for investment in exterior architecture

differentiation, store display, and signage).

• Remove the Ann Taylor name from LOFT (like GAP did with Old Navy and Banana

Republic).

• Don’t spend time and resources on the separate “older women” concept. Instead, spend

time keeping close watch on customer trends, and include a wide range of boomer

fashions as part of the AT and LOFT merchandise offerings.

• Hire creative and capable merchandising managers and delegate appropriately so Krill

isn’t spread so thin.

• Revere the roots of the original Ann Taylor concept: the original brand is the most

valuable resource the company has. Position AT as the premier destination. Pursue

market penetration as the growth strategy.

• Remember, differentiation is all about hard choices and creating a value proposition that

targeted customers can’t ignore. ANN may currently be “stuck in the middle”, trying to

do too many things in too many markets with too few appropriate resources and

capabilities (especially in the human resource area). It seems that specialty retailers try to

follow each other’s lead too much. If someone can break from the crowd, that firm might

grab the lion’s share of the market.

TCJ05-02-02TN

31

For use in conjunction with Strategic Management 13E, Pearce & Robinson. Expiry date 2015.

The CASE Journal Volume 5, Issue 2 (Spring 2009)

SELECTED EXHIBITS/HANDOUTS

Exhibit A: Ann Taylor Stores Corp.

Selected Ratio Analysis for Fiscal Year Ended

LIQUIDITY Jan08 Jan07 Jan06 Jan05 Jan04

Current Ratio 1.62 2.31 2.63 2.41 3.57

Quick Ratio 0.51 1.26 1.54 1.10 2.16

Working Capital Per Share 3.20 5.64 5.77 4.86 6.11

Cash Flow Per Share 3.52 3.59 2.42 2.01 2.24

(Using Annual Statement of Cash Flows)

ACTIVITY

Inventory Turnover 4.25 4.47 4.26 4.12 N/A

Receivables Turnover 143.36 139.54 139.78 148.00 N/A

Total Asset Turnover 1.62 1.53 1.47 1.50 N/A

Average Collection Period (Days) 2.51 2.58 2.58 2.43 N/A

Days to Sell Inventory (Days) 84.76 80.47 84.55 87.30 N/A

Operating Cycle (Days) 87.27 83.05 87.13 89.73 N/A

PERFORMANCE

Sales/Net Property, Plant & Equipment 4.27 4.27 4.15 4.04 4.27

Sales/Stockholder Equity 2.85 2.85 2.23 2.00 2.00

PROFITABILITY

Operating Margin Before Depr 12.70 14.07 11.62 9.91 14.08

or EBITDA Margin (%)

Operating Margin After Depr (%) 7.83 9.55 7.09 5.66 10.81

Pretax Profit Margin (%) 6.72 10.19 6.67 5.74 10.60

Net Profit Margin (%) 4.06 6.10 3.95 3.41 6.36

Tax Rate, Effective (%) 39.62 40.12 40.78 40.50 40.02

Return on Assets (%) 6.98 9.12 5.48 4.77 8.76

Return on Equity (%) 11.58 13.62 7.91 6.83 12.15

Return on Average Assets (%) 6.56 9.34 5.81 5.10 17.53

Return on Average Equity (%) 10.29 13.72 8.35 7.20 24.30

LEVERAGE

Interest Coverage Before Tax 75.14 108.08 67.38 30.21 26.25

Interest Coverage After Tax 45.77 65.12 40.30 18.38 16.15

Long-Term Debt/Common Equity (%) 0.00 0.00 0.00 0.00 0.15

Long-Term Debt/Shareholder Equity (%) 0.00 0.00 0.00 0.00 0.15

Total Debt/Total Assets (%) 0.00 0.00 0.00 0.00 0.11

Total Assets/Common Equity 1.66 1.49 1.44 1.43 1.39

DIVIDENDS

Dividend Payout (%) 0.00 0.00 0.00 0.00 0.00

Source: Standard & Poor’s

TCJ05-02-02TN

32

For use in conjunction with Strategic Management 13E, Pearce & Robinson. Expiry date 2015.

The CASE Journal Volume 5, Issue 2 (Spring 2009)

Exhibit B: Definitions of Ratio Analysis Calculations

LIQUIDITY DEFINITION

(Using Annual Statement of Cash Flows)

ACTIVITY

Inventory Turnover = COGS / Average Inventory*

Receivables Turnover = Sales / Average Total Receivables

Total Asset Turnover = Sales / Average Total Assets

Average Collection Period (Days) = 360 / Receivables Turnover

Days to Sell Inventory (Days) = 360 / Inventory Turnover

PERFORMANCE

Sales/Net Property, Plant & Equipment Self Explanatory

Sales/Stockholder Equity Self Explanatory

PROFITABILITY

Operating Margin Before Depr = (Operating Income + Depreciation, Amortization & Depletion) / Sales

or EBITDA Margin (%)

Operating Margin After Depr (%) = Operating Income / Sales

Pretax Profit Margin (%) = Pretax Income / Sales

Net Profit Margin (%) = Net Income / Sales

LEVERAGE

Interest Coverage Before Tax = (Pretax Income + Interest Expense) / Interest Expense

Interest Coverage After Tax = (Net Income + Interest Expense) / Interest Expense

Long-Term Debt/Common Equity (%) Self Explanatory

Long-Term Debt/Shareholder Equity (%) Self Explanatory

Total Debt/Total Assets (%) Self Explanatory

Total Assets/Common Equity Self Explanatory

TCJ05-02-02TN

33

The CASE Journal Volume 5, Issue 2 (Spring 2009)

Handout A: Selected Financial Data: Current Competitor Comparison

Selected Financial Data: Current Competitor Comparison

Data as of 7/11/2008

CWTR ANN CHS TLB Industry

Market Cap: 441.83M 1.24B 859.27M 591.88M 400.65M

Key Employees: 3,394 5,500 5,720 6,300 3.14K

Qtrly Rev Growth (yoy): 3.60% 2.00% 9.60% 5.40% 5.10%

Revenue (ttm): 1.14B 2.41B 1.67B 2.26B 1.48B

Gross Margin (ttm): 36.32% 52.13% 54.95% 40.01% 31.68%

EBITDA (ttm): 12.29M 302.01M 159.38M 127.11M 70.97M

Oper Margins (ttm): 3.81% 7.60% 3.80% 0.24% 2.39%

EPS (ttm): 0.258 1.495 0.309 3.624 0.54

P/E (ttm): N/A 14.05 15.76 N/A 15.04

PEG (5 yr expected): N/A 0.8 0.98 0.79 0.91

P/S (ttm): 0.38 0.52 0.50 0.26 0.39

Industry = Apparel Stores.

Releases and SEC filings are posted.)

TCJ05-02-02TN

34

For use in conjunction with Strategic Management 13E, Pearce & Robinson. Expiry date 2015.

The CASE Journal Volume 5, Issue 2 (Spring 2009)

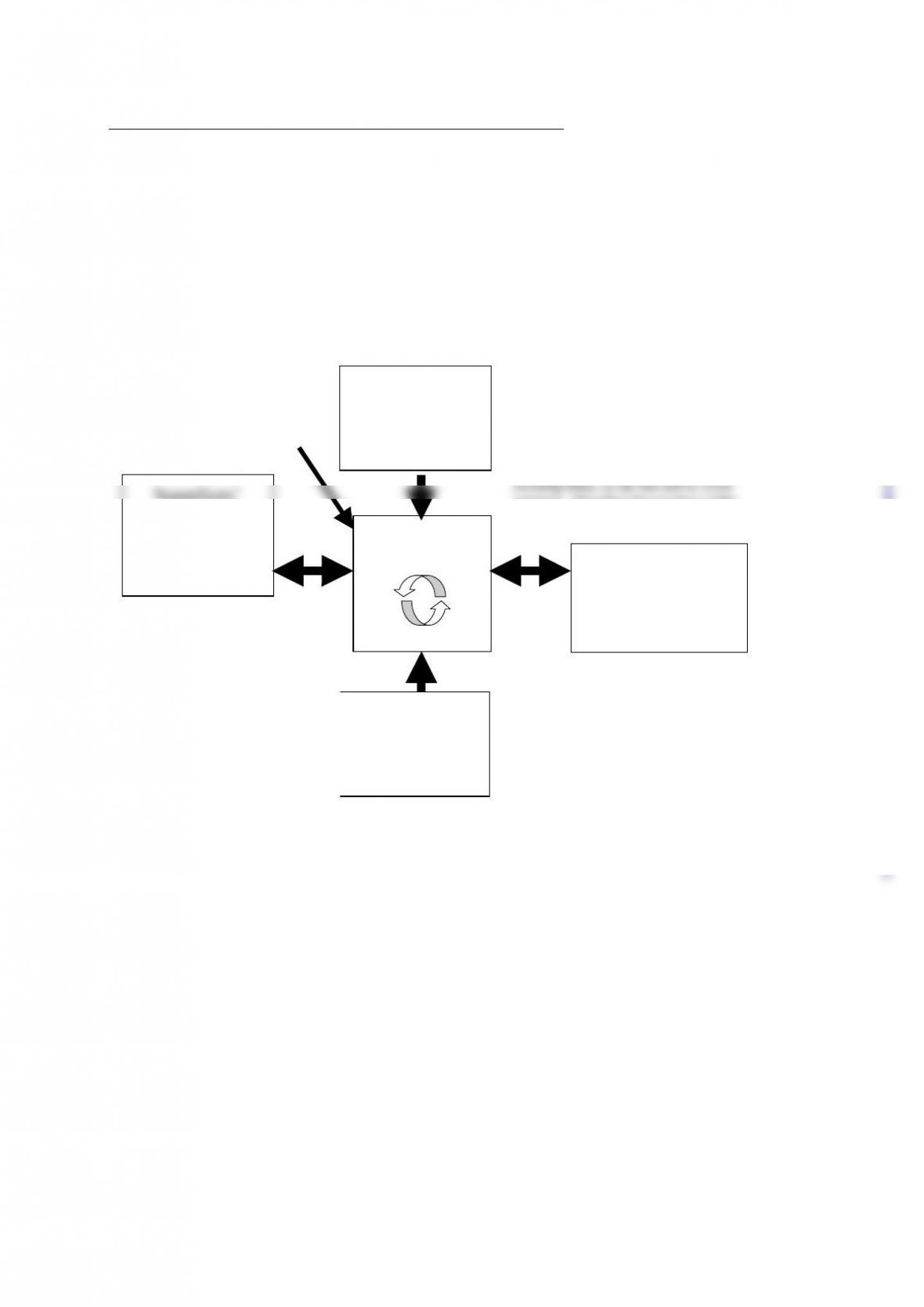

Handout B: Porter’s Five Forces Analysis

Porter’s Five Forces Analysis

Rivalry

High

Threat of

Substitutes

Low

Buyers’

Bargaining

Power

Low

Threat of

New Entrants

Med-High

Suppliers’

Bargaining

Power

Low

Suggested: There are no real substitutes

for a woman’s career wardrobe.

Suggested: The industry has low

concentration with many rivals

competing for market share. Some

p

roduct differentiation exists, but

a lack of switching costs means

firms will compete to steal

customers.

Suggested: Retail Buyers have many

choices of retailers and clothing lines.

However many women’s specialty

stores design their own private label

retailers. Therefore buyers have little

p

ower.

Suggested: At the regional level, entry

is not difficult as a retailer can enter as

small scale with little capital and be

able to find raw materials/suppliers

and target consumers. Likely entry is

from expansion of existing

competitors (similar to what ANN did

with LOFT). However, at a national

level, entry is more difficult.

Suggested: Given that there are

many supplier firms and that there

is a lack of differentiation between

them, their power is lowered. Some

switching costs may exist if the

clothing buyer changes suppliers,

but the costs are manageable. Lots

of capacity exists in Asia and

suppliers have few alternative

markets in which to sell their

p

roducts, reducing their power.

TCJ05-02-02TN

35

The CASE Journal Volume 5, Issue 2 (Spring 2009)

TEACHING NOTE REFERENCES

(and possible additional assigned readings)

Aaker, D.A. 2007. Strategic Market Management, 8th edition, Wiley & Sons.

Marketing, 54(1): 27-41.

Ansoff, H.I. 1957. “Strategies for diversification”. Harvard Business Review, 35(5): 113-124.

Barney, J. 1991. “Firm resources and sustained competitive advantage”, Journal of Management,

17(1): 99-120.

14.

Grant, R.M. 1991. “The resource-based theory of competitive advantage: Implications for

strategy formulation”, California Management Review, 33(3): 114-135.

O’Riordan, C. 2006. “Using the VRIO framework in practicing firms taking the resource-based

view (RBV)”, Accountancy Ireland, 38(3): 42-44.

Porter, M.E. 1985. Competitive Advantage: Creating and sustaining superior performance. New

York: The Free Press. (Republished with a new introduction, 1998.)

Porter, M.E. 1996. “What is strategy?”, Harvard Business Review, 74(6): 61-78.

Porter, M.E. 2008. “The five competitive forces that shape strategy”, Harvard Business

Review,86(1): 78-93.

Prahalad, C.K. & Hamel, G. 1990. “The core competence of the corporation”, Harvard Business

Review, 68(3): 79-91

TCJ05-02-02TN

36

The CASE Journal Volume 5, Issue 2 (Spring 2009)

i Letter to Shareholders, ANN 2007 Annual Report, at

http://investor.anntaylor.com/phoenix.zhtml?c=78167&p=irol-reportsAnnual

ii This article is also available in the Handbook of Niche Marketing, by Tevfik Dalgic, published in 2006 by Haworth

Press, with a preview at

TCJ05-02-02TN

37

For use in conjunction with Strategic Management 13E, Pearce & Robinson. Expiry date 2015.