1. “How does APEI compare to the University of Phoenix?”

The companion case in the book is on The Apollo Group – University of Phoenix. They

provide an interesting two case set to discuss. UOP is the big player in this working

The information provided on the next page is available to you but has not been provided

2006

2007

2008

2009

2010

REVENUE in millions

APEI Revenue in millions

$40

$69

$107

$149

$198

Growth Rate

73%

55%

39%

33%

UOP Revenue in millions

$2,478

$2,724

$3,133

$3,954

$4,926

Growth Rate

10%

15%

26%

25%

UOP vs. APEI in Revenue

$2,438

$2,655

$3,026

$3,805

$4,728

[UOP Rev is $ ___ more than APEI’s]

UOP ÷ APEI on size of Rev.

62Xs

39Xs

29Xs

27Xs

25Xs

[UOP Rev is ___ Xs APEI Rev]

COSTS AS % OF REVENUE:

Instructional cost as % rev.

APEI

44.8%

42.6%

40.7%

39.2%

38.0%

UOP

44.8%

45.4%

43.1%

39.7%

43.1%

Selling and Promotional

APEI

12.2%

9.8%

11.5%

13.7%

17.3%

UOP

22.0%

24.2%

25.6%

24.1%

22.6%

General and

Admin

APEI

22.8%

22.2%

19.9%

16.8%

16.2%

UOP

6.2%

7.4%

7.2%

6.8%

7.2%

Litigation, writeoffs, fines

APEI

7.9%

0.0%

0.0%

0.0%

0.0%

UOP

0.0%

2.0%

3.6%

Operating Income

APEI

7.3%

25.4%

24.0%

26.8%

25.2%

UOP

26.2%

23.0%

24.5%

27.0%

20.5%

Net Income [after tax]

APEI

4.5%

25.4%

15.1%

16.2%

15.1%

UOP

16.7%

15.0%

15.1%

15.2%

11.2%

APEI has higher revenue growth, as would be expected with a much smaller base. The

Instructional costs are similar, although APEI’s are steadily dropping % of Rev wise,

while the UOP is seeing a significant increase, probably due to efforts to keep classes

General and Admin is interesting. UOP is doing much better than APEI here. Part is the

large revenue base over which UOP can allocate admin responsibilities. APEI’s is

Operating income is rather similar for both – mid twenties as a percent of revenue.

recruitment; advisement; class-based oversight; etc.

UOP is much closer to dangerous regulatory thresholds like the 90/10 rule than APEI,

which in turn means the UOP has to focus on adjusting its student composition, raise its

tuition, increase its admission standards, and discourage student borrowing in order to

regard.

A third, interesting question in this regard, given The Apollo Group’s use of acquisition

for expansion from time to time, is the possibility of them looking to acquire APEI as an

Related to this third notion, the opposite interesting question might be, “Is APEI

positioning itself to be bought by UOP [The Apollo Group] at some future date?”

The key, attractive thing for APEI, relative not only to UOP but to all the other public

for many players in the industry, or in complementary industries. It’s 2010AR made

this observation regarding the impetus for all the U.S. DOE’s Title IV and recruiting

investigations, making particular note in the comment of the fact that APEI was NOT

chosen for investigation:

congressional investigation into for-profit institutions. In 2010, both the U.S. Senate and the

U.S. House of Representatives held separate hearings related to for-profit postsecondary

education institutions. In addition, the Government Accountability Office released a report in

2010 based on a three-month undercover investigation of recruiting practices at forprofit

Nonetheless, as is pointed out in the case, APEI is also feeling [and concerned about] the

attention other competitors are placing on “its” military market; and apparently starting to

feel that attention may be the reason behind a slowing of APEI’s growth rate in new

course registrations among its military customer target market. They had this to say in

their 2010AR:

(except for certain institutional loans) for any fiscal year, more than 90% of its revenues (as

computed for 90/10 Rule purposes). We believe that for-profit schools are increasingly

seeking to attract military students in order to comply with the 90/10 Rule, as currently DoD

tuition assistance and veterans education benefits do not count towards the 90% limit.”

2. Greater discussion of the 90/10 rule; the gainful employment rule; student default

and the cohort default rate; and recruitment/enrollment practice regulation could be

Rather than repeating some of the analytical guidance on the issues we have provided

APEI because the majority of its students work fulltime in the military or civilian

public sector jobs].

It is important to note, however, that APEI’s continued effort to grow in the civilian

“Since the founding of American Military University, we have gradually transitioned from a

military focus to a more broad-based focus on the military and public services communities.

We expect the percentage of our students that are not eligible for tuition assistance programs

of the Department of Defense or DoD to continue to increase, particularly as a result of our

student body.”

3. Where you have members of the military in your class, it is an excellent added

our most dedicated, talented students in our strategy classes. Let them know in the

4. While as noted above expansion into public service communities will introduce some

change in its military intensive focus, it is still unlikely that such a focus will

dramatically change for some time to come. APEI’s 2010AR offers some interesting

commentary that you might find useful to read here as a preparation reference before

“There are more than 2.2 million active and reserve military professionals in the United States

Armed Forces. Each year, approximately 300,000 new service members are enlisted or

commissioned to replace retiring and separating members. We believe that the unpredictable

and demanding work schedules of military personnel and their geographic distribution make

level eligibility requirements for assignments, promotions, and service schools, and entering

remarks on performance appraisals.

Active duty and reserve component military personnel are eligible for tuition assistance

costs above the DoD limits through the GI Bill’s Top-Up feature. Most military veterans are

also eligible to use their GI Bill entitlements in continuing their education after retirement or

separation. We believe that national security, homeland security, and public safety

professionals also represent a large and growing market for online education. As with their

traditional universities”.

5. And, APEI remains unquestionably committed to an online only focus. In their

“Within the postsecondary education market, we believe that there is significant opportunity

adult, to distance learning.”

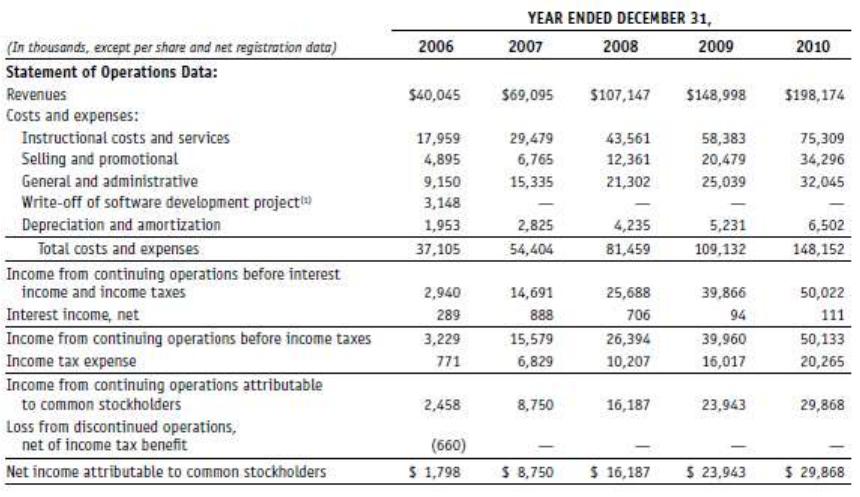

6. Finally, the financials provided in the case and analyzed for you above in item # 1c

are reproduced on the next few pages for your convenience:

Percent of Sales Analysis

2006

2007

2008

2009

2010

REVENUES

100.0%

100.0%

100.0%

100.0%

100.0%

Costs and Expenses

Instructional Costs & Services

44.8%

42.6%

40.7%

39.2%

38.0%

Selling and Promotional

12.2%

9.8%

11.5%

13.7%

17.3%

General and administrative

22.8%

22.2%

19.9%

16.8%

16.2%

Write off software

developmt

7.9%

Depreciation and Amortiz.

4.9%

3.9%

3.5%

3.3%

Total Costs and Expenses

92.6%

74.6%

76.0%

73.2%

74.8%

Income from oprns before II &

Txs

7.3%

25.4%

24.0%

26.8%

25.2%

Interest Income, net

0.7%

0.6%

0.1%

0.1%

Income from perations bef.

Taxes

8.1%

25.4%

24.6%

26.9%

25.3%

Income Tax Expense

1.9%

9.5%

10.7%

10.2%

Income from continuing

operations

6.1%

25.4%

15.1%

16.2%

15.1%

Loss from discontinued

operations

–1.6%

NET INCOME

4.5%

25.4%

15.1%

16.2%

15.1%

APEI CONSOLIDATED BALANCE SHEET [in thousands]

2006

2007

2008

2009

2010

ASSETS

Current Assets

Cash and cash equivalents

$ 11,678

$ 26,951

$ 47,714

$ 74,866

$ 81,352

Accounts receivable, net

$ 5,448

$ 4,896

$ 6,188

$ 8,664

10,269

Prepaid Expenses

$ 856

$ 1,596

$ 2,156

$ 2,990

$ 4,233

Income tax receivable

$ 679

$ 1,089

$ 1,306

$ 863

$ 780

Deferred income taxes

$ 299

$ 309

$ 640

$ 999

$ 1,369

Total current assets

$ 18,960

$ 34,841

$ 58,004

$ 88,382

$ 98,003

Property and Equipment, net

$ 9,363

$ 13,364

$ 19,662

$ 25,294

$ 42,415

Other assets

$ 427

$ 775

$ 1,187

$ 2,077

$ 1,421

Total assets

$ 28,750

$ 48,980

$ 78,853

$ 115,753

$ 141,839

LIABILITIES &

STOCKHOLDER EQTY

Current Liabilities

Accounts payable

$ 1,502

$ 2,471

$ 4,946

$ 6,756

$ 9,422

Accrued liabilities

$ 3,165

$ 2,770

$ 5,250

$ 8,003

$ 9,349

Accrued bonuses

$ 1,553

$ 1,825

Deferred rev. & student deposits

$ 3,852

$ 6,614

$ 9,626

$ 14,204

$ 18,815

Current portion of L-term debt

$ 29

Total current liabilities

$ 8,548

$ 13,408

$ 21,647

$ 28,963

$ 37,586

Deferred Taxes

$ 1,437

$ 2,065

$ 3,691

$ 4,772

$ 6,953

Long-term debt

$ 1,944

Total Liabilities

$ 11,929

$ 15,473

$ 25,338

$ 33,735

$ 44,539

Commitments & Contingencies

Stockholder equity

$ 118

$ 177

$ 180

$ 183

$ 186

Additional paid-in capital

$ 26,378

$ 128,005

$ 132,078

$ 136,380

$ 141,757

Less share repurchase

$ (295)

$ (19,966)

Accumulated deficit

$ (9,675)

$ (94,675)

$ (78,488)

$ (54,545)

$ (24,677)

Total stockholders’ equity

$ 16,821

$ 33,507

$ 53,475

$ 82,018

$ 97,300

Total Liabilities & Stockhldrs’

equity

$ 28,750

$ 48,980

$ 78,813

$ 115,753

$ 141,839