S9–5 (continued)

Req. 2 (continued)

unnecessary costs associated with renegotiating the terms of its loan to the company—

renegotiations that could ultimately reveal that the company is generating sufficient cash

flows to repay the loan (despite what net income suggests under the alternative

S9–6

One way to evaluate a company’s success is to look for trends in its financial results.

The trend in Fast Corporation’s earnings is a positive one, suggesting that Fast has

improved its management of operations. In contrast, the slight decline in earnings for

(1) different assets were acquired at different costs, (2) different estimates are used for

useful lives, (3) different estimates are used for residual values, and (4) different

depreciation methods are used. The first potential explanation can be ruled out because

the case indicates that the companies “use very similar assets.” Among the remaining

three possibilities, the most likely explanation is that different depreciation methods are

S9–6 (continued)

The prior analysis would probably get you an interview with the Wall Street firm. If you

extended your analysis as shown below, you’d likely get the job without an interview.

The analysis can be taken even deeper yet, by breaking apart gains (losses) on fixed

asset disposals. The equation for computing a gain (or loss) subtracts the book value

AD – Gain (Loss) = C – SP.

Now, using last year and current year numbers for Fast in the above equation, you can

determine the following:

AD – Gain (Loss) = C – SP

($10,667 + 3,555) – 2,222 = C – SP

$30,000 and Fast has earned total income of $30,000.)

The above analysis relies on two key assumptions: (1) it assumes that both companies

disposed of identical equipment, and (2) the numbers used above actually assume that

both companies sold all of their equipment. While unrealistic, these assumptions allow

the analysis to demonstrate the key point of all this: differences in depreciation affect

S9–6 (continued)

A more informed decision could be made if the companies’ depreciation methods and

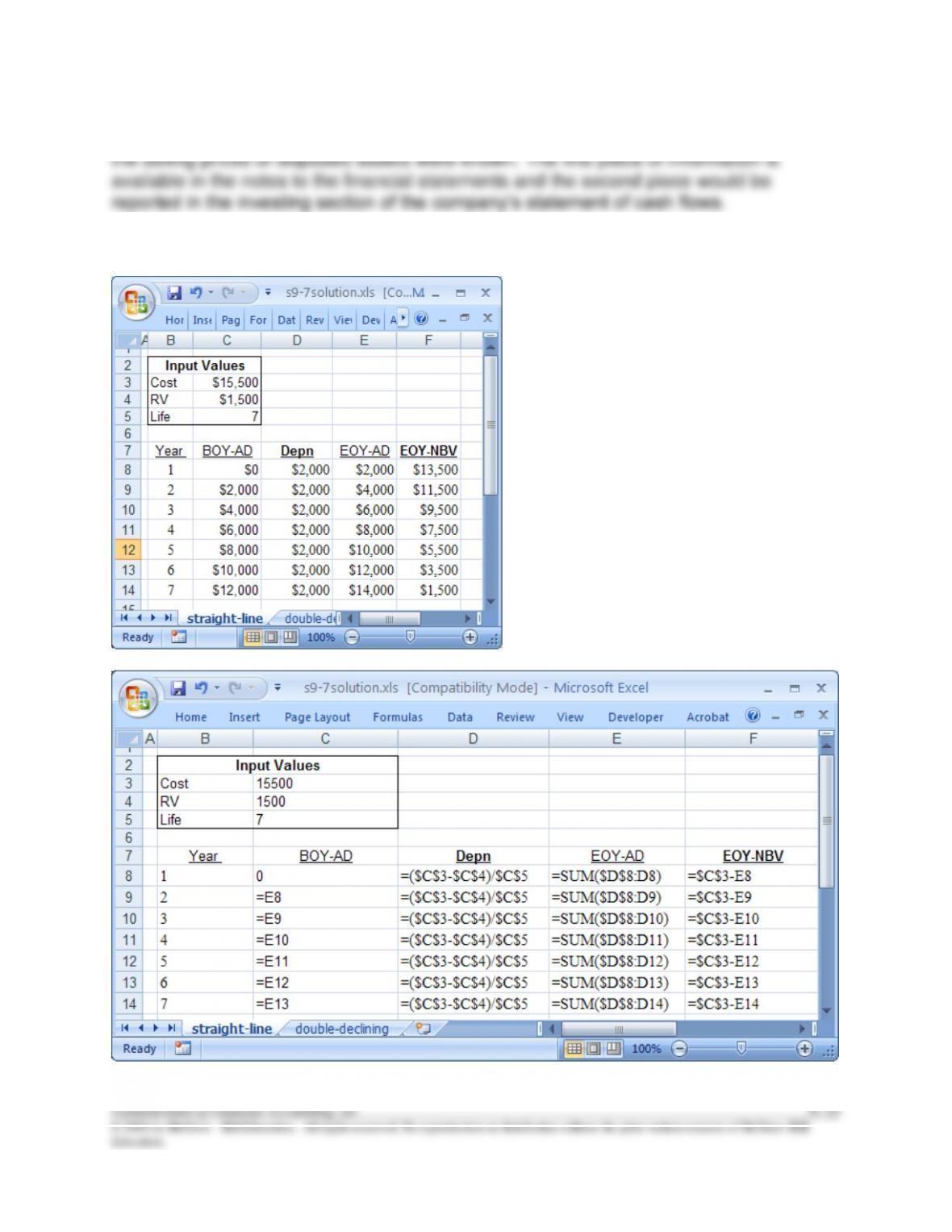

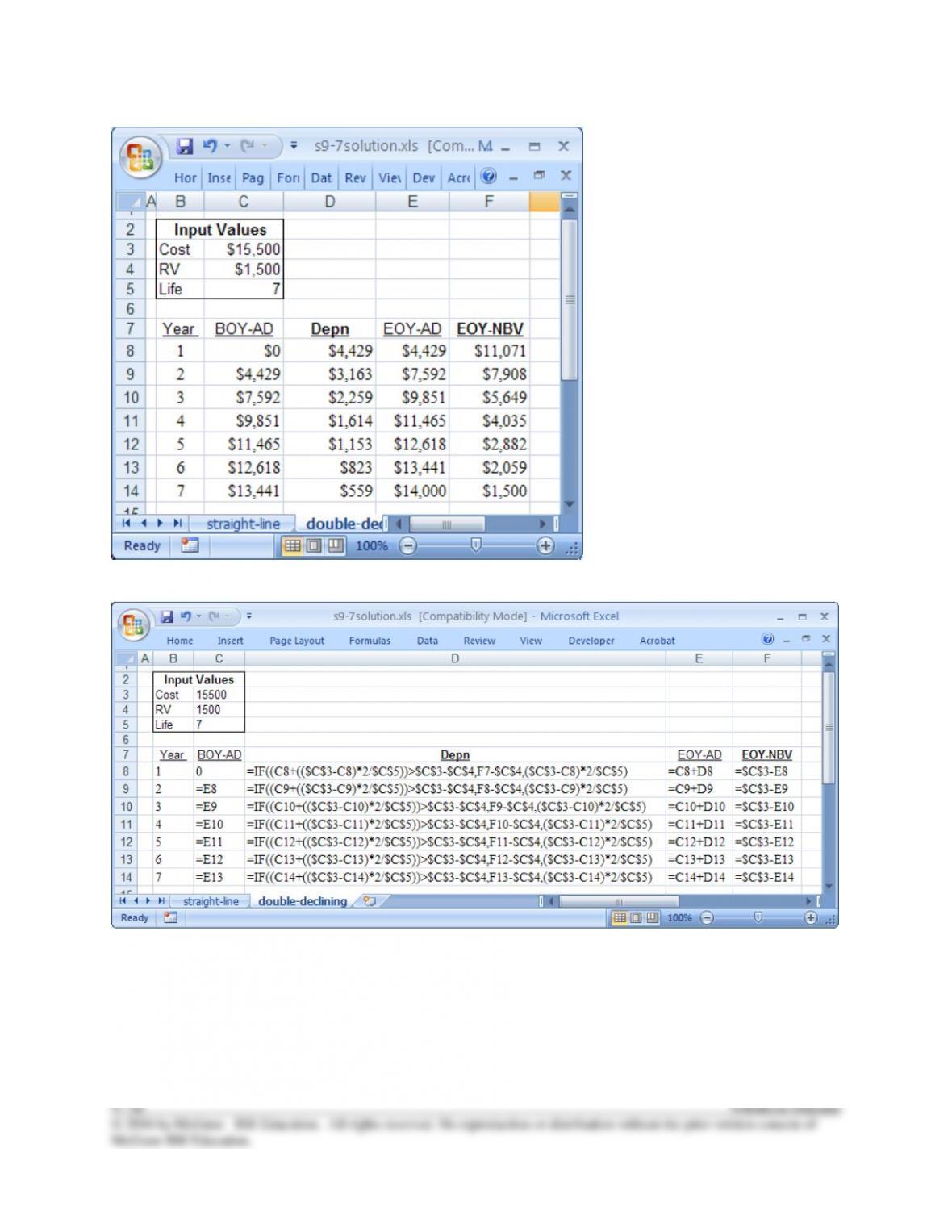

S9–7

S9–7 (continued)

ANSWERS TO CONTINUING CASE

CC9-1

Req. 1

a. Straight-line:

Year

Computation

Depreciation

Expense

Accumulated

Depreciation

Book

Value

At Acquisition

$7,000

Year 1

($7,000 – $500) X 1/5

$1,300

$ 1,300

5,700

Year 2

($7,000 – $500) X 1/5

1,300

2,600

4,400

Year 3

($7,000 – $500) X 1/5

1,300

3,900

3,100

Year 4

($7,000 – $500) X 1/5

1,300

5,200

1,800

Year 5

($7,000 – $500) X 1/5

1,300

6,500

500

b. Units-of-production:

Year

Computation

Depreciation

Expense

Accumulated

Depreciation

Book

Value

At Acquisition

$7,000

Year 1

($7,000 – 500) x

3,100/13,000

$1,550

$1,550

5,450

Year 2

($7,000 – 500) x

2,500/13,000

1,250

2,800

4,200

Year 3

($7,000 – 500) x

3,400/13,000

1,700

4,500

2,500

Year 4

($7,000 – 500) x

2,200/13,000

1,100

5,600

1,400

Year 5

($7,000 – 500) x

1,800/13,000

900

6,500

500

c. Double-declining balance:

Year

Computation

Depreciation

Expense

Accumulated

Depreciation

Book

Value

At Acquisition

$7,000

Year 1

($7,000 – $0) X 2/5

$2,800

$2,800

4,200

Year 2

($7,000 – $2,800) X 2/5

1,680

4,480

2,520

Year 3

($7,000 – $4,480) X 2/5

1,008

5,488

1,512

Year 4

($7,000 – $5,488) X 2/5

605

6,093

907

Year 5

($7,000 – $6,093) X 2/5

407*

6,500

500

*Even though the computation yields $362.80, $407 should be recorded as depreciation

expense because the equipment is at the end of its useful life (5 years); the ending book

value must be at the $500 residual value at the end of its useful life.

CC9-1 (continued)

Req. 2

Straight line method

Cash Received

$

2,100

Original cost of hydrotherapy tub system

$7,000

Less: Accumulated depreciation (3 years)

3,900

Book value at date of sale

3,100

Loss on sale of hydrotherapy tub system

$

(1,000)

Cash ………………………………………………………………..

Accumulated Depreciation ……….……………………………...

Loss on Disposal …………………………………………………

Equipment ……………..……………………………………..

2,100

3,900

1,000

7,000

Units–of-production method:

Cash Received

$

2,100

Original cost of hydrotherapy tub system

$7,000

Less: Accumulated depreciation (3 years)

4,500

Book value at date of sale

2,500

Loss on sale of hydrotherapy tub system

$

(400)

Cash ……………………………………………………………....….

Accumulated Depreciation ………………………………………..

Loss on Disposal ……………….…….…….…….…….…….…...

Equipment ……………………………………………………..

2,100

4,500

400

7,000

Double-declining balance method:

Cash Received

$

2,100

Original cost of hydrotherapy tub system

$7,000

Less: Accumulated Depreciation

5,488

Book value at date of sale

1,512

Gain on sale of hydrotherapy tub system

$

588

Cash ……………………………………………………………....….

Accumulated Depreciation ………………………………………..

Equipment ……………….……………………………………..

Gain on Disposal ………………….…….…….…….…….…...

2,100

5,488

7,000

588

CC9-1 (continued)

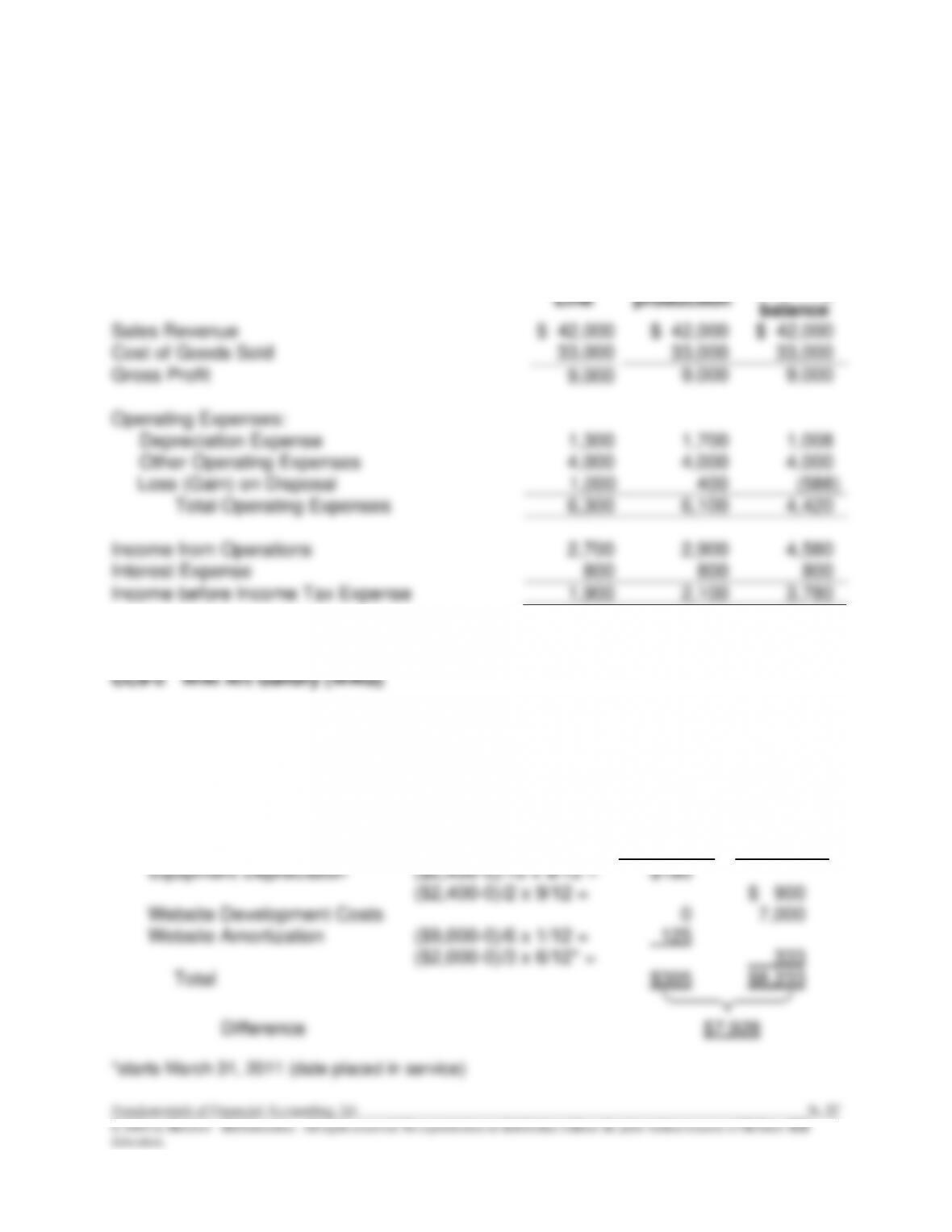

Req. 3

NICOLE’S GETAWAY SPA

(Forecasted) Income Statement

For Year 3

Straight

Line

Units-of–

production

Double-

declining

balance

Sales Revenue

Cost of Goods Sold

$ 42,000

33,000

9,000

$ 42,000

33,000

$ 42,000

33,000

Gross Profit

9,000

9,000

Operating Expenses:

Depreciation Expense

Other Operating Expenses

Loss (Gain) on Disposal

1,300

4,000

1,000

1,700

4,000

400

1,008

4,000

(588)

Total Operating Expenses

6,300

6,100

4,420

Income from Operations

Interest Expense

2,700

800

2,900

800

4,580

800

Income before Income Tax Expense

1,900

2,100

3,780

1. B

2. A

3. D

4. D (see computations below) Amount deducted

from net income

As reported

As restated

Equipment Depreciation

($2,400-0)/10 x 9/12 =

$180

($2,400-0)/2 x 9/12 =

$ 900

Website Development Costs

0

7,000

Website Amortization

($9,000-0)/6 x 1/12 =

125

($2,000-0)/3 x 6/12* =

333

Total

$305

$8,233

Difference

$7,928

*starts March 31, 2011 (date placed in service)