E9–13

(a)

Trademarks

Bal. 1,800

Purch. 216

31 Disposal

End. 1,985

Bal. 31

Amort. 7

(c)

Proceeds on disposal

$12

– Book value of asset sold

Cost

31

Accumulated Amortization

10

21

= Gain (loss) on disposal

$(9)

E9–14

Req. 1 Fixed asset turnover ratio: (dollars in millions)

Net

Sales

Average

Net Fixed Assets*

=

Fixed Asset

Turnover

2011

$108,249

($4,768 + $7,777) / 2

17.3

2012

$156,500

($7,777 + $15,450) / 2

13.5

2013

$170,910

($15,450 + $16,600) / 2

10.7

* [(Beginning net fixed assets + Ending net fixed assets) 2]

Req. 2

Apple’s fixed asset turnover ratio in 2013 was 10.7 which was greater than Microsoft’s

ratio of 8.5, suggesting that Apple is more efficient than Microsoft at using its investment

in fixed assets to generate revenue.

End. 28

E9–15

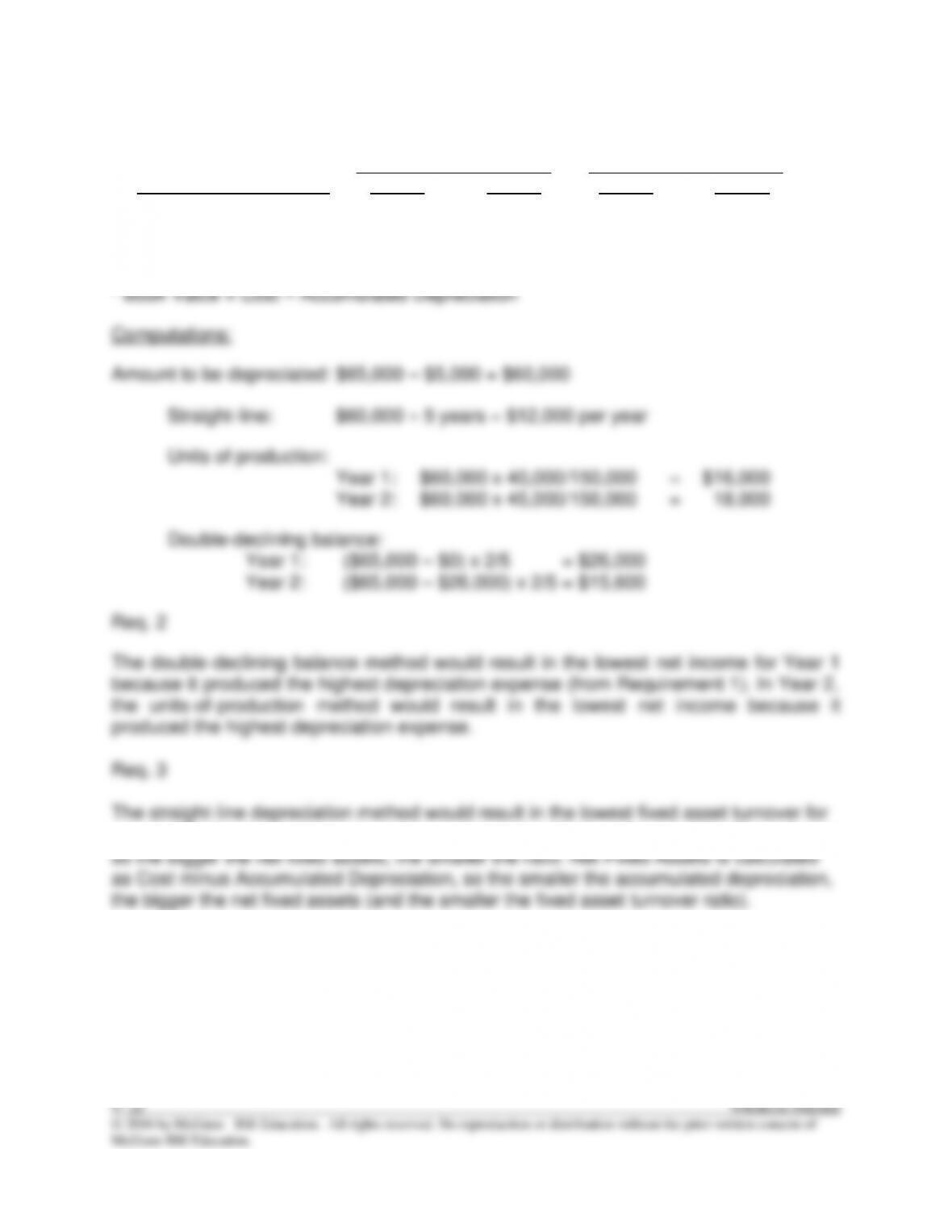

Req. 1

Depreciation Expense for

Book Value at End of *

Method of Depreciation

Year 1

Year 2

Year 1

Year 2

Straight-line ……………………..

$12,000

$12,000

$53,000

$41,000

Units-of-production ……………

16,000

18,000

49,000

31,000

Double-declining-balance …..

26,000

15,600

39,000

23,400

Year 1:

$60,000 x 40,000/150,000

=

$16,000

Year 2:

$60,000 x 45,000/150,000

=

18,000

Double-declining balance:

Year 1:

($65,000 – $0) x 2/5 = $26,000

Year 2:

($65,000 – $26,000) x 2/5 = $15,600

year 1. The fixed asset turnover ratio is calculated as Sales Average Net Fixed Assets,

E9–16

Year 1

Year 2

Year 3

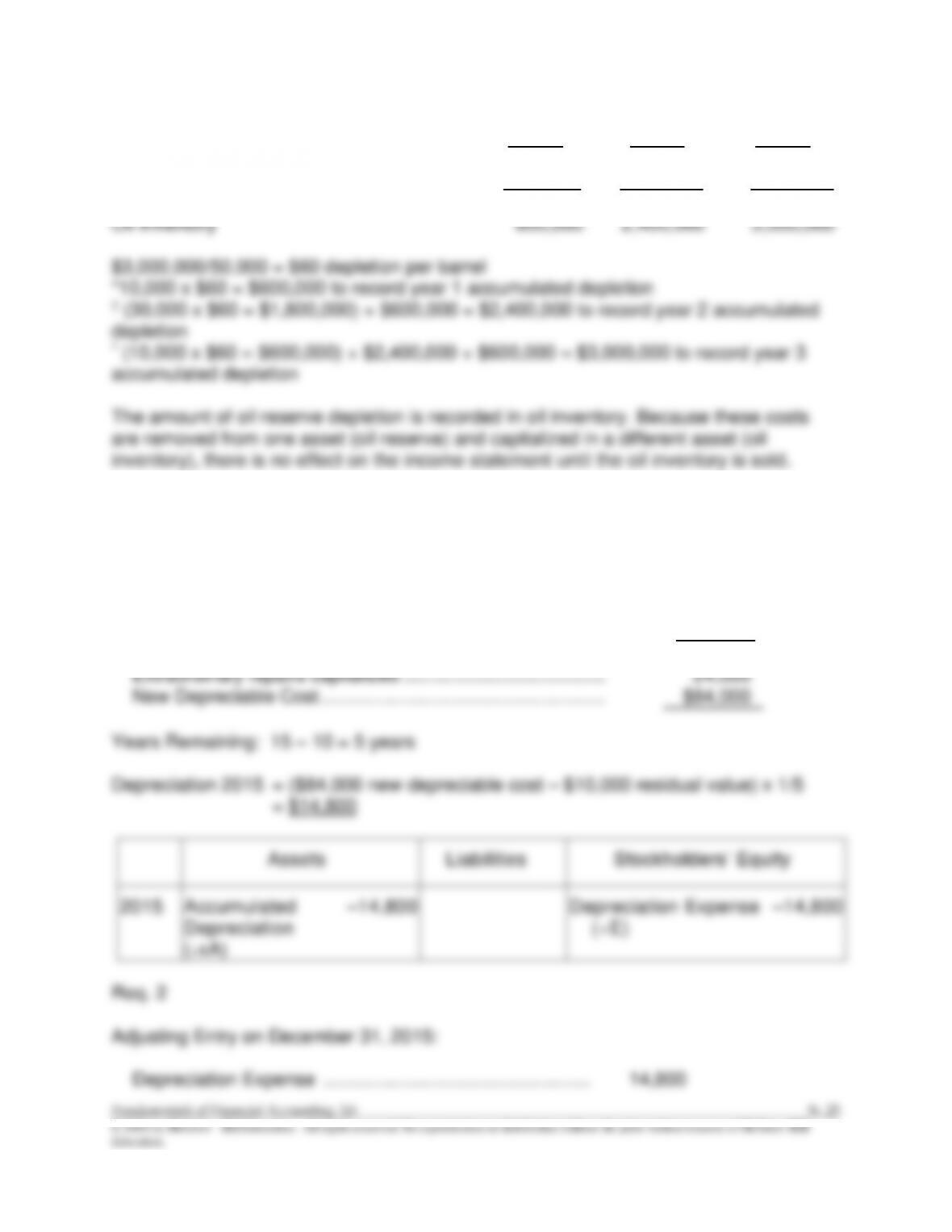

Oil Reserve

$ 3,000,000

$ 3,000,000

$3,000,000

Accumulated Depletion

600,000*

2,400,000†

3,000,000^

Oil Reserve, Net

2,400,000

600,000

0

Oil Inventory

600,000

2,400,000

3,000,000

E9–17

Req. 1

Equipment book value on January 1, 2015:

Original cost: …………………………………………………………

Accumulated Depreciation ………………………………………

Book value ……………………………………………………………

$160,000

(100,000)

60,000

Extraordinary repairs capitalized …………………………………

24,000

New Depreciable Cost ……………………………………………….

$84,000

Years Remaining: 15 – 10 = 5 years

Depreciation 2015 = ($84,000 new depreciable cost – $10,000 residual value) x 1/5

= $14,800

Assets

Liabilities

Stockholders’ Equity

2015

Accumulated

Depreciation

(+xA)

–14,800

Depreciation Expense

(+E)

–14,800

Req. 2

Adjusting Entry on December 31, 2015:

Depreciation Expense ……………………………………………

14,800

Accumulated Depreciation ……………………………

14,800

ANSWERS TO COACHED PROBLEMS

CP9–1

Req. 1

Cost of each machine:

Machine

A

B

C

Total

Purchase price …………………………..

$7,600

$25,600

$9,300

$42,500

Installation costs ………………….……….

200

600

500

1,300

Renovation costs …………………………..

1,500

1,200

1,000

3,700

Total cost ………………………..…

$9,300

$27,400

$10,800

$47,500

Depreciation Expense ($1,740 + $4,620 + $3,600)

9,960

Accumulated Depreciation, Machine A

1,740

Accumulated Depreciation, Machine B

4,620

Accumulated Depreciation, Machine C

3,600

CP9–2

Req. 1

Machine A – Jan. 2:

Cash …………………………..…………………………………………….

20,000

Accumulated Depreciation–Equipment …………………………..

62,400

Gain on Disposal ………………………………………………..

6,200

Equipment ………………………………………………………..

76,200

Req. 2

Machine B – Jan. 2:

Accumulated Depreciation–Equipment ………………………….

13,500

Loss on Disposal ………………………………………………………

6,500

Equipment …………………………………………………………

20,000

CP9–3

Req. 1

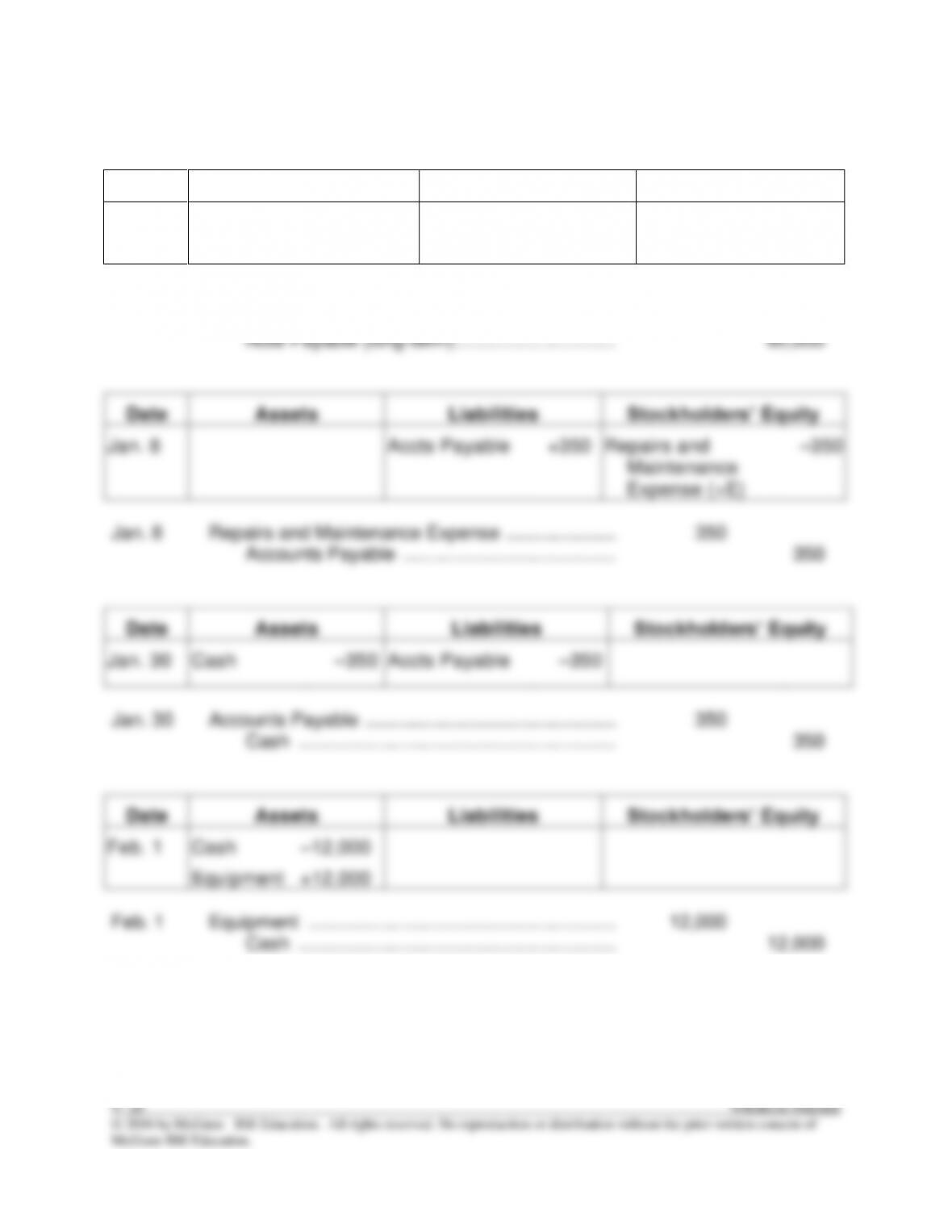

Date

Assets

Liabilities

Stockholders’ Equity

Jan. 2

Cash

Vehicle

–20,000

+80,000

Note Payable

(long–term)

+60,000

Jan. 2

Vehicle ………………………………………………………….

80,000

Cash …………………………………………………….

20,000

Note Payable (long-term) ………………………….

60,000

Date

Assets

Liabilities

Stockholders’ Equity

Jan. 8

Accts Payable

+350

Repairs and

Maintenance

Expense (+E)

–350

Jan. 8

Repairs and Maintenance Expense …………………

350

Accounts Payable …………………………..………

350

Date

Assets

Liabilities

Stockholders’ Equity

Jan. 30

Cash

–350

Accts Payable

–350

Jan. 30

Accounts Payable …………………………………………

350

Cash …………………………………………………….

350

Date

Assets

Liabilities

Stockholders’ Equity

Feb. 1

Cash

Equipment

–12,000

+12,000

Feb. 1

Equipment …………………………………………………..

12,000

Cash …………………………………………………….

12,000

CP9–3 (continued)

Req. 1 (continued)

Date

Assets

Liabilities

Stockholders’ Equity

Feb. 8

Cash

–250

R&M Expense (+E)

–250

Feb. 8

Repairs and Maintenance Expense …………………

250

Cash …………………………………………………….

250

Date

Assets

Liabilities

Stockholders’ Equity

Mar. 1

Cash

Land

Building

–20,000

+105,000

+105,000

Note Payable

(long–term)

+190,000

Mar. 1

Land ……………………………………………………………

105,000

Building ……………………………………………………….

105,000

Cash …………………………………………………….

20,000

Note Payable (long-term) …………………………

190,000

Date

Assets

Liabilities

Stockholders’ Equity

Mar. 31

Cash

Equipment

Goodwill

–90,000

+80,000

+10,000

Mar. 31

Equipment …………………………………………………..

80,000

Goodwill ………………………………………………………

10,000

Cash …………………………………………………….

90,000

CP9–3 (continued)

Req. 2

Vehicle (Straight-Line)

Annual

Partial Year

(Cost – Residual Value) x 1/Useful Life

($80,000 – $0) x 1/5

= $16,000

$16,000 x 3/12 = $4,000

Equipment (Straight-Line)

Annual

Partial Year

(Cost – Residual Value) x 1/Useful Life

($12,000 – $0) x 1/5

= $2,400

$2,400 x 2/12 = $ 400

Building (Double-Declining)

Annual

Partial Year

(Cost – Acc. Depn) x 2/Useful Life

($105,000 – $0) x 2/10

= $21,000

$21,000 x 1/12 = $1,750

Fundamentals of Financial Accounting, 5/e 9– 29

© 2016 by McGraw– Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO GROUP A PROBLEMS

PA9–1

Req. 1

Cost of each machine:

Machine

A

B

C

Total

Purchase price ……………..……………

$ 9,000

$38,200

$22,000

$69,200

Installation costs …………………………..

800

2,100

1,200

4,100

Renovation costs …………..………………

600

1,700

2,200

4,500

Total cost ………………….……….

$10,400

$42,000

$25,400

$77,800

Depreciation Expense ($2,350 + $10,000 + $5,080) …………

17,430

Accumulated Depreciation, Machine A ………………

2,350

Accumulated Depreciation, Machine B ………………

10,000

Accumulated Depreciation, Machine C ………………

5,080

PA9–2

Req. 1

Machine A – Jan. 1:

(a)

Depreciation expense in current year– none recorded because

disposal date was Jan. 1 (beginning of year).

(b)

To record disposal:

Cash ……………………………………………………………………..

9,000

Accumulated Depreciation–Equipment ………………………

21,600

Gain on Disposal ……………………………………………….

600

Equipment …………………………………………………………

30,000

Req. 2

Machine B – Jan. 1:

(a)

Depreciation expense in current year – none recorded because

disposal date was Jan. 1 (beginning of year).

(b)

To record disposal:

Accumulated Depreciation–Equipment ………………………

44,000

Loss on Disposal …………………………………………………….

15,200

Equipment ………………………………………………………..

59,200