Chapter 9

1. Long-lived assets are any assets that will not be used up within the next year, which

a business retains, not for sale, but for use in the course of normal operations.

Long-lived assets include the following:

(2) Intangible Assets:

2. The general rule for tangible assets, under the cost principle, is that all reasonable

3. The act of recording costs as assets rather than as expenses is what accountants

and analysts call capitalizing the costs. In the period a decision is made to

4. All reasonable and necessary costs to acquire and prepare an asset for use should

be capitalized. One could argue that to locate new landfill sites, Waste

5. Ordinary repairs and maintenance are expenditures for routine maintenance and

upkeep of long-lived assets. These expenditures are recurring in nature, involve

relatively small amounts at each occurrence, and do not directly lengthen the useful

6. In measuring and reporting long-lived assets, the expense recognition (“matching”)

principle is applied. As a long-lived asset is used, revenues are earned over a

7. Different depreciation methods are allowed because companies own different

tangible assets and use them in different ways.

8. To compute depreciation, the three values that must be known or estimated are:

(1) Asset cost – This includes all the costs capitalized for the asset, such as

purchase price, sales tax, legal fees, and other related costs.

(2) Residual value – This is an estimate of the amount that the company will get

9. a. The straight-line method of depreciation causes an equal amount of depreciation

expense to be apportioned to, or matched with, the revenues of each period. It is

especially appropriate for tangible long-lived assets that are used at an

approximately uniform level from period to period.

10. An increase in the estimated useful life would stretch depreciation over longer

11. Deferred income taxes represent the income taxes that companies have deferred

by taking tax deductions (for depreciation, for example) that exceed the expenses

12. An asset impairment occurs when events or changes in circumstances cause the

book value of long-lived assets to be higher than their related estimated future cash

13. The book (or carrying) value of a long–lived asset is its acquisition cost less the

accumulated depreciation from acquisition date to the balance sheet date. When

14. Depreciation is the allocation of costs of long-lived tangible assets over their useful

15. Goodwill represents an intangible asset that exists because of the good reputation,

customer appeal, and general acceptance of a business. Goodwill has value

because other parties often are willing to pay a substantial amount for it when they

16. IFRS requires the cost of long-lived assets to be separated into individual

components, if they have different useful lives. FedEx’s aircraft would likely to

17. The fixed asset turnover ratio =

Net sales revenue

Fundamentals of Financial Accounting, 5/e 9– 5

18. One complication is that, under IFRS, Bayer could revalue its long-lived assets at

fair value each year whereas, under GAAP, Johnson & Johnson must report its

assets based on historical costs. Another complication that could arise is that,

19. Depletion describes the process of allocating a natural resource’s cost over the

period of its extraction or harvesting. When a natural resource is depleted the

20. The cost of an addition to an existing long-lived asset should be depreciated over

the remaining life of the existing asset to which it relates. This rule is necessary

because an addition to an existing long-lived asset has no use after the useful life

of the existing asset has expired.

Authors’ Recommended Solution Time

(Time in minutes)

Mini-exercises

Exercises

Problems

Skills

Development

Cases*

Continuing

Case

No.

Time

No.

Time

No.

Time

No.

Time

No.

Time

1

5

1

10

CP9-1

25

1

25

1

25

2

3

2

10

CP9-2

20

2

25

2

20

3

3

3

15

CP9-3

18

3

30

4

4

4

15

PA9-1

25

4

60

5

4

5

15

PA9-2

20

5

30

6

5

6

20

PA9-3

18

6

30

7

5

7

6

PA9-4

25

7

25

8

5

8

15

PB9-1

25

9

5

9

20

PB9-2

20

10

5

10

8

PB9-3

18

11

6

11

15

PB9-4

25

12

5

12

15

C9-1

25

13

5

13

15

14

3

14

15

15

6

15

15

16

15

17

20

Fundamentals of Financial Accounting, 5/e 9– 7

© 2016 by McGraw– Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO MINI-EXERCISES

M9–1

Asset

Nature

Cost Allocation

1.

Property

L

NO

2.

Delivery vans

E

D

3.

Warehouse

B

D

4.

Trademark

I

NO

5.

New engine

E

D

6.

Franchise

I

A

7.

Software license

I

A

8.

Computers

E

D

9.

Production plant

B

D

M9–2

1. C

2. C

3. E

4. C

5. E

6. E

M9–3

Transactions

C

1.

Purchased a machine, $70,000; gave long-term note.

E

2.

Paid $600 for ordinary repairs.

C

3.

Purchased a patent, $45,300 cash.

C

4.

Paid cash, $200,000, for addition to old building.

E

5.

Paid $20,000 for monthly salaries.

E

6.

Paid $250 for routine maintenance.

C

7.

Paid $16,000 for extraordinary repairs.

M9–4

Machinery (original cost) $400,000

Accumulated Depreciation at end of year 3:

M9–5

Machinery (original cost) $400,000

Accumulated Depreciation at end of third year

Depreciation Expense per machine hour

M9–6

Machinery (original cost) $400,000

Accumulated Depreciation:

M9–7

(a) Annual straight-line depreciation = (Cost – Residual Value) x 1/Useful Life

= ($43,000 – $3,000) x 1/5 years

= $8,000 per year

M9–8

(a) The gain on sale that Liz Claiborne reported in 2011 when it disposed of its brand

names is equal to the total proceeds of $268 million (because the brand names had

a book value of zero). Gain = Proceeds – book value, so $268 = $268 – 0.

M9–9

(a) To record disposal of computers:

Accumulated Depreciation–Equipment ………………………..

4,800

Equipment ………………………………………………………..

4,800

(b) To record disposal of computers:

Accumulated Depreciation–Equipment ……………………….

3,600

Loss on Disposal ……………………………………………………..

1,200

Equipment ………………………………………………………..

4,800

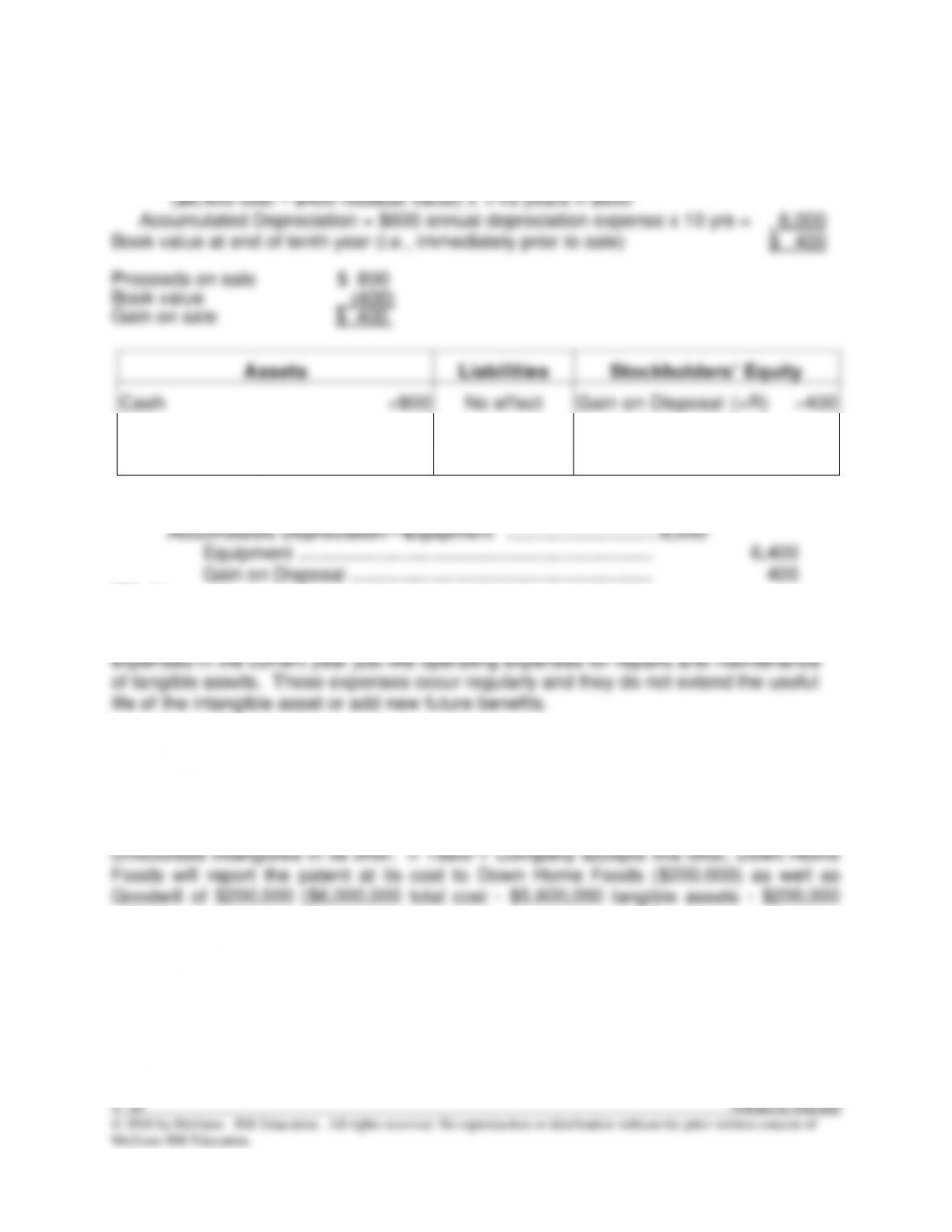

M9–10

Equipment (original cost) $6,400

Accumulated Depreciation at end of tenth year

Depreciation Expense =