Chapter Outline

Teaching Notes

7. Partial-Year Depreciation Calculations

a. Purchases of long-lived assets seldom occur on the

first or last day of the period; depreciation must

sometimes be calculated for periods shorter than a

year.

b. Under the straight-line and declining-balance methods,

the annual depreciation is multiplied by the fraction of

the year for which depreciation is being calculated.

c. These partial-year modifications are not required in

the units-of-production method.

8. Tax Depreciation

a. Most public companies use one method of

depreciation for reporting to stockholders and a

different method for determining income taxes.

i. The IRS allows companies to deduct larger

amounts of tax depreciation allowed by GAAP; the

deduction reduces the company’s income taxes

significantly in the years immediately following

the purchase of a long-lived asset.

ii. The IRS doesn’t allow a company to depreciate

more than an asset’s depreciable cost over its life;

so, the tax savings enjoyed in the early years of an

asset’s life will eventually be paid back in later

years of the asset’s life.

iii. The amount of tax put off (deferred) as a result of

taking large tax depreciation deductions is reported

as a long-term liability called Deferred Income

Tax.

b. Least and latest rule––All taxpayers want to pay the

least tax that is legally permitted and at the latest

possible date.

LO 9-4 Explain the effect of asset impairment on the financial statements.

C. Asset Impairment Losses––An asset’s book value could

exceed its current value

1. Impairment––Occurs when the cash to be generated by

an asset is estimated to be less than the carrying value of

that asset.

2. Events or changed circumstances can interfere with a

company’s ability to recover the value of an asset through

future operations.

3. If this occurs, the book value should be written down to

what the asset is worth (called fair value); the amount of

the write-down is reported as an impairment loss.

4. Impairment losses are classified as an operating expense

on the income statement and reported above the Income

from Operations subtotal.

Chapter Outline

Teaching Notes

LO 9-5 Analyze the disposal of long-lived tangible assets.

D. Disposal of Tangible Assets

1. In some cases, a business may voluntarily decide not to

hold a long-term asset for its entire life.

2. The disposal of a depreciable asset usually requires two

accounting adjustments:

a. Update the Depreciation Expense and Accumulated

Depreciation accounts; if asset is disposed of during

the year, must first record depreciation through the

date of disposal.

b. Record the disposal.

i. All disposals of long-lived assets require

accounting for (1) the book value of the items

given up, (2) the value of the items received, and

(3) any difference between the two amounts, which

reflects a gain or loss on the disposal.

ii. Any gain or loss on disposal is included on the

income statement when calculating Income from

Operations.

3. At the end of the year, the company sold equipment for

$50,000 cash. The original cost was $100,000 and the

related accumulated depreciation is $60,000.

a. Analyze (rounded to nearest thousand):

Assets = Liabilities + Stockholders’ Equity

Equipment (–A) –100; Accumulated Depreciation

(–xA) +60; Cash (A) +50; Gain on Disposal (+R) +10

b. Record:

Cash

50

Accumulated Depreciation

60

Equipment

100

Gain on Disposal

10

LO 9-6 Analyze the acquisition, use, and disposal of long-lived intangible assets.

E. Intangible Assets

1. Intangible assets––Long-lived assets that lack physical

substance. Examples:

a. Trademark––A special name, image, or slogan

identified with a product or company.

b. Copyright––A form of protection provided to the

original authors of literary, musical, artistic, dramatic,

and other works of authorship.

c. Patent––A right to exclude others from making,

using, selling, or importing an invention.

d. Technology assets––Acquired computer software and

development costs.

e. Licensing rights––The limited permissions to use

property according to specific terms and conditions set

out in a contract.

Chapter Outline

Teaching Notes

f. Franchise––A contractual right to sell certain

products or services, use certain trademarks, or

perform activities in a certain geographical region.

g. Goodwill––The premium a company pays to obtain

the favorable reputation associated with another

company.

2. Acquisition, Use, and Disposal

a. The costs of intangible assets are recorded as assets

only if they have been purchased.

i. Research and development––Expenditures that

may someday lead to patents, copyrights, or other

intangible assets; the uncertainty about their future

benefits requires they be expensed.

ii. The primary reason that the cost of self-developed

intangibles is reported as an expense rather than an

asset is that it’s easy for people to claim that

they’ve developed a valuable (but invisible)

intangible asset.

iii. Evidence of what it is actually worth only happens

when someone gives up their hard-earned cash to

buy it; at that time, the purchaser records the

intangible asset at its acquisition cost.

iv. This general rule applies to trademarks, copyrights,

patents, licensing rights, franchises, and goodwill.

v. Goodwill is the difference between the purchase

price of a company as a whole and the fair market

value of the net assets of the business.

The “Spotlight on Business

Decisions” feature addresses

valuing goodwill.

b. Use of intangible assets, after they have been

purchased––Rules depend on whether the intangible

asset has a limited or unlimited life.

i. Intangibles with limited useful lives––Cost is

spread on a straight-line basis over each period of

useful life.

▪ Amortization––Process of allocating the cost

of intangible assets over their limited useful

lives; similar to depreciation.

▪ Most companies do not estimate a residual

value because intangible assets usually have no

value at the end of their useful lives.

▪ Amortization is reported as an expense each

period on the income statement.

▪ Amortization is accumulated on the balance

sheet in the contra asset account, Accumulated

Amortization.

Chapter Outline

Teaching Notes

ii. Assume that amortization of $40,000 is recorded.

▪ Analyze (rounded to nearest thousand):

Assets = Liabilities + Stockholders’ Equity

Accumulated Amortization (xA) –40;

Amortization Expense (E) –40

▪ Record:

Amortization Expense

40

Accumulated Amortization

40

iii. Intangibles with unlimited or indefinite lives

(trademarks and most goodwill)––Cost is not

amortized.

The “Spotlight on the World”

feature addresses differences

between GAAP and IFRS.

c. Disposal of intangible assets––Results in gains (or

losses) if the amounts received on disposal are greater

than (less than) their book values.

III. Evaluate the Results

LO 9-7 Interpret the fixed asset turnover ratio.

A. Turnover Analysis

1. The fixed asset turnover ratio measures the sales dollars

generated by each dollar invested in (tangible) fixed

assets.

2. Fixed Asset Turnover Ratio = Net Sales Revenue ÷

Average Net Fixed Assets.

3. Average net fixed assets equals sum of beginning and

ending balances (net of accumulated depreciation)

divided by 2.

4. A higher fixed asset turnover ratio implies greater

efficiency.

LO 9–8 Describe factors to consider when comparing companies’ long-lived assets.

B. The Impact of Depreciation Differences

1. Depreciation can vary from one company to the next.

Illustrated in Exhibit 9.6

a. Even if the two companies are otherwise the same, the

reported net income will differ each year if the two

companies use different (but equally acceptable)

methods of depreciation.

i. These differences in depreciation affect more than

just depreciation expense; a different gain/loss on

disposal may also be reported on the income

statement.

Illustrated in Exhibit 9.7

ii. Any gain or loss on disposal that is reported on the

income statement tells you as much about the

method used to depreciate the asset as about

management’s apparent ability to successfully

negotiate the sale of long-lived assets.

Chapter Outline

Teaching Notes

b. The same effects can exist between two companies

that use the same depreciation methods but estimate

different useful lives or different residual values for

their long-lived assets. Useful lives can vary for

several reasons including differences in the:

i. Type of equipment each company used.

ii. Frequency of repairs and maintenance.

iii. Frequency and duration of use.

iv. Degree of conservatism in estimates.

2. Some analysts try to sidestep possible differences in

depreciation calculations by focusing on financial

measures that exclude the effects of depreciation.

a. EBITDA––An abbreviation for “earnings before

interest, taxes, depreciation, and amortization,” which

is a measure of operating performance that some

managers and analysts use in place of net income.

b. The idea is that this measure allows analysts to

conduct financial analyses without having to deal with

possible differences in depreciation and amortization.

IV. Natural Resources

LO 9-S1 Analyze and report depletion of natural resources.

A. Acquisition––When a company first acquires or develops a

natural resource, the cost of the natural resource is recorded

in conformity with the cost principle.

B. Use––As the natural resource is used up, its acquisition cost

must be split among the periods in which revenues are

earned in conformity with the expense recognition principle.

1. Depletion––Process of allocating a natural resource’s

cost over the period of its extraction or harvesting.

2. When a natural resource is depleted, the company obtains

inventory.

3. Because depletion is necessary to obtain the inventory,

the depletion computed during a period is added to the

cost of the inventory, not expensed in the period.

4. A timber tract costing $530,000 is depleted over its

estimated cutting period based on a “cutting” rate of

approximately 20 percent per year, it would be depleted

by $106,000 each year.

a. Analyze (rounded to nearest thousand):

Assets = Liabilities + Stockholders’ Equity

Accumulated Depletion (xA) –106; Depletion

Expense (E) –106.

b. Record:

Depletion Expense

106

Accumulated Depletion

106

Chapter Outline

Teaching Notes

V. Changes in Depreciation Estimates

LO 9–S2 Calculate changes in depreciation arising from changes in estimates or capitalized cost.

A. Depreciation is based on two estimates, useful life and

residual value.

1. One or both of these initial estimates may need to be

revised; in addition, extraordinary repairs and additions

may be added to the original acquisition cost at some time

during the asset’s use.

2. If either estimate is revised or if the asset’s cost has

changed, the undepreciated asset balance (less any

residual value estimated at that date) should be assigned

to each of the remaining years of estimated life using a

new amount of depreciation.

3. To compute the new depreciation expense due to the

changes described above, substitute the book value for the

original acquisition cost, the new residual value for the

original residual value, and the estimated remaining life

for the original useful life.

B. Companies may also change depreciation methods (for

example, from declining-balance to straight-line).

Covered more fully in

intermediate accounting

1. Change requires significantly more disclosure.

textbooks.

2. Under GAAP, changes in accounting estimates and

depreciation methods should be made only when a new

estimate or accounting method “better measures” the

periodic income of the business.

Supplemental Enrichment Activities

Note: These activities would be suitable for individual or group activities and class discussion.

1. Handout 9–1

Use Handout 9–1 for an in-class activity designed to review acquisition cost, depreciation

computations using all four methods, and the calculation of a gain/loss on sale. The solution follows

the handout master.

2. Handout 9–2

If you used Handout 9–1, use Handout 9–2 for an in-class discussion of the results of the calculations

performed in Handout 9–1.

HANDOUT 9–1

DEPRECIATION METHODS AND GAIN (LOSS) ON SALE

Joel Harvey Florists acquired a truck on January 1, 2016. The company paid $11,000 for the truck, $500

for destination charges, and $250 to paint the company name on the side of the truck. The company’s

accounting manager estimates the truck to have a five-year useful life and a residual value of $1,750. The

truck is expected to be driven 100,000 miles in five years. It is actually driven 15,000 miles in 2016,

25,000 miles in 2017, 30,000 miles in 2018, 25,000 miles in 2019, and 5,000 miles in 2020.

Part 1

On January 1, 2016, how much should Joel Harvey Florists capitalize for the cost of the truck?

Part 2

How much depreciation expenses would be recorded for the years 2016 through 2020 using each of the

following methods?

a. Straight-line

b. Unit-of-production

c. Declining-balance

Part 3

On December 31, 2020, at the end of its useful life, Joel Harvey sold the truck for $3,000 cash. Compute

the gain or loss on sale.

HANDOUT 9–1 SOLUTION

DEPRECIATION METHODS AND GAIN (LOSS) ON SALE

Joel Harvey Florists acquired a truck on January 1, 2016. The company paid $11,000 for the truck, $500

for destination charges, and $250 to paint the company name on the side of the truck. The company’s

accounting manager estimates the truck to have a five-year useful life and a residual value of $1,750. The

truck is expected to be driven 100,000 miles in five years. It is actually driven 15,000 miles in 2016,

25,000 miles in 2017, 30,000 miles in 2018, 25,000 miles in 2019, and 5,000 miles in 2020.

Part 1

On January 1, 2016, how much should Joel Harvey Florists capitalize for the cost of the truck?

11,000 + 500 + 250 = $11,750.

Part 2

How much depreciation expenses would be recorded for the years 2016 through 2020 using each of the

following methods?

a. Straight-line

(11,750 – 1,750) ÷ 5 = $2,000 per year

b. Unit-of-production

(11,750 – 1,750) ÷ 100,000 = 10 cents/mile

2016: 15,000 × 0.10 = $1,500;

2017: 25,000 × 0.10 = $2,500;

2018: 30,000 × 0.10 = $3,000;

2019: 25,000 × 0.10 = $2,500;

2020: 5,000 × 0.10 = $500.

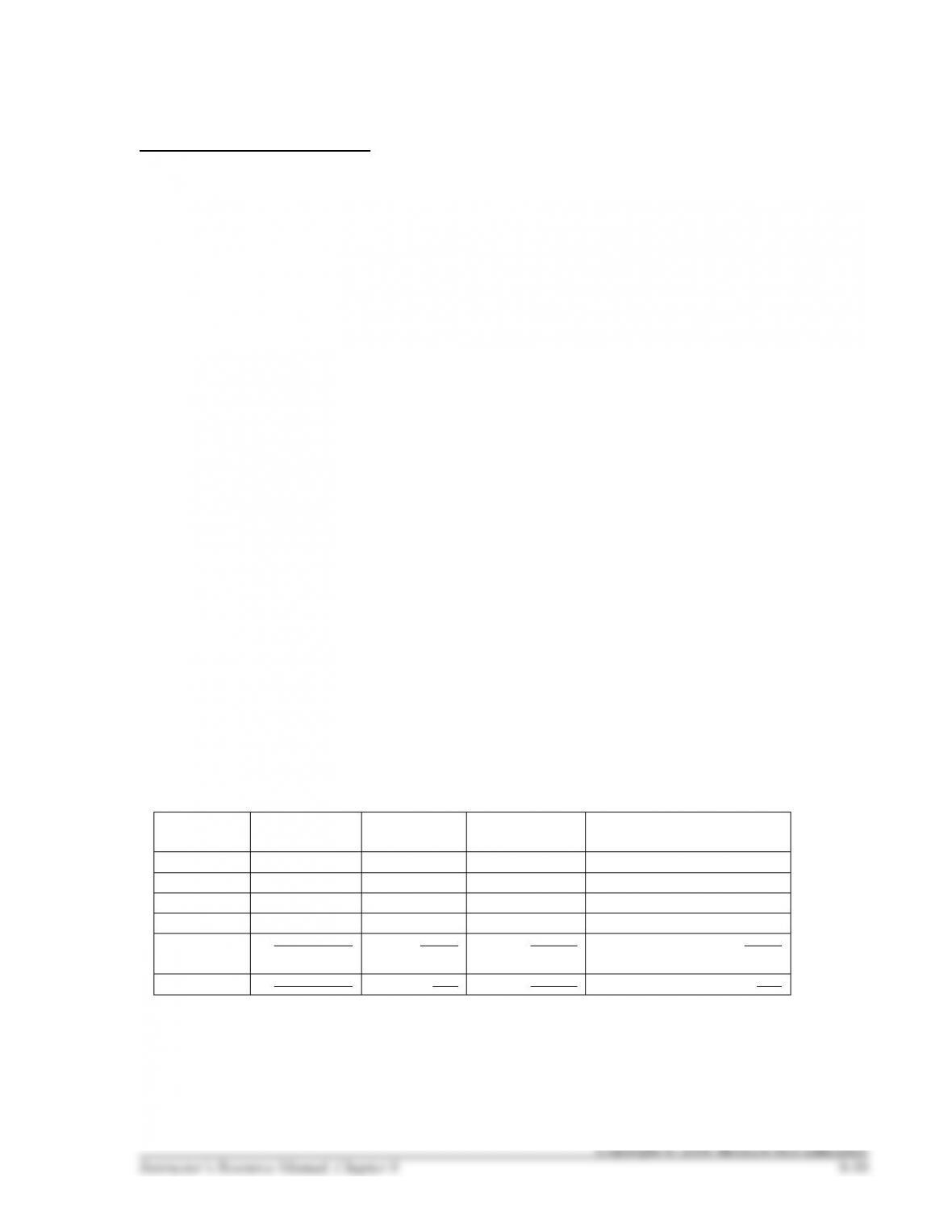

c. Declining-balance

Year

Computation

Depreciation

Expense

Accumulated

Depreciation

Net Book Value

Acquisition

11,750

2016

11,750 × 2/5

$4,700

$4,700

7,050

2017

7,050 × 2/5

2,820

7,520

4,230

2018

4,230 × 2/5

1,692

9,212

2,538

2019

2,538 × 2/5

2,538 – 1,750

788 1,015

10,000 10,227

1,750 1,448

2020

1,448 × 2/5

0 579

0 10,806

1,750 944

Part 3

On December 31, 2020, at the end of its useful life, Joel Harvey sold the truck for $3,000 cash. Compute

the gain or loss on sale.

Cost of $3,000 – Accumulated depreciation of $1,750 = Gain of $1,250

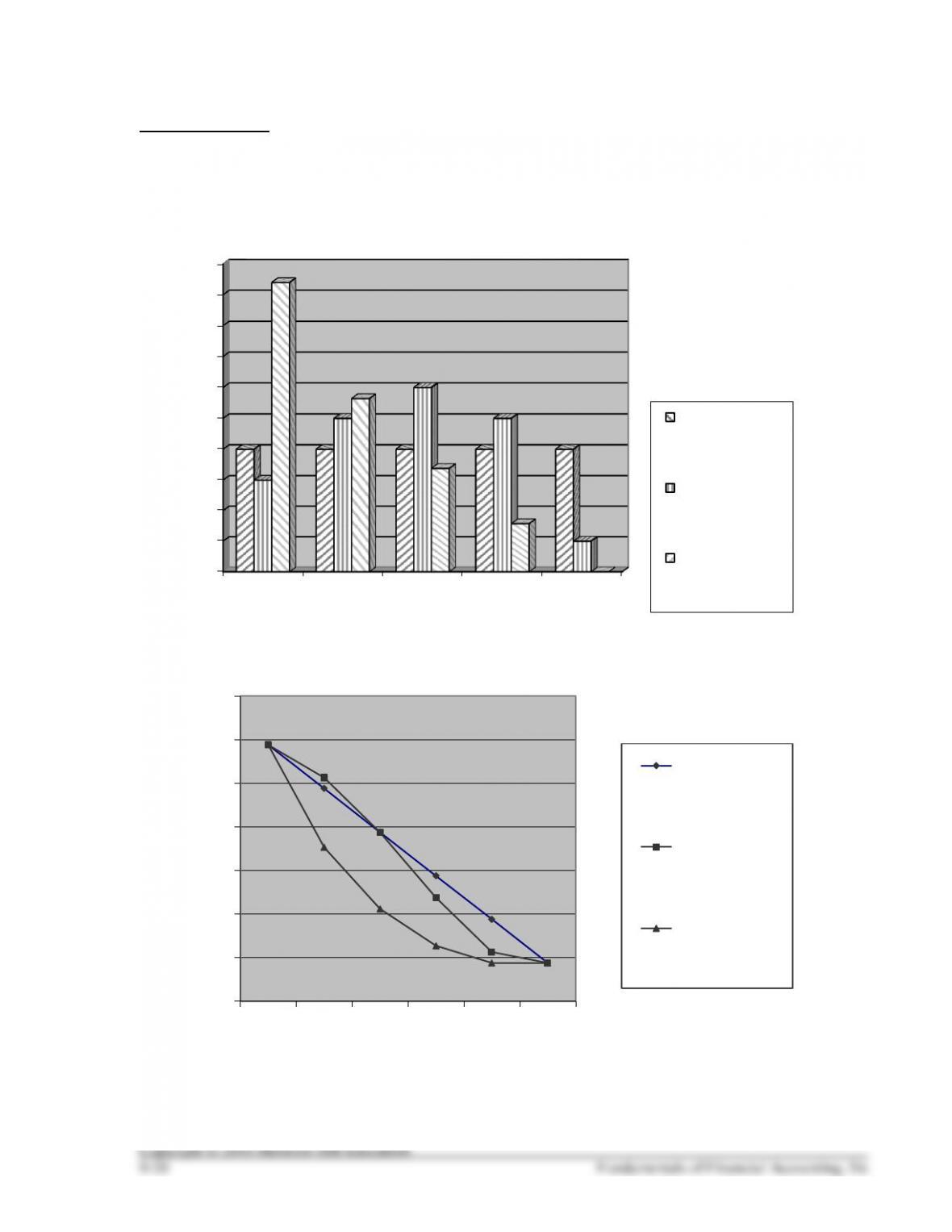

HANDOUT 9–2

COMPARISON OF DEPRECIATION EXPENSE AND NET BOOK VALUE

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

2016 2017 2018 2019 2020

$2,000 $2,000 $2,000 $2,000 $2,000

$1,500

$2,500

$3,000

$2,500

$500

$4,700

$2,820

$1,692

$788

$0

Depreciation Expense

Straight-line

Units–of-

production

Double-

declining

balance

$11,750

$9,750

$7,750

$5,750

$3,750

$1,750

$11,750

$10,250

$7,750

$4,750

$2,250 $1,750

$11,750

$7,050

$4,230

$2,538

$1,750 $1,750

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

Pre-

2016 2016 2017 2018 2019 2020

Net Book Value

Straight-line

Units–of–

production

Double-

declining

balance