C7–2 (continued)

COLLEGE COASTERS

Adjusted Trial Balance

At December 31

Account Titles

Debit

Credit

Cash

$ 8,905

Accounts Receivable

2,800

Inventory

275

Prepaid Rent

500

Equipment

810

Accumulated Depreciation–Equipment

$ 120

Accounts Payable

910

Income Tax Payable

789

Salaries and Wages Payable

100

Common Stock

6,500

Retained Earnings

3,030

Sales Revenue

17,785

Cost of Goods Sold

9,935

Office Expense

1,600

Salaries and Wages Expense

2,300

Rent Expense

1,200

Depreciation Expense

120

Income Tax Expense

789

Totals

$ 29,234

$ 29,234

Req. 4

COLLEGE COASTERS

Income Statement

For the Year Ended December 31

Sales Revenues

$ 17,785

Cost of Goods Sold

9,935

Gross Profit

7,850

Operating Expenses

Salaries and Wages Expense

2,300

Office Expenses

1,600

Rent Expense

1,200

Depreciation Expense

120

Total Operating Expenses

5,220

Income before Income Tax Expense

2,630

Income Tax Expense

789

Net Income

$ 1,841

C7–2 (continued)

Req. 4 (continued)

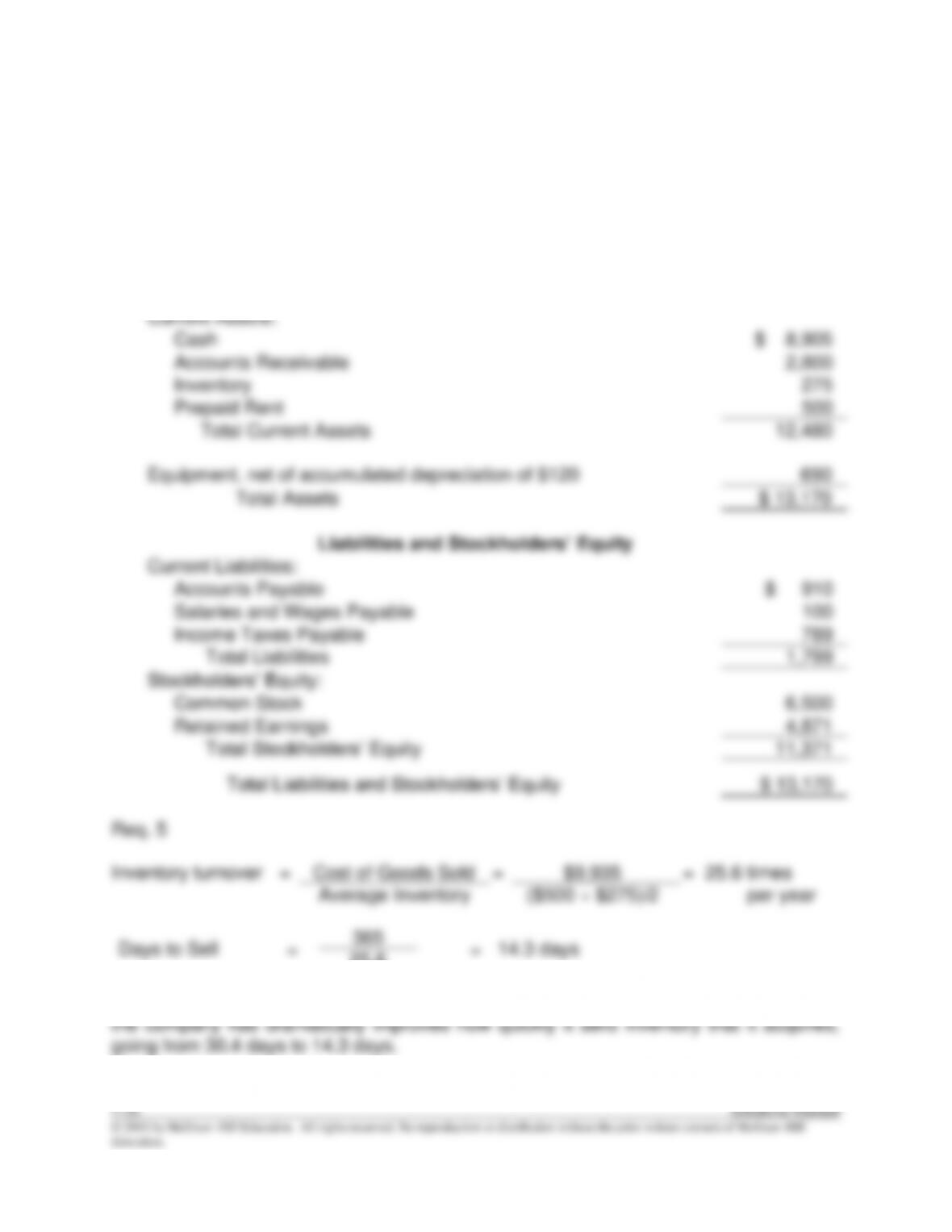

COLLEGE COASTERS

Balance Sheet

As of December 31

Assets

Current Assets:

Cash

$ 8,905

Accounts Receivable

2,800

Inventory

275

Prepaid Rent

500

Total Current Assets

12,480

Equipment, net of accumulated depreciation of $120

690

Total Assets

$ 13,170

Liabilities and Stockholders’ Equity

Current Liabilities:

Accounts Payable

$ 910

Salaries and Wages Payable

100

Income Taxes Payable

789

Total Liabilities

1,799

Stockholders’ Equity:

Common Stock

6,500

Retained Earnings

4,871

Total Stockholders’ Equity

11,371

Total Liabilities and Stockholders’ Equity

$ 13,170

C7–3

1) The gross profit percentage of Merchandise Mavens Corporation (MMC) has

declined from 15.9% to 10.0% to 3.8% over the last three years (see calculations

below). The 3.8% gross profit percentage in the most recent year indicates MMC’s

selling price barely exceeds its cost to acquire the goods. If the gross profit

Gross Profit

$ 15,000 /$ 390,000

$ 40,000/ $ 398,000

$ 63,000/$ 397,000

Percentage

= 3.8%

= 10.0%

= 15.9%

2) Sales returns and allowances have grown dramatically in the most recent year,

3)

2015

2014

Inventory Turnover

Ratio

=

Cost of Goods Sold

=

8.3*

11.3**

Average Inventory

Days to Sell

=

365 Days

=

44.0

32.3

Inventory Turnover

Ratio

* 8.3 =

$375,000

** 11.3 =

$358,000

($34,000 + $56,410) ÷ 2

($29,425 + $34,000) ÷ 2

The previous calculations demonstrate that Merchandise Mavens Corporation’s

inventory turnover ratio is drastically decreasing from 11.3 times in 2014 to 8.3 times in

2014. Consequently, the days to sell ratio has increased suggesting that the inventory

is not selling as quickly, possibly due to a decreased demand for the product.

times per year

days

S7–1

1. D

2. B

3. A

4. B

Calculations:

Req. 3

Inventory

Turnover

Ratio

=

Cost of Goods Sold

=

$51,422

Average Inventory

($11,057 + $10,710) ÷ 2

=

4.7 times per year

Days to Sell

=

365 Days

=

(365 ÷ 4.7) = 77.7 days

Inventory Turnover

Ratio

S7–2

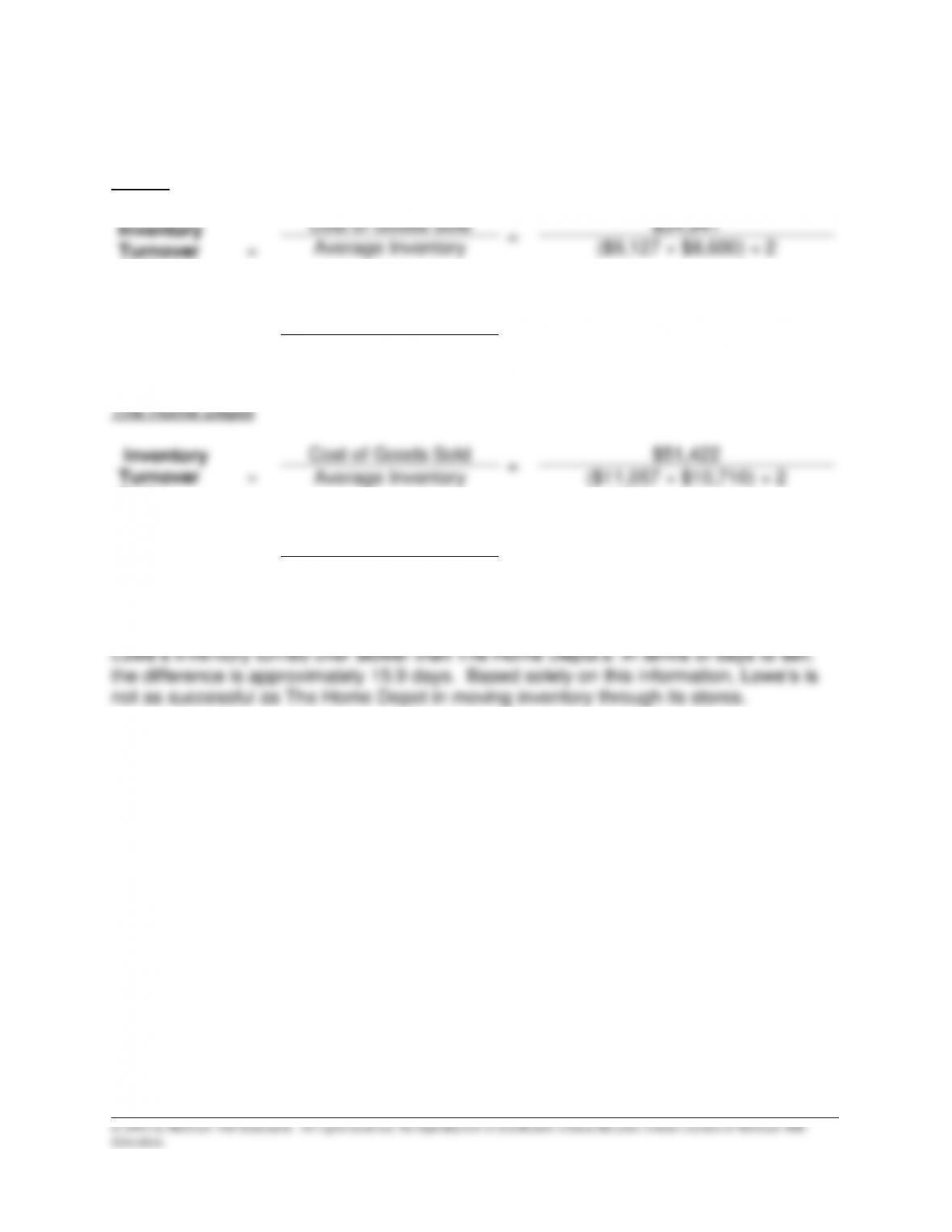

Req. 1

Lowe’s inventories of $9,127 (million) are less than The Home Depot’s inventories of

$11,057 (million).

Req. 2

S7–2 (continued)

Req. 3

Lowe’s

Inventory

Turnover

Ratio

=

Cost of Goods Sold

=

$34,941

Average Inventory

($9,127 + $8,600) ÷ 2

=

3.9 times per year

Days to Sell

=

365 Days

=

(365 ÷ 3.9) = 93.6 days

Inventory Turnover

Ratio

Cost of Goods Sold

=

$51,422

Average Inventory

S7–4

Evidence

Suspicion

– inventory tripled and then quadrupled in

the last three years

– is it possible that this much inventory

exists?

– perhaps its market value is less than cost

– top management wanted to know in

advance which stores auditors would

attend

– top management reduced inventory levels

at audited stores

– perhaps the company is removing

inventory that can’t be sold above its cost,

and is moving it to other company stores so

the auditors don’t detect the old inventory

– unusual account name (“cookies”) used

for the debit

– perhaps the write–down will not be properly

classified as an expense

– “cookies” account was allocated back to

the stores

– are the allocations back to the stores simply

putting the write–downs back in inventory?

– amount of journal entries are for peculiar

amounts (e.g., $9,999,999.99)

– do these odd amounts represent actual

inventory costs or are they made up?

– one store recorded the allocated “cookie”

as “accrued inventory”

– this fake–sounding account name seems

more like an asset than an expense.

S7–5

Req. 1

The cost of goods sold using LIFO is (2,500 units @ $50) + (500 units @ $45) which

totals $147,500. This is the exact figure used in calculating the reported gross profit of

$17,500.

Req. 2

Yes it is likely that both FIFO and the weighted average cost method would produce

S7–5 (continued)

Req. 4

Yes, it is acceptable within GAAP for companies to use different inventory methods for

different product lines included in inventory as long as the methods are used

consistently over time.

Req. 5

Although generally accepted accounting principles do allow different inventory costing

S7–6

Req.1

Sales Revenue (45 @ $25,000) $1,125,000

Cost of Goods Sold (40 @ $10,000) + (5 @ $12,000) 460,000

Gross Profit 665,000

Operating Expenses 300,000

Income from Operations $ 365,000

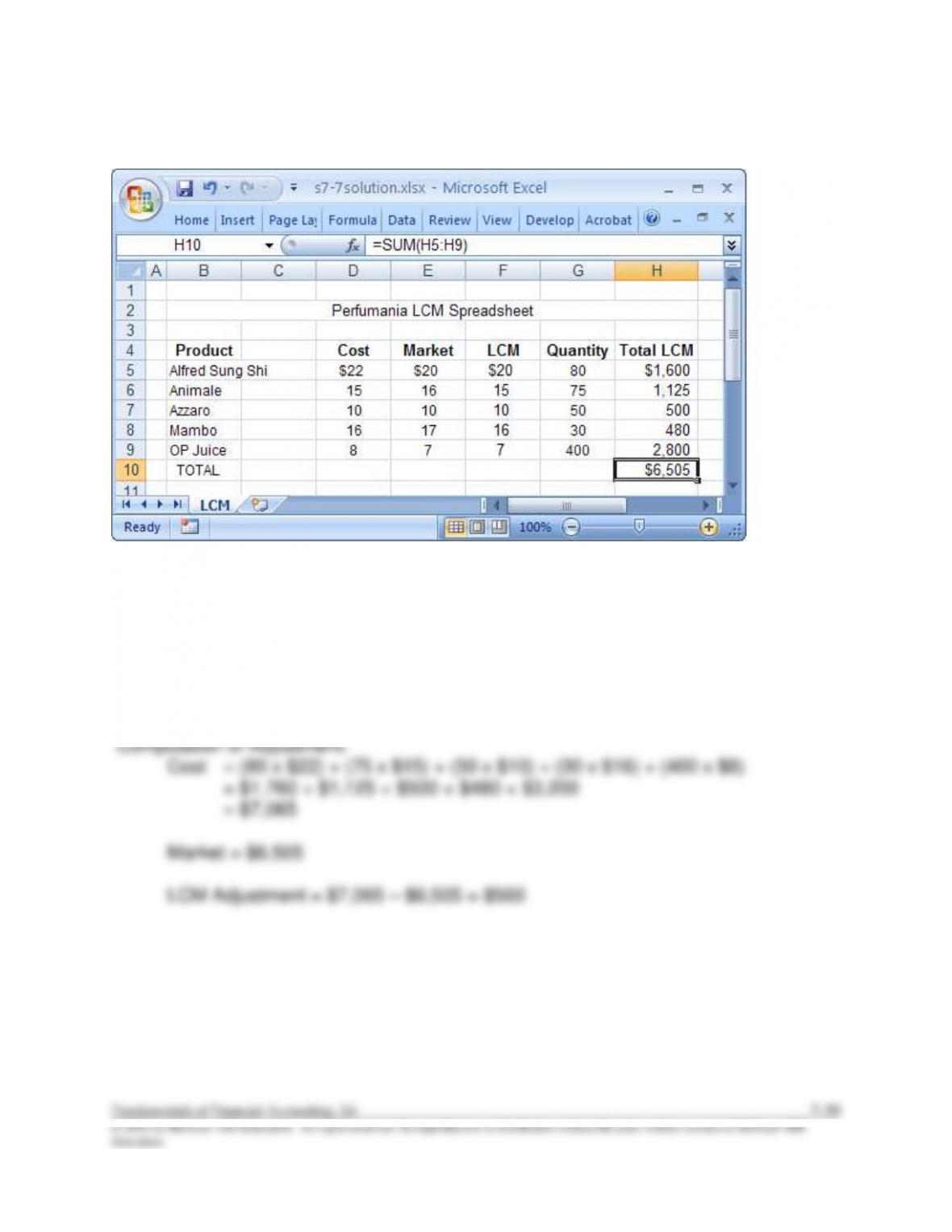

S7–7

Req. 1

Req. 2

Cost of Goods Sold …………………………………..

$560

Inventory …………………………………………

$560

To record reduction in market value of inventory.

ANSWERS TO CONTINUING CASES

CC7–1

Req. 1

According to the cost principle, inventory is recorded initially at the cost to acquire it in a

condition and location ready for sale. Transportation is a necessary cost of acquiring

inventory in location, so the costs of transportation should be recorded as part of the