PA7–5

Req. 1

Sherwood Company

Income Statements (Corrected)

2012 2013 2014 2015

Net Sales $2,000,000 $2,400,000 $2,500,000 $3,000,000

Cost of goods sold 1,400,000 1,680,000* 1,750,000* 2,100,000

7–42 Solutions Manual

© 2016 by McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO GROUP B PROBLEMS

PB7–1

Req. 1 Unit Total

Goods available for sale for all methods: Units Cost Cost

Beginning inventory, January 1 250 $2.50 $625

Purchase, January 12 300 3.00 900

Purchase, January 26 80 4.00 320

Ending inventory (80 units x $4.00)

(200 units x $3.00) $920

Cost of goods sold (250 units x $2.50)

(100 units x $3.00) $925

c. Last–in, first–out:

PB7–1 (continued)

Req. 2

PB7–2

Req. 1

MONDETTA CLOTHING

Income Statement (LCM basis)

For the Year Ended December 31

Net Sales $420,000

Original

Replacement

LCM

Item

Unit Cost

Cost (Market)

per Unit

Quantity

LCM Valuation

A

$4.50

$6.00

$4.50

x

3,000

$13,500

B

6.00

3.00

3.00

x

1,500

4,500

C

3.00

6.00

3.00

x

7,000

21,000

D

7.50

4.50

4.50

x

3,000

13,500

LCM Inventory Valuation

$52,500

PB7–2 (continued)

Req. 2 Amount of

FIFO LCM Increase

Item Changed Cost Basis Basis (Decrease)

PB7–3

Req. 1

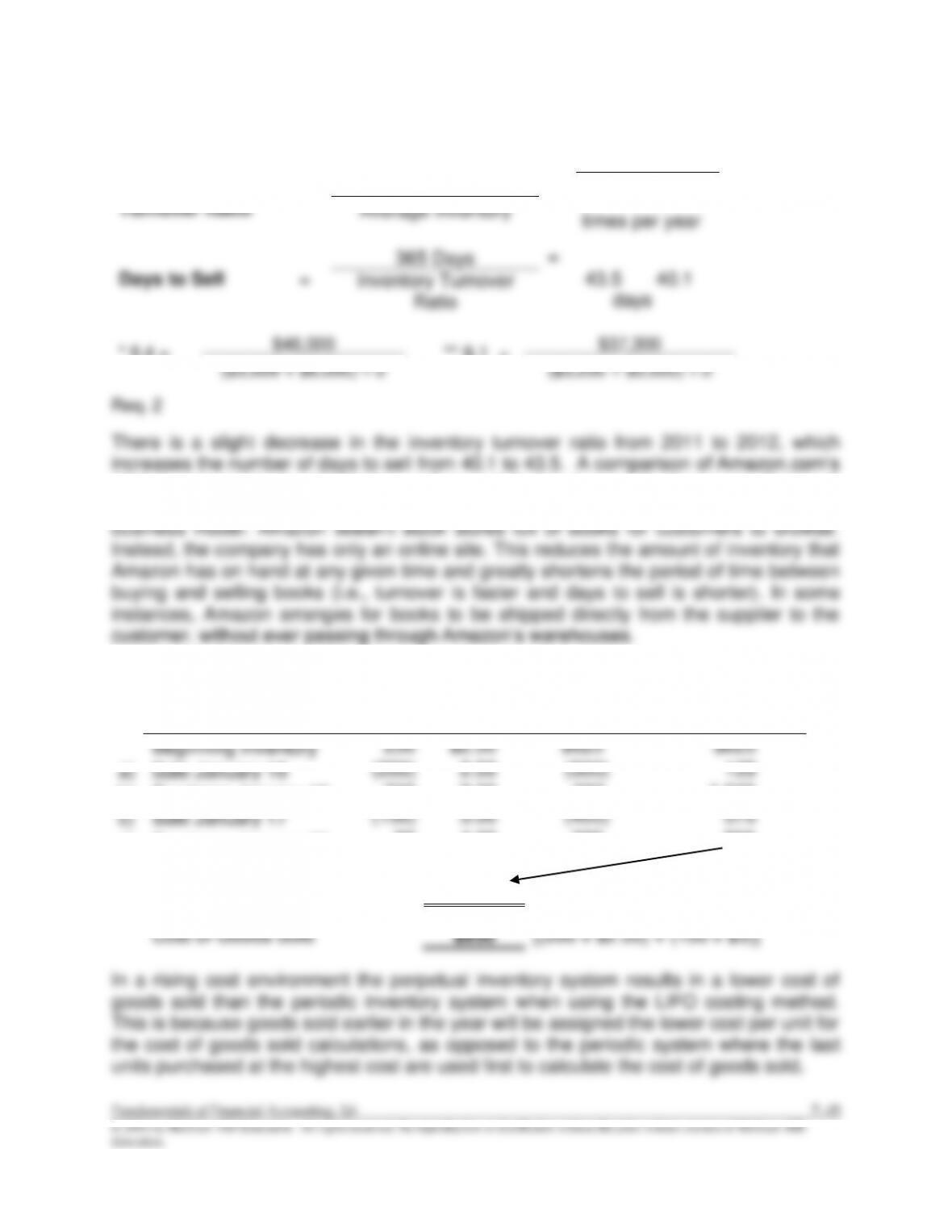

2012

2011

Inventory

Turnover Ratio

=

Cost of Goods Sold

=

8.4*

9.1**

Average Inventory

Days to Sell

=

365 Days

=

43.5

40.1

Inventory Turnover

Ratio

* 8.4 =

$46,000

** 9.1 =

$37,300

($5,000 + $6,000) ÷ 2

($3,200 + $5,000) ÷ 2

Req. 2

There is a slight decrease in the inventory turnover ratio from 2011 to 2012, which

increases the number of days to sell from 40.1 to 43.5. A comparison of Amazon.com’s

43.5 days to sell to the 104.3 days at Barnes & Noble, Inc., really does make Barnes &

Noble seem like a library. This dramatic difference is caused by Amazon.com’s

PB7–4

Remaining

Perpetual LIFO

Units

Unit Cost

Total Cost

Inventory Value

Beginning Inventory

250

$2.50

$625

$625

a)

Sale January 10

(200)

2.50

(500)

125

b)

Purchase January 12

300

3.00

900

1,025

c)

Sale January 17

(150)

3.00

(450)

575

d)

Purchase January 26

80

4.00

320

895

Ending Inventory

$895

[(50 x $2.50) + (150 x $3) + (80 x $4)]

Cost of Goods Sold

$950

[(200 x $2.50) + (150 x $3)]

In a rising cost environment the perpetual inventory system results in a lower cost of

goods sold than the periodic inventory system when using the LIFO costing method.

This is because goods sold earlier in the year will be assigned the lower cost per unit for

the cost of goods sold calculations, as opposed to the periodic system where the last

units purchased at the highest cost are used first to calculate the cost of goods sold.

times per year

days

PB7–5

Req. 1 Spears & Cantrell Company

Income Statements (Corrected)

Q1 Q2 Q3

PB7–5 (continued)

Req. 2

Q1 Q2 Q3

Gross profit percentage [(Gross profit ÷ Sales revenue) x 100]:

a) Before correction:

ANSWER TO COMPREHENSIVE PROBLEMS

C7–1

Req. 1

When using FIFO, ending inventory cost is computed using the cost of last–in goods, so

(a) = 4 units x $16 each = $64.

(b) = $10 + $64 + $107 = $181

(c) = (b) = $181

(d) = (c) – $36 – $44 = $181 – $36 – $44 = $101

Req. 2

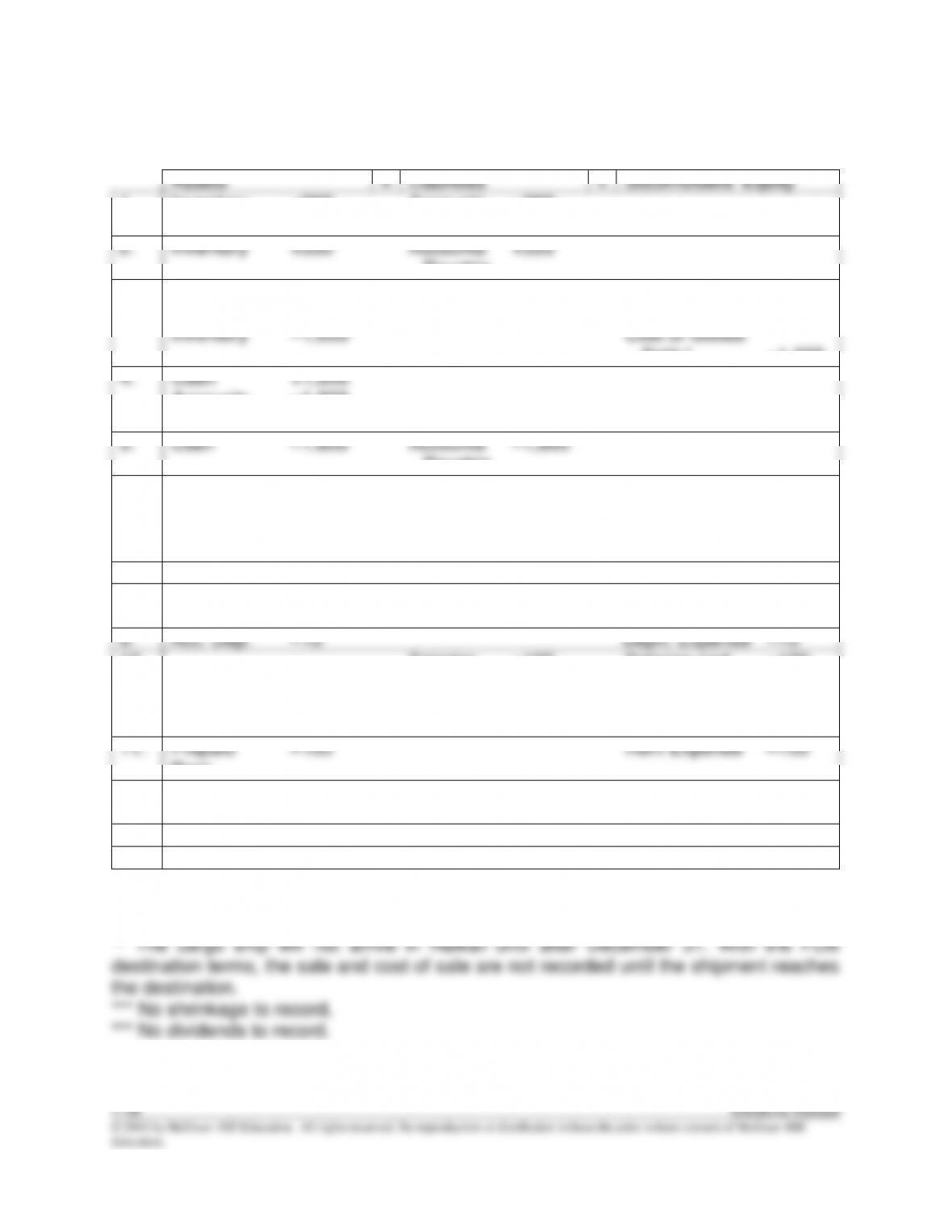

C7–2

Req. 1

Assets

=

Liabilities

+

Stockholders’ Equity

1.

Inventory

+260

Accounts

Payable

+260

2.

Inventory

+550

Accounts

Payable

+550

3.

Accounts

Receivable

Inventory

+1,800

–1,035*

Sales

Revenue

Cost of Goods

Sold *

+1,800

–1,035

4.

Cash

Accounts

Receivable

+1,000

–1,000

5.

Cash

–1,600

Accounts

Payable

–1,600

6.

Cash

–500

Salaries

and

Wages

Payable

–300

Salaries and

Wages

Expense

–200

7.

NE**

NE

NE

8.

Accounts

Payable

+200

Office

Expenses

–200

9.

Acc. Dep.

–10

Depn. Expense

–10

10.

Salaries

and

Wages

Payable

+100

Salaries and

Wages

Expense

–100

11.

Prepaid

Rent

–100

Rent Expense

–100

12.

Inc. Tax

Payable

+789

Income Tax

Expense

–789

13.

NE***

NE

NE

14.

NE****

NE

NE

* Cost of goods sold = (1,000 units x $0.50) + (500 units x $0.52) + (500 units x $0.55)

= $1,035

Fundamentals of Financial Accounting, 5/e 7–49

© 2016 by McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

C7–2 (continued)

Req. 2

1.

Inventory ……………………………………………………..

260

Accounts Payable …………………………………..

260

2.

Inventory ……………………………………………………..

550

Accounts Payable …………………………………..

550

3.

Accounts Receivable …………………………………….

1,800

Sales Revenue ………………………………………

1,800

Cost of Goods Sold* ……………………………………..

1,035

Inventory ……………………………………………….

1,035

4.

Cash …………………………………………………………..

1,000

Accounts Receivable ………………………………

1,000

5.

Accounts Payable …………………………………………

1,600

Cash …………………………………………………….

1,600

6.

Salaries and Wages Expense …………………………

200

Salaries and Wages Payable ………………………….

300

Cash …………………………………………………….

500

7.

No journal entry because the goods did not arrive at the destination.*

8.

Office Expenses ……………………………………………

200

Accounts Payable …………………………………..

200

9.

Depreciation Expense …………………………..……….

10

Accumulated Depreciation–Equipment ……….

10

10.

Salaries and Wages Expense …………………………

100

Salaries and Wages Payable ……………………

100

11.

Rent Expense ………………………………………………

100

Prepaid Rent …………………………………………

100

12.

Income Tax Expense …………………………………….

789

Income Taxes Payable …………………………...

789

C7–2 (continued)

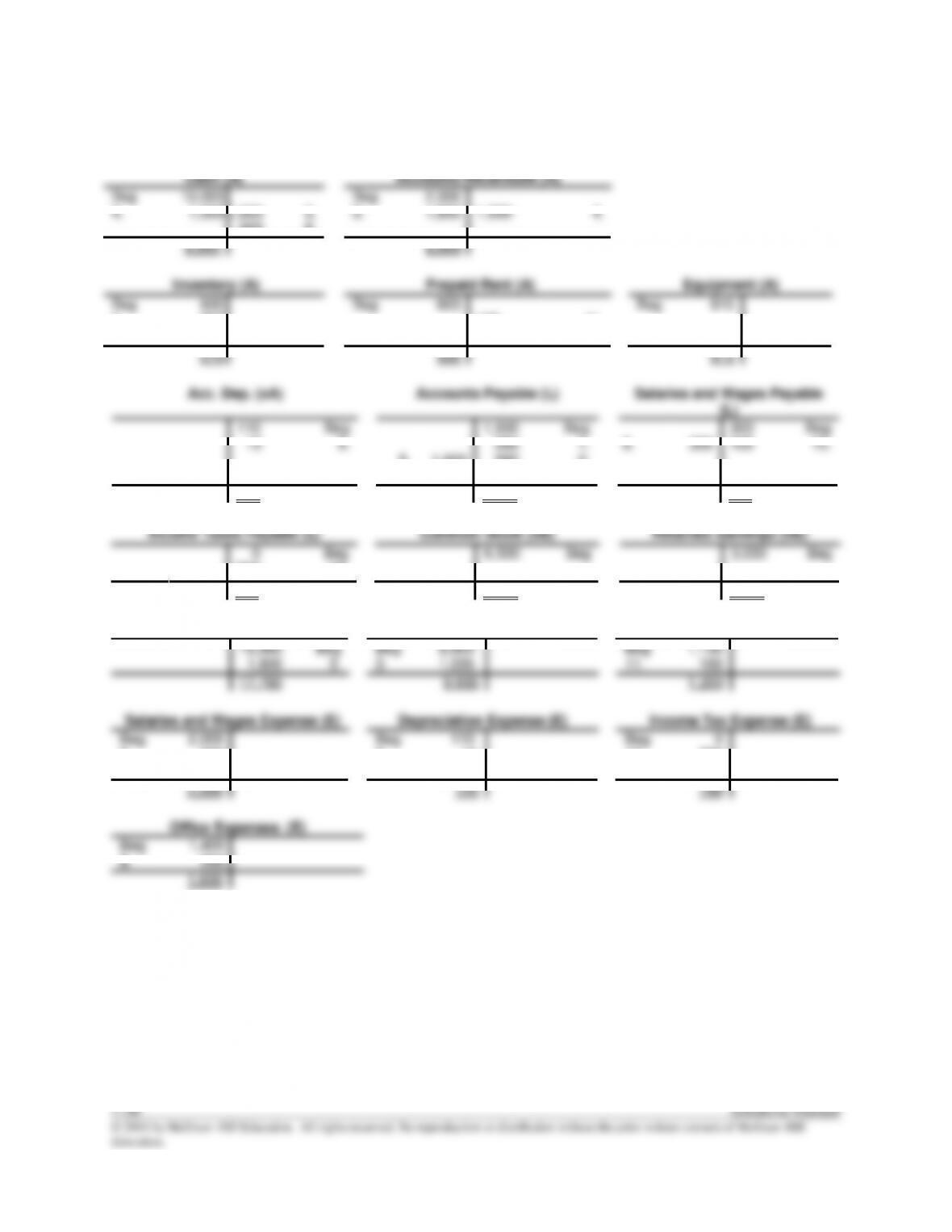

Req. 3

Cash (A)

Accounts Receivable (A)

Beg

4.

10,005

1,000

1,600

500

5.

6.

Beg

3.

2,000

1,800

1,000

4.

8,905

2,800

Inventory (A)

Prepaid Rent (A)

Equipment (A)

Beg

1.

2.

500

260

550

1,035

3.

Beg

600

100

11.

Beg

810

275

500

810

Acc. Dep. (xA)

Accounts Payable (L)

Salaries and Wages Payable

(L)

110

10

Beg

9.

5.

1,600

1,500

260

550

200

Beg

1.

2.

8.

6.

300

300

100

Beg

10.

120

910

100

Income Taxes Payable (L)

Common Stock (SE)

Retained Earnings (SE)

0

789

Beg

12.

6,500

Beg

3,030

Beg

789

6,500

3,030

Sales Revenue (R)

Cost of Goods Sold (E)

Rent Expense (E)–

15,985

1,800

Beg

3.

Beg

3.

8,900

1,035

Beg

11.

1,100

100

17,785

9,935

1,200

Salaries and Wages Expense (E)

Depreciation Expense (E)

Income Tax Expense (E)

Beg

6.

10,

2,000

200

100

Beg

9.

110

10

Beg

12.

0

789

2,300

120

789

Beg

1,600