ANSWERS TO COACHED PROBLEMS

CP7–1

Req. 1 Unit Total

Goods available for sale for all methods: Units Cost Cost

Beginning inventory, January 1 200 $30 $6,000

Purchase, March 2 300 32 9,600

Purchase, June 30 250 36 9,000

Average unit cost $24,600 ÷ 750 = $32.80

Ending inventory (350 units x $32.80) $11,480

Cost of goods sold (400 units x $32.80) $13,120

c. First–in, first–out:

Ending inventory (250 units x $36)

CP7–2

Req. 1

SMART COMPANY

Income Statement (LCM basis)

For the Year Ended December 31

Sales Revenue $280,000

Cost of Goods Sold:

*Computation of ending inventory on LCM basis:

Original

Replacement

Item

Unit Cost

Cost (Market)

LCM per Unit

Quantity

LCM Valuation

A

$3

$4

$3

x

3,000

$ 9,000

B

4

2

2

x

1,500

3,000

C

2

4

2

x

7,000

14,000

D

5

2

2

x

3,000

6,000

LCM Inventory Valuation

$32,000

Req. 2

Amount of

FIFO LCM Increase

Item Changed Cost Basis Basis (Decrease)

Ending Inventory $ 44,000 $ 32,000 $(12,000)

Cost of Goods Sold 168,000 180,000 12,000

Gross Profit 112,000 100,000 ( 12,000)

Income from Operations 51,000 39,000 ( 12,000)

Income Tax Expense 15,300 11,700 ( 3,600)

Net Income 35,700 27,300 ( 8,400)

CP7–2 (continued)

Analysis

Ending inventory, cost of goods sold, gross profit, and operating income each

CP7–3

Req. 1

2013

2012

Inventory

Turnover Ratio

=

Cost of Goods Sold

=

5.4*

5.8**

Average Inventory

Days to Sell

=

365 Days

=

67.6

62.9

Inventory Turnover

Ratio

*5.4 =

$6,240

** 5.8 =

$6,870

($1,200+ $1,100) ÷ 2

($1,100+ $1,250) ÷ 2

Req. 2

The inventory turnover ratio reflects how many times average inventory was bought and

times per year

days

CP7–4

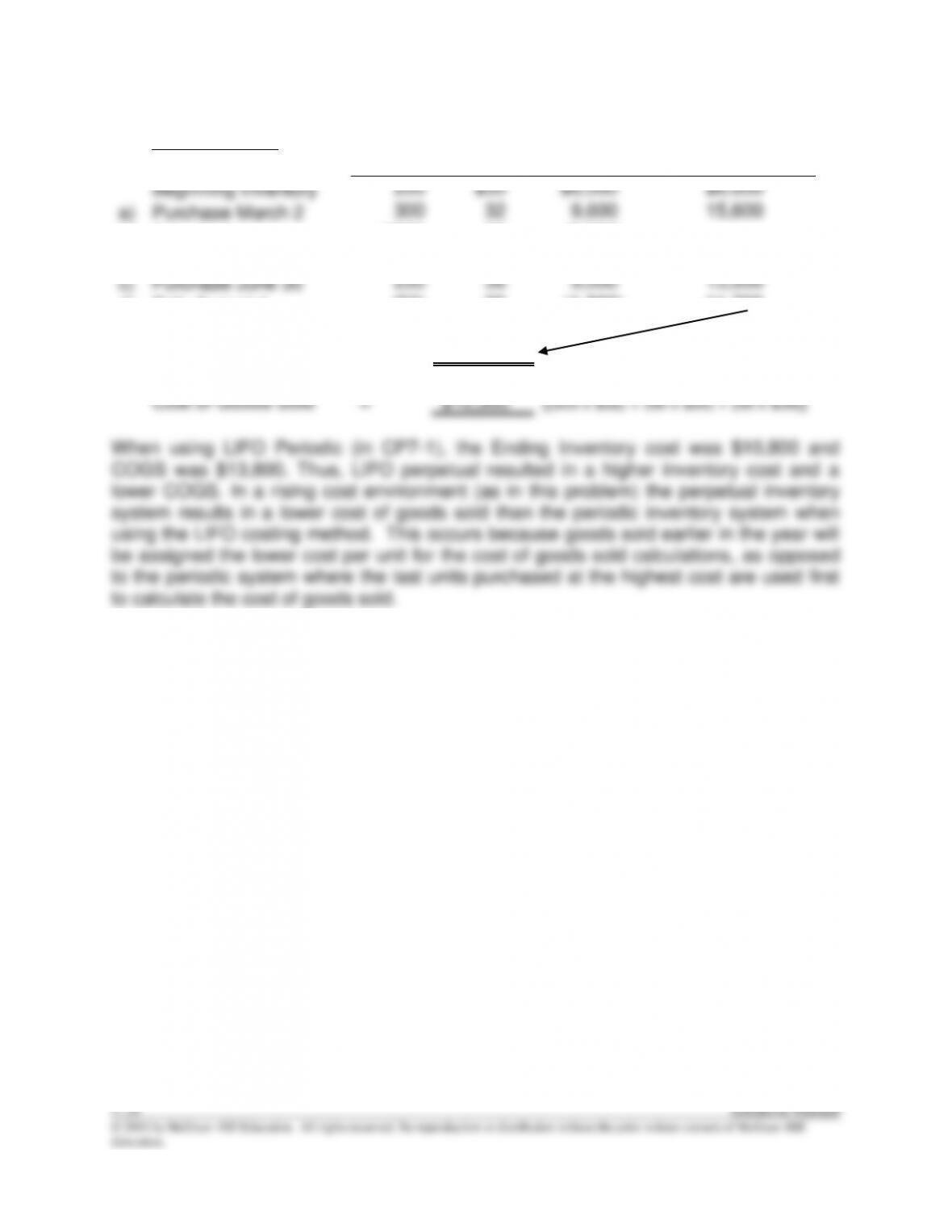

LIFO Perpetual

Remaining

Units

Unit Cost

Total Cost

Inventory Value

Beginning Inventory

200

$30

$6,000

$6,000

a)

Purchase March 2

300

32

9,600

15,600

b)

Sale April 1

(300)

32

(9,600)

(50)

30

(1,500)

4,500

c)

Purchase June 30

250

36

9,000

13,500

d)

Sale August 1

(50)

36

(1,800)

11,700

Ending Inventory

=

$11,700

[(150 x $30) + (200 x $36)]

Cost of Goods Sold

=

$12,900

[(300 x $32) + (50 x $30) + (50 x $36)]

CP7–5

Req. 1

Murphy & Murphy Company

Income Statements (Corrected)

Quarter 1 Quarter 2 Quarter 3 Quarter 4

Net Sales $50,000 $49,000 $71,000 $58,000

Cost of Goods Sold 32,500 32,000* 46,000* 37,000

7–36 Solutions Manual

© 2016 by McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO GROUP A PROBLEMS

PA7–1

Req. 1

Unit Total

Goods available for sale for all methods: Units Cost Cost

Beginning inventory, January 1 1,800 $50 $ 90,000

Purchase, January 30 2,500 62 155,000

Purchase, May 1 1,200 80 96,000

PA7–1 (continued)

Req. 1 (continued)

d. Specific identification:

Ending inventory ( 520 units x $80)***

(1,630 units x $62)**** $142,660

PA7–2

Req. 1

SPRINGER ANDERSON GYMNASTICS

Income Statement (LCM basis)

For the Year Ended December 31

Sales Revenue $140,000

Cost of Goods Sold:

*Computation of ending inventory on LCM basis:

Original

Replacement

LCM

Item

Unit Cost

Cost (Market)

per Unit

Quantity

LCM Valuation

A

$3

$4

$3

x

1,500

$4,500

B

4

2

2

x

750

1,500

C

2

1

1

x

3,500

3,500

D

5

3

3

x

1,500

4,500

LCM Inventory Valuation

$14,000

Req. 2 Amount of

FIFO LCM Increase

Item Changed Cost Basis Basis (Decrease)

Ending Inventory $ 22,000 $ 14,000 $ (8,000)

Cost of Goods Sold 84,000 92,000 8,000

Gross Profit 56,000 48,000 ( 8,000)

Income from Operations 25,000 17,000 ( 8,000)

Income Tax Expense 7,500 5,100 ( 2,400)

Net Income 17,500 11,900 ( 5,600)

PA7–2 (continued)

Analysis

Ending inventory, cost of goods sold, gross profit, and operating income each

PA7–3

Req. 1

2013

2012

Inventory

Turnover Ratio

=

Cost of Goods Sold

=

6.5*

7.5**

Average Inventory

Days to Sell

=

365 Days

=

56.2

48.7

Inventory Turnover

Ratio

* 6.5 =

$3,200

** 7.5 =

$3,180

($430 + $550) ÷ 2

($420 + $430) ÷ 2

Req. 2

The inventory turnover ratio reflects how many times average inventory was acquired

times per year

days

PA7–4

Remaining

Perpetual LIFO

Units

Unit Cost

Total Cost

Inventory Value

Beginning Inventory

1,800

$50

$ 90,000

$ 90,000

a)

Purchase January 30

2,500

62

155,000

245,000

b)

Sale March 14

(1,450)

62

(89,900)

155,100

c)

Purchase May 1

1,200

80

96,000

251,100

d)

Sale August 31

(1,200)

80

(96,000)

155,100

(700)

62

(43,400)

111,700

Ending Inventory

$111,700

[(1,800 x $50) + (350 x $62)]

Cost of Goods Sold

$229,300

[(1,450 x $62) + (1,200 x $80) + (700 x $62)]

In a rising cost environment the perpetual inventory system generally results in a lower

cost of goods sold than the periodic inventory system when using the LIFO costing

method. This is because goods sold earlier in the year will be assigned the lower cost

per unit for the cost of goods sold calculations, as opposed to the periodic system

where the last units purchased at the highest cost are used first to calculate the cost of

goods sold. However in this instance the timing of the purchases and sales are

organized in a manner that both the periodic and the perpetual systems arrive at the

same cost of goods sold value.