E7–8

Req. 1

Inventory Costing Method

Weighted

Income Statement Units FIFO LIFO Average

Sales Revenue ……………………………….. 4,100 $307,500 $307,500 $307,500

Cost of Goods Sold* ………………………… 4,100 152,800 155,500 153,340

Cost of Goods Sold ………. 4,100 $152,800 $155,500 $153,340

**Inventory computations:

FIFO: 900 units @ $38 = $34,200

LIFO: 900 units @ $35 = $31,500

Average: [(1,000 units @ $35) + (4,000 units @ $38)] ÷ 5,000 units = $37.40

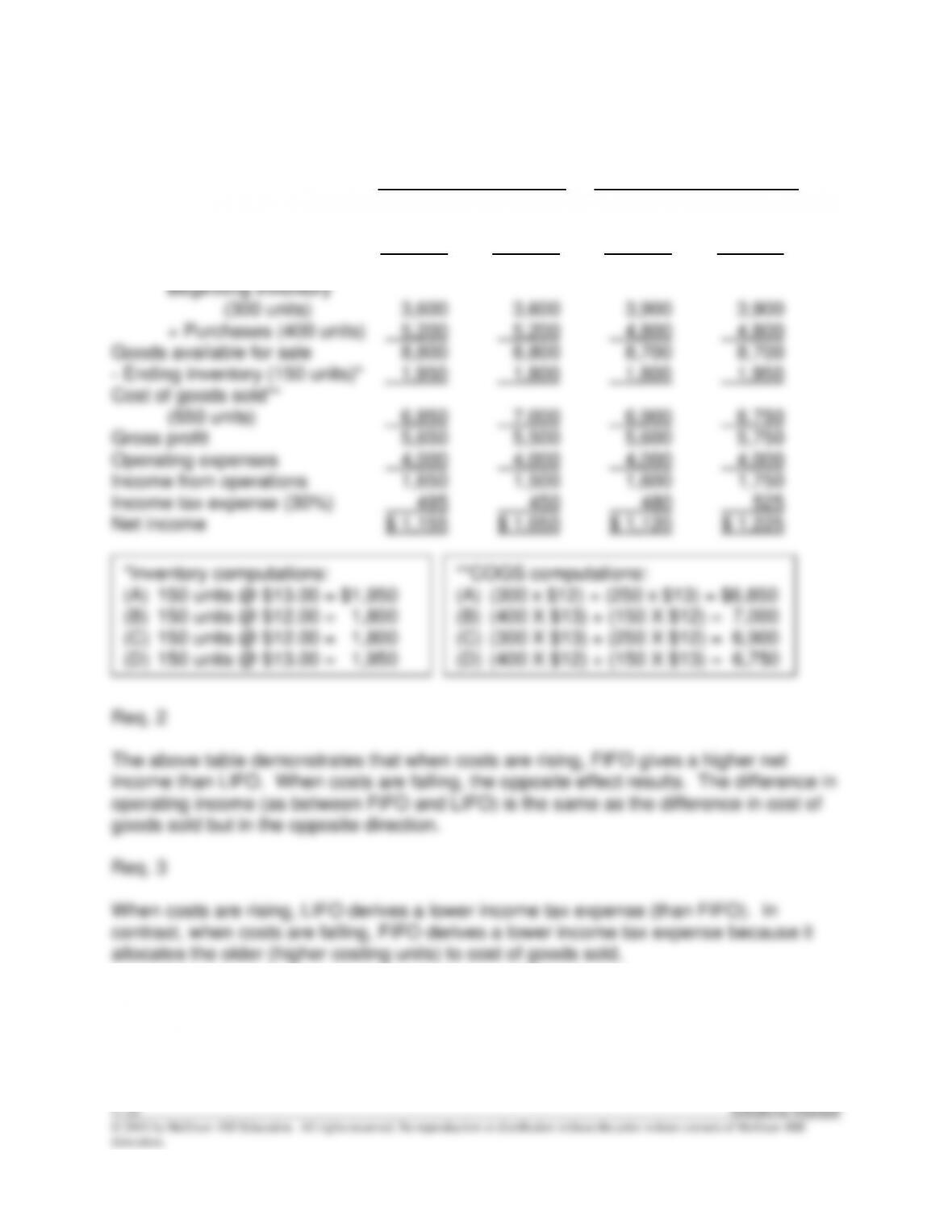

E7–9

Req. 1

Costs Rising Costs Falling

FIFO LIFO FIFO LIFO

(A) (B) (C) (D)

Sales revenue (550 units) $12,500 $12,500 $12,500 $12,500

Cost of goods sold:

E7–10

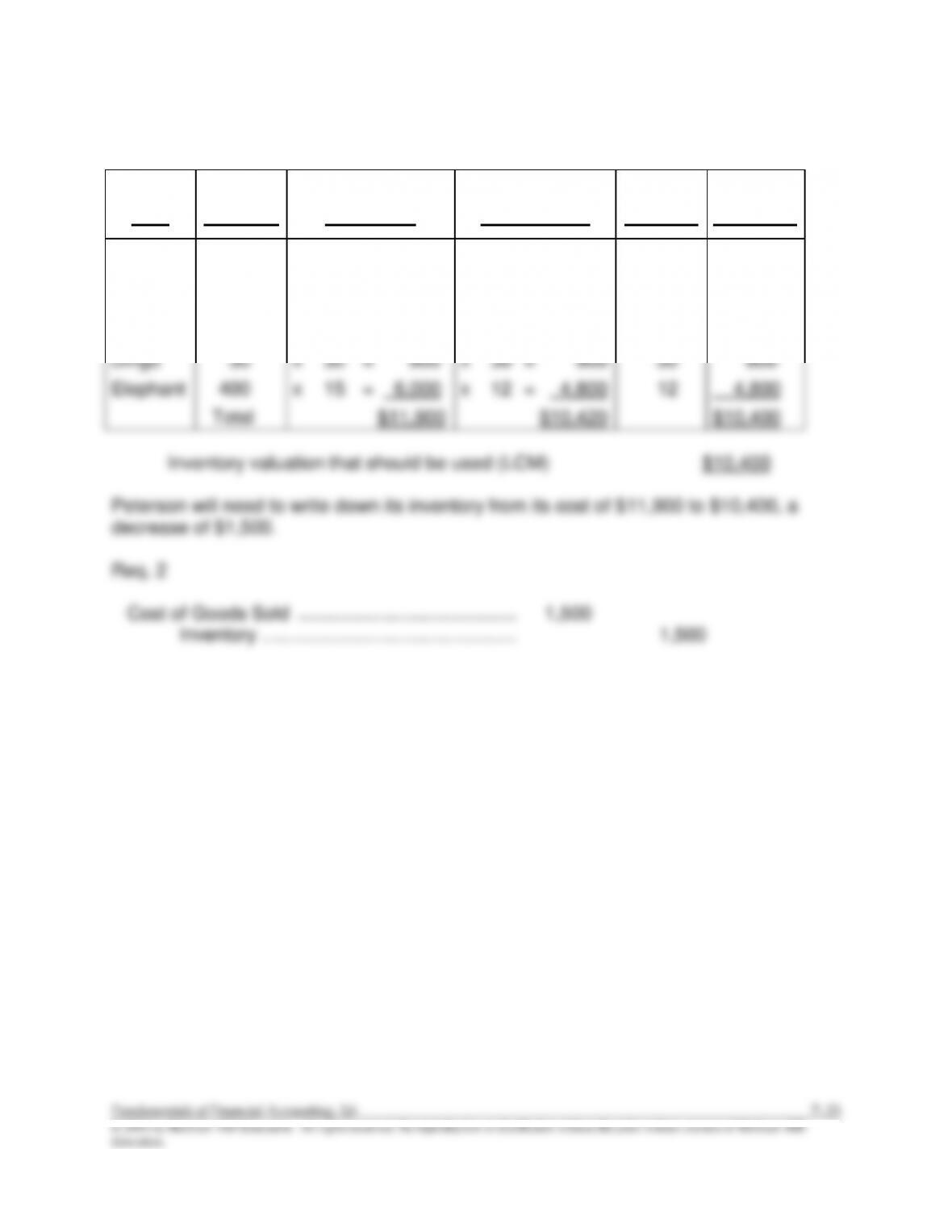

Req. 1

Item

Quantity

Total Cost

Total Market

LCM

Per Item

LCM

Valuation

Alligator

50

x

$30

=

$1,500

x

$24

=

$1,200

$ 24

$1,200

Bear

75

x

40

=

3,000

x

40

=

3,000

40

3,000

Cougar

10

x

50

=

500

x

52

=

520

50

500

Dingo

30

x

30

=

900

x

30

=

900

30

900

Elephant

400

x

15

=

6,000

x

12

=

4,800

12

4,800

Total

$11,900

$10,420

$10,400

Inventory valuation that should be used (LCM) $10,400

Peterson will need to write down its inventory from its cost of $11,900 to $10,400, a

decrease of $1,500.

Req. 2

Cost of Goods Sold ……………………………………

1,500

Inventory ………………………………………….

1,500

E7–11

Req. 1

Item

Quantity

Total Cost

Total Market

LCM

Valuation

Air Flow

20

x

$12

=

$ 240

x

$14

=

$ 280

$ 240

B Buster

75

x

40

=

3,000

x

38

=

2,850

2,850

Coolonite

35

x

55

=

1,925

x

50

=

1,750

1,750

Dudesly

10

x

30

=

300

x

35

=

350

300

Total

$5,465

$5,230

$5,140

Inventory valuation that should be used (LCM) $5,140

Req. 2

The write–down to lower of cost or market will increase Cost of Goods Sold by the

amount of the write–down, $325:

Total Cost − LCM Valuation = Write–down

$5,465 − $5,140 = $325 Write–down

E7–12

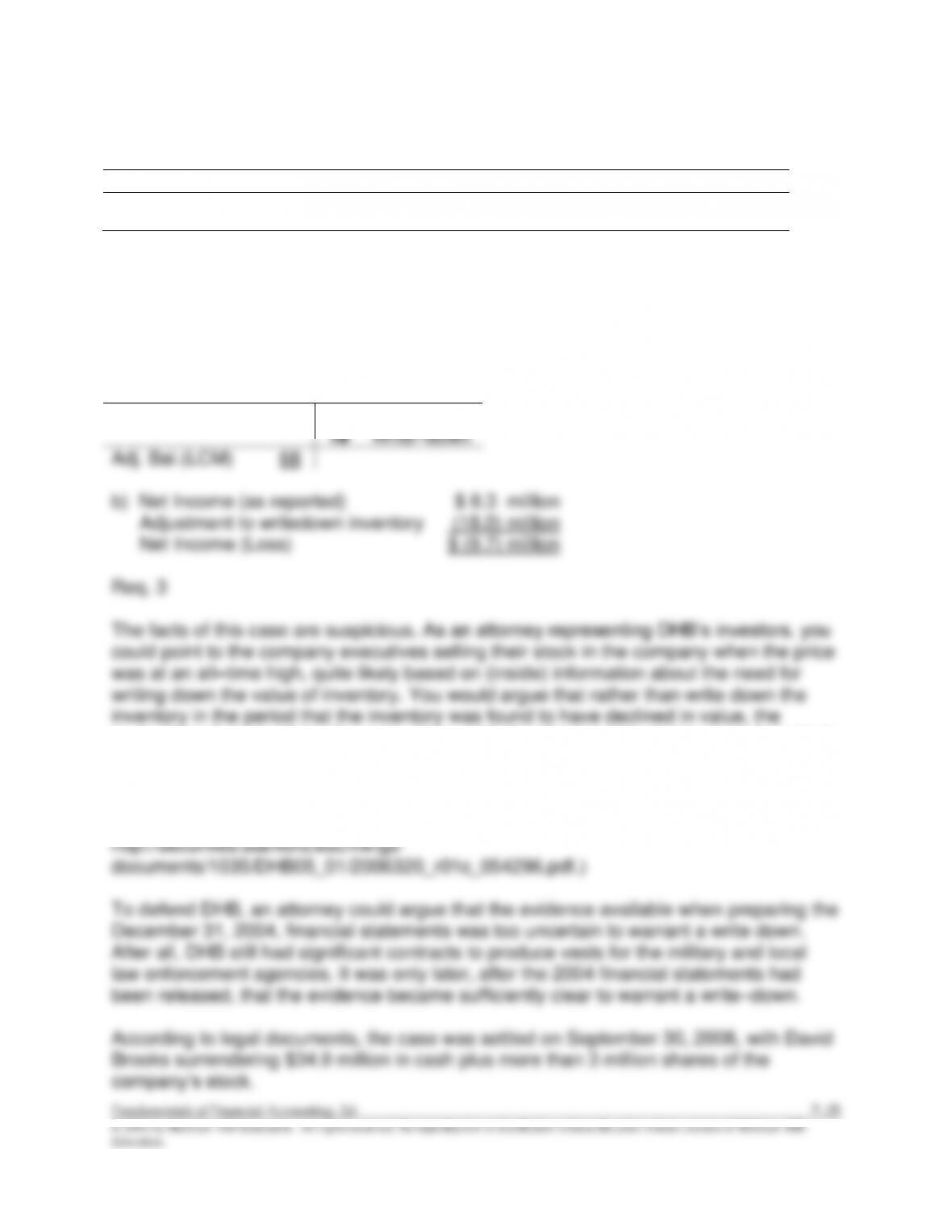

Req. 1

Assets =

Liabilities

+ Stockholders’ Equity

Inventory –18 million

Cost of Goods Sold (+E) –18 million

Cost of Goods Sold …………………………..……………….. 18 million

Inventory ……………………………………………………… 18 million

Req. 2

a)

Inventory

Unadj. Bal.

86

18

Write–down

Adj. Bal.(LCM)

68

executives chose to delay the write–down until after they had been able to cash–in their

own personal stock at a higher stock price. You would argue that the failure of Second

Chance was evidence that the market value of Zylon and Zylon–based inventories were

less than their cost. (Interesting enough, these are the precise claims made in a class

action lawsuit filed on March 20, 2006. A copy of that complaint is posted online at

E7–13

Req. 1

2012

2011

2010

Inventory

Turnover Ratio

=

Cost of Goods Sold

=

7.1*

7.0**

7.0***

Average Inventory

Days to Sell

=

365 Days

=

51.4

52.1

52.1

Inventory Turnover

Ratio

Calculations:

* 7.1 = $2,280 ÷ $320

** 7.0 = $1,900 ÷ $270

*** 7.0 = $1,460 ÷ $210

Req. 2

The inventory turnover ratio reflects how many times average inventory was acquired

and sold during the year. The inventory turnover ratio for Polaris Industries has been

consistent throughout 2010 to 2012. Polaris is performing better than Arctic Cat, where

the inventory turnover is 5.4 times per year or every 67.6 days.

times per year

days

E7–14

Req. 1

Units Sold = 80 + 56 = 136.

Ending Inventory Units = Units Available – Units Sold = 188 – 136 = 52 units.

FIFO

Beginning Inventory

38 units x $ 14

$ 532

+ Purchase

50 units x $ 15

750

+ Purchase

100 units x $ 16

1,600

Goods Available for Sale

188 units

2,882

– Ending Inventory (LIST) (52 × $16)

832

Cost of Goods Sold (FIFO) (38 x $14)+(50 × $15)+(48 x $16)

$ 2,050

LIFO

Beginning Inventory

38 units x $ 10

$ 380

+ Purchase

50 units x $ 15

750

+ Purchase

100 units x $ 16

1,600

Goods Available for Sale

188 units

2,730

– Ending Inventory (FIST) (38 × $10) + (14 x $15)

590

Cost of Goods Sold (LIFO) (100 x $16) + (36 x $15)

$ 2,140

Req. 2

FIFO

Inventory turnover

=

Cost of Goods Sold

=

$2,050

=

3.01

Average Inventory

($532 + $832)/2

LIFO

Inventory turnover

=

Cost of Goods Sold

=

$2,140

=

4.41

Average Inventory

($380 + $590)/2

Req. 3

The inventory method used does make a significant difference in the inventory turnover

ratio. If analysts are comparing across companies, they must take this into account

before deciding whether one company has better inventory management than another.

If they are comparing the same company over time, however, it is not as important

provided the company is consistent in the method it uses.

E7–15

Remaining

Perpetual FIFO

Units

Unit Cost

Total Cost

Inventory Value

Beginning Inventory

120

$80

$ 9,600

$ 9,600

Purchase January 15

380

90

34,200

43,800

Sale

(120)

80

(9,600)

34,200

(120)

90

(10,800)

23,400

Purchase January 24

200

110

22,000

45,400

Ending Inventory

$45,400

[(260 x $90) + (200 x $110)]

Cost of Goods Sold

$20,400

[(120 x $80) + (120 x $90)]

Remaining

Perpetual LIFO

Units

Unit Cost

Total Cost

Inventory Value

Beginning Inventory

120

$80

$ 9,600

$ 9,600

Purchase January 15

380

90

34,200

43,800

Sale

(240)

90

(21,600)

22,200

Purchase January 24

200

110

22,000

44,200

Ending Inventory

$44,200

[(120 x $80) + (140 x $90) + (200 x $110)]

Cost of Goods Sold

$21,600

(240 x $90)

E7–16

Remaining

Perpetual FIFO

Units

Unit Cost

Total Cost

Inventory Value

a)

Beginning Inventory

300

$12

$ 3,600

$ 3,600

b)

Purchase April 11

900

10

9,000

12,600

d)

Sale May 1

(300)

12

(3,600)

9,000

c)

Purchase June 1

800

13

10,400

19,400

e)

Sale July 3

(600)

10

(6,000)

13,400

Ending Inventory

$13,400

[(300 x $10) + (800 x $13)]

Cost of Goods Sold

$9,600

[(300 x $12) + (600 x $10)]

Remaining

Perpetual LIFO

Units

Unit Cost

Total Cost

Inventory Value

a)

Beginning Inventory

300

$12

$ 3,600

$ 3,600

b)

Purchase April 11

900

10

9,000

12,600

d)

Sale May 1

(300)

10

(3,000)

9,600

c)

Purchase June 1

800

13

10,400

20,000

e)

Sale July 3

(600)

13

(7,800)

12,200

Ending Inventory

$12,200

[(300 x $12) + (600 x $10) + (200 x $13)]

Cost of Goods Sold

$10,800

[(300 x $10) + (600 x $13)]

E7–17

Req. 1

The $400 understatement of ending inventory produced operating income amounts that

were incorrect by the amount of $400 for each quarter. However, the effects on

operating income for each quarter were opposing (i.e., the first quarter operating income

was understated by $400, and in the second quarter it was overstated by $400). This

self–correction produces a correct combined income for the two quarters.

Req. 2