Chapter 7

1. Three goals of inventory management are to make or buy products (1) in sufficient

quantities to avoid stock–outs (which could result in lost sales revenue and

2. Merchandisers hold merchandise inventory, which usually is acquired in a finished

(1) Raw materials inventory includes materials that eventually are processed further

(2) Work in process inventory includes goods that are in the process of being

(3) Finished goods inventory includes manufactured goods that are complete and

3. (a) Specific identification–This inventory costing method requires that each

item in the beginning inventory and each item purchased during the period

be identified specifically so that its unit cost can be determined by

identifying the specific item sold. This method usually requires that each

item be marked, often with a code that indicates its cost. When it is sold,

4. The first–in, first–out (FIFO) cost flow assumption is most similar to the gumball

machine. Gumballs (inventory) placed first in the machine are the first out through

the bottom of the machine.

5. Inventory costing does not have to follow the actual flow of a company’s products.

6. LIFO and FIFO have opposite effects on ending inventory on the balance sheet.

The ending inventory is based upon either the oldest unit cost or the newest unit

7. LIFO versus FIFO affects both cost of goods sold and gross profit on the income

8. In times of rising costs, LIFO results in the highest Cost of Goods Sold and,

therefore, the lowest Net Income. Consequently, it is true that the switch from LIFO

to FIFO would increase the company’s Gross Profit and Net Income. Whether this

switch would benefit the managers by increasing their bonus is debatable. One

9. LCM is applied when market (often defined as current replacement cost) is lower

than the cost of units on hand. The LCM requirement to write down ending

10. If the new evidence causes the market value of the existing inventory to fall below

its original cost, the lower of cost or market rule requires that the inventory be

written down. This LCM write–down will reduce the Inventory account on the

balance sheet and will increase the Cost of Goods Sold account on the income

11. The owner is correct in thinking that outsourcing will reduce the amount of inventory

that the company needs to carry. All else equal, a reduction in inventory will cause

12. In a perpetual inventory system, LIFO numbers are calculated using the cost of

period.

13. The effects of inventory errors are felt in more than one period because the ending

inventory for the current period becomes the beginning inventory of the next period.

Authors’ Recommended Solution Time

(Time in minutes)

Mini–exercises

Exercises

Problems

Skills

Development

Cases*

Continuing

Case

No.

Time

No.

Time

No.

Time

No.

Time

No.

Time

1

5

1

10

CP7–1

30

1

20

1

15

2

3

2

15

CP7–2

40

2

25

2

10

3

3

3

15

CP7–3

20

3

30

4

3

4

30

CP7–4

15

4

35

5

2

5

30

CP7–5

30

5

35

6

5

6

30

PA7–1

30

6

40

7

5

7

30

PA7–2

40

7

20

8

10

8

25

PA7–3

20

9

3

9

15

PA7–4

15

10

5

10

15

PA7–5

30

11

3

11

10

PB7–1

30

12

3

12

15

PB7–2

40

13

6

13

20

PB7–3

30

14

6

14

10

PB7–4

15

15

10

15

30

PB7–5

30

16

10

16

30

C7–1

20

17

10

17

25

C7–2

60

C7–3

20

* It is difficult to estimate the time students will need to complete cases. As with any

open–ended project, students could devote significant time to these assignments.

7–6 Solutions Manual

© 2016 by McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO MINI–EXERCISES

M7–1

Type of Business

Type of Inventory Merchandising Manufacturing

M7–2

The inventory in transit to Abercrombie & Fitch was sold as FOB shipping point since the

inventory in transit was considered to be owned by Abercrombie & Fitch before the

M7–3

I/S

a.

Sales Revenue

Not

b.

Inventories (held on consignment)

I/S

c.

Cost of Goods Sold

B/S

d.

Inventories (out on consignment)

M7–4

1. Declining Costs

2. Rising Costs

a. Lowest net income

FIFO

LIFO

b. Lowest ending inventory

FIFO

LIFO

M7–5

(a)

Declining costs

FIFO

(b)

Rising costs

LIFO

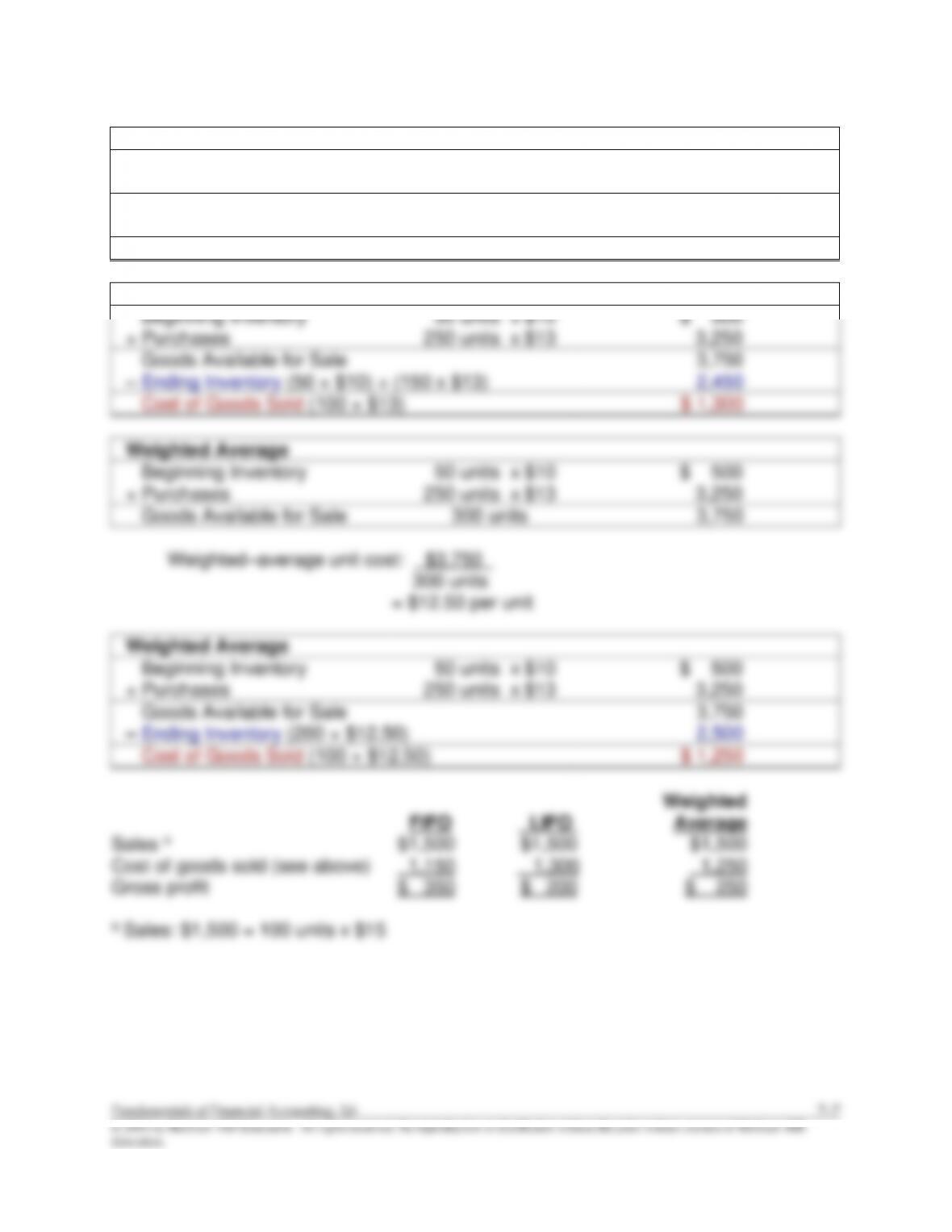

M7–6

FIFO

Beginning Inventory

50 units x $10

$ 500

+ Purchases

250 units x $13

3,250

Goods Available for Sale

3,750

– Ending Inventory (200 × $13)

2,600

Cost of Goods Sold (50 × $10) + (50 × $13)

$ 1,150

LIFO

Beginning Inventory

50 units x $10

$ 500

+ Purchases

250 units x $13

3,250

Goods Available for Sale

3,750

– Ending Inventory (50 × $10) + (150 x $13)

2,450

Cost of Goods Sold (100 × $13)

$ 1,300

Beginning Inventory

50 units x $10

$ 500

+ Purchases

250 units x $13

3,250

Goods Available for Sale

3,750

Weighted Average

$ 500

3,250

3,750

Cost of Goods Sold (100 × $12.50)

$ 1,250

1,250

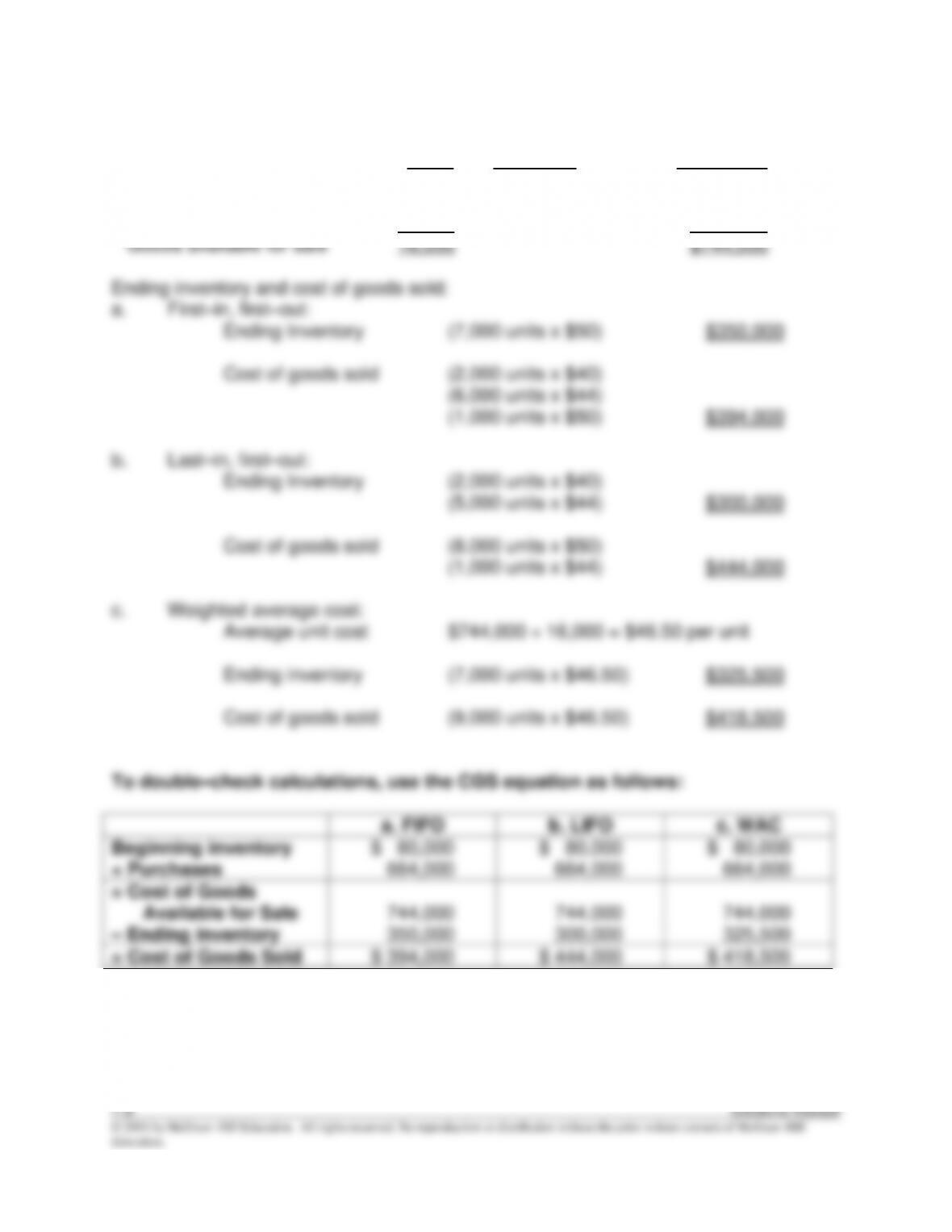

M7–7

Goods available for sale –

All methods

Units

Unit Cost

Total Cost

Beginning inventory

2,000

$40

$ 80,000

Next units in (7/13 purchase)

6,000

44

264,000

Next units in (7/25 purchase)

8,000

50

400,000

Goods available for sale

16,000

$744,000

Ending inventory and cost of goods sold:

a. First–in, first–out:

Ending Inventory (7,000 units x $50) $350,000

Cost of goods sold (2,000 units x $40)

(6,000 units x $44)

(1,000 units x $50) $394,000

b. Last–in, first–out:

Ending Inventory (2,000 units x $40)

(5,000 units x $44) $300,000

Cost of goods sold (8,000 units x $50)

(1,000 units x $44) $444,000

c. Weighted average cost:

Average unit cost $744,000 ÷ 16,000 = $46.50 per unit

Ending inventory (7,000 units x $46.50) $325,500

Cost of goods sold (9,000 units x $46.50) $418,500

To double–check calculations, use the CGS equation as follows:

a. FIFO

b. LIFO

c. WAC

Beginning inventory

$ 80,000

$ 80,000

$ 80,000

+ Purchases

664,000

664,000

664,000

= Cost of Goods

Available for Sale

744,000

744,000

744,000

– Ending inventory

350,000

300,000

325,500

= Cost of Goods Sold

$ 394,000

$ 444,000

$ 418,500

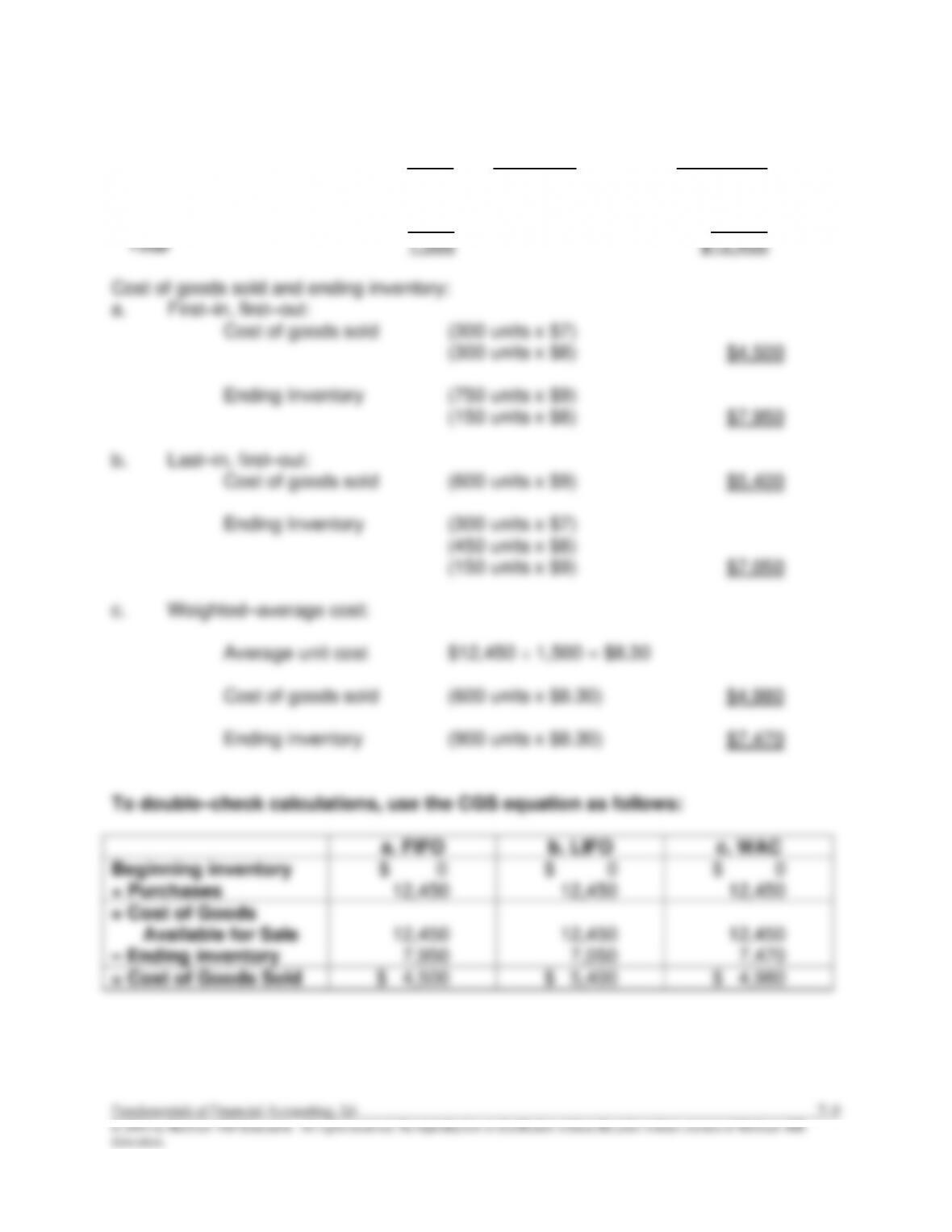

M7–8

Goods available for sale –

All methods

Units

Unit Cost

Total Cost

First units in (January 1)

300

$7

$2,100

Next units in (January 8)

450

8

3,600

Next units in (January 29)

750

9

6,750

Total

1,500

$12,450

Cost of goods sold and ending inventory:

a. First–in, first–out:

Cost of goods sold (300 units x $7)

(300 units x $8) $4,500

Ending Inventory (750 units x $9)

(150 units x $8) $7,950

b. Last–in, first–out:

Cost of goods sold (600 units x $9) $5,400

Ending Inventory (300 units x $7)

(450 units x $8)

(150 units x $9) $7,050

c. Weighted–average cost:

Average unit cost $12,450 ÷ 1,500 = $8.30

Cost of goods sold (600 units x $8.30) $4,980

Ending inventory (900 units x $8.30) $7,470

To double–check calculations, use the CGS equation as follows:

a. FIFO

b. LIFO

c. WAC

Beginning inventory

$ 0

$ 0

$ 0

+ Purchases

12,450

12,450

12,450

= Cost of Goods

Available for Sale

12,450

12,450

12,450

– Ending inventory

7,950

7,050

7,470

= Cost of Goods Sold

$ 4,500

$ 5,400

$ 4,980

M7–9

Cost per

item

Replacement

cost per item

Lower of cost

or market

Quantity

Total reported on

balance sheet

Necklaces

$ 75

$70

$70

10

10 x $70 = $ 700

Bracelets

40

60

40

50

50 x $40 = $2,000

Total

$2,700

M7–10

Assets = Liabilities + Stockholders’ Equity

Inventory –1,700,000,000 Cost of Goods Sold (+E) –1,700,000,000

Cost of Goods Sold …………………………………….

1,700,000,000

Inventory ………………………………………….

1,700,000,000

To record inventory write down to LCM.

M7–11

+

(a)

Inventory delivered by suppliers daily instead of weekly.

+

(b)

Shorten production process from 10 days to 8 days.

NE

(c)

Extend payments for inventory purchases from 15 days to 30 days.

M7–12

a.

“the current rate of sale”

Inventory turnover ratio or Days to sell

b.

“the age of the inventory”

Inventory turnover ratio or Days to sell

c.

“the profitability of the inventory”

Gross profit percentage

M7–13

Case

BI

Purchases

CGS

EI

Inventory

Turnover

Ratio

Days to

Sell

a.

$100

$700

$600

$200

4.0

91.3

b.

200

1200

1,200

200

6.0

60.8

c.

50

1,100

1,000

150

10.0

36.5

Notes:

b. Inv. Turn. = COGS/Avg. Inventory, so 1,200/x = 6 implies x = 200 (Avg Inv), so if BE = 200, EI = 200

c. 365 / Turnover = Days to Sell, so 365/x = 36.5, so x = 10 times