Chapter Outline

Teaching Notes

B. Comparison to Benchmarks

Illustrated in Exhibit 7.7

1. Inventory turnover ratios and the number of days to sell

can be helpful in comparing different companies’

inventory management practices.

2. These measures can vary significantly between industries:

a. For merchandisers, inventory turnover refers to buying

and selling goods.

b. For manufacturers, it refers to producing and

delivering inventory to customers

3. Inventory turnover measures also can vary significantly

between companies within the same industry, particularly

if they take different approaches to pricing their

inventories.

The “Spotlight on Financial

Reporting” feature suggests

4. Often, the company with a lower gross profit percentage

has a faster inventory turnover

That worsening inventory

turnover and gross profit

5. With this big a range in ratios between industries and

companies, it’s most useful to compare a company’s

turnover with its own results from prior periods.

percentages may signal the

need for a write-down to

report inventory at LCM

IV. Supplement 7A—FIFO, LIFO, and Weighted Average in a

Perpetual Inventory System

LO 7–S1 Compute inventory costs in perpetual systems.

A. Reasons for Showing Cost Flow Assumptions in a Periodic

Inventory System:

1. First, only the LIFO and weighted average calculations

differ between periodic and perpetual inventory systems.

2. FIFO calculations don’t differ between periodic and

perpetual systems.

3. Nearly half of all U.S. companies use FIFO, so even if

they calculate costs under a perpetual system, it is

identical to calculating costs under a periodic system.

4. Also, most LIFO companies actually use FIFO during the

period and then adjust to LIFO at the end of the period.

By waiting to the end of the period to calculate this LIFO

adjustment, it’s as if all purchases during the period were

recorded before the Cost of Goods Sold is calculated and

recorded.

B. FIFO (First-in, First-Out)—FIFO calculations don’t differ

between periodic and perpetual systems.

C. LIFO (Last-in, First-Out)

1. LIFO numbers are calculated using the cost of goods last

in as of the date of sale.

2. This differs from a periodic system, where the cost of

goods sold is calculated as if all sales occurred at the end

of the period.

Chapter Outline

Teaching Notes

D. Weighted Average Cost—In a perpetual inventory system,

the weighted average cost must be calculated each time a

sale is recorded.

E. Financial Statement Effects

Summarized in Exhibit 7A.1

1. These methods differ only in the way they split the cost of

goods available for sale between ending inventory and

cost of goods sold.

2. If a cost goes into Cost of Goods Sold, it must be taken

out of Inventory.

3. Thus, the method that assigns the highest cost to cost of

goods sold assigns the lowest cost to ending inventory

(and vice versa).

V. Supplement 7B—The Effects of Errors in Ending Inventory

LO 7–S2 Determine the effects of inventory errors.

A. Impact of Errors on Current Year’s Financial Statements

1. Errors in inventory affect both the balance sheet and

income statement.

Impact on income taxes

ignored in the discussion.

2. As the cost of goods sold equation indicates, a direct

relationship exists between ending inventory and cost of

goods sold because items not in the ending inventory are

assumed to have been sold.

3. Thus, any errors in ending inventory will affect the

balance sheet (current assets) and the income statement

(cost of goods sold, gross profit, and net income).

B. Impact of Errors on Following Year’s Financial Statements

Illustrated in Exhibit 7B.1

The effects of inventory errors are felt in more than one year

because the ending inventory for one year becomes the

beginning inventory for the next year.

C. Determining the Effects of Errors in Inventory

To determine the effects of inventory errors on the financial

statements in both the current year and the following year,

use the cost of goods sold equation.

Supplemental Enrichment Activities

Note: These activities would be suitable for individual or group activities.

1. Handout 7–1

Use Handout 7–1 for an in-class activity designed to review the calculation of costs using all four

inventory costing methods. The solution follows the handout master.

2. Handout 7–2

Use Handout 7–2 for an in-class activity designed to review the application of the lower of cost or

market rule. The solution follows the handout master.

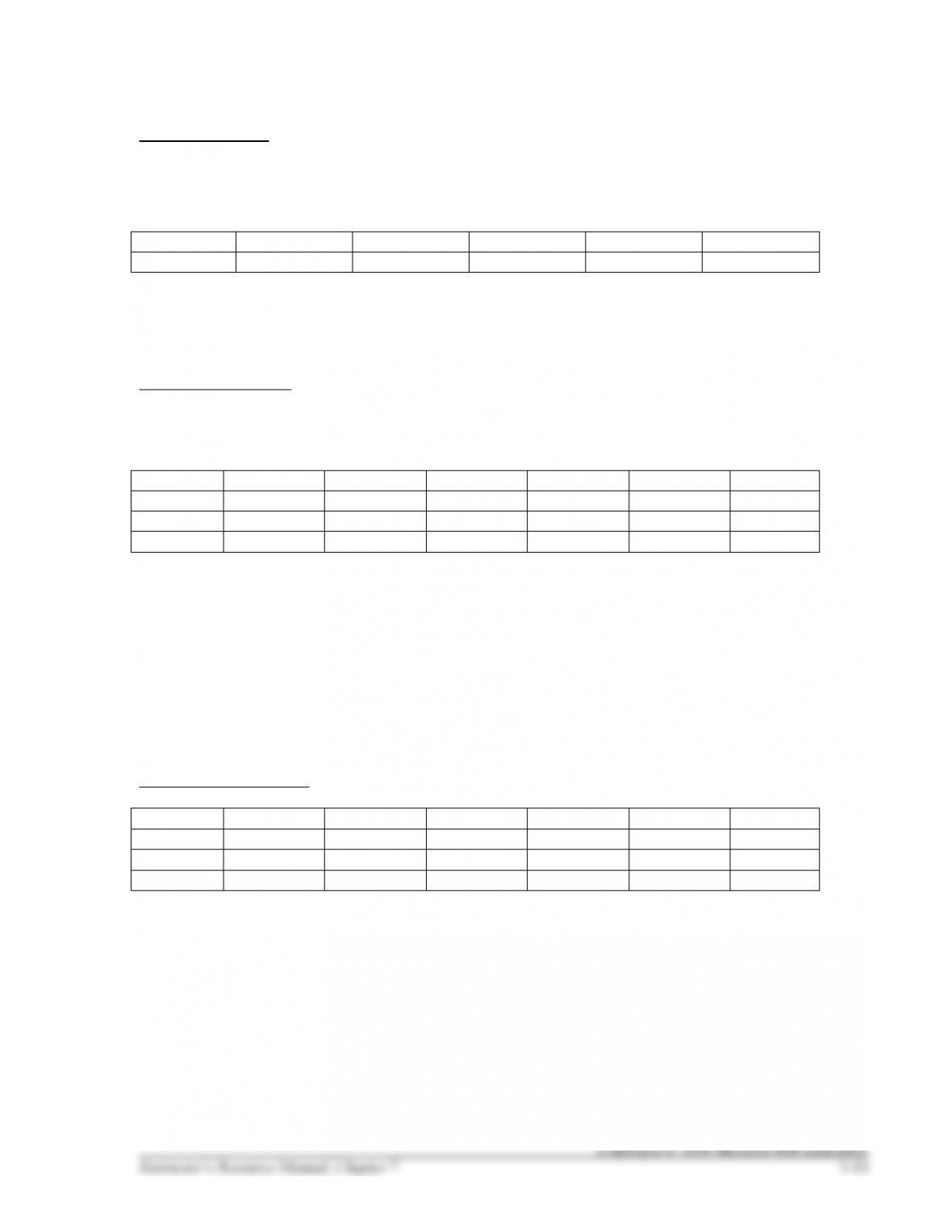

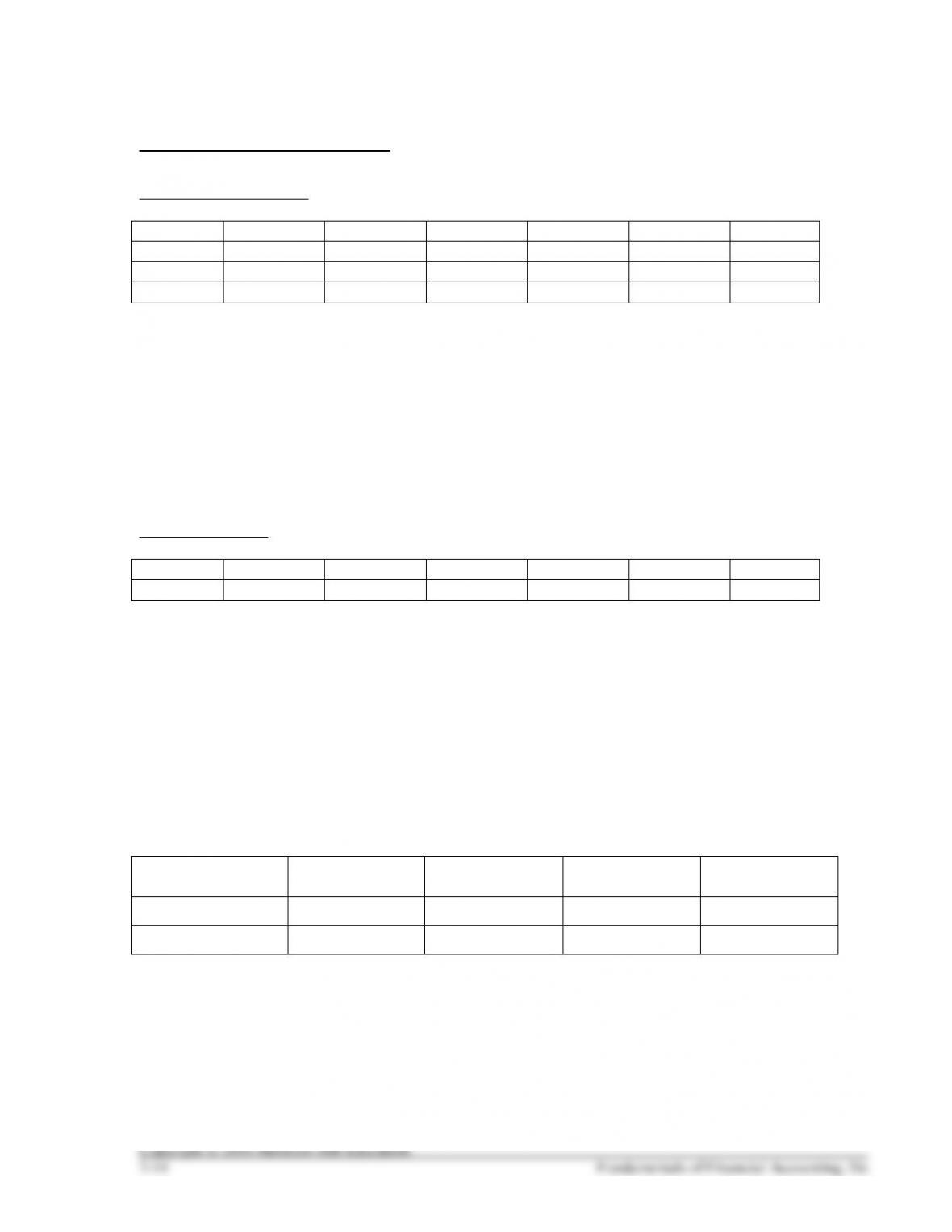

HANDOUT 7–1

INVENTORY COSTING METHODS

Quickie Grocery acquired the following five bottles of Corporate-Cola soft drink:

Date

Jan. 2

Jan. 10

Jan. 12

Jan. 16

Jan. 25

Cost

$1.00

$2.00

$3.00

$4.00

$5.00

A January 31 inventory count revealed that two bottles remained on the shelf. How many bottles were

sold in January?

Specific Identification

The Quickie Grocery keeps track of each individual bottle. Suppose the Grocery knows that it sold the

bottles acquired on Jan. 2, 12, and 16.

Date

Jan. 2

Jan. 10

Jan. 12

Jan. 16

Jan. 25

Total

Cost

$1.00

$2.00

$3.00

$4.00

$5.00

$15.00

COGS

Inventory

What was the value of inventory on January 31?

What was the cost of goods sold for January?

First-in, First-out (FIFO)

Date

Jan. 2

Jan. 10

Jan. 12

Jan. 16

Jan. 25

Total

Cost

$1.00

$2.00

$3.00

$4.00

$5.00

$15.00

COGS

Inventory

What was the value of inventory on January 31?

What was the cost of goods sold for January?

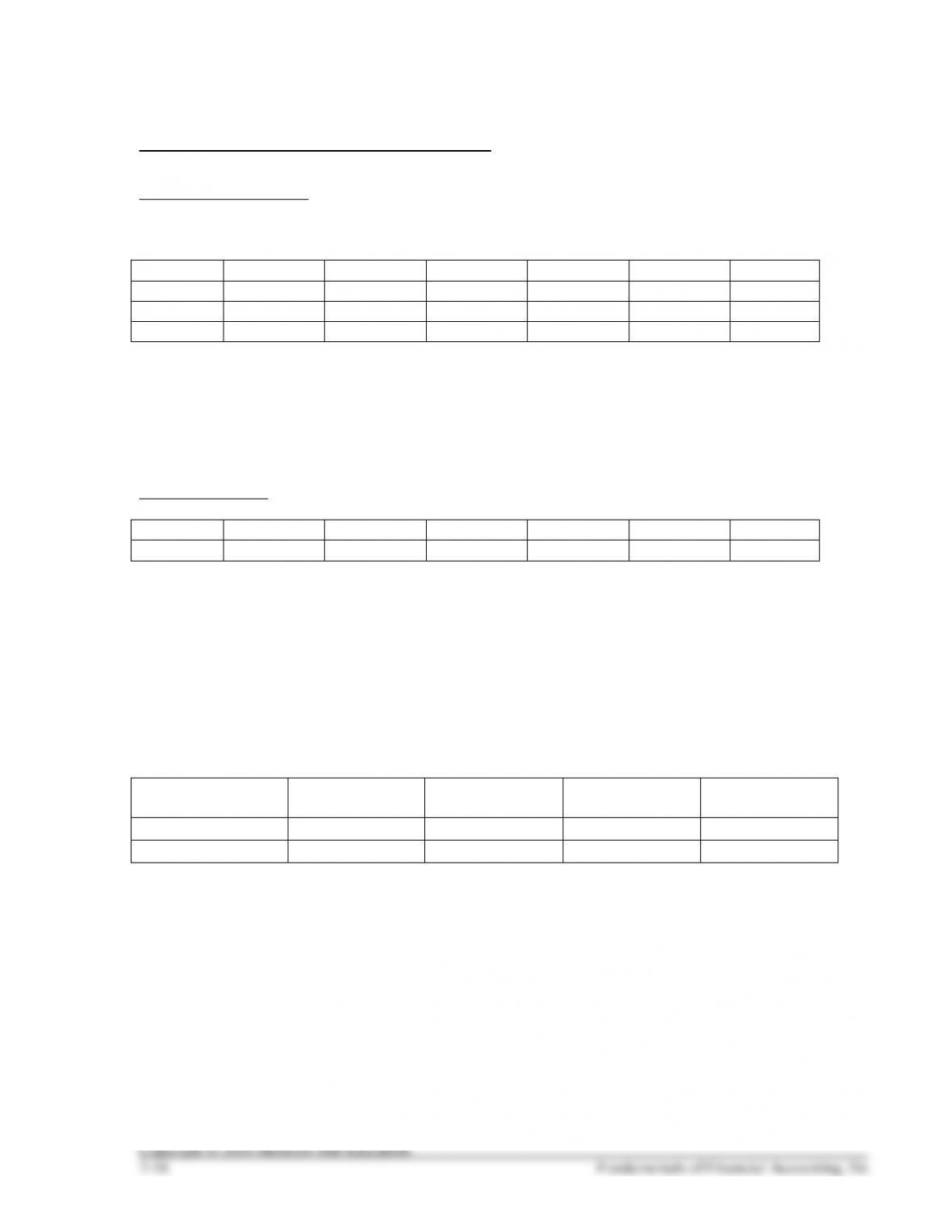

HANDOUT 7–1, CONTINUED

Last-in, First-out (LIFO)

Date

Jan. 2

Jan. 10

Jan. 12

Jan. 16

Jan. 25

Total

Cost

$1.00

$2.00

$3.00

$4.00

$5.00

$15.00

COGS

Inventory

What was the value of inventory on January 31?

What was the cost of goods sold for January?

Weighted Average

Date

Jan. 2

Jan. 10

Jan. 12

Jan. 16

Jan. 25

Cost

$1.00

$2.00

$3.00

$4.00

$5.00

$15.00

What was the value of inventory on January 31?

What was the cost of goods sold for January?

Complete the following table:

Specific

Identification

FIFO

LIFO

Weighted

Average

Cost of Goods Sold

Inventory

HANDOUT 7–1 SOLUTION

INVENTORY COSTING METHODS

Quickie Grocery acquired the following five bottles of Corporate-Cola soft drink:

Date

Jan. 2

Jan. 10

Jan. 12

Jan. 16

Jan. 25

Cost

$1.00

$2.00

$3.00

$4.00

$5.00

A January 31 inventory count revealed that two bottles remained on the shelf.

How many bottles were sold in January?

5 – 2 = 3 bottles

Specific Identification

The Quickie Grocery keeps track of each individual bottle. Suppose the Grocery knows that it sold the

bottles acquired on Jan. 2, 12, and 16.

Date

Jan. 2

Jan. 10

Jan. 12

Jan. 16

Jan. 25

Cost

$1.00

$2.00

$3.00

$4.00

$5.00

$15.00

COGS

$1.00

$3.00

$4.00

$8.00

Inventory

$2.00

$5.00

$7.00

What was the cost of goods sold for January?

$8.00

What was the value of inventory on January 31?

$7.00

First-in, First-out (FIFO)

Date

Jan. 2

Jan. 10

Jan. 12

Jan. 16

Jan. 25

Cost

$1.00

$2.00

$3.00

$4.00

$5.00

$15.00

COGS

$1.00

$2.00

$3.00

$6.00

Inventory

$4.00

$5.00

$9.00

What was the cost of goods sold for January?

$6.00

What was the value of inventory on January 31?

$9.00

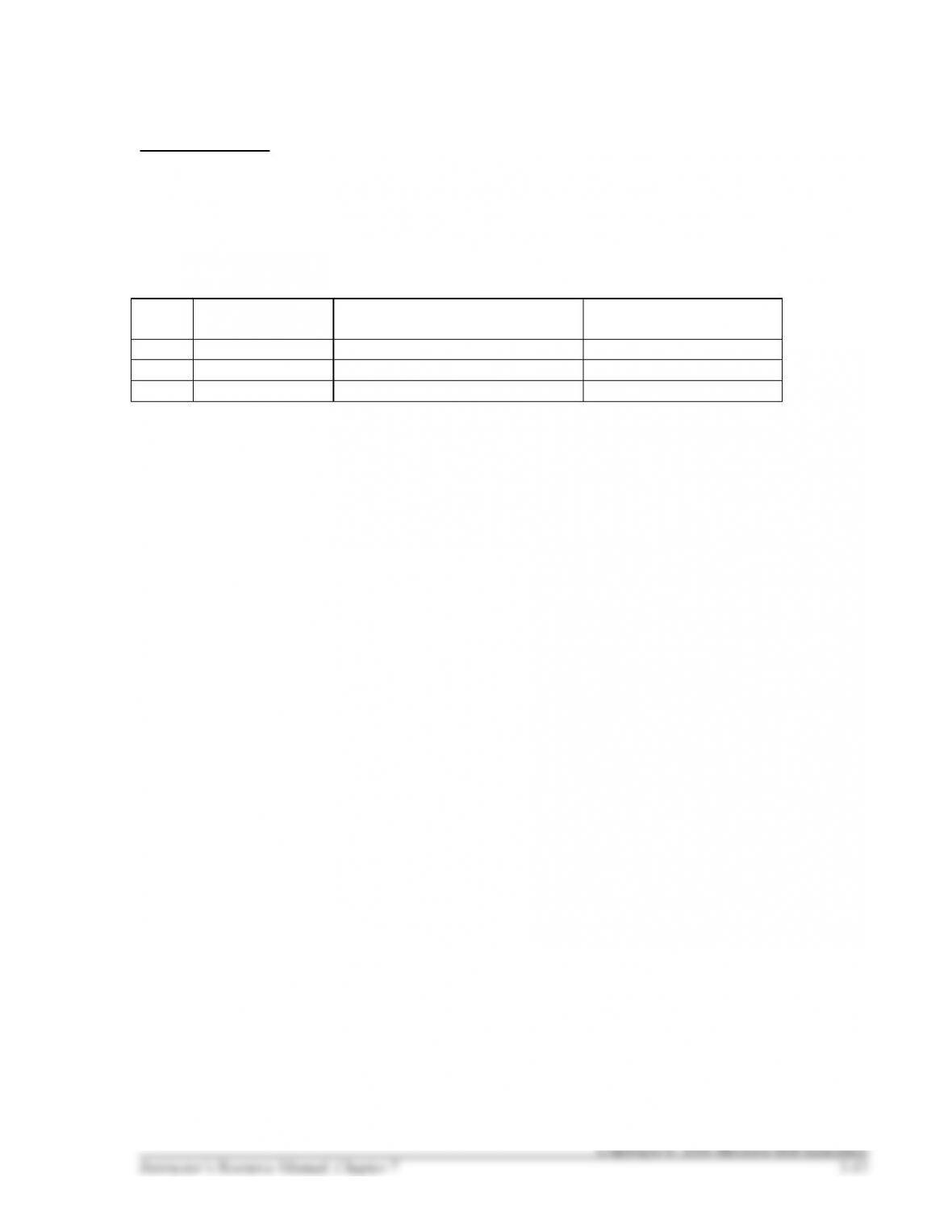

HANDOUT 7–1 SOLUTION, CONTINUED

Last-in, First-out (LIFO)

Assume that the last bottles purchased were the first to be sold. First bottles are still here.

Date

Jan. 2

Jan. 10

Jan. 12

Jan. 16

Jan. 25

Cost

$1.00

$2.00

$3.00

$4.00

$5.00

$15.00

COGS

$3.00

$4.00

$5.00

$12.00

Inventory

$1.00

$2.00

$3.00

What was the cost of goods sold for January?

$12.00

What was the value of inventory on January 31?

$3.00

Weighted Average

Date

Jan. 2

Jan. 10

Jan. 12

Jan. 16

Jan. 25

Cost

$1.00

$2.00

$3.00

$4.00

$5.00

$15.00

What was the cost of goods sold for January?

$15.00 / 5 = $3.00 average cost per unit

$3 × 3 units = $9.00

What was the value of inventory on January 31?

$15.00 / 5 = $3.00 average cost per unit

$3 × 2 units= $6.00

Complete the following table:

Specific

Identification

FIFO

LIFO

Weighted

Average

Cost of Goods Sold

8

6

12

9

Inventory

7

9

3

6

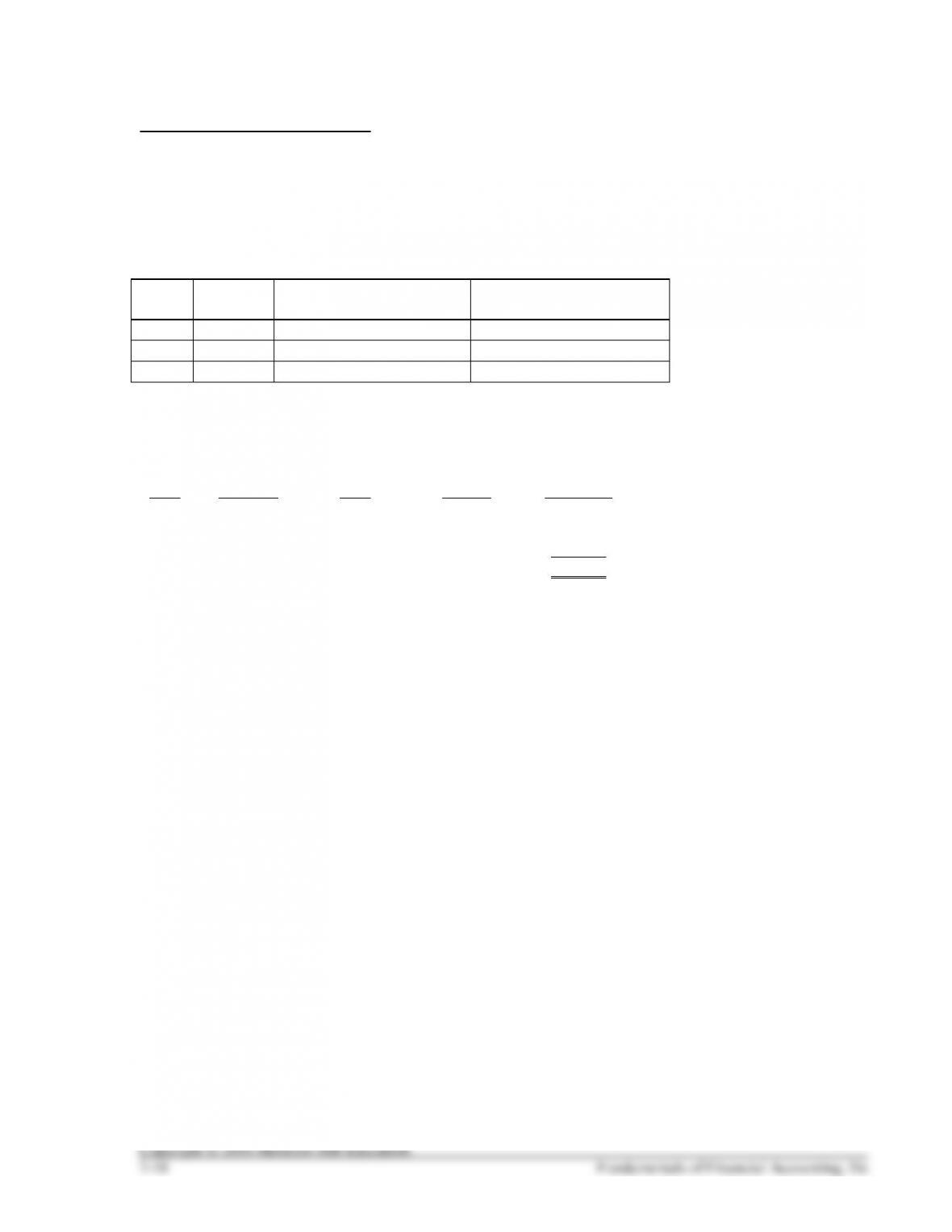

HANDOUT 7–2

LOWER OF COST OR MARKET (LCM)

Amanda Corporation is preparing its financial statements for the year ending December 31, 2013. Ending

inventory information about the three major items stocked for regular sale follows:

Item

Quantity on Hand

Unit Cost When Acquired (FIFO)

Replacement Cost

(Market) at Year-End

AA

100

$ 30

$ 26

BB

150

80

80

CC

200

100

104

Compute the valuation that should be used for the ending inventory using the LCM rule applied on an

item-by-item basis.

HANDOUT 7–2 SOLUTION

LOWER OF COST OR MARKET (LCM)

Amanda Corporation is preparing its financial statements for the year ending December 31, 2013. Ending

inventory information about the three major items stocked for regular sale follows:

Item

Quantity

on Hand

Unit Cost When Acquired

(FIFO)

Replacement Cost

(Market) at Year-End

AA

100

$ 30

$ 26

BB

150

80

80

CC

200

100

104

Compute the valuation that should be used for the ending inventory using the LCM rule applied on an

item-by-item basis.

Item

Quantity

Total

Cost

Total

Market

LCM

Valuation

AA

100

$ 3,000 (1)

$ 2,600 (2)

$ 2,600

BB

150

12,000 (3)

12,000 (3)

12,000

CC

200

20,000 (4)

20,800 (5)

20,000

$34,600

Calculations:

(1) 100 units @ $30 per unit = $3,000

(2) 100 units @ $26 per unit = $2,600

(3) 150 units @ $80 per unit = $12,000

(4) 200 units @ $100 per unit = $20,000

(5) 200 units @ $104 per unit = $20,800