M6–16

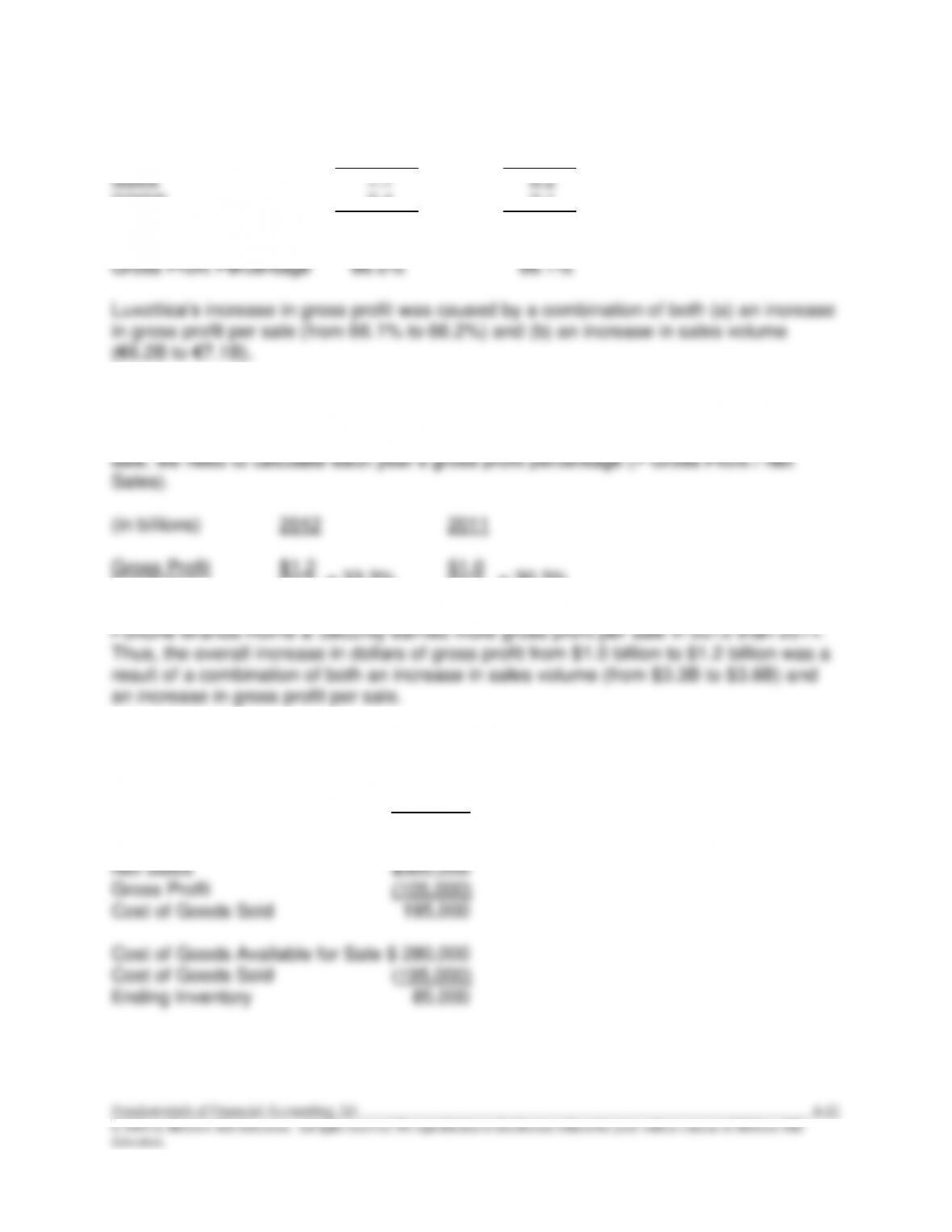

(in billions of euro)

2012 2011

COGS 2.4 2.1

Gross Profit 4.7 4.1

M6–17

To determine whether Fortune Brands Home & Security earned more gross profit per

Net Sales $3.6 $3.3

M6–18

Net Sales $300,000

Gross Profit Percentage 35%

Gross Profit 105,000

= 33.3%

= 30.3%

6-12 Solutions Manual

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO EXERCISES

E6–1

Financial Statement

Type of Company

Inventory

B/S

MC

Sales Revenue

I/S

MC

Cost of Goods Available for Sale

Not

MC

Service Revenue

I/S

SC

E6-2

Sales – CGS = GP

$4.0 – CGS = $2.4 (in billions)

E6–3

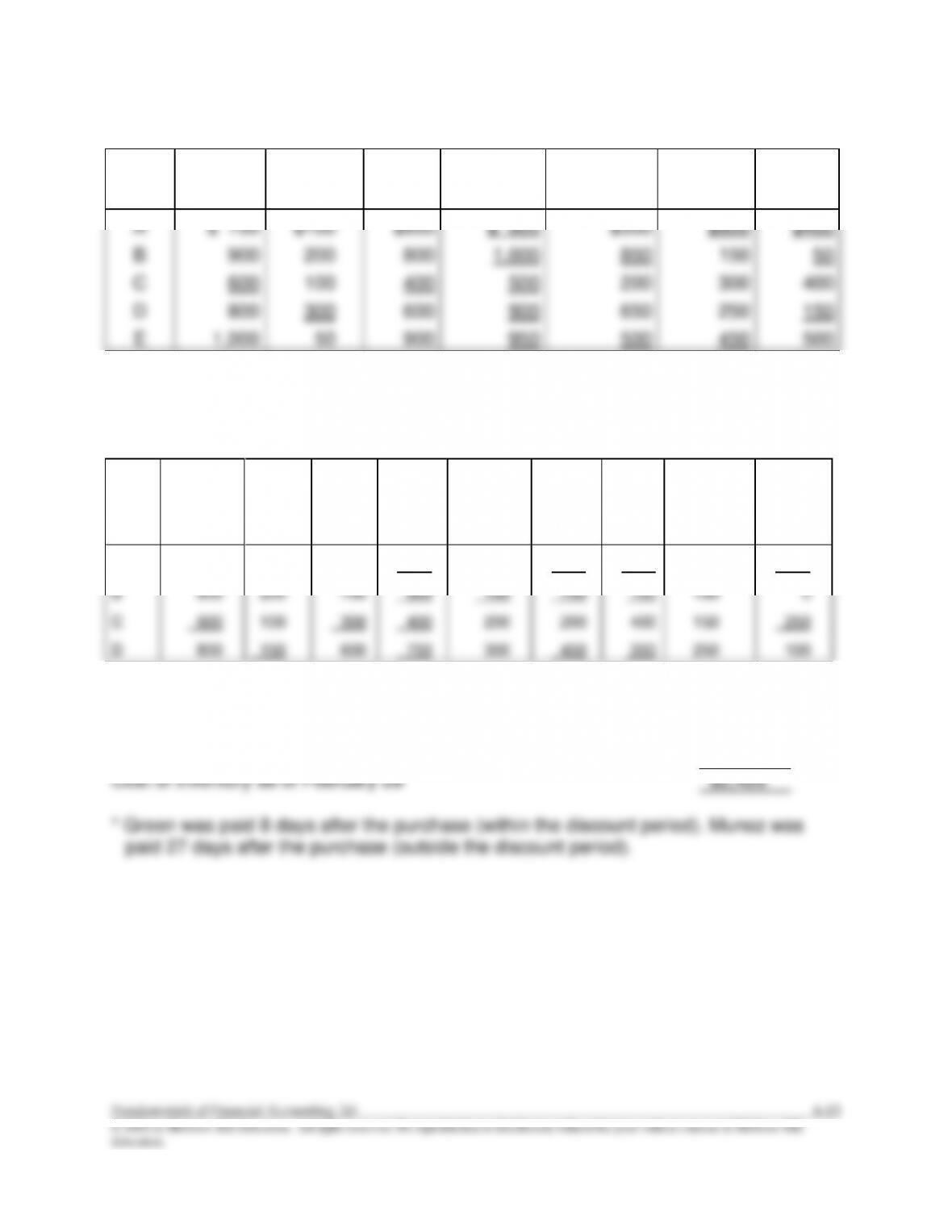

(Underscore for missing amounts only.)

Case

Beg.

Inventory

Purchases

Cost of

Goods Sold

Ending

Inventory

(perpetual)

Ending Inventory

(as counted)

Shrinkage

A

$100

$700

$300

$500

$420

$80

B

200

800

850

150

150

0

C

150

500

200

450

440

10

D

260

600

650

210

200

10

E6–4

(amounts in billions)

Beginning inventory

$ 5.1

+ Purchases

16.9

–Cost of Goods Sold

(16.5)

Ending inventory, prior to shrinkage adjustment

5.5

Ending inventory, as reported (after shrinkage adjustment)

(5.3)

Shrinkage

$ 0.2

E6-5

(Underlined items are the missing amounts.)

Cases

Sales

Revenue

Beg.

Inventory

Purch.

Cost of

Goods

Available

Cost of

Goods Sold

Cost of

Ending

Inventory

Gross

Profit

A

$ 700

$100

$800

$ 900

$300

$600

$400

B

900

200

800

1,000

850

150

50

C

600

100

400

500

200

300

400

D

800

300

600

900

650

250

150

E

1,000

50

900

950

500

450

500

E6-6

(Underscore for missing amounts only.)

Case

Sales

Revenue

Beg.

Inven-

tory

Pur-

chases

Total

Avail-

able

Ending

Inventory

Cost of

Goods

Sold

Gross

Profit

Operating

Expenses

Income

from

Oper-

ations

A

$ 800

$100

$700

$800

$500

$300

$500

200

$300

B

900

200

700

900

150

750

150

150

0

C

600

100

300

400

200

200

400

150

250

D

800

150

600

750

300

450

350

250

100

E6-7

Purchases ($1,200 + $900 + $350)

$2,450

Less: Purchase discount from Green ($1,200 x 2%)

(24)*

Cost of inventory as of February 28

$2,426

E6-8

Jan. 6

Inventory ………………………………………………………….………

1,200

Accounts Payable …………………………………………………

1,200

Jan. 6

Inventory ………………………………………………………….………

900

Accounts Payable …………………………………………………

900

Jan. 14

Accounts Payable ……………………………………………..………

1,200

Inventory ($1,200 x 2%) …………………………………………

24

Cash ($1,200 x 98%) ……………………………………..………

1,176

Feb. 2

Accounts Payable ……………………………………………..………

900

Cash …………………………………………………………..………

900

Feb. 28

Inventory ………………………………………………………….………

350

Accounts Payable …………………………………………………

350

E6-9

Purchases ($4,100 + $1,000)

$5,100

Less: Purchase returns

(1,100)

Less: Purchase discount from Diamond [($4,100 – $1,100) x 2%]

(60)*

Cost of inventory as of June 30

$3,940

E6–10

June 3

Inventory ………………………………………………………….………

4,100

Accounts Payable …………………………………………………

4,100

June 5

Accounts Payable ……………………………………………..………

1,100

Inventory …………………………………………………….…

1,100

June 6

Inventory …………………………………………………………..………

1,000

Accounts Payable …………………………………………………

1,000

June 11

Accounts Payable ($4,100 – $1,100) …………………….…….

3,000

Cash ($3,000 x 98%) ……………………………………..………

2,940

Inventory ($3,000 x 2%) …………………………………………

60

June 22

Accounts Payable ……………………………………………..………

1,000

Cash …………………………………………………………..………

1,000

E6–11

Req. 1

PC Mall’s shipping terms are FOB destination because the company retains control of

the inventory until it arrives at the customer’s location.

Req. 2

December

E6–12

Sales Revenue ($100 + $80 + $50)……………………………………………… $230

Sales Discount ($100 collected from Wizard Inc. x 2%) ………………….. (2)*

E6–13

Jan. 6

Accounts Receivable …………………………………………………

100

Sales Revenue …………………………………………….………

100

Cost of Goods Sold ……………………………………………………

70

Inventory …………………………………………………….…

70

Jan. 6

Accounts Receivable …………………………………………………

80

Sales Revenue …………………………………………….………

80

Cost of Goods Sold ……………………………………………………

60

Inventory …………………………………………………….…

60

Jan. 14

Cash ($100 x 98%) …………………………………………….………

98

Sales Discounts ($100 x 2%) ……………………………….………

2

Accounts Receivable …………………………………….………

100

Feb. 2

Cash ……………………………………………………………….………

80

Accounts Receivable …………………………………….………

80

Feb. 28

Accounts Receivable …………………………………………………

50

Sales Revenue …………………………………………….………

50

Cost of Goods Sold ……………………………………………………

30

Inventory …………………………………………………….…

30

E6–14

Sales Revenue ($1,000 + $5,000 + $3,000) ………………………………….. $9,000

E6–15

July 12

Cash ……………………………………………………………….………

1,000

Sales Revenue …………………………………………….………

1,000

Cost of Goods Sold ……………………………………………………

600

Inventory …………………………………………………….…

600

July 15

Accounts Receivable …………………………………………………

5,000

Sales Revenue …………………………………………….………

5,000

Cost of Goods Sold ……………………………………………………

3,500

Inventory …………………………………………………….…

3,500

July 20

Accounts Receivable …………………………………………………

3,000

Sales Revenue …………………………………………….………

3,000

Cost of Goods Sold ……………………………………………………

1,900

Inventory …………………………………………………….…

1,900

July 23

Cash ($5,000 x 97%) ………………………………………….………

4,850

Sales Discounts ($5,000 x 3%) …………………………….………

150

Accounts Receivable …………………………………….………

5,000

Aug. 25

Cash ……………………………………………………………….………

3,000

Accounts Receivable …………………………………….………

3,000

E6–16

Sales Revenue ($400 + $4,000 + $6,000) …………………………………….. $10,400

Sales Returns and Allowances (1/10 x $6,000 from Nancy’s) ……………. (600)*

Sales Discounts (9/10 x $6,000 x 3% from Nancy’s) ………………………… (162)**

E6–17

Nov. 20

Cash …………………………………………………………………….…

400

Sales Revenue ………………………………………………….…

400

Cost of Goods Sold ……………………………………………………

300

Inventory …………………………………………………………..…

300

Nov. 25

Accounts Receivable …………………………………………………

4,000

Sales Revenue …………………………………………………..…

4,000

Cost of Goods Sold ………………………………………………….…

2,500

Inventory …………………………………………………………..…

2,500

Nov. 28

Accounts Receivable …………………………………………………

6,000

Sales Revenue …………………………………………….………

6,000

Cost of Goods Sold ……………………………………………………

4,000

Inventory …………………………………………………….…

4,000

Nov. 29

Sales Returns and Allowances (1/10 x $6,000) ………………

600

Accounts Receivable ……………………………………..………

600

Inventory ………………………………………………………….………

400

Cost of Goods Sold ………………………………………………

400

($4,000 x 1/10 = $400)

Dec. 6

Cash [($6,000 − $600) x 97%] ……………………………..………

5,238

Sales Discounts ($5,400 x 3%) …………………………….………

162

Accounts Receivable ($6,000 – $600) ………………………

5,400

Dec. 30

Cash ……………………………………………………………….………

4,000

Accounts Receivable ……………………………………..………

4,000

E6–18

Transaction

July 12

July 15

July 20

July 21

July 23

TOTALS

Sales Revenue

+300

+5,000

NE

+2,000

NE

+7,300

Sales Returns & Allow.

NE

NE

NE

NE

+1,000

+1,000

Sales Discounts

NE

NE

+150

NE

NE

+150

Net Sales

+300

+5,000

−150

+2,000

−1,000

+6,150

Cost of Goods Sold

+160

+3,000

NE

+1,200

− 600

+3,760

Gross Profit

+140

+2,000

−150

+800

− 400

+2,390

E6–19

Req. 1

Accounts Receivable …………………………………………………

800

Sales Revenue …………………………………………….………

800

Cost of Goods Sold ……………………………………………………

500

Inventory …………………………………………………….…

500

Req. 2

Cash ($800 x 98%) …………………………………………….………

784

Sales Discounts ($800 x 2%) ……………………………….………

16

Accounts Receivable …………………………………….………

800

Req. 3

Cash ……………………………………………………………….………

800

Accounts Receivable …………………………………….………

800

Req. 4

Gross profit

percentage

=

Gross profit

x 100

=

284*

x100

=

36.2%

Net Sales

784**

*$284 = $800 – $500 – (2% x $800)

** $784 = $800 – (2% x $800)

E6–20

(Boxed items are the missing amounts.)

Case A Case B Case C

E6–21

Req. 1 MYSTERY INCORPORATED

Income Statement

For the Year Ended December 31

Sales Revenue ($240,000 + $42,000) …………… $282,000

Sales Returns and Allowances …………………….. (7,000)