Chapter Outline

Teaching Notes

C. Sales on Account and Sales Discounts

1. Sales discount––A sales price reduction given to

customers for prompt payment of their account balance.

2. Sales discount is calculated after taking into account any

sales returns and allowances.

3. When the customer pays, Cash is increased with a debit,

Sales Discounts, a contra revenue account, is increased

with a debit, and Accounts Receivable is reduced with a

credit.

4. Summary of Sales-Related Transactions

Summarized in Exhibit 6.7

a. Sales returns and allowances and sales discounts are

recorded using contra-revenue accounts.

b. Net Sales = Sales Revenues – Sales Returns and

Allowances – Sales Discounts.

D. Inventory Purchases and Sales Transactions Compared

Compared in Exhibit 6.8

1. Purchase transactions affect only balance sheet accounts.

The “Spotlight on Financial

2. Sales transactions affect accounts on both the balance

sheet and income statement.

Reporting” feature addresses

customer theft.

III. Evaluate the Results

LO 6–5 Prepare and analyze a merchandiser’s multistep income statement.

A. Gross Profit Analysis

1. Multistep income statement––Presents important

subtotals, such as gross profit, to help distinguish core

operating results from other, less significant items that

affect net income.

Illustrated in Exhibit 6.9

a. Expenses are subtracted from sales to arrive at net

income.

b. This format separates revenues and expenses that

related to core operations from all other (peripheral)

items that affect net income.

c. For merchandisers, a key measure is the amount of

profit earned over the cost of goods sold.

2. Gross profit (gross margin or simply margin)––Net sales

minus cost of goods sold; it is a subtotal, not an account.

3. Category called Selling, General, and Administrative

Expenses includes a variety of operating expenses, such

as wages, utilities, advertising, rent, and the costs of

delivering merchandise to customers.

4. Selling, General, and Administrative Expenses are

subtracted from gross profit to yield Income from

Operations, which is a measure of the company’s income

from regular operating activities before considering the

effects of interest, income taxes, and any nonrecurring

items.

Chapter Outline

Teaching Notes

B. Gross Profit Percentage

1. Gross profit percentage––A ratio indicating the

percentage of profit earned on each dollar of sales, after

considering the cost of products sold.

a. Gross profit percentage = ((Net Sales – COGS) ÷ Net

Sales) × 100.

b. Measures the percentage of profit earned on each

dollar of sales, after considering the cost of products

sold.

c. A higher gross profit ratio means that greater profit is

available to cover operating and other expenses.

2. Comparing Gross Profit Percentages

b. Gross profit percentages can vary greatly between

companies

a. Gross profit percentages can vary across industries.

LO 6–S1 Record inventory transactions in a periodic system.

IV. Recording Inventory Transactions in a Periodic System

A. Inventory Purchases—Purchases of merchandise inventory

are recorded in the Purchases account (with a debit).

B. Record Sales – No Cost of Goods Sold entry.

C. Record End-of-Period Adjustments

a. Count the number of units on hand, compute the dollar

valuation of the ending inventory, and compute and

record the cost of goods sold.

b. Transfer beginning inventory and net purchases to cost of

goods sold.

c. Adjust the cost of goods sold by subtracting the amount

of ending inventory still on hand (recognize that not all

goods were sold).

Supplemental Enrichment Activities

Note: These activities would be suitable for individual or group activities.

1. Handout 6–1

Use Handout 6–1 for an in-class activity designed to review the preparation of journal entries for

purchase transactions under a perpetual inventory system. The solution follows the handout master.

2. Handout 6–2

Use Handout 6–2 for an in-class activity designed to review the preparation of journal entries for

sales transactions under a perpetual inventory system. The solution follows the handout master.

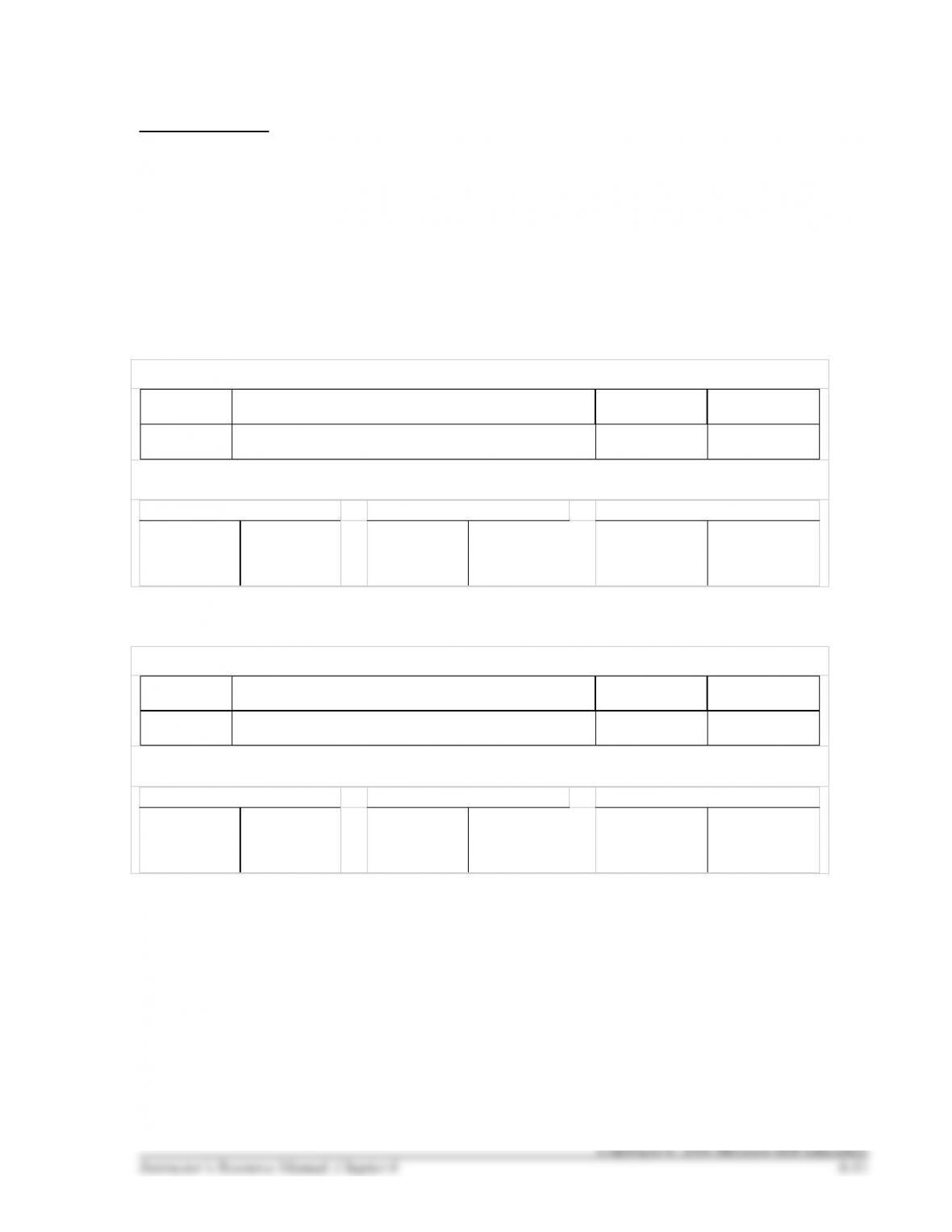

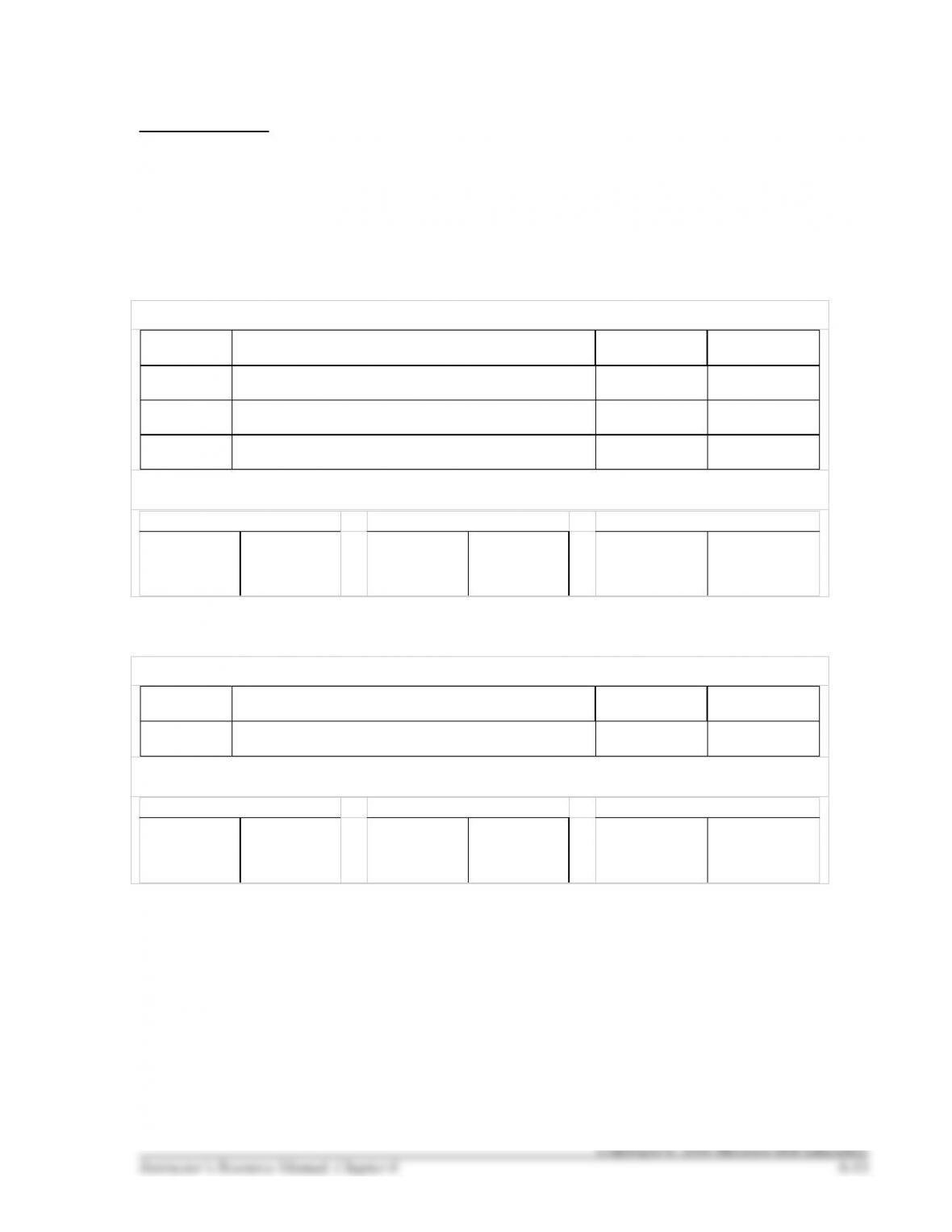

HANDOUT 6–1

PURCHASE TRANSACTIONS UNDER A PERPETUAL INVENTORY SYSTEM

Hamm Manufacturing Corp. uses a perpetual inventory system. The following activities occurred during

February 2016. Prepare a journal entry for ensure that the basic accounting equation balances for each

transaction.

On February 2, Hamm purchased $40,000 worth of inventory, on credit terms 3/10 n/30.

Prepare the required journal entries.

Debit and credit the accounts affected

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

On February 10, Hamm paid for the inventory, taking advantage of all available discounts.

Debit and credit the accounts affected

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

HANDOUT 6–1 SOLUTION

PURCHASE TRANSACTIONS UNDER A PERPETUAL INVENTORY SYSTEM

Hamm Manufacturing Corp. uses a perpetual inventory system. The following activities occurred during

February 2016. Prepare a journal entry for ensure that the basic accounting equation balances for each

transaction.

On February 2, Hamm purchased $40,000 worth of inventory, on credit terms 3/10 n/30.

Debit and credit the accounts affected

Feb. 2

Inventory

40,000

Accounts Payable

40,000

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Inventory

+40,000

Accounts

Payable

+40,000

On February 10, Hamm paid for the inventory, taking advantage of all available discounts.

Debit and credit the accounts affected

Feb. 10

Accounts Payable

40,000

Cash

38,800

Inventory

1,200

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

–38,800

Accounts

–40,000

Inventory

–1,200

Payable

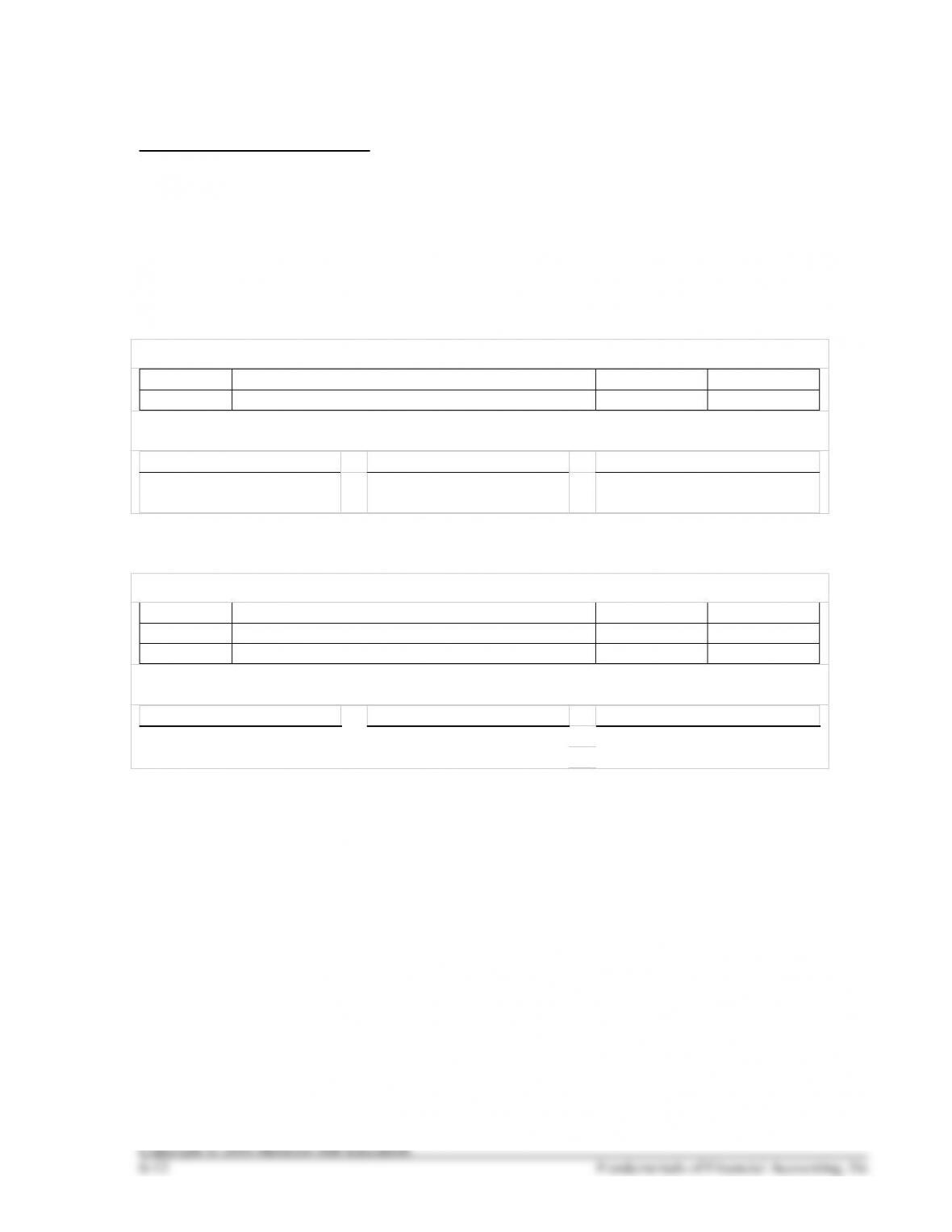

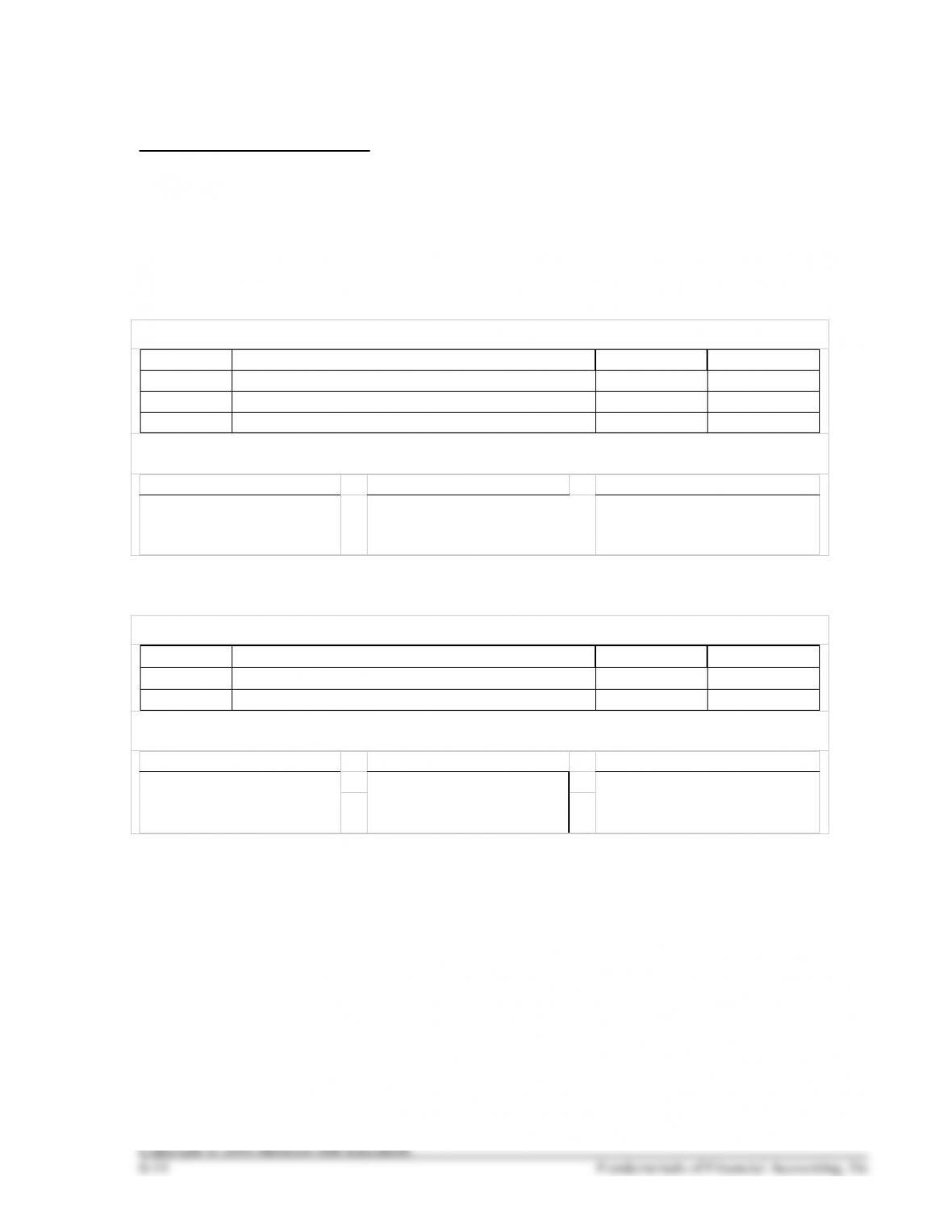

HANDOUT 6–2

SALES TRANSACTIONS UNDER A PERPETUAL INVENTORY SYSTEM

Gooddeal Inc. uses a perpetual inventory system. The following activities occurred during February 2016.

Prepare a journal entry for ensure that the basic accounting equation balances for each transaction.

On March 3, Gooddeal sold inventory costing $2,000 for $2,500, terms 2/10, n/30.

Debit and credit the accounts affected

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Gooddeal’s customer paid for the merchandise on March 6, taking advantage of the permitted discount.

Debit and credit the accounts affected

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

HANDOUT 6–2 SOLUTION

SALES TRANSACTIONS UNDER A PERPETUAL INVENTORY SYSTEM

Gooddeal Inc. uses a perpetual inventory system. The following activities occurred during February 2016.

Prepare a journal entry for ensure that the basic accounting equation balances for each transaction.

On March 3, Gooddeal sold inventory costing $2,000 for $2,500, terms 2/10, n/30.

Debit and credit the accounts affected

Mar. 3

Accounts Receivable

2,500

Sales

2,500

Cost of Goods Sold

2,000

Inventory

2,000

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Accounts

+2,500

Sales

+2,500

Receivable

Inventory

–2,000

Cost of

Goods Sold

–2,000

Gooddeal’s customer paid for the merchandise on March 6, taking advantage of the permitted discount.

Debit and credit the accounts affected

Mar. 6

Cash [2,500 × 98%]

2,450

Sales Discounts [2,500 × 2%]

50

Accounts Receivable

2,500

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

+2,450

Sales

–50

Accounts

Receivable

–2,500

Discounts