Fundamentals of Financial Accounting, 5/e 5-21

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO GROUP A PROBLEMS

PA5–1

Req. 1

a. Weakness – By not issuing a receipt for all cash sales, the company does not

adequately document procedures performed. This could allow a cashier to take

cash rather than place it in the cash register.

b. Strength – The cash count sheet is a useful means of documenting the

PA5–2

Req. 1 MARTIN COMPANY

Bank Reconciliation

At May 31

Bank Statement

Company’s Books

Ending balance per bank

statement ……………………

$14,480

Ending balance per Cash

account ……………………..

$19,400

Additions:

Additions:

5/29 Deposit in transit …

6,000

Interest earned …………

120

20,480

19,520

Deductions:

Deductions:

Bank service charges …

$ 60

Outstanding check #305

1,300

NSF check ……………….

280

340

Up–to-date cash balance ..

$19,180

Up–to-date cash balance ..

$19,180

(1) Cash …………………………………………………………………….. 120

(2) Accounts Receivable ………………………………………………… 280

(3) Office Expenses ………………………………………………………. 60

Cash …………………………………………………………….. 60

Bank service charges deducted from bank statement.

PA5–3

Req. 1

Comparison of deposits listed in the Cash account with deposits listed on the bank statement

reveals a $13,000 deposit in transit on December 31.

Req. 2

Comparison of the checks cleared on the bank statement with checks written in December

reveals two outstanding checks at the end of December ($4,500 + $150 = $4,650).

(1) Cash …………………………..…………………………………………….. 50

(2) Office Expenses …………………………………………………………….. 150

(3) Accounts Receivable ………………………………………………………. 300

Cash ………………………………………………………………….. 300

PA5–4

Req. 1

a. Petty Cash …………………………………………………………….. 250

Cash ………………………………………………………….. 250

b. No journal entry. Journal entries are made only when the petty cash fund is

established, replenished, increased, or eliminated.

c. No journal entry.

Fundamentals of Financial Accounting, 5/e 5-25

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO GROUP B PROBLEMS

PB5–1

Req. 1

a. Strength – By documenting procedures, the company reduces the risk of failing

to record (or recording twice) sales transactions.

b. Strength – Segregating the duties of depositing cash from recording cash helps

reduce the risk of embezzlement, and it provides an opportunity to ensure that

the cash deposited (debit to Cash) equals the credits to customer accounts

PB5–2

Req. 1 TONY COMPANY

Bank Reconciliation

At February 29

Bank Statement

Company’s Books

Ending balance per bank

statement ……………………

$30,640

Ending balance per Cash

account ………………………

$37,450

Additions:

Additions:

2/28 Deposit in transit …

7,800

Interest earned ………….

150

38,440

37,600

Deductions:

Deductions:

Bank service charges …

$ 40

Outstanding check #106

1,200

NSF check ………………

320

360

Up–to-date cash balance ..

$37,240

Up–to-date cash balance …

$37,240

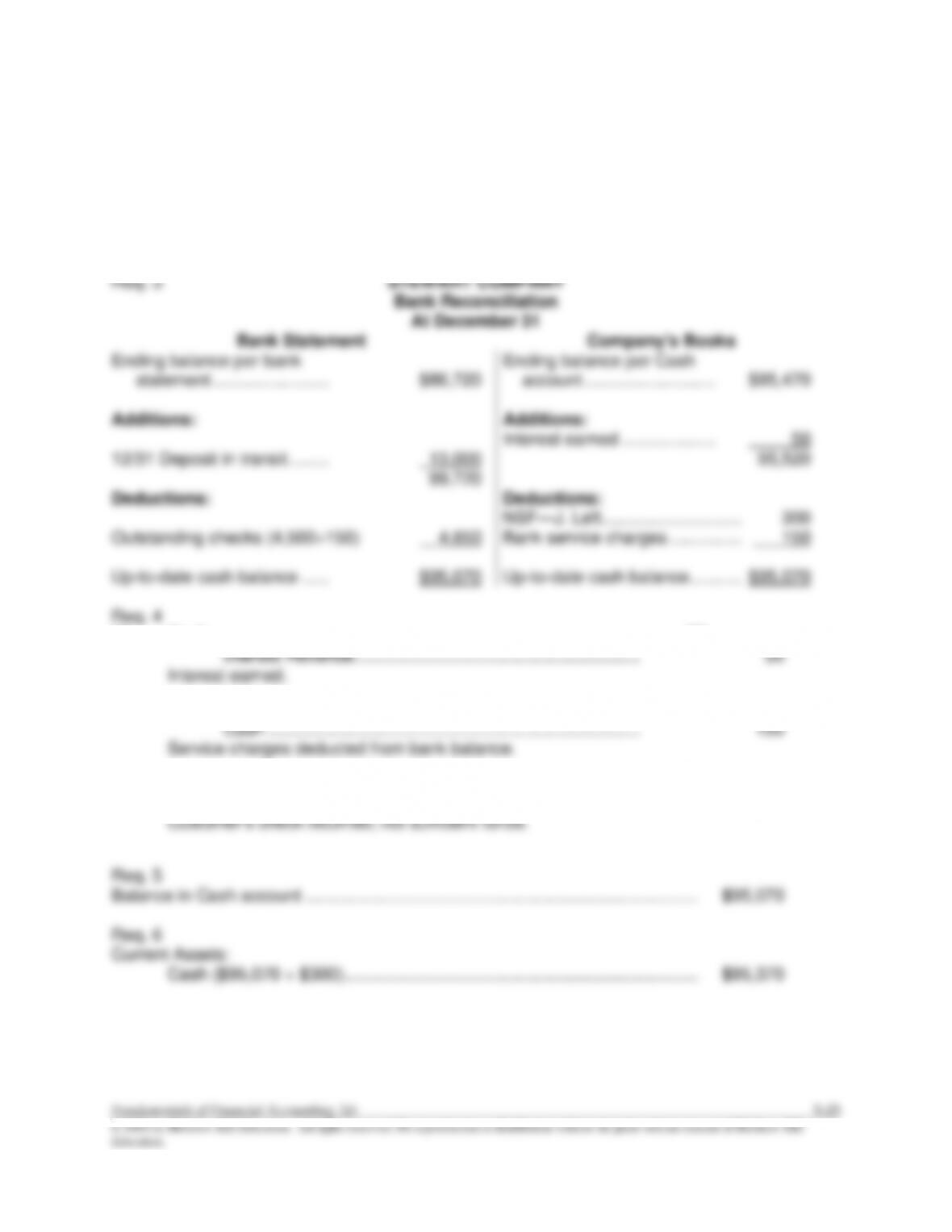

Req. 2

(1) Cash …………………………………………………………………….. 150

(2) Accounts Receivable ………………………………………………… 320

(3) Office Expenses ………………………………………………………. 40

Cash …………………………………………………………….. 40

PB5–2 (continued)

Req. 3

Balance in Cash account …………………………………………………………. $37,240

Req. 4

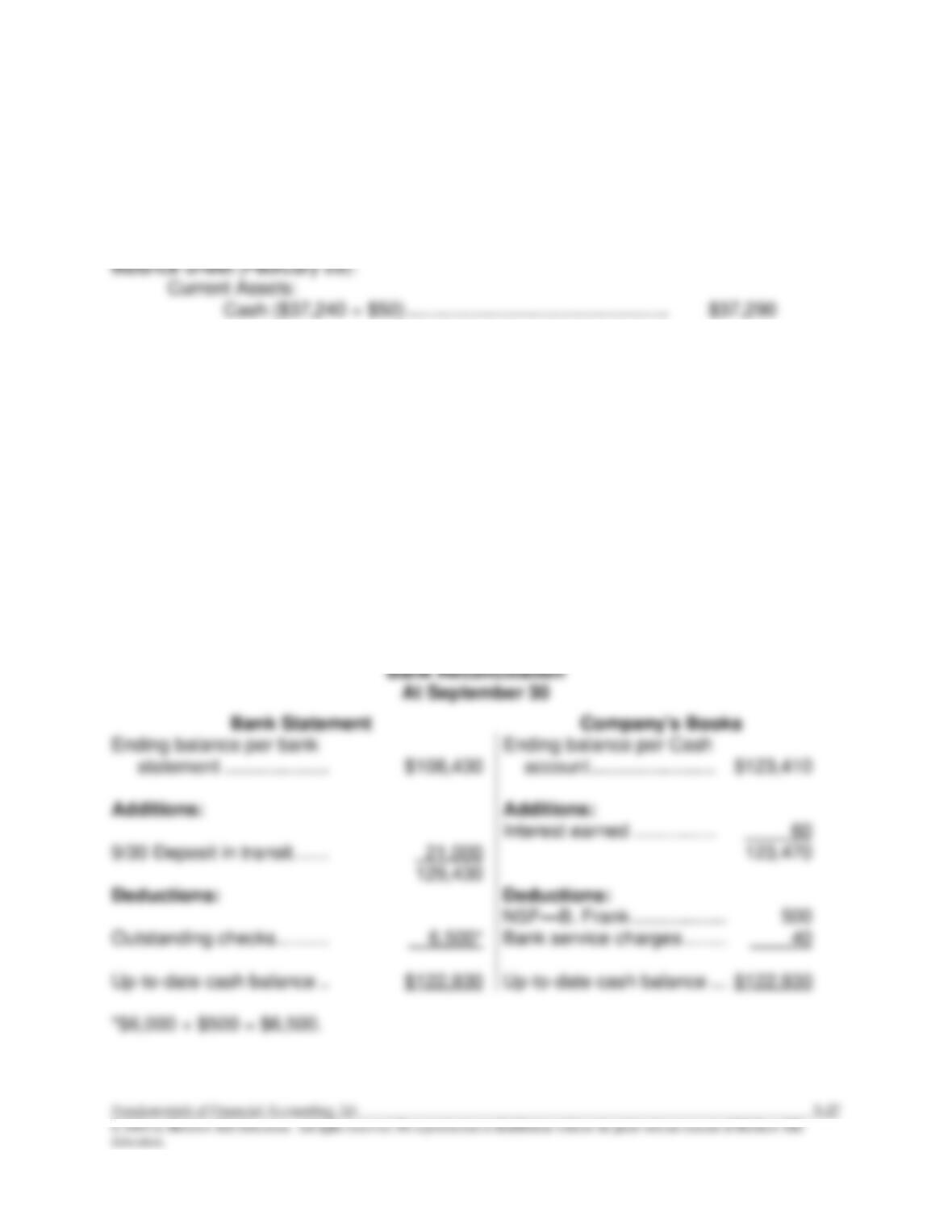

PB5–3

Req. 1

Comparison of deposits listed in the Cash account with deposits listed on the bank

statement reveals a $21,000 deposit in transit on September 30.

Req. 2

Comparison of the checks cleared on the bank statement with checks written in

September reveals two outstanding checks at the end of September ($500 + $6,000 =

$6,500).

Req. 3 TERRICK COMPANY

5-28 Solutions Manual

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

PB5–3 (continued)

Req. 4

(1) Cash …………………………………………………………………….. 60

(2) Office Expenses ………………………………………………………. 40

(3) Accounts Receivable ………………………………………………… 500

Cash …………………………………………………………….. 500

PB5–4

Req. 1

a. Petty Cash …………………………………………………………….. 300

Cash ………………………………………………………….. 300

b. No journal entry. Journal entries are made only when the petty cash fund is

established, replenished, increased, or eliminated.

($400), and the Treasury bills ($500) that were purchased within 90 days of maturity for

a total of $1,900. The $750 of cash set aside for legal reasons would be excluded from

5-30 Solutions Manual

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWER TO COMPREHENSIVE PROBLEM

C5–1

Req. 1

1/1 Cash …………………………………………………………….. 2,500

Accounts Receivable ………………………………….. 2,500

1/2 Accounts Payable …………………………..………………. 4,000

Cash ………………………………………………………… 4,000