E5–3 (continued)

Req. 2

Because the supervisor was responsible for handling the cash, preparing the cash

E5–4

Req. 1

a. Document procedures

b. Segregate duties / Document procedures

E5–4 (continued)

Req. 3

Because receiving reports were not prepared, there was no way to independently verify

that amounts charged by suppliers were for goods that had been delivered to authorized

site.

E5–5

Req. 1

HILLS COMPANY

Bank Reconciliation

June 30

Bank Statement

Company’s Books

Ending balance per bank

statement………………….

$6,070

Ending balance per Cash

account………………………

$6,400

Additions:

Additions:

Deposit in transit…………….

1,000*

None

7,070

6,400

Deductions:

Deductions:

Outstanding checks…………

700

Bank service charge……

30

Up–to-date cash balance….

$6,370

Up–to-date cash balance……

$6,370

*$19,000 – $18,000 = $1,000.

Req. 2

Office Expenses …………………………………………………………….. 30

Cash ……………………………………………………………………. 30

To record bank service charges.

Req. 3

The updated cash balance after the reconciliation entry is ($6,400 – $30) $6,370.

Req. 4

Balance sheet (June 30):

Current assets:

Cash ($6,370 + $300) ………………………………………………… $6,670

E5–6

Req. 1 CADIEUX COMPANY

Bank Reconciliation

September 30

Bank Statement

Company’s Books

Ending balance per bank

statement ……………………

$ 230

Ending balance per Cash

account ……………………..

$2,650

Additions:

Additions:

9/30 Deposit in transit ……

2,500

EFT deposit …………….

150

2,730

2,800

Deductions:

Deductions:

Bank service charges …

$ 20

9/28 Outstanding check #104

50

NSF check ………………

100

120

Up–to-date cash balance ..

$2,680

Up–to-date cash balance ..

$2,680

(1) Cash …………………………………………………………………………. 150

(2) Office Expenses ……………………………………………………….….. 20

(3) Accounts Receivable …………………………………………………….. 100

Cash …………………………………………………………………. 100

E5–7

Balance Sheet (September 30): in millions

Current Assets:

Cash and Cash Equivalents ($410 + $970) …………………………... $1,380

E5–8

Req. 1

Cash and Cash Equivalents:

Cash ………. …………………………………………………………………………….. $10

Petty Cash..………………………………………………………………………………. 5

Cash Equivalents …………………………..………………………………………….. 15

Total Cash and Cash Equivalents …………………………..…………… 30

Req. 2

E5–9

Req. 1

Jan. 1 Petty Cash……………………………………………………….. 100

Cash ………………………………………………………… 100

Req. 2

E5–10

Req. 1

Jan. 1 Petty Cash……………………………………………………….. 200

Cash ………………………………………………………… 200

Req. 2

ANSWERS TO COACHED PROBLEMS

CP5–1

Req. 1

a. Strength – Use of a cash register restricts access to a valuable asset (cash), and

issuance of a receipt helps to document the procedure of collecting cash.

b. Strength – The cash count sheet is a useful means of documenting the

procedure performed (cash count).

c. Strength – Independent verification by the manager helps to ensure the accuracy

CP5–2

Req. 1 KMaxx Company

Bank Reconciliation

At April 30

Bank Statement

Company’s Books

Ending balance per bank

statement ……………………

$5,775

Ending balance per Cash

account ……………………..

$ 6,200

Additions:

Additions:

4/28 Deposit in transit …

500

–0-

6,275

6,200

Deductions:

Deductions:

EFT payment …………..

$200

Bank error * ……………….

100

NSF check ……………….

100

Outstanding check #105

300

Bank service charges …

25

325

Up–to-date cash balance ..

$5,875

Up–to-date cash balance ..

$5,875

* Check number 104 was written and recorded in the accounting records for $1,100 but

was incorrectly cleared by the bank for $1,000. Therefore the bank did not take out

enough funds and a $100 deduction is required on the bank’s side of the bank

reconciliation to allow for the bank’s error.

Req. 2

(1) Accounts Payable …………………………………………………….. 200

(2) Accounts Receivable ………………………………………………… 100

(3) Office Expenses ………………………………………………………. 25

Cash …………………………………………………………….. 25

CP5–3

Req. 1

Comparison of deposits listed in the Cash account with deposits listed on the bank

statement reveals a $5,000 deposit in transit on August 31.

Req. 2

Comparison of the checks cleared on the bank statement with (a) outstanding checks

from July, and (b) checks written in August reveals two outstanding checks at the end of

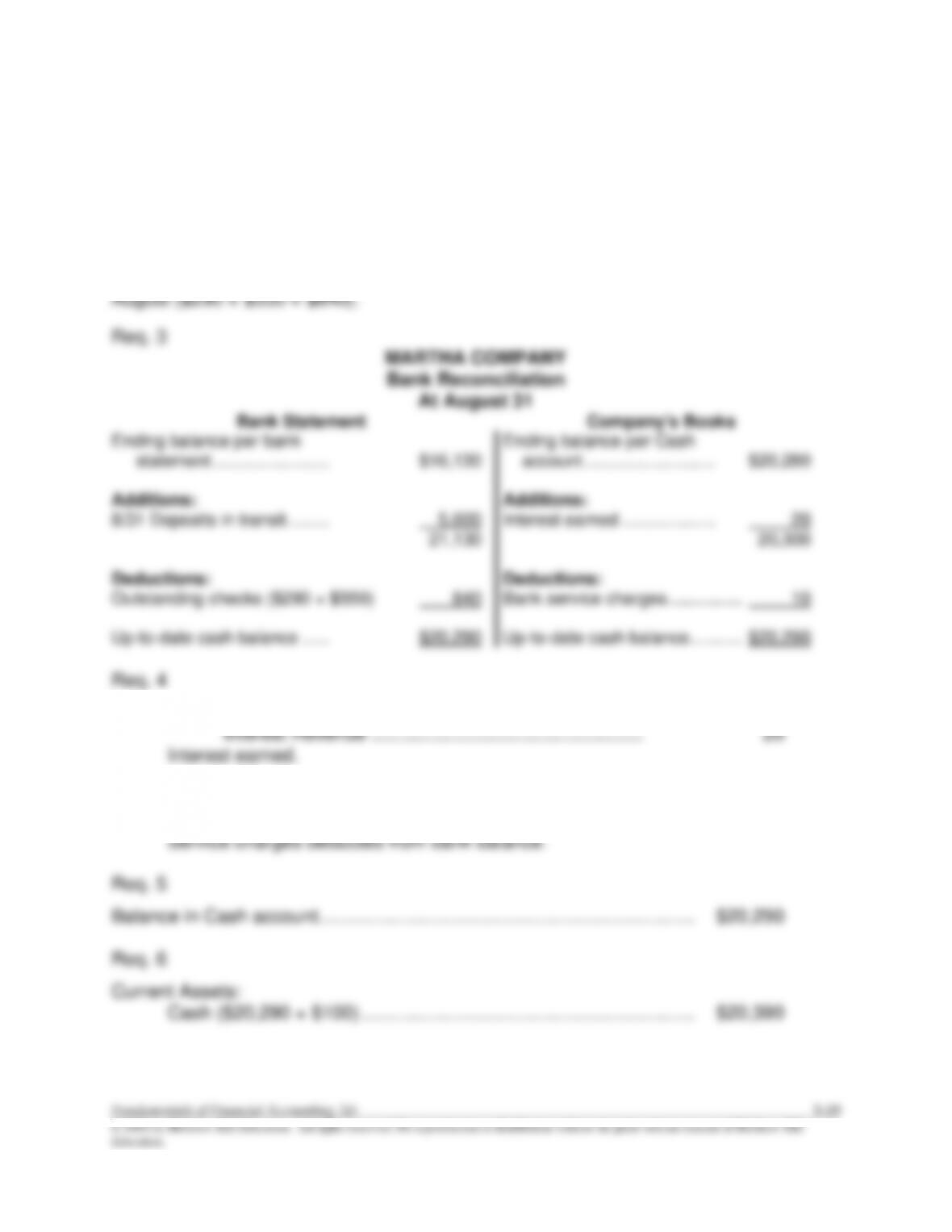

(1) Cash …………………………………………………………………….. 20

(2) Office Expenses ………………………………………………………. 10

Cash …………………………………………………………….. 10

CP5–4

Req. 1

a. Petty Cash …………………………………………………………….. 300

Cash ………………………………………………………….. 300

b. No journal entry. Journal entries are made only when the petty cash fund is

established, replenished, increased, or eliminated.

c. No journal entry.