Chapter Outline

Teaching Notes

3. Cash Paid to Reimburse Employees (Petty Cash)

a. Petty cash fund—A system used to reimburse

employees for expenditures they have made on behalf

of the organization.

i. Acts as a control by establishing a limited amount

of cash to use for specific types of expenses.

ii. Rather than transfer funds from a general bank

account to another special account at the bank, the

company removes cash from its general bank

account to hold at its premises in a locked cash box

b. The company’s petty cash custodian is responsible for

operating the petty cash fund; he or she should be

supervised and the petty cash fund should be subject

to surprise audits.

The “Spotlight on Controls”

feature addresses the use of

Pcards for small dollar

transactions

III. Cash Reporting

The balance in a company’s cash records usually differs from

the balance in the bank’s records for a variety of valid reasons

LO 5-4 Perform the key control of reconciling cash to bank statements.

A. Bank Statement

1. Bank reconciliation––An internal report prepared to

verify the accuracy of both the bank statement and the

cash accounts of a business or individual.

2. Checks cleared—The payee presents the check to a

financial institution, which contacts the check writer’s

bank, which in turn withdraws the amount of the check

from the check writer’s account and reports it as a

deduction on the bank statement; the check has then

cleared the bank.

A bank statement is

illustrated in Exhibit 5.7

3. Deposits made—Deposits are listed on the bank

statement in the order in which the bank processes them.

4. Other transactions—The balance in a bank account can

change for a variety of other reasons.

a. The bank statement is presented from the bank’s point

of view; the amounts in a company’s bank account are

liabilities to the bank.

b. Increases are reported as credits on the bank

statement.

c. Amounts that are removed from a bank account are

reported as debits on the bank statement.

B. Bank Reconciliation

1. Company’s records can differ from bank’s statement of

account for two basic reasons:

Reconciling differences are

listed in Exhibit 5.8

a. The company has recorded some items that the bank

doesn’t know about at the time it prepares the

statement of account.

b. The bank has recorded some items that the company

doesn’t know about until the bank statement arrives.

Chapter Outline

Teaching Notes

2. Causes of differences:

a. Bank errors—If you discover a bank error, you’ll need

to ask the bank to correct its records, but you should

not change yours.

b. Time lags—Common:

i. Deposit in transit—Time lag occurs when you

make a deposit after the bank’s normal business

hours. You know you’ve made the deposit, but

your bank doesn’t know until it processes the

deposit the next day.

ii. Outstanding check—Occurs when you write and

mail a check to a company, but your bank doesn’t

find out about it until that company deposits the

check in its own bank, which then notifies your

bank.

c. Interest deposited—You probably do not know the

amount of interest until you read your bank statement.

d. Electronic funds transfer (EFT)—Occasionally funds

may be transferred into or out of your account without

your knowledge.

e. Service charges—Amounts the bank charges you for

processing your transactions.

f. NSF (not sufficient funds) checks––Another name

for bounced checks; they arrive when the check writer

(your customer) does not have sufficient funds to

cover the amount of the check.

i. Because the bank increased your account when

you first deposited the check, the bank will

decrease your account when it discovers the

deposit was not valid.

ii. You will need to reduce the Cash balance by the

amount of these bounced checks (plus any

additional bank charges), and you’ll have to try to

collect the amount from the check writer.

g. Your errors—These are mistakes that you’ve made or

amounts that you haven’t yet recorded in your

checkbook.

3. Bank Reconciliation Illustrated

Illustrated in Exhibit 5.9

a. To prepare the bank reconciliation, the entries in the

Cash account are compared to the bank statement with

the following goals:

✓ Supplemental Enrichment

Activity (Activity) #1

✓ Activity #2

i. Identify the deposits in transit.

ii. Identify the outstanding checks.

iii. Record other transactions on the bank statement

and correct your errors.

Chapter Outline

Teaching Notes

b. Journal entries that will bring the Cash account to that

balance are then prepared and recorded.

i. Entries on the Bank Statement side of the bank

reconciliation do not need to be adjusted because

they will work out automatically when the bank

processes them next month.

The “Spotlight on Controls”

ii. Only the items on the Company’s Books side of

the bank reconciliation need to be recorded in the

company’s records.

feature addresses frauds

committed by “trustworthy”

employees.

LO 5-5 Explain the reporting of cash.

C. Reporting Cash—Cash, as reported on the balance sheet,

includes: cash deposited with banks, petty cash on hand, and

cash equivalents.

1. Cash––Money or any instrument that banks will accept

for deposit and immediate credit to a company’s account,

such as a check, money order, or bank draft.

2. Cash equivalents––Short-term, highly liquid investments

purchased within three months of maturity; equivalent to

cash because they are both readily convertible to known

amounts of cash and so near to maturity that there is little

risk their value will change.

D. Restricted cash––Not available for general use but rather

restricted for a specific purpose.

1. Restricted cash must be reported separately on the

balance sheet.

2. Classification on balance sheet:

a. Restricted cash that is expected to be used up within a

year would be classified as a current asset.

b. Restricted cash that is not expected to be used up

within a year would be classified as a noncurrent asset.

III. Petty Cash Systems

LO 5–S1 Describe the operations of petty cash systems.

A. A petty cash system involves three steps:

1. Putting money into petty cash to establish a fund.

a. The company establishes the fund by writing a

check to the petty cash custodian; the amount of

the check equals the total estimated payments to be

made from the fund over a fairly short period.

b. Entry includes debit to Petty Cash and credit to

Cash.

Chapter Outline

Teaching Notes

2. Paying money out to reimburse others.

a. The custodian determines when to make payments

out of the cash box following policies established

by the company’s managers.

b. The custodian attaches any related documents to

the petty cash receipt and places it in the cash box.

c. Payments out of petty cash are not recorded in the

accounting system until the fund is replenished.

3. Putting money back into petty cash to replenish the

fund.

a. When the amount of cash in the cash box runs low,

the petty cash custodian asks that the fund be

replenished.

b. The amount of the check is recorded as a reduction

in Cash (with a credit), and the various items that

were paid are recorded in their corresponding

accounts (with debits).

Supplemental Enrichment Activities

Note: These activities would be suitable for individual or group activities.

1. Handout 5–1

Use Handout 5–1 for an in-class activity designed to review the preparation of a bank reconciliation.

The solution follows the handout master.

2. Handout 5–2

Use Handout 5–2 for a second in-class activity designed to review the preparation of a bank

reconciliation. The solution follows the handout master.

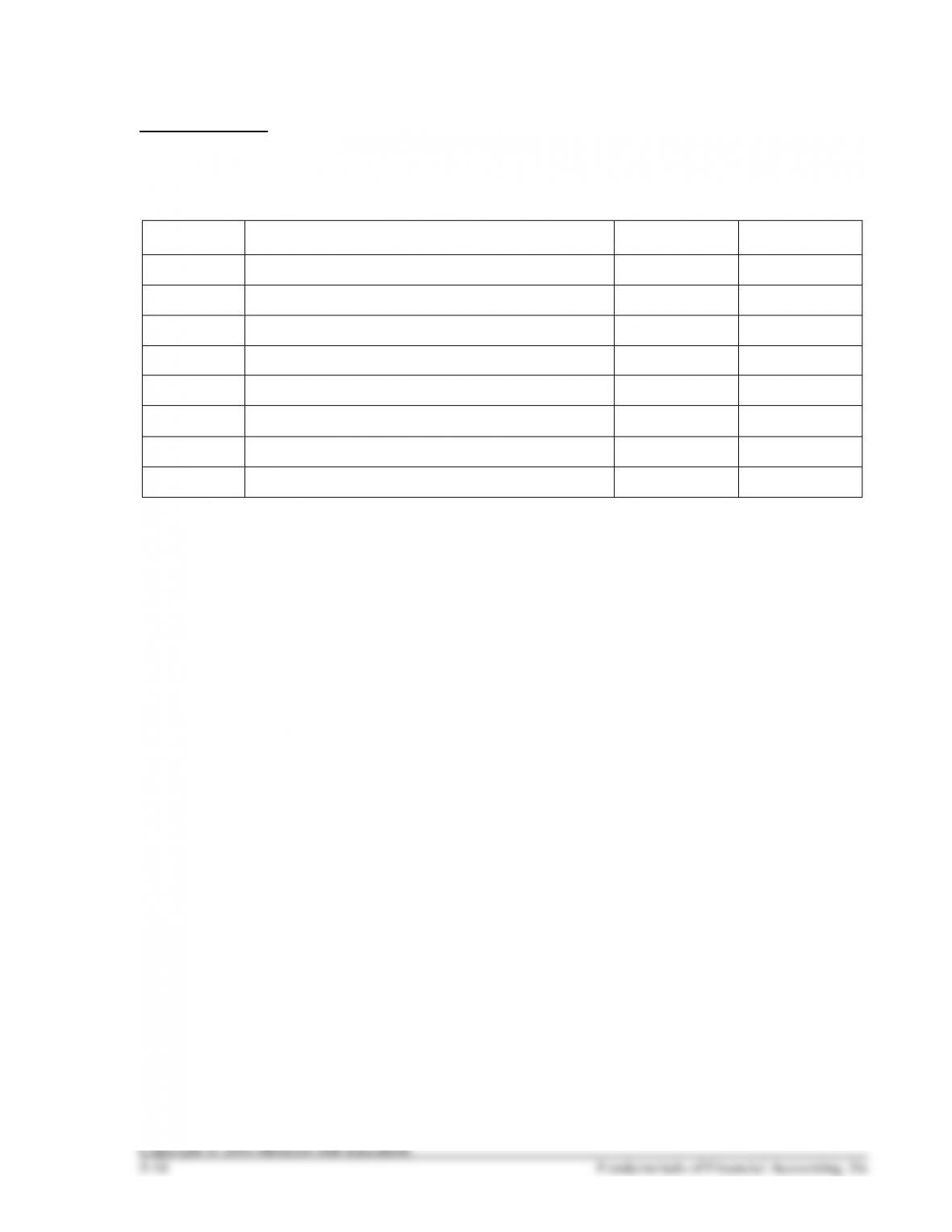

HANDOUT 5–1

BANK RECONCILIATION

Information from the records and bank statement and of Matrix, Inc. as of July 31, 2016 is set forth below

Cash balance per bank, July 31, 2016

$9,610

Cash balance per general ledger, July 31, 2016

7,430

Outstanding checks at July 31, 2016

2,417

Check mailed to the bank for deposit that had not reached the bank by July 31, 2016

500

NSF check (from a customer for a payment on account) returned by bank

281

July interest earned per bank statement

30

Check no. 781 for supplies expense cleared the bank for $240, but was erroneously

recorded in the books at $268

Deposit by Acme Company erroneously credited by the bank to our account

486

Part A

Prepare the bank reconciliation for Matrix, Inc.

HANDOUT 5–1, continued

Part B

Prepare any journal entries that should be made as a result of the bank reconciliation.

Date

Accounts

Debit

Credit