CP4–2 (continued)

Req. 2

a.

Interest Expense (+E, −SE)………………………….

700

Interest Payable (+L)…………………………

700

To accrue interest expense incurred but not paid.

b.

Unearned Revenue (−L) ………………………………………

3,200

Rent Revenue (+R, +SE) …………………………….

3,200

$4,800 ÷ 6 months = $800 per month x 4 months. This entry reduces (debits) the

liability for the amount earned and records the revenue.

c.

Accounts Receivable (+A)…………………………………….

3,300

Service Revenue (+R, +SE) …………………………

3,300

This entry records an asset for the amount due from customers and recognizes the

revenue because it was earned in 2015.

d.

Insurance Expense (+E, −SE)……………………………….

700

Prepaid Insurance (−A) ………………………………

700

$4,200 ÷ 12 months = $350 per month x 2 months of coverage. This entry reduces the

asset (Prepaid Insurance) because part of it has been used and only $3,500 represents

future benefits (an asset) to the company.

e.

Salaries and Wages Expense (+E, −SE) ………………..

1,100

Salaries and Wages Payable (+L) ………………..

1,100

Salaries and Wages Expense is increased (debited) because this expense was incurred

in 2015. A liability (Salaries and Wages Payable) is credited because this amount is

owed to the employees.

f.

Depreciation Expense (+E, −SE) …………………………...

1,000

Accumulated Depreciation–Equipment (+xA, −A)

1,000

To record depreciation for the truck for the year (amount is given).

g.

Income Tax Expense (+E, −SE) …………………………….

9,000

Income Tax Payable (+L) ………………………………

9,000

To accrue income tax expense incurred but not paid:

Income before income taxes 30,000

Income tax rate x 30%

Income tax expense $ 9,000

Fundamentals of Financial Accounting, 5/e 4–42

CP4–3

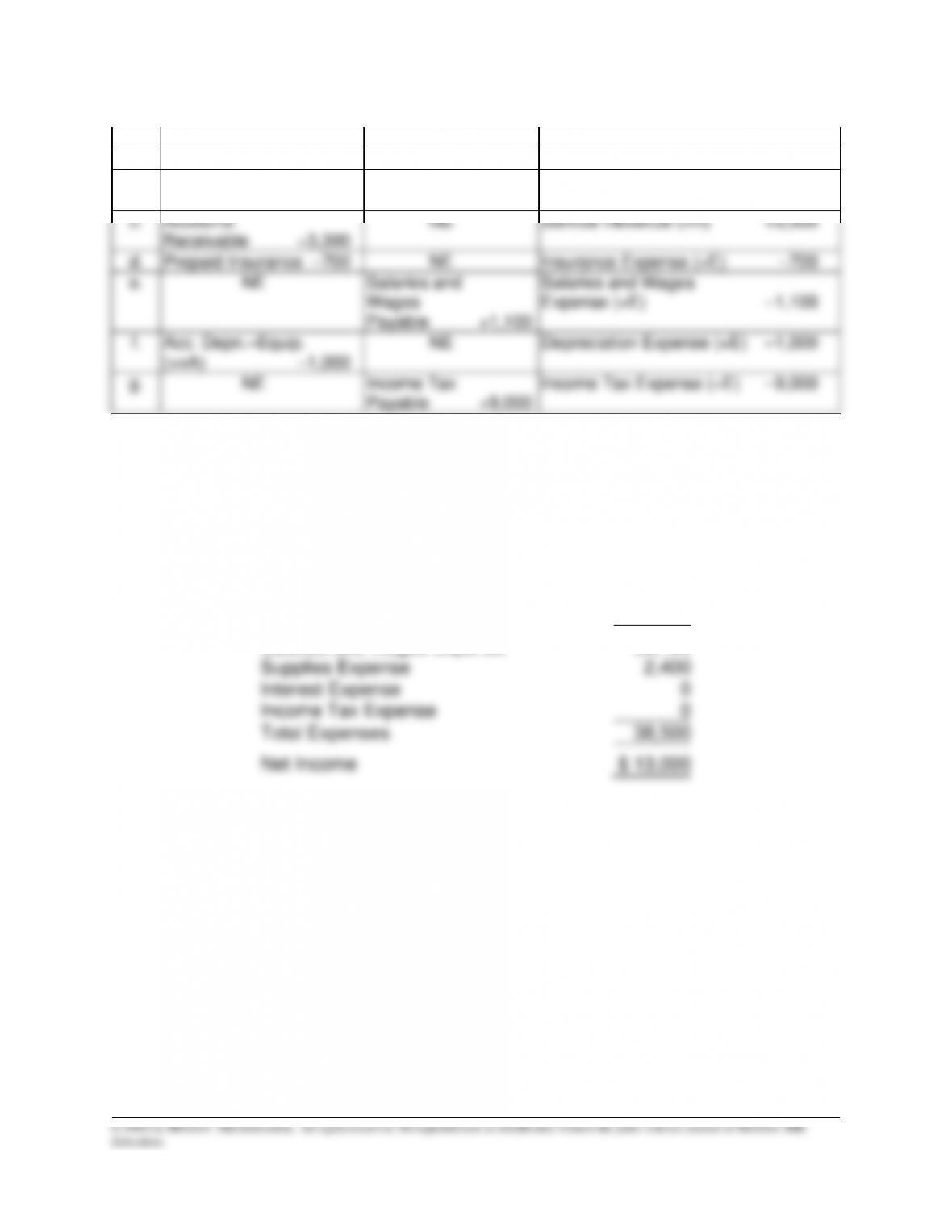

Assets

Liabilities

Stockholders’ Equity

a.

NE

Interest Payable +700

Interest Expense (+E) −700

b.

NE

Unearned

Revenue –3,200

Rent Revenue (+R) +3,200

c.

Accounts

Receivable +3,300

NE

Service Revenue (+R) +3,300

d.

Prepaid Insurance –700

NE

Insurance Expense (+E) –700

e.

NE

Salaries and

Wages

Payable +1,100

Salaries and Wages

Expense (+E) –1,100

f.

Acc. Depn.–Equip.

(+xA) –1,000

NE

Depreciation Expense (+E) –1,000

g.

NE

Income Tax

Payable +9,000

Income Tax Expense (+E) –9,000

CP4–4

Req. 1

GOLF ACADEMY, INC.

Unadjusted Income Statement

For the Year Ended December 31, 2015

Service Revenue

$ 51,500

Salaries and Wages Expense

36,100

Supplies Expense

2,400

Interest Expense

0

Income Tax Expense

0

Total Expenses

38,500

Net Income

$ 13,000

Fundamentals of Financial Accounting, 5/e 4–43

CP4–4 (continued)

Req. 2

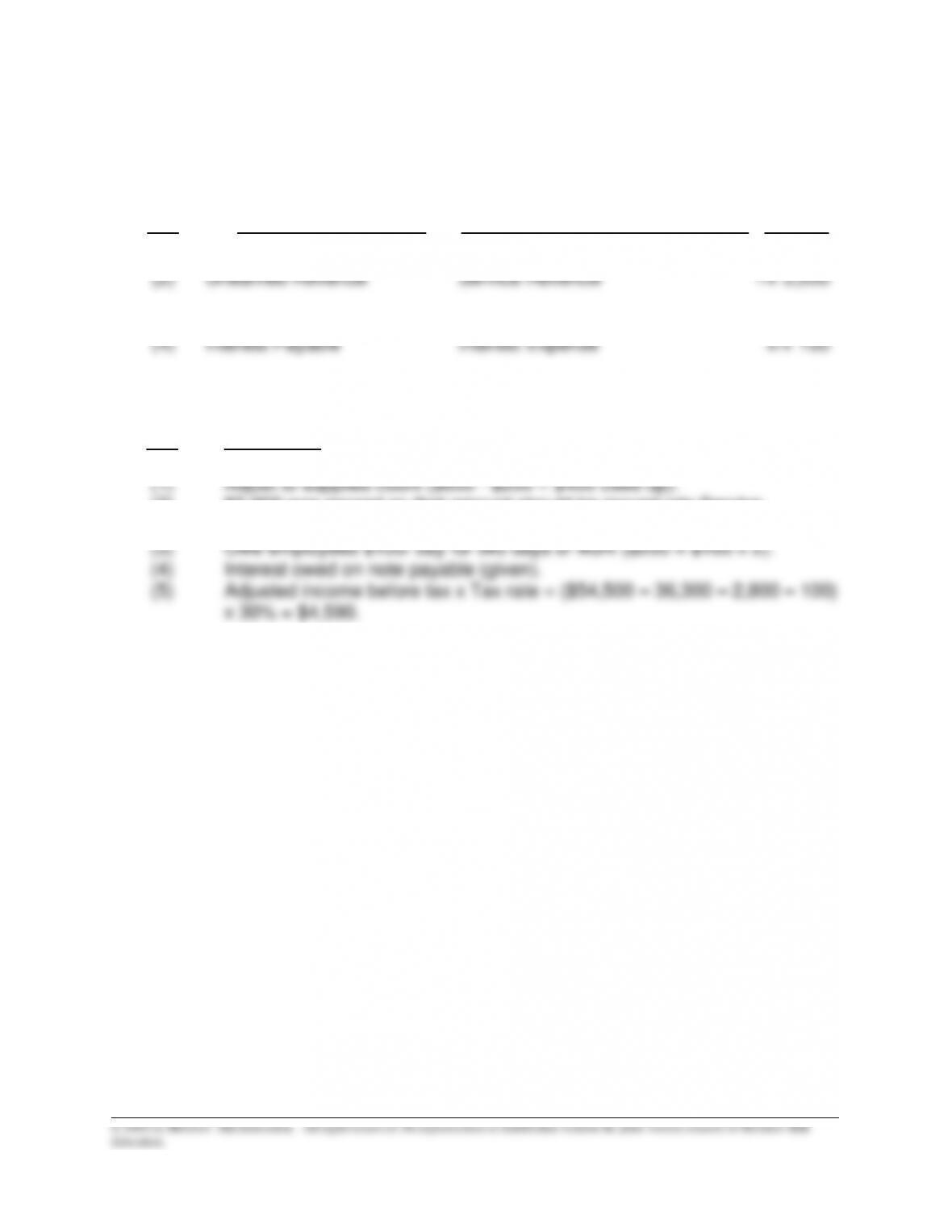

The pairs of accounts that require adjustment include:

Adj.

Balance sheet account

Related income statement account

Amount

(1)

Supplies

Supplies Expense

-/+ $ 400

(2)

Unearned Revenue

Service Revenue

-/+ 3,000

(3)

Salaries and Wages Payable

Salaries and Wages Expense

+/+ 200

(4)

Interest Payable

Interest Expense

+/+ 100

(5)

Income Tax Payable

Income Tax Expense

+/+

4,590

Adj.

Explanation

(1)

Adjust to supplies count ($600 – $200 = $400 used up).

(2)

$3,000 was earned so that amount should be moved into Service

Revenue, leaving $500 unearned.

(3)

Owe employees $100/ day for two days of work ($200 = $100 x 2).

(4)

Interest owed on note payable (given).

(5)

Adjusted income before tax x Tax rate = ($54,500 – 36,300 – 2,800 – 100)

x 30% = $4,590.

CP4–4 (continued)

Req. 3

a) Supplies Expense (+E, –SE) 400

Supplies (–A) 400

b) Unearned Revenue (–L) 3,000

Service Revenue (+R, +SE) 3,000

Fundamentals of Financial Accounting, 5/e 4–45

© 2016 by McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO GROUP A PROBLEMS

PA4–1

Req. 1 STARBOOKS CORPORATION

Adjusted Trial Balance

At September 30, 2015

Account Titles

Debit

Credit

Cash

$ 300

Accounts Receivable

300

Supplies

500

Prepaid Rent

100

Equipment

3,200

Accumulated Depreciation–Equipment

$ 900

Accounts Payable

600

Unearned Revenue

200

Note Payable (short–term)

500

Note Payable (long–term)

200

Common Stock

200

Retained Earnings

1,500

Service Revenue

6,200

Interest Revenue

100

Travel Expense

2,600

Salaries and Wages Expense

2,200

Rent Expense

400

Depreciation Expense

300

Supplies Expense

200

Income Tax Expense

300

Totals

$ 10,400

$ 10,400

PA4–1 (continued)

No. The amount to be reported for retained earnings on the balance sheet would be the

amount reported on the statement of retained earnings. The $1,500 in the adjusted trial

balance does not yet include the net income generated by Starbooks for the year ended

September 30, 2015.

Req. 2

Service Revenue (−R) ……………………………………..

6,200

Interest Revenue (−R) ……………………………………..

100

Travel Expense (−E) ……………………………….

2,600

Salaries and Wages Expense (−E) ……………

2,200

Rent Expenses (−E) ………………………………..

400

Depreciation Expense (−E) ………………………

300

Supplies Expense (−E) …………………………...

200

Income Tax Expense (−E) ……………………….

300

Retained Earnings (+SE) …………………………

300

Req. 3 STARBOOKS CORPORATION

Post–closing Trial Balance

At September 30, 2015

Account Titles

Debit

Credit

Cash

$ 300

Accounts Receivable

300

Supplies

500

Prepaid Rent

100

Equipment

3,200

Accumulated Depreciation–Equipment

$ 900

Accounts Payable

600

Unearned Revenue

200

Note Payable (short–term)

500

Note Payable (long–term)

200

Common Stock

200

Retained Earnings

1,800

Service Revenue

0

Interest Revenue

0

Travel Expense

0

Salaries and Wages Expense

0

Rent Expense

0

Depreciation Expense

0

Supplies Expense

0

Income Tax Expense

0

Totals

$ 4,400

$ 4,400

PA4–2

Req. 1

a.

Insurance Expense (+E, −SE)……………………………….

150

Prepaid Insurance (−A) …………………………..….

150

$600 x 6/24 months of coverage. This entry reduces the asset (Prepaid

Insurance), because part of it has been used and only $450 represents future

benefits (an asset) to the company.

b.

Supplies Expense (+E, −SE)…………………………………

700

Supplies (−A) …………………………………………….

700

The Supplies account is decreased (credited) to record the use of supplies during

the year, because this expense was incurred in 2015, calculated as

Unadjusted balance of $1,000 – Ending balance of $300.

c.

Repairs and Maintenance Expense (+E, −SE)…………

800

Accounts Payable (+L) ………………………………..

800

Repairs and Maintenance Expense is increased (debited) because this expense

was incurred in 2015. A liability (accounts payable) is credited, because this

amount is owed but will not be paid until 2016.

d.

Accounts Receivable (+A)…………………………………….

7,950

Service Revenue (+R, +SE) …………………………

7,950

This entry records an asset for the amount due from customers and recognizes the

revenue, because it was earned in 2015.

e.

Depreciation Expense (+E, −SE) …………………………...

2,750

Accumulated Depreciation–Equipment (+xA, −A)

2,750

To record depreciation on van for six months (amount is given).

f.

Interest Expense (+E, −SE) …………………………………..

500

Interest Payable (+L) …………………………………….

500

To accrue interest expense incurred but not paid (given).

g.

Income Tax Expense (+E, −SE) …………………………….

Income Tax Payable (+L) ………………………………

Income tax expense $ 9,000

PA4–2 (continued)

Req. 2

PA4–3

Transaction

Assets

Liabilities

Stockholders’ Equity

a.

− 150

NE

Insurance Expense (+E) − 150

b.

− 700

NE

Supplies Expense (+E) − 700

c.

NE

+ 800

Repairs & Maintenance Expense (+E) − 800

d.

+ 7,950

NE

Service Revenue (+R) + 7,950

e.

− 2,750

NE

Depreciation Expense (+E) − 2,750

f.

NE

+ 500

Interest Expense (+E) − 500

g.

NE

+ 9,000

Income Tax Expense (+E) − 9,000

PA4–4

Req. 1

VAL’S HAIR EMPORIUM

Unadjusted Income Statement (preliminary)

For the Year Ended December 31, 2015

Service Revenue

$75,800

Salaries and Wages Expense

29,100

Utilities Expense

12,200

Rent Expense

20,000

Supplies Expense

4,800

Income Tax Expense

0

Total Expenses

66,100

Net Income

$9,700

Req. 2

The pairs of accounts that require adjustment include:

Adj.

Balance sheet account

Related income statement account

Amount

(1)

Supplies

Supplies Expense

-/+ $3,000

(2)

Prepaid Rent

Rent Expense

-/+ 4,000

(3)

Accounts Payable

Utilities Expense

+/+ 450

(4)

Salaries and Wages Payable

Salaries and Wages Expense

+/+ 150

(5)

Income Taxes Payable

Income Tax Expense

+/+ 450

Adj.

Explanation

(1)

Based on supplies count ($4,300 – $1,300 = $3,000 used).

(2)

Two months of rent at $2,000/month have been used so $4,000 is expensed.

(3)

Additional $450 for utility services must be added to previously recorded

amount.

(4)

Owe stylists $150 in wages (given).

(5)

Adjusted income before tax x Tax rate =

[($75,800 – 29,250 – 12,650 – 24,000 – 7,800) x 30% = $630.

PA4–4 (continued)

Req. 3

a) Supplies Expense (+E, –SE) 3,000

Supplies (–A) 3,000

b) Rent Expense (+E, –SE) 4,000

Prepaid Rent (–A) 4,000