S4–5

The change in estimated depreciation expense will increase net income this year but

some depreciation will now extend into next year, decreasing net income then.

Although it’s true that GAAP requires the use of estimates in certain instances (such as

depreciation), the estimates should be fair and unbiased. Given the increasing

competition from online products, we must question whether DVD demand would

S4–6

Req.1

(a)

Supplies Expense (+E, −SE)…………………

4,200

Supplies (−A)……………………………….

4,200

To record supplies used ($6,000 − $1,800 = $4,200).

(b)

Insurance Expense (+E, −SE)…………………….

2,000

Prepaid Insurance (−A)……………………

2,000

To record expired insurance at December 31.

(c)

Depreciation Expense (+E, −SE)…………………

8,000

Accum. Depn–Equip (+xA, −A)…….

8,000

To record depreciation for one year.

(d)

Salaries and Wages Expense (+E,−SE)…………

2,200

Salaries and Wages Payable (+L)…………

2,200

To record salaries and wages earned but not paid.

(e)

Service Revenue (−R, −SE)..…………

7,000

Unearned Revenue (+L) ……………..

7,000

To record service revenue not earned but

collected in advance, previously recorded as earned.

(f)

Income Tax Expense (+E, −SE)……………………

3,650

Income Tax Payable (+L)……………………

3,650

To record income taxes.

Computation:

Service revenue: $85,000 − 7,000 = $78,000

Expenses: $47,000 + 4,200 + 2,000 + 8,000 + 2,200 = 63,400

Net income before taxes $14,600

Income tax expense: $14,600 x 25% = $ 3,650

Fundamentals of Financial Accounting, 5/e 4–101

S4–6 (continued)

Req. 2 PIRATE PETE MOVING CORPORATION

Corrections to the Financial Statements

Amounts

Reported

Changes

Plus Minus

Correct

Amounts

Income Statement:

Revenue:

Service Revenue

$ 85,000

e

7,000

$ 78,000

Expenses:

Salaries and Wages Expense

17,000

d

2,200

19,200

Supplies Expense

12,000

a

4,200

16,200

Other Expenses

18,000

18,000

Insurance Expense

0

b

2,000

2,000

Depreciation Expense

0

c

8,000

8,000

Income Tax Expense

0

f

3,650

3,650

Total Expenses

47,000

67,050

Net Income

$ 38,000

$ 10,950

December 31 Balance Sheet

Assets:

Current Assets:

Cash

$ 2,000

$ 2,000

Receivables

3,000

3,000

Supplies

6,000

a

4,200

1,800

Prepaid Insurance

4,000

b

2,000

2,000

Total Current Assets

15,000

8,800

Equipment

40,000

40,000

Accumulated Depn.

0

c

8,000

(8,000)

Remaining Assets

27,000

27,000

Total Assets

$ 82,000

$ 67,800

Liabilities:

Current Liabilities:

Accounts Payable

$ 9,000

$ 9,000

Salaries and Wages Payable

0

d

2,200

2,200

Unearned Revenue

0

e

7,000

7,000

Income Tax Payable

0

f

3,650

3,650

Total Current Liabilities

9,000

21,850

Stockholders’ Equity:

Common Stock

35,000

35,000

Retained Earnings

38,000

10,950

Total Stockholders’ Equity

73,000

45,950

Total Liab. and Stockholders’ Equity

$ 82,000

$ 67,800

S4–6 (continued)

Req.3

(a) Decrease Net Income by $27,050.

(b) Decrease Total Assets by $14,200.

Req. 4

(today’s date)

Fundamentals of Financial Accounting, 5/e 4–103

© 2016 by McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

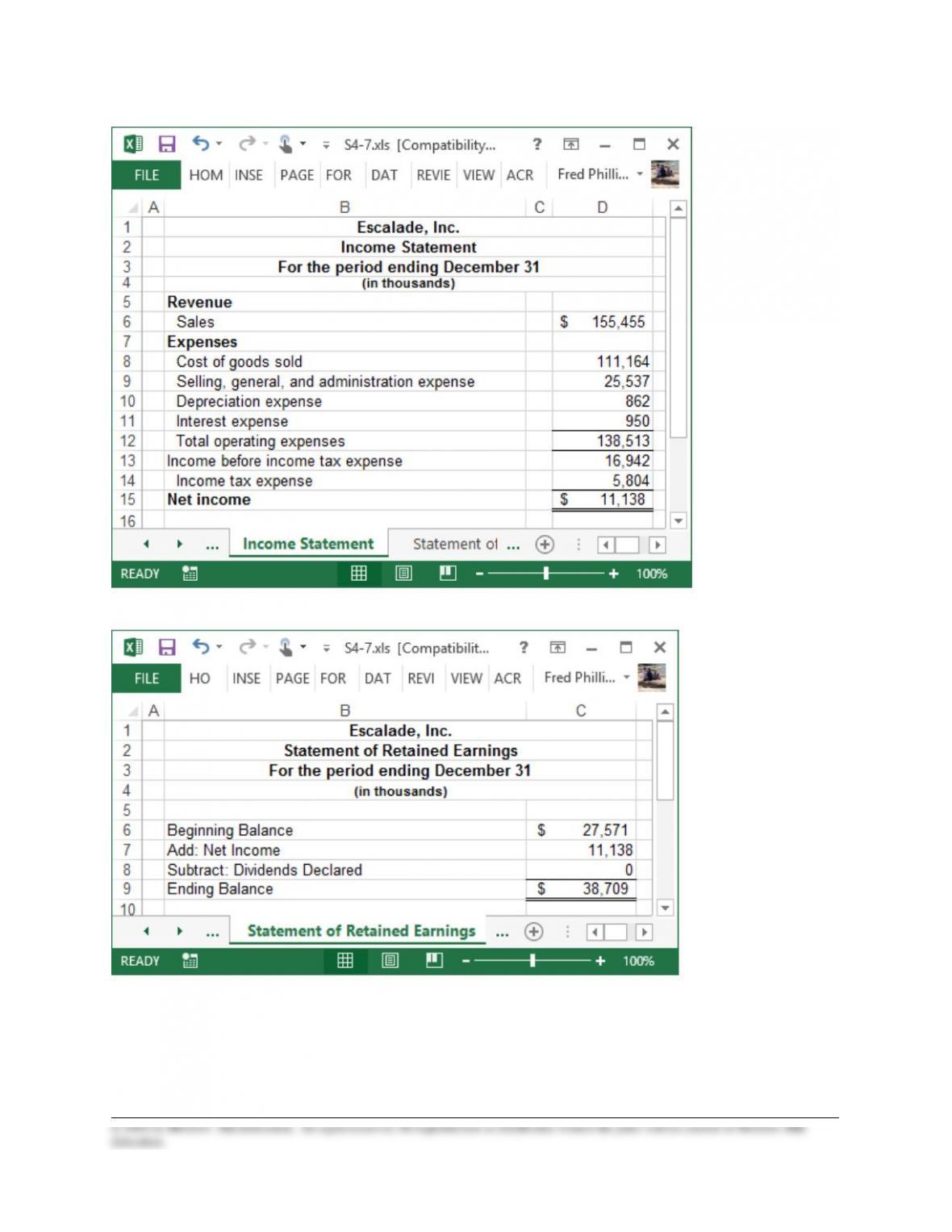

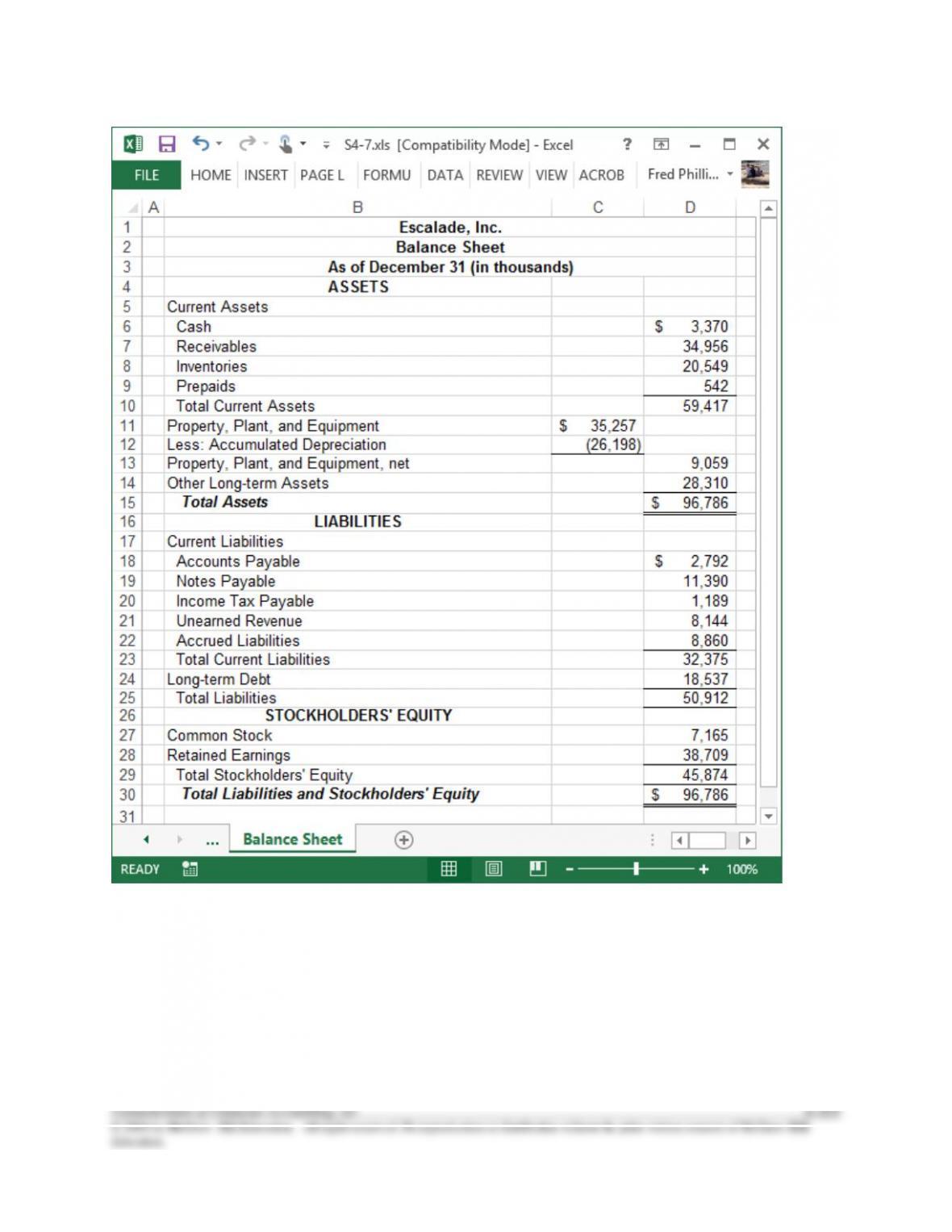

S4–7

Fundamentals of Financial Accounting, 5/e 4–104

S4–7 (continued)

S4–7 (continued)

Fundamentals of Financial Accounting, 5/e 4–106

© 2016 by McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO CONTINUING CASE

CC–4

Req. 1

a) Deferral

b) Deferral

c) Accrual

d) Deferral

e) Deferral

f) Deferral

Req. 2

a)

Prepaid Rent (+A)…………………………………..

Cash (–A)…………………………………………

4,800

4,800

b)

Building (+A)……………..…………………………....….

Cash (–A)…………………………………………

47,000

47,000

c)

This requires an accrual adjustment (see requirement 3).

d)

Prepaid Insurance (+A)…………………………….

Cash (–A)…………………………………………

3,000

3,000

e)

Supplies (+A)………………………………………..

Accounts Payable (+L)…………………………

2,000

2,000

f)

Cash (+A)……………………………………………

Unearned Revenue (+L)……………………….

90

90

Req. 3

a)

Rent Expense (+E, –SE)…………………………..

Prepaid Rent (–A)………………………………

(4/8 x $4,800)

2,400

2,400

b)

Depreciation Expense (+E, –SE)………………….

Accum. Depn.–Equip. (+xA, –A)………………

2,000

2,000

c)

Salaries and Wages Expense (+E, –SE).…….…..

Salaries and Wages Payable (+L)………..…..

($1,000 x 2)

2,000

2,000

d)

Insurance Expense (+E, –SE)…………………….

Prepaid Insurance (–A)…………………………

(7/12 x 3,000)

1,750

1,750

e)

Supplies Expense (+E, –SE)……………………...

Supplies (–A)……………………………………

($2,000 – $700)

1,300

1,300

f)

Unearned Revenue (–L)…………………………..

Service Revenue (+R, +SE)…………………..

90

90